Key Insights

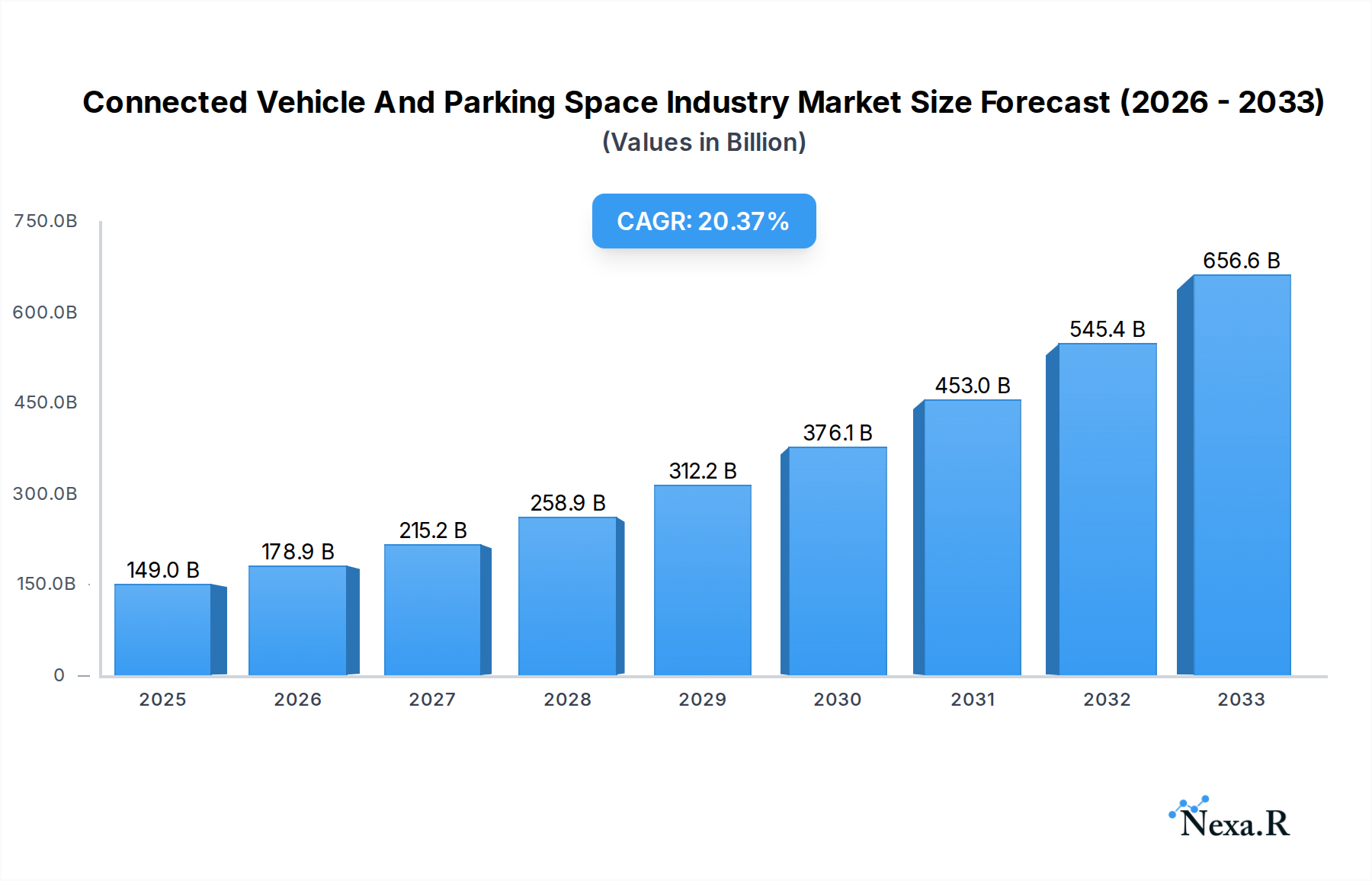

The Connected Vehicle and Parking Space Industry is poised for remarkable expansion, driven by the accelerating integration of smart technologies in transportation. With a current market size of $149.03 billion in 2025, the industry is projected to experience a robust compound annual growth rate (CAGR) of 19.2%, reaching significant value by 2033. This impressive growth is fueled by several key drivers. The increasing adoption of connected vehicle technologies, including V2X (Vehicle-to-Everything) communication, is transforming how vehicles interact with their environment, especially parking infrastructure. Government initiatives promoting smart cities and sustainable urban development are further bolstering this trend. Moreover, the growing demand for seamless parking experiences, driven by urbanization and the proliferation of private vehicles, necessitates intelligent parking solutions. The convenience of finding and paying for parking through connected car interfaces or mobile applications is a major consumer attraction, leading to a surge in demand for both on-street and off-street smart parking systems.

Connected Vehicle And Parking Space Industry Market Size (In Billion)

The market's segmentation reveals a diverse landscape catering to various needs. Passenger cars dominate the vehicle type segment due to their sheer volume, but commercial vehicles are increasingly adopting connected parking solutions for operational efficiency. Off-street parking, encompassing both regulated and unregulated spaces, is a significant area of growth, particularly private properties like residential and work locations. Trends indicate a strong shift towards automated and sensor-based parking management, real-time availability data, and integrated payment systems. While the industry is experiencing substantial growth, potential restraints include high initial investment costs for infrastructure deployment, data security and privacy concerns, and the need for standardization across different platforms and regions. Leading players such as Swarco AG, Q-Free ASA, and major automotive manufacturers like Volkswagen AG and BMW AG are actively investing in research and development to capture market share and drive innovation.

Connected Vehicle And Parking Space Industry Company Market Share

Connected Vehicle and Parking Space Industry Market Dynamics & Structure

The Connected Vehicle and Parking Space industry is experiencing a dynamic evolution, driven by the synergistic integration of advanced automotive technologies and smart urban infrastructure. Market concentration is moderate, with key players like Volkswagen AG, BMW AG, Mercedes-Benz AG, and Audi AG leading in connected vehicle development, while Swarco AG, Q-Free ASA, and Amano Inc. are prominent in parking solutions. Technological innovation is the primary growth engine, with advancements in Artificial Intelligence (AI), the Internet of Things (IoT), and 5G communication enabling sophisticated parking assistance, automated parking, and seamless vehicle-to-infrastructure (V2I) communication. Regulatory frameworks are increasingly supporting the deployment of connected and autonomous technologies, though standardization remains a challenge. Competitive product substitutes include traditional parking meters and manual parking guidance systems, which are rapidly being outpaced by smarter, integrated solutions. End-user demographics are shifting towards tech-savvy urban dwellers and businesses seeking efficiency and convenience. Mergers and Acquisitions (M&A) activity is on the rise as companies aim to consolidate their market positions and acquire complementary technologies.

- Market Concentration: Moderate, with a blend of large automotive manufacturers and specialized technology providers.

- Technological Drivers: AI for navigation and parking, IoT for real-time data exchange, 5G for low-latency communication.

- Regulatory Frameworks: Evolving to support connected and autonomous driving, with a focus on safety and data privacy.

- Competitive Substitutes: Traditional parking meters, manual guidance systems.

- End-User Demographics: Urban professionals, fleet operators, smart city initiatives.

- M&A Trends: Increasing consolidation to enhance technological capabilities and market reach.

Connected Vehicle and Parking Space Industry Growth Trends & Insights

The Connected Vehicle and Parking Space industry is poised for substantial growth, projected to reach an estimated value of $XXX billion by 2033, with a compound annual growth rate (CAGR) of XX.X% during the forecast period of 2025–2033. This robust expansion is fueled by a confluence of factors, including the escalating adoption of connected car technologies, the burgeoning demand for intelligent parking solutions, and supportive governmental initiatives aimed at creating smarter, more efficient urban environments. The market size has witnessed a steady increase from an estimated $XXX billion in the base year of 2025, reflecting a significant upward trajectory. Adoption rates for connected parking features are accelerating, driven by the perceived benefits of reduced search time for parking, improved traffic flow, and enhanced user experience. Technological disruptions, such as the advancement of autonomous driving capabilities and the proliferation of sensors, are fundamentally reshaping how vehicles interact with parking infrastructure. Consumer behavior is also shifting, with a growing preference for app-based parking services, real-time availability information, and integrated payment systems. The integration of Vehicle-to-Everything (V2X) communication is a key disruptor, enabling vehicles to not only locate parking but also communicate with other vehicles and infrastructure to optimize parking availability and traffic management. The increasing complexity of urban landscapes and the growing number of vehicles on the road necessitate these smart solutions. The market penetration of these technologies is expected to deepen considerably as costs decrease and awareness increases. Furthermore, the growing focus on sustainability and efficient resource utilization in urban planning is providing further impetus for the adoption of connected parking systems. These systems contribute to reduced emissions by minimizing unnecessary vehicle idling while searching for parking. The report delves into granular details of market evolution, examining how each segment contributes to the overall growth narrative, and explores the impact of emerging technologies like AI-powered parking analytics and blockchain for secure parking transactions.

Dominant Regions, Countries, or Segments in Connected Vehicle and Parking Space Industry

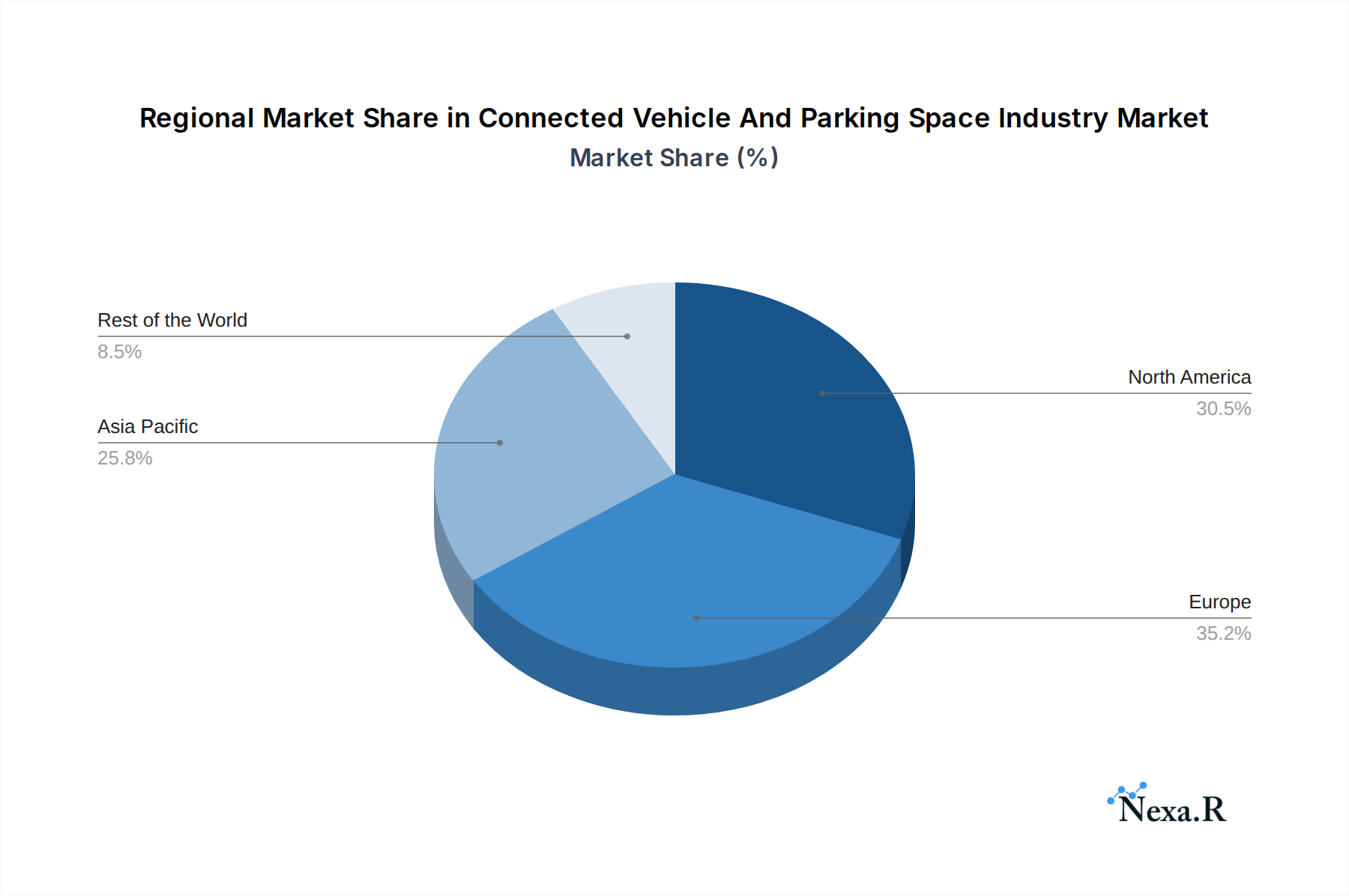

North America and Europe currently stand as the dominant regions in the Connected Vehicle and Parking Space industry, driven by a mature automotive market, strong government support for smart city initiatives, and a high consumer propensity for adopting advanced technologies. Within these regions, countries like the United States, Germany, and the United Kingdom are leading the charge due to substantial investments in smart infrastructure and a robust presence of key industry players.

The Passenger Car segment within Vehicle Type is a primary driver of market growth. These vehicles are equipped with increasingly sophisticated connected features, including advanced driver-assistance systems (ADAS) that integrate parking functionalities. The demand for convenience and reduced driving stress among passenger car owners directly translates into higher adoption rates for smart parking solutions.

In terms of Parking Category, Off-Street parking, particularly Off-street purpose-built regulated parking, exhibits significant dominance. This is due to the concentration of commercial and residential complexes that benefit most from integrated smart parking management systems, offering features like pre-booking, automated payment, and real-time occupancy monitoring. The development of multi-story car parks and intelligent parking garages is a key factor in this segment's growth.

Among Parking Space categories, Residential and Work Private Property is a significant contributor, with smart parking solutions being integrated into new developments and retrofitted in existing ones to manage private parking assets more efficiently. However, Non-regulated Public Access and Off-street open-air barrier regulated parking spaces are also seeing increased adoption of connected technologies as cities strive to optimize public parking availability and revenue generation.

Key drivers for this regional and segmental dominance include:

- Government Initiatives: Strong backing for smart city development, V2X deployment, and autonomous vehicle testing.

- Infrastructure Development: Significant investments in 5G networks, intelligent traffic management systems, and smart parking infrastructure.

- Consumer Demand: High awareness and willingness to adopt technologies that offer convenience, efficiency, and time savings.

- Presence of Key Players: Concentration of major automotive manufacturers and technology providers focusing on R&D and market penetration.

- Economic Policies: Favorable policies encouraging technological innovation and investment in smart urban solutions.

The market share in these dominant segments is substantial, with the passenger car segment alone accounting for over 70% of the connected vehicle market. Off-street regulated parking is projected to capture over 60% of the smart parking market share by 2030. The growth potential in these areas is immense, driven by the ongoing technological advancements and the increasing urbanization trends globally.

Connected Vehicle and Parking Space Industry Product Landscape

The product landscape for the Connected Vehicle and Parking Space industry is characterized by innovation in intelligent parking assistance systems, automated valet parking, and seamless integration of vehicle and parking infrastructure. Key product innovations include advanced sensors and camera systems that enable vehicles to detect parking spaces autonomously, navigate tight spots, and execute parking maneuvers with precision. Smart parking management platforms are also a critical component, offering real-time occupancy data, dynamic pricing, and reservation capabilities for parking facilities. Furthermore, mobile applications are revolutionizing the user experience, allowing drivers to locate, book, and pay for parking remotely. Performance metrics focus on efficiency, accuracy, and user convenience, with an emphasis on reducing parking search times and improving traffic flow in urban areas. Unique selling propositions lie in the seamless integration of vehicle capabilities with parking infrastructure, creating an end-to-end smart parking ecosystem. Technological advancements are continuously pushing the boundaries, with AI playing an increasingly vital role in optimizing parking allocation and predictive maintenance of parking facilities.

Key Drivers, Barriers & Challenges in Connected Vehicle and Parking Space Industry

The Connected Vehicle and Parking Space industry is propelled by several key drivers, including the escalating demand for convenience and efficiency in urban mobility, the rapid advancements in automotive technology like AI and IoT, and growing government support for smart city initiatives. The integration of connected vehicles with smart parking infrastructure promises to alleviate traffic congestion and reduce carbon emissions by optimizing parking search times.

However, the industry faces significant barriers and challenges. High initial investment costs for smart parking infrastructure and connected vehicle technologies can be a deterrent for widespread adoption, particularly in developing economies. Cybersecurity concerns related to data privacy and the potential for hacking into connected systems pose a critical threat. Regulatory fragmentation and a lack of standardized protocols across different regions and municipalities can hinder seamless interoperability. Furthermore, public perception and trust in autonomous parking technologies require continuous effort to build. Supply chain disruptions and the availability of skilled labor for installation and maintenance also present ongoing challenges.

Emerging Opportunities in Connected Vehicle and Parking Space Industry

Emerging opportunities in the Connected Vehicle and Parking Space industry are diverse and rapidly expanding. The integration of electric vehicle (EV) charging infrastructure within smart parking solutions presents a significant growth avenue, catering to the surging EV market. The application of AI and machine learning for predictive parking analytics, optimizing space utilization, and dynamic pricing models offers substantial value to operators and users alike. Untapped markets in developing economies, with their rapidly urbanizing populations, represent a vast potential for smart parking solutions. The development of integrated mobility platforms that combine ride-sharing, public transport, and smart parking services offers a holistic approach to urban transportation challenges. Evolving consumer preferences for seamless, touchless, and personalized parking experiences are creating demand for innovative, user-centric solutions.

Growth Accelerators in the Connected Vehicle and Parking Space Industry Industry

The long-term growth of the Connected Vehicle and Parking Space industry is being significantly accelerated by several catalysts. Technological breakthroughs in autonomous driving, sensor fusion, and V2X communication are enabling more sophisticated and reliable parking solutions. Strategic partnerships between automotive manufacturers, technology providers, and urban developers are fostering integrated ecosystems and accelerating product development. Market expansion strategies focusing on emerging economies, where the need for efficient urban mobility solutions is paramount, are opening new avenues for growth. Furthermore, increasing government incentives and favorable policies aimed at promoting smart city development and sustainable transportation are creating a conducive environment for sustained expansion. The growing adoption of subscription-based models for smart parking services is also expected to drive recurring revenue and market penetration.

Key Players Shaping the Connected Vehicle and Parking Space Industry Market

- Swarco AG

- Q-Free ASA

- Wohr Parking Systems Pvt Lt

- Volkswagen AG

- Amano Inc

- Hyundai Motor Company

- BMW AG

- Tesla Inc

- Mercedes-Benz AG

- Audi AG

- Honda Motor Company

- GROUP Indigo

- 6 3 Parking Space Providers

Notable Milestones in Connected Vehicle and Parking Space Industry Sector

- August 2023: Mercedes-Benz introduced highly automated and driverless parking (SAE Level 4) in its EQE Saloon with the Remote Parking Package and the Mercedes Me connect service Intelligent Park Pilot.

- May 2023: Continental AG announced the integration of Imagry's technology into its Autonomous Driving (AD) platform to support automated parking for passenger vehicles. The technology will assist in both covered parking garages and uncovered parking lots, allowing vehicles to explore parking lots, detect suitable spaces, and park without driver intervention.

In-Depth Connected Vehicle and Parking Space Industry Market Outlook

The future outlook for the Connected Vehicle and Parking Space industry is exceptionally bright, driven by the relentless pursuit of urban efficiency and enhanced mobility experiences. Growth accelerators, including advancements in AI-powered parking analytics and the widespread adoption of electric vehicle charging within parking facilities, are setting the stage for a transformative period. Strategic partnerships between key industry players and municipal authorities will be pivotal in expanding smart parking infrastructure and fostering interoperability. The increasing demand for integrated mobility solutions, encompassing everything from parking reservations to seamless payment, will fuel innovation and market penetration. As cities worldwide prioritize sustainability and smart urban development, the adoption of connected vehicle and parking technologies will become not just a convenience, but a necessity, unlocking significant future market potential and creating a more fluid and efficient urban landscape for all.

Connected Vehicle And Parking Space Industry Segmentation

-

1. Vehicle Type

- 1.1. Passenger Car

- 1.2. Commercial Vehicles

-

2. Parking Category

- 2.1. Off-Street

- 2.2. On-Street

-

3. Parking Space

- 3.1. Residential and Work Private Property

- 3.2. Non-regulated Public Access

- 3.3. Off-street open-air barrier regulated

- 3.4. Off-street purpose built regulated

Connected Vehicle And Parking Space Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Rest of North America

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Spain

- 2.5. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. India

- 3.3. Japan

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

-

4. Rest of the World

- 4.1. South America

- 4.2. Middle East and Africa

Connected Vehicle And Parking Space Industry Regional Market Share

Geographic Coverage of Connected Vehicle And Parking Space Industry

Connected Vehicle And Parking Space Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 19.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Passenger Car

- 5.1.2. Commercial Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Parking Category

- 5.2.1. Off-Street

- 5.2.2. On-Street

- 5.3. Market Analysis, Insights and Forecast - by Parking Space

- 5.3.1. Residential and Work Private Property

- 5.3.2. Non-regulated Public Access

- 5.3.3. Off-street open-air barrier regulated

- 5.3.4. Off-street purpose built regulated

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. Global Connected Vehicle And Parking Space Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.1.1. Passenger Car

- 6.1.2. Commercial Vehicles

- 6.2. Market Analysis, Insights and Forecast - by Parking Category

- 6.2.1. Off-Street

- 6.2.2. On-Street

- 6.3. Market Analysis, Insights and Forecast - by Parking Space

- 6.3.1. Residential and Work Private Property

- 6.3.2. Non-regulated Public Access

- 6.3.3. Off-street open-air barrier regulated

- 6.3.4. Off-street purpose built regulated

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7. North America Connected Vehicle And Parking Space Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7.1.1. Passenger Car

- 7.1.2. Commercial Vehicles

- 7.2. Market Analysis, Insights and Forecast - by Parking Category

- 7.2.1. Off-Street

- 7.2.2. On-Street

- 7.3. Market Analysis, Insights and Forecast - by Parking Space

- 7.3.1. Residential and Work Private Property

- 7.3.2. Non-regulated Public Access

- 7.3.3. Off-street open-air barrier regulated

- 7.3.4. Off-street purpose built regulated

- 7.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 8. Europe Connected Vehicle And Parking Space Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 8.1.1. Passenger Car

- 8.1.2. Commercial Vehicles

- 8.2. Market Analysis, Insights and Forecast - by Parking Category

- 8.2.1. Off-Street

- 8.2.2. On-Street

- 8.3. Market Analysis, Insights and Forecast - by Parking Space

- 8.3.1. Residential and Work Private Property

- 8.3.2. Non-regulated Public Access

- 8.3.3. Off-street open-air barrier regulated

- 8.3.4. Off-street purpose built regulated

- 8.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 9. Asia Pacific Connected Vehicle And Parking Space Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 9.1.1. Passenger Car

- 9.1.2. Commercial Vehicles

- 9.2. Market Analysis, Insights and Forecast - by Parking Category

- 9.2.1. Off-Street

- 9.2.2. On-Street

- 9.3. Market Analysis, Insights and Forecast - by Parking Space

- 9.3.1. Residential and Work Private Property

- 9.3.2. Non-regulated Public Access

- 9.3.3. Off-street open-air barrier regulated

- 9.3.4. Off-street purpose built regulated

- 9.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 10. Rest of the World Connected Vehicle And Parking Space Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 10.1.1. Passenger Car

- 10.1.2. Commercial Vehicles

- 10.2. Market Analysis, Insights and Forecast - by Parking Category

- 10.2.1. Off-Street

- 10.2.2. On-Street

- 10.3. Market Analysis, Insights and Forecast - by Parking Space

- 10.3.1. Residential and Work Private Property

- 10.3.2. Non-regulated Public Access

- 10.3.3. Off-street open-air barrier regulated

- 10.3.4. Off-street purpose built regulated

- 10.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Swarco AG

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Q-Free ASA

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Wohr Parking Systems Pvt Lt

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Volkswagen AG

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Amano Inc

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Hyundai Motor Company

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 BMW AG

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Tesla Inc

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Mercedes-Benz AG

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Audi AG

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 Honda Motor Company6 3 Parking Space Providers

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 GROUP Indigo

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.1 Swarco AG

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Connected Vehicle And Parking Space Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Connected Vehicle And Parking Space Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 3: North America Connected Vehicle And Parking Space Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 4: North America Connected Vehicle And Parking Space Industry Revenue (billion), by Parking Category 2025 & 2033

- Figure 5: North America Connected Vehicle And Parking Space Industry Revenue Share (%), by Parking Category 2025 & 2033

- Figure 6: North America Connected Vehicle And Parking Space Industry Revenue (billion), by Parking Space 2025 & 2033

- Figure 7: North America Connected Vehicle And Parking Space Industry Revenue Share (%), by Parking Space 2025 & 2033

- Figure 8: North America Connected Vehicle And Parking Space Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: North America Connected Vehicle And Parking Space Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Connected Vehicle And Parking Space Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 11: Europe Connected Vehicle And Parking Space Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 12: Europe Connected Vehicle And Parking Space Industry Revenue (billion), by Parking Category 2025 & 2033

- Figure 13: Europe Connected Vehicle And Parking Space Industry Revenue Share (%), by Parking Category 2025 & 2033

- Figure 14: Europe Connected Vehicle And Parking Space Industry Revenue (billion), by Parking Space 2025 & 2033

- Figure 15: Europe Connected Vehicle And Parking Space Industry Revenue Share (%), by Parking Space 2025 & 2033

- Figure 16: Europe Connected Vehicle And Parking Space Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: Europe Connected Vehicle And Parking Space Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Connected Vehicle And Parking Space Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 19: Asia Pacific Connected Vehicle And Parking Space Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 20: Asia Pacific Connected Vehicle And Parking Space Industry Revenue (billion), by Parking Category 2025 & 2033

- Figure 21: Asia Pacific Connected Vehicle And Parking Space Industry Revenue Share (%), by Parking Category 2025 & 2033

- Figure 22: Asia Pacific Connected Vehicle And Parking Space Industry Revenue (billion), by Parking Space 2025 & 2033

- Figure 23: Asia Pacific Connected Vehicle And Parking Space Industry Revenue Share (%), by Parking Space 2025 & 2033

- Figure 24: Asia Pacific Connected Vehicle And Parking Space Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Asia Pacific Connected Vehicle And Parking Space Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Rest of the World Connected Vehicle And Parking Space Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 27: Rest of the World Connected Vehicle And Parking Space Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 28: Rest of the World Connected Vehicle And Parking Space Industry Revenue (billion), by Parking Category 2025 & 2033

- Figure 29: Rest of the World Connected Vehicle And Parking Space Industry Revenue Share (%), by Parking Category 2025 & 2033

- Figure 30: Rest of the World Connected Vehicle And Parking Space Industry Revenue (billion), by Parking Space 2025 & 2033

- Figure 31: Rest of the World Connected Vehicle And Parking Space Industry Revenue Share (%), by Parking Space 2025 & 2033

- Figure 32: Rest of the World Connected Vehicle And Parking Space Industry Revenue (billion), by Country 2025 & 2033

- Figure 33: Rest of the World Connected Vehicle And Parking Space Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Connected Vehicle And Parking Space Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 2: Global Connected Vehicle And Parking Space Industry Revenue billion Forecast, by Parking Category 2020 & 2033

- Table 3: Global Connected Vehicle And Parking Space Industry Revenue billion Forecast, by Parking Space 2020 & 2033

- Table 4: Global Connected Vehicle And Parking Space Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Global Connected Vehicle And Parking Space Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 6: Global Connected Vehicle And Parking Space Industry Revenue billion Forecast, by Parking Category 2020 & 2033

- Table 7: Global Connected Vehicle And Parking Space Industry Revenue billion Forecast, by Parking Space 2020 & 2033

- Table 8: Global Connected Vehicle And Parking Space Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: United States Connected Vehicle And Parking Space Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Canada Connected Vehicle And Parking Space Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Rest of North America Connected Vehicle And Parking Space Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Global Connected Vehicle And Parking Space Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 13: Global Connected Vehicle And Parking Space Industry Revenue billion Forecast, by Parking Category 2020 & 2033

- Table 14: Global Connected Vehicle And Parking Space Industry Revenue billion Forecast, by Parking Space 2020 & 2033

- Table 15: Global Connected Vehicle And Parking Space Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Germany Connected Vehicle And Parking Space Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: United Kingdom Connected Vehicle And Parking Space Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: France Connected Vehicle And Parking Space Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Spain Connected Vehicle And Parking Space Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Rest of Europe Connected Vehicle And Parking Space Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Global Connected Vehicle And Parking Space Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 22: Global Connected Vehicle And Parking Space Industry Revenue billion Forecast, by Parking Category 2020 & 2033

- Table 23: Global Connected Vehicle And Parking Space Industry Revenue billion Forecast, by Parking Space 2020 & 2033

- Table 24: Global Connected Vehicle And Parking Space Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 25: China Connected Vehicle And Parking Space Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: India Connected Vehicle And Parking Space Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Japan Connected Vehicle And Parking Space Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: South Korea Connected Vehicle And Parking Space Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: Rest of Asia Pacific Connected Vehicle And Parking Space Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Global Connected Vehicle And Parking Space Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 31: Global Connected Vehicle And Parking Space Industry Revenue billion Forecast, by Parking Category 2020 & 2033

- Table 32: Global Connected Vehicle And Parking Space Industry Revenue billion Forecast, by Parking Space 2020 & 2033

- Table 33: Global Connected Vehicle And Parking Space Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 34: South America Connected Vehicle And Parking Space Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: Middle East and Africa Connected Vehicle And Parking Space Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Connected Vehicle And Parking Space Industry?

The projected CAGR is approximately 19.2%.

2. Which companies are prominent players in the Connected Vehicle And Parking Space Industry?

Key companies in the market include Swarco AG, Q-Free ASA, Wohr Parking Systems Pvt Lt, Volkswagen AG, Amano Inc, Hyundai Motor Company, BMW AG, Tesla Inc, Mercedes-Benz AG, Audi AG, Honda Motor Company6 3 Parking Space Providers, GROUP Indigo.

3. What are the main segments of the Connected Vehicle And Parking Space Industry?

The market segments include Vehicle Type, Parking Category, Parking Space.

4. Can you provide details about the market size?

The market size is estimated to be USD 149.03 billion as of 2022.

5. What are some drivers contributing to market growth?

Rise in demand for Advanced Comfort Systems In Vehicles.

6. What are the notable trends driving market growth?

Connected Passenger Car Vehicle Market is Expected to Grow Significantly.

7. Are there any restraints impacting market growth?

High Cost Assoicated with Advanced Features.

8. Can you provide examples of recent developments in the market?

August 2023: Mercedes-Benz introduced highly automated and driverless parking (SAE Level 4) in EQE Saloon with the Remote Parking Package and the Mercedes Me connect to service Intelligent Park Pilot.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Connected Vehicle And Parking Space Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Connected Vehicle And Parking Space Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Connected Vehicle And Parking Space Industry?

To stay informed about further developments, trends, and reports in the Connected Vehicle And Parking Space Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence