Key Insights

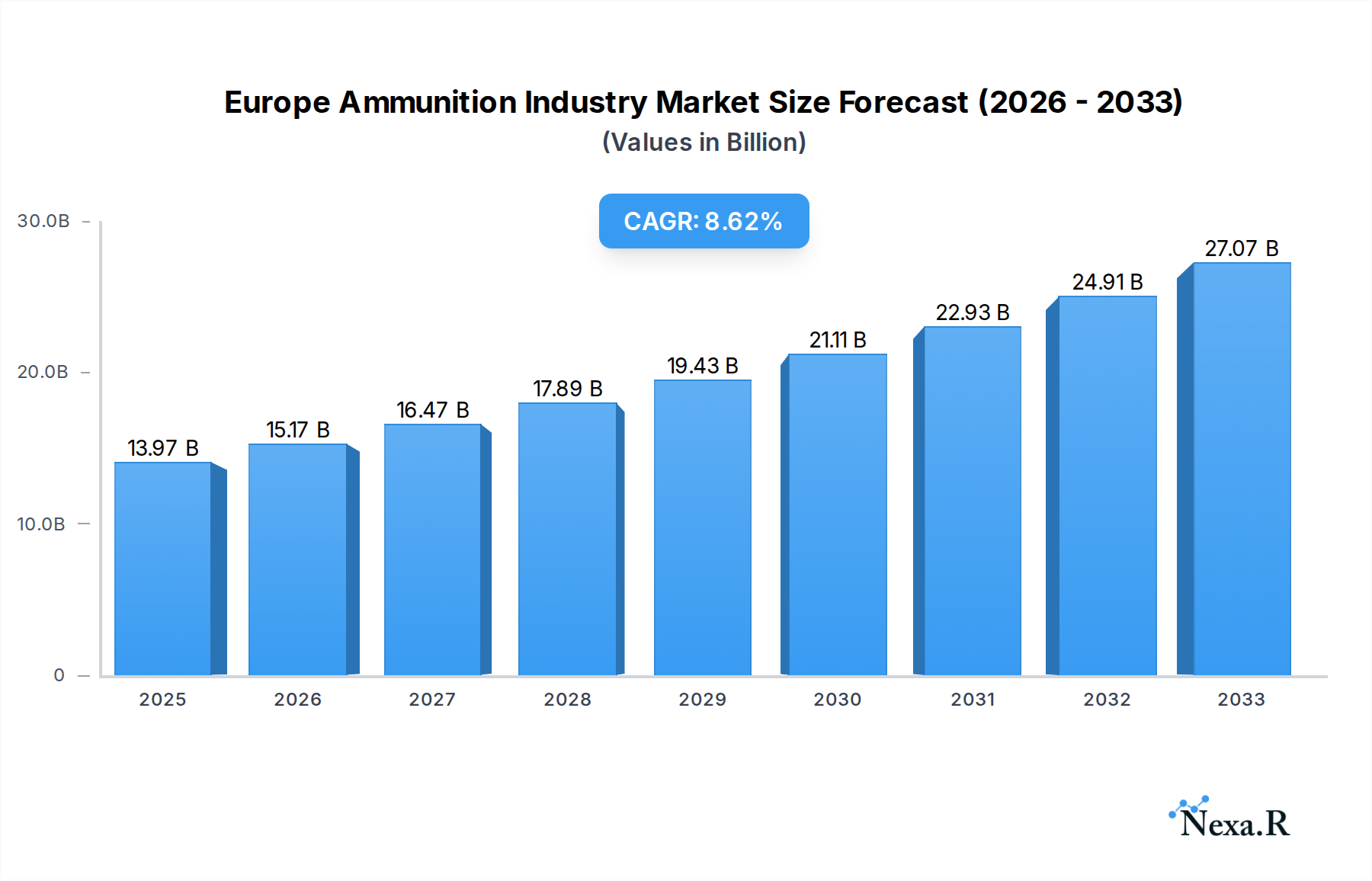

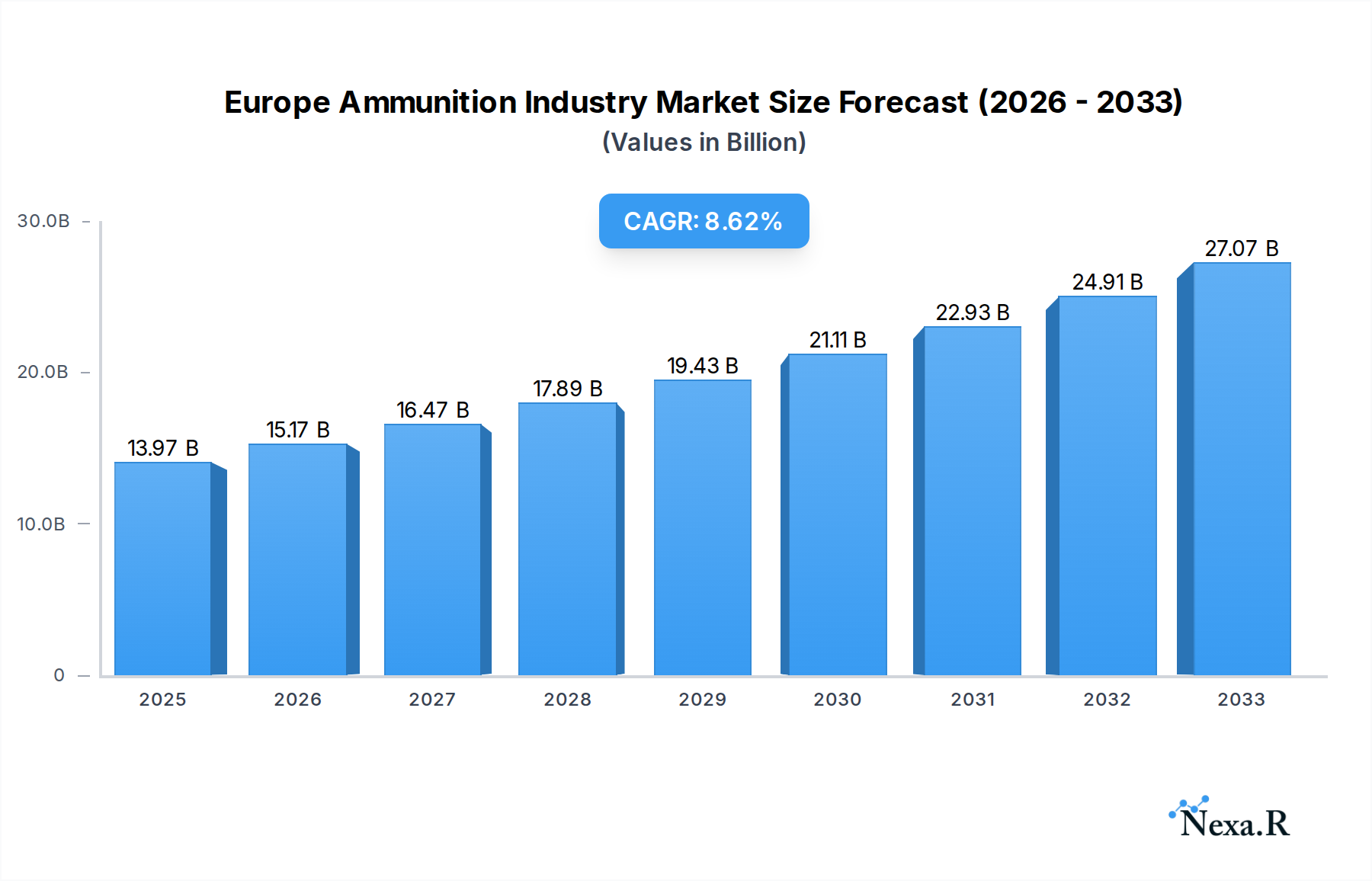

The European ammunition industry is poised for significant expansion, projected to reach $13.97 billion in 2025, with a robust Compound Annual Growth Rate (CAGR) of 8.64% anticipated through 2033. This growth is primarily fueled by heightened geopolitical tensions across the continent, prompting a substantial increase in defense spending by European nations. Governments are prioritizing the modernization and expansion of their military arsenals, leading to elevated demand for a wide array of ammunition types, from small-caliber rounds to advanced artillery shells and missiles. The ongoing conflict in Eastern Europe, coupled with the evolving threat landscape, has created an imperative for defense readiness, directly stimulating procurement activities. Furthermore, technological advancements in ammunition design, including precision-guided munitions and smart ordnance, are also contributing to market growth as militaries seek to enhance their combat effectiveness and reduce collateral damage.

Europe Ammunition Industry Market Size (In Billion)

Several key drivers are propelling the European ammunition market forward. Increased military modernization programs, driven by a need to replace aging inventories and adopt next-generation weaponry, are a primary catalyst. The persistent global security challenges necessitate enhanced defense capabilities, translating into sustained demand for ammunition. Additionally, the rise of asymmetric warfare and the increasing deployment of special forces underscore the need for specialized ammunition types. While the market benefits from strong demand, certain restraints could influence its trajectory. Supply chain complexities, particularly concerning raw materials and specialized components, can pose challenges. Regulatory frameworks surrounding the production and trade of ammunition, although necessary for safety and security, can also impact market agility. Nevertheless, the overarching trend points towards a dynamic and expanding European ammunition sector, characterized by innovation and strategic procurement to meet contemporary defense needs.

Europe Ammunition Industry Company Market Share

Europe Ammunition Industry Report: Market Dynamics, Trends, and Future Outlook (2019–2033)

This comprehensive report provides an in-depth analysis of the Europe Ammunition Industry, offering critical insights into market dynamics, growth trends, regional dominance, product landscape, key drivers, challenges, and emerging opportunities. Covering the study period of 2019–2033, with a base and estimated year of 2025 and a forecast period of 2025–2033, this report is an indispensable resource for industry stakeholders, including manufacturers, suppliers, investors, and defense procurement agencies. We present all values in billion units for clear understanding of market scale.

Europe Ammunition Industry Market Dynamics & Structure

The Europe Ammunition Industry is characterized by a moderately consolidated market structure, driven by significant investments in defense modernization and geopolitical stability concerns. Technological innovation is a primary driver, with a constant push for advanced materials, precision-guided munitions, and smart ammunition solutions. Stringent regulatory frameworks, particularly concerning the export and domestic sale of ordnance, influence market access and product development. Competitive product substitutes, while limited in direct high-caliber applications, exist in the form of electronic warfare systems and advanced drone capabilities. End-user demographics are predominantly government defense forces, with a growing segment in law enforcement and private security. Mergers & Acquisitions (M&A) trends indicate strategic consolidation among key players to enhance production capabilities and expand market reach.

- Market Concentration: Dominated by a few large defense conglomerates, but with a significant number of specialized SMEs.

- Technological Innovation: Focus on precision, lethality, and reduced collateral damage through smart fuzes, GPS guidance, and novel propellant technologies.

- Regulatory Frameworks: Strict adherence to international arms treaties and national defense procurement regulations.

- Competitive Substitutes: Emerging non-kinetic solutions and advanced surveillance technologies are indirectly impacting demand for traditional munitions.

- End-User Demographics: Primarily military forces, with increasing demand from specialized law enforcement units.

- M&A Trends: Strategic acquisitions to gain technological expertise, production capacity, and market share. Estimated M&A deal volume in the past five years is around 25-35 deals, with an average undisclosed value.

Europe Ammunition Industry Growth Trends & Insights

The Europe Ammunition Industry is poised for robust growth, fueled by escalating geopolitical tensions, a renewed focus on national security by European nations, and significant modernization programs within defense forces. The market size is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 4.5% to 5.5% during the forecast period (2025–2033). This growth is underpinned by increased defense spending across NATO member states and a persistent demand for a wide range of ammunition calibers, from small arms to heavy artillery.

Adoption rates of advanced ammunition technologies, such as programmable fuzes and guided projectiles, are steadily increasing as militaries seek to enhance precision engagement capabilities and minimize operational risks. Technological disruptions are evident in the development of next-generation propellants, reduced-size ammunition for lighter platforms, and integrated electronic components for enhanced battlefield awareness. Consumer behavior shifts, while not in the traditional sense, are reflected in military procurement strategies that prioritize lifecycle cost, logistical efficiency, and interoperability alongside raw performance.

The market penetration of high-precision munitions is expanding, driven by the need for greater effectiveness in complex operational environments. Consumer preferences are leaning towards solutions that offer superior accuracy, extended range, and multi-functionality. This evolving demand landscape necessitates continuous R&D investment from key players to maintain a competitive edge. The historical period (2019–2024) saw a steady increase in production and consumption, laying the groundwork for the projected growth. For instance, production volume in 2024 is estimated to be around 7.2 billion units, with consumption mirroring this trend closely.

Dominant Regions, Countries, or Segments in Europe Ammunition Industry

Within the Europe Ammunition Industry, several regions, countries, and segments are driving market growth and exhibiting significant dominance.

Production Analysis: Germany, France, and the United Kingdom consistently emerge as dominant countries in ammunition production. Their established defense industrial bases, coupled with substantial government investment in domestic manufacturing capabilities, ensure high output volumes. The Parent Market for overall ammunition production is substantial, estimated to reach over 9.5 billion units by 2033. Key drivers include:

- Economic Policies: Favorable government incentives and long-term procurement contracts supporting domestic defense manufacturers.

- Infrastructure: Well-developed industrial infrastructure and specialized manufacturing facilities.

- Technological Expertise: Decades of experience in munition development and production.

- Market Share: These countries collectively hold an estimated 45-55% of the total European production volume.

- Growth Potential: Continuous modernization programs and export opportunities fuel ongoing growth.

Consumption Analysis: The Child Market for 155mm artillery ammunition represents a significant and growing segment of consumption. This is directly linked to ongoing artillery modernization efforts and the increased focus on indirect fire capabilities by European armed forces. Consumption is also heavily influenced by:

- Geopolitical Stability: Regional conflicts and heightened security concerns drive demand for battlefield-ready ammunition.

- Military Doctrines: Emphasis on conventional warfare and combined arms operations necessitates high volumes of artillery and small arms ammunition.

- Market Share: The 155mm segment alone accounts for approximately 20-25% of the total European ammunition consumption in terms of volume.

- Growth Potential: Continued deployment of advanced artillery systems and the replenishment of stockpiles are key growth factors.

Import Market Analysis (Value & Volume): While Europe is a significant producer, certain specialized ammunition types and components are imported, primarily from North America and select Asian countries. The import market is crucial for filling specific technological gaps and ensuring supply chain resilience. Key factors include:

- Technological Specialization: Imports often focus on advanced precision-guided munitions or niche calibers not extensively produced domestically.

- Strategic Partnerships: Interoperability agreements and collaborative defense initiatives drive import volumes.

- Value & Volume: Estimated import volume in 2025 is around 0.8 billion units, with a value projected to be approximately USD 4.5 billion.

Export Market Analysis (Value & Volume): European nations are significant exporters of ammunition, catering to allied nations and friendly regimes. This export market is vital for revenue generation and maintaining production capacities. The primary export drivers are:

- Global Defense Demand: Increased defense spending in regions like the Middle East, Asia-Pacific, and Africa.

- Quality and Reliability: European-manufactured ammunition is recognized for its high quality and reliability.

- Value & Volume: Estimated export volume in 2025 is around 1.2 billion units, with a projected value of USD 6.8 billion.

Price Trend Analysis: Price trends are influenced by raw material costs (metals, propellants), manufacturing complexity, R&D investments, and geopolitical demand. The average price per unit is projected to see a steady increase of 2-3% annually due to inflationary pressures and the rising cost of advanced technologies.

Europe Ammunition Industry Product Landscape

The Europe Ammunition Industry product landscape is characterized by a diverse portfolio catering to a wide array of military and law enforcement applications. Innovations are focused on enhancing precision, effectiveness, and safety. Key product categories include small-caliber ammunition (5.56mm, 7.62mm), medium-caliber ammunition (20mm, 30mm), large-caliber artillery shells (105mm, 155mm), mortar rounds, and various specialized munitions such as anti-tank rounds, illumination flares, and training ammunition.

Emerging trends involve the integration of smart technologies, such as programmable fuzes that allow for in-flight adjustments of detonation timing, thereby increasing target accuracy and reducing collateral damage. The development of insensitive munitions (IM) to enhance safety during handling and storage is also a significant focus. Performance metrics are continually being improved through advancements in propellants, projectile design, and terminal ballistics. Unique selling propositions often revolve around superior accuracy, extended range, multi-target engagement capabilities, and adherence to stringent environmental and safety standards.

Key Drivers, Barriers & Challenges in Europe Ammunition Industry

Key Drivers:

- Geopolitical Instability and Defense Modernization: Increased global tensions and a renewed emphasis on national defense are driving significant investment in ammunition procurement and modernization programs across European nations. This translates to sustained demand for a broad spectrum of ammunition types.

- Technological Advancements: The continuous development of smart munitions, precision-guided systems, and advanced propellants offers enhanced battlefield effectiveness and creates new market opportunities for manufacturers.

- Interoperability and NATO Standards: The drive for interoperability within NATO necessitates the adoption and production of standardized ammunition calibers and types, leading to large-scale procurement contracts.

- Replacement and Stockpile Replenishment: Aging ammunition stockpiles and the operational expenditure of ongoing military exercises and deployments necessitate regular replenishment.

Key Barriers & Challenges:

- High Research & Development Costs: Developing cutting-edge ammunition technologies requires substantial investment in R&D, posing a barrier for smaller manufacturers.

- Stringent Regulatory and Export Controls: Navigating complex international arms regulations and obtaining export licenses can be a lengthy and challenging process, impacting market access.

- Supply Chain Volatility and Raw Material Costs: Fluctuations in the cost and availability of critical raw materials, such as specialty metals and chemical propellants, can impact production costs and lead times.

- Environmental Regulations and Disposal: Strict environmental regulations concerning the manufacturing, testing, and disposal of ammunition present ongoing compliance challenges.

- Intensifying Competition: While consolidated, the market faces competition from both established global players and emerging regional manufacturers.

- Limited Domestic Production Capacity for Specific Components: Reliance on external suppliers for certain critical components can create supply chain vulnerabilities.

Emerging Opportunities in Europe Ammunition Industry

Emerging opportunities in the Europe Ammunition Industry lie in the growing demand for smart ammunition and non-lethal munitions. The increasing focus on precision warfare and reducing collateral damage is driving the adoption of guided projectiles and programmable fuzes. Furthermore, the development of training ammunition with realistic ballistics but reduced lethality is crucial for cost-effective military training. The expansion of the child market for advanced mortar rounds and artillery systems presents opportunities for manufacturers specializing in these calibers. The potential for cybersecurity-enhanced munitions also represents a nascent but promising area, where ammunition can communicate and provide real-time battlefield data.

Growth Accelerators in the Europe Ammunition Industry Industry

Several catalysts are accelerating long-term growth in the Europe Ammunition Industry. Significant defense spending increases by European nations, particularly in response to recent geopolitical shifts, are a primary accelerator. The continuous drive for technological superiority, leading to the development of next-generation munitions with enhanced capabilities, further fuels market expansion. Strategic partnerships and collaborations between defense contractors and technology firms are enabling the rapid integration of innovative solutions. Moreover, the ongoing modernization of legacy military equipment across various European armed forces necessitates a corresponding upgrade and replenishment of ammunition stocks. The increasing export potential to allied nations also acts as a significant growth accelerator.

Key Players Shaping the Europe Ammunition Industry Market

- General Dynamics Corporation

- Rheinmetall AG

- Elbit Systems Ltd

- Heckler & Koch GmbH

- Nexter Group

- Nammo AS

- Denel PMP

- BAE Systems plc

- ROSTEC

- Saab AB

Notable Milestones in Europe Ammunition Industry Sector

- December 2022: A European NATO customer entered into a contract with Rheinmetall to supply a maximum of 300,000 rounds of 40mm ammunition, consisting of LV (low velocity) and HV (high velocity) variants. The contract includes a first call-off of approximately 75,000 cartridges, significantly boosting production for this caliber.

- January 2022: The German Bundeswehr signed a contract with Rheinmetall AG to modernize its mortar systems and provide 120mm mortar ammunition. The contract, worth approximately EUR 27 million (USD 30 million) and to be completed by 2023, underscored the importance of indirect fire capabilities and the demand for specialized mortar ammunition.

In-Depth Europe Ammunition Industry Market Outlook

The Europe Ammunition Industry is projected to experience sustained and robust growth, driven by a confluence of geopolitical imperatives and technological advancements. The ongoing defense spending spree across European nations, coupled with the strategic imperative to maintain and modernize national defense capabilities, will continue to be the primary growth accelerator. The increasing adoption of smart and precision-guided munitions will redefine battlefield effectiveness and create a lucrative market for high-value products. Strategic partnerships and the relentless pursuit of innovation by key players will ensure a dynamic and evolving market landscape. The continued replacement of aging ammunition stockpiles and the replenishment of expended rounds from ongoing military operations will provide a steady demand stream, solidifying the positive outlook for the Europe Ammunition Industry.

Europe Ammunition Industry Segmentation

- 1. Production Analysis

- 2. Consumption Analysis

- 3. Import Market Analysis (Value & Volume)

- 4. Export Market Analysis (Value & Volume)

- 5. Price Trend Analysis

Europe Ammunition Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

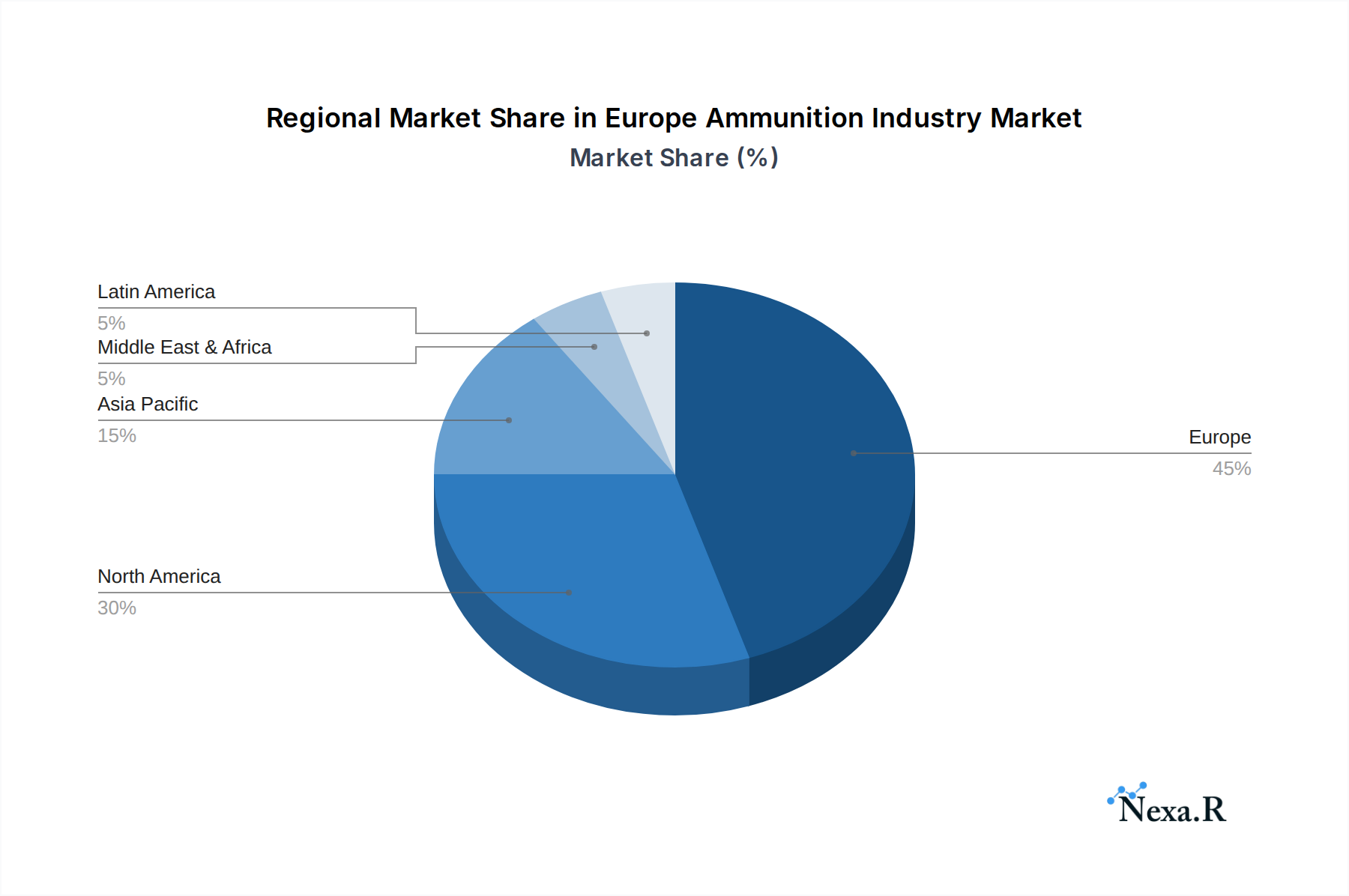

Europe Ammunition Industry Regional Market Share

Geographic Coverage of Europe Ammunition Industry

Europe Ammunition Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 5.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 5.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 5.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 5.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. Europe

- 6. Europe Ammunition Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Production Analysis

- 6.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 6.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 6.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 6.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 General Dynamics Corporation

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Rheinmetall AG

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Elbit Systems Ltd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Heckler & Koch Gmb

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Nexter Group

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Nammo AS

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Denel PMP

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 BAE Systems plc

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 ROSTEC

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Saab AB

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 General Dynamics Corporation

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Ammunition Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Ammunition Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Ammunition Industry Revenue billion Forecast, by Production Analysis 2020 & 2033

- Table 2: Europe Ammunition Industry Revenue billion Forecast, by Consumption Analysis 2020 & 2033

- Table 3: Europe Ammunition Industry Revenue billion Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 4: Europe Ammunition Industry Revenue billion Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 5: Europe Ammunition Industry Revenue billion Forecast, by Price Trend Analysis 2020 & 2033

- Table 6: Europe Ammunition Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 7: Europe Ammunition Industry Revenue billion Forecast, by Production Analysis 2020 & 2033

- Table 8: Europe Ammunition Industry Revenue billion Forecast, by Consumption Analysis 2020 & 2033

- Table 9: Europe Ammunition Industry Revenue billion Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 10: Europe Ammunition Industry Revenue billion Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 11: Europe Ammunition Industry Revenue billion Forecast, by Price Trend Analysis 2020 & 2033

- Table 12: Europe Ammunition Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: United Kingdom Europe Ammunition Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Germany Europe Ammunition Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: France Europe Ammunition Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Italy Europe Ammunition Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Spain Europe Ammunition Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Netherlands Europe Ammunition Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Belgium Europe Ammunition Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Sweden Europe Ammunition Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Norway Europe Ammunition Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Poland Europe Ammunition Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Denmark Europe Ammunition Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Ammunition Industry?

The projected CAGR is approximately 3.8%.

2. Which companies are prominent players in the Europe Ammunition Industry?

Key companies in the market include General Dynamics Corporation, Rheinmetall AG, Elbit Systems Ltd, Heckler & Koch Gmb, Nexter Group, Nammo AS, Denel PMP, BAE Systems plc, ROSTEC, Saab AB.

3. What are the main segments of the Europe Ammunition Industry?

The market segments include Production Analysis, Consumption Analysis, Import Market Analysis (Value & Volume), Export Market Analysis (Value & Volume), Price Trend Analysis.

4. Can you provide details about the market size?

The market size is estimated to be USD 26.4 billion as of 2022.

5. What are some drivers contributing to market growth?

; Increasing Number Of Air Passengers; Use Of Portable Electronic Devices.

6. What are the notable trends driving market growth?

Military to Dominate Market Share During the Forecast Period.

7. Are there any restraints impacting market growth?

; High Cost Of Connectivity Equipments.

8. Can you provide examples of recent developments in the market?

December 2022: A European NATO customer entered into a contract with Rheinmetall to supply a maximum of 300,000 rounds of 40mm ammunition, consisting of LV (low velocity) and HV (high velocity) variants. The contract includes a first call-off of approximately 75,000 cartridges.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Ammunition Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Ammunition Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Ammunition Industry?

To stay informed about further developments, trends, and reports in the Europe Ammunition Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence