Key Insights

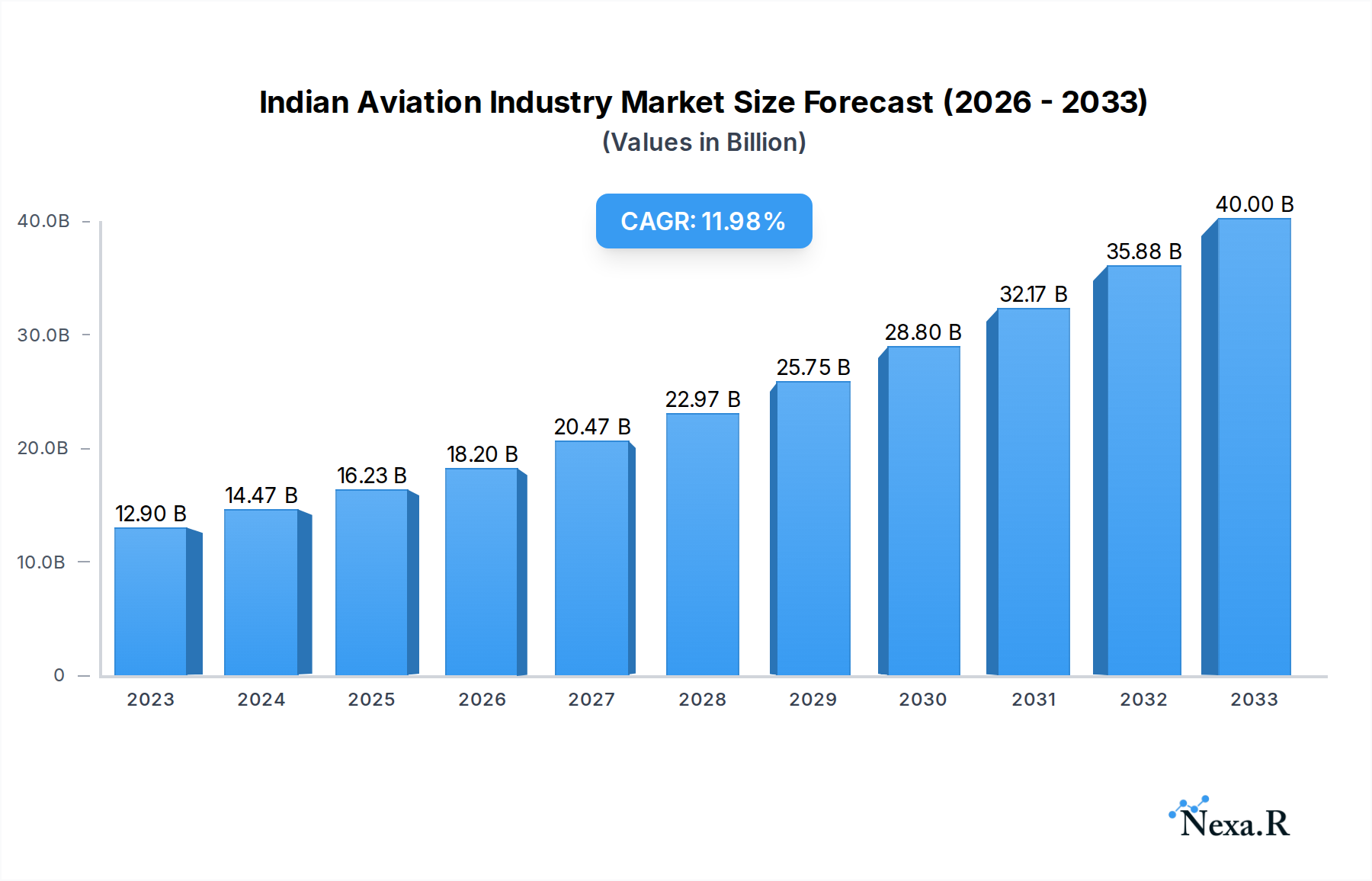

The Indian Aviation Industry is poised for remarkable expansion, with a current market size estimated at USD 14.47 billion in 2024. This robust growth is projected to continue at a Compound Annual Growth Rate (CAGR) of 12.21% over the forecast period. The industry's dynamism is fueled by a confluence of powerful drivers, including a rapidly expanding middle class with increasing disposable incomes, a growing demand for air travel for both business and leisure, and significant government initiatives aimed at bolstering aviation infrastructure and connectivity. The "UDAN" (Ude Desh Ka Aam Nagrik) scheme, for instance, has been instrumental in promoting regional air connectivity, opening up new routes and making air travel more accessible to a wider population. Furthermore, the increasing adoption of modern, fuel-efficient aircraft, coupled with technological advancements in air traffic management and airline operations, are contributing to operational efficiencies and enhancing the overall passenger experience. The strategic importance of aviation in India's economic development, facilitating trade, tourism, and investment, further underpins this optimistic outlook.

Indian Aviation Industry Market Size (In Billion)

The market segments within the Indian Aviation Industry showcase diverse growth trajectories. Commercial aviation, encompassing both passenger and freighter aircraft, represents the largest and fastest-growing segment, driven by the sheer volume of air traffic and the increasing need for efficient cargo movement. General aviation, particularly business jets, is also witnessing steady growth as corporate expansion and the need for private travel solutions increase. Military aviation, while driven by different factors such as national security and defense modernization, also contributes to the overall market expansion through procurements and upgrades. Emerging trends like the focus on sustainable aviation fuels, the integration of digital technologies for enhanced passenger services, and the development of advanced aerospace manufacturing capabilities are shaping the future landscape. However, potential restraints such as fluctuating fuel prices, regulatory hurdles, and the need for continuous infrastructure development to match demand require careful navigation by industry stakeholders. Despite these challenges, the underlying demand for air travel and the strategic impetus for aviation development in India suggest a bright and expansive future for the sector.

Indian Aviation Industry Company Market Share

Report: Indian Aviation Industry Market Dynamics, Growth & Future Outlook (2019-2033)

This comprehensive report provides an in-depth analysis of the Indian aviation industry, offering a detailed understanding of its market dynamics, growth trajectory, and future potential. Covering the historical period from 2019-2024 and projecting to 2033, with a base and estimated year of 2025, this report is an essential resource for industry stakeholders, investors, and policymakers. We delve into parent and child market segments, providing quantitative and qualitative insights to empower strategic decision-making in this rapidly evolving sector.

Indian Aviation Industry Market Dynamics & Structure

The Indian aviation industry is characterized by a dynamic interplay of market concentration, rapid technological innovation, and an evolving regulatory landscape. Major global players like Airbus SE and The Boeing Company, alongside domestic giants Hindustan Aeronautics Limited, are key contributors to this complex ecosystem. While competition is intense, it also spurs continuous innovation, particularly in areas like fuel efficiency and advanced avionics. Regulatory frameworks, such as the Directorate General of Civil Aviation (DGCA) guidelines, play a crucial role in shaping market access and operational standards. The burgeoning middle class and increasing disposable incomes are driving demand for air travel, influencing end-user demographics. Mergers and acquisitions (M&A) trends, though not as frequent as in mature markets, are anticipated to gain traction as companies seek to consolidate market share and expand capabilities. The cost of new aircraft and the complexity of maintenance present innovation barriers, requiring significant capital investment and specialized expertise.

- Market Concentration: Dominated by a few major global manufacturers for large commercial aircraft, with increasing indigenous capabilities in military and smaller aircraft segments.

- Technological Innovation Drivers: Focus on sustainable aviation fuels (SAF), advanced composite materials, and digital transformation for operational efficiency.

- Regulatory Frameworks: Governed by the DGCA, with a focus on safety, airworthiness, and passenger rights.

- Competitive Product Substitutes: While direct substitutes for air travel are limited for long distances, efficient high-speed rail can impact shorter domestic routes.

- End-User Demographics: Shifting from primarily business and premium leisure travelers to a broader demographic segment with increasing demand for affordable travel.

- M&A Trends: Expected growth in strategic alliances and potential consolidations to leverage economies of scale and technological advancements.

Indian Aviation Industry Growth Trends & Insights

The Indian aviation industry is poised for significant expansion, driven by robust economic growth, increasing disposable incomes, and a growing emphasis on connectivity. The market size is projected to witness a Compound Annual Growth Rate (CAGR) of approximately xx% during the forecast period. Adoption rates for new aircraft technologies, particularly those focusing on fuel efficiency and reduced emissions, are on an upward trajectory. Technological disruptions, such as the integration of Artificial Intelligence (AI) in air traffic management and predictive maintenance, are set to redefine operational paradigms. Consumer behavior is shifting towards more frequent and accessible air travel, influenced by competitive pricing and improved passenger experience. The penetration of air travel into Tier 2 and Tier 3 cities is a key trend, fueled by government initiatives like the Regional Connectivity Scheme (RCS). The airline industry's expansion is also directly linked to cargo demand, with freighter aircraft playing a crucial role in supporting India's manufacturing and e-commerce growth. The introduction of new aircraft models and advancements in cabin comfort are further enhancing the passenger experience.

The forecast period, 2025–2033, anticipates a substantial increase in the overall market value, projected to reach over $300 billion. This growth will be propelled by a combination of fleet expansion by major Indian carriers and the emergence of new airlines. The adoption of advanced aircraft, such as the Boeing 737 MAX and Airbus A330neo, signifies a commitment to modernizing fleets and improving operational efficiency. The growing demand for international travel will also contribute to the expansion of wide-body aircraft segments. Furthermore, the military aviation sector is undergoing significant modernization, driving demand for advanced multi-role and transport aircraft. The general aviation segment, encompassing business jets and piston-fixed-wing aircraft, is also expected to see steady growth as India's corporate sector expands.

- Market Size Evolution: Projected to more than double its current valuation by 2033, fueled by passenger and cargo demand.

- Adoption Rates: Increasing for fuel-efficient aircraft and digital solutions that enhance operational efficiency and safety.

- Technological Disruptions: AI in air traffic control, advanced manufacturing techniques for aircraft components, and the growing importance of sustainable aviation.

- Consumer Behavior Shifts: A move towards more frequent domestic and international travel, with increased demand for budget-friendly options and enhanced travel experiences.

- Market Penetration: Expanding reach into smaller cities and remote areas, democratizing air travel.

Dominant Regions, Countries, or Segments in Indian Aviation Industry

Commercial Aviation stands as the dominant segment within the Indian aviation industry, driven by the nation's rapidly growing passenger and cargo traffic. Within this segment, Passenger Aircraft, particularly Narrowbody Aircraft, commands the largest market share due to their efficiency and suitability for high-frequency domestic routes. The sheer volume of travelers on inter-city routes makes this sub-segment a consistent revenue generator. Freighter Aircraft are also experiencing substantial growth, underpinning the expansion of India's e-commerce and logistics sectors, with projected growth rates exceeding xx%. Widebody Aircraft, while representing a smaller portion of the total fleet, are crucial for long-haul international routes and are witnessing increased demand as India's global connectivity expands and major carriers like Air India invest in modernizing their long-haul fleets, as evidenced by their recent orders for Boeing 777X and 787 aircraft.

The growth in Commercial Aviation is intricately linked to India's economic policies, such as Make in India, which stimulates manufacturing and consequently cargo movement. Infrastructure development, including the expansion of existing airports and the construction of new ones, is a critical enabler. The government's focus on improving air connectivity to remote regions through schemes like UDAN (Ude Desh Ka Aam Nagrik) further boosts the demand for passenger aircraft. The rising disposable incomes of the Indian population directly translate into increased air travel propensity. The recent large-scale orders placed by Indian airlines, such as Air India's order for 220 Boeing aircraft, underscore the significant growth potential and the strategic importance of this segment. This colossal order includes 190 737 MAX aircraft, highlighting the continued dominance of narrowbody planes for domestic and short-to-medium haul international routes, alongside 20 787 Dreamliners and 10 777X for long-haul operations, signaling an ambitious expansion strategy for international connectivity.

General Aviation, though smaller in scale, is an essential component of the Indian aviation ecosystem. Business Jets are gaining traction as Indian corporations expand their global footprint and prioritize efficient business travel. The demand for Large Jets, Mid-Size Jets, and Light Jets reflects the growing wealth and business activities in the country. Piston Fixed-Wing Aircraft cater to smaller charter operations, flight training, and niche aviation activities. While still nascent, the growth potential for General Aviation is significant, driven by a desire for personalized and time-efficient travel solutions.

Military Aviation is another crucial segment, with ongoing modernization efforts by the Indian Armed Forces. Multi-Role Aircraft are critical for defense strategies, and the demand for advanced trainers and transport aircraft remains consistent. Rotorcraft, including Multi-Mission Helicopters and Transport Helicopters, are vital for reconnaissance, troop deployment, disaster relief, and VVIP transportation. The recent contract awarded to Textron Inc.'s Bell unit for next-generation helicopters by the US Army for its "Future Vertical Lift" program highlights the global advancements in this domain and suggests potential future upgrade paths for India's rotorcraft fleet as it looks to retire aging UH-60 Black Hawk utility helicopters.

- Commercial Aviation (Dominant):

- Passenger Aircraft:

- Narrowbody Aircraft: Highest market share, driven by high domestic demand and operational efficiency.

- Widebody Aircraft: Growing demand for international routes and long-haul travel.

- Freighter Aircraft: Significant growth fueled by e-commerce and manufacturing expansion.

- Passenger Aircraft:

- General Aviation:

- Business Jets: Increasing adoption by corporations for efficient travel.

- Piston Fixed-Wing Aircraft: Niche applications in training and charter services.

- Military Aviation:

- Multi-Role Aircraft: Continuous demand for modernization and strategic capabilities.

- Training Aircraft: Essential for pilot development and skill enhancement.

- Transport Aircraft: Supporting logistical needs of the armed forces.

- Rotorcraft: Critical for various defense and civilian operations.

Indian Aviation Industry Product Landscape

The Indian aviation industry is witnessing a surge in product innovations focused on enhancing efficiency, safety, and passenger comfort. Advanced materials, such as composites, are being increasingly integrated into aircraft structures to reduce weight and improve fuel economy. The development of next-generation avionics and navigation systems is enhancing flight safety and operational capabilities. Key players like Airbus SE and The Boeing Company are continuously introducing updated models with improved aerodynamic designs and more powerful, fuel-efficient engines. In the military sector, Hindustan Aeronautics Limited is at the forefront of developing indigenous multi-role aircraft and advanced rotorcraft, showcasing technological advancements in areas like stealth technology and integrated digital cockpits. The focus is on delivering high-performance, reliable, and sustainable aviation solutions that meet the diverse needs of both commercial and defense sectors.

Key Drivers, Barriers & Challenges in Indian Aviation Industry

Key Drivers:

- Economic Growth & Rising Disposable Incomes: Fueling increased demand for air travel.

- Government Initiatives: Schemes like UDAN promoting regional connectivity.

- Increasing Air Cargo Demand: Supporting e-commerce and manufacturing expansion.

- Fleet Modernization: Airlines investing in newer, fuel-efficient aircraft.

- Technological Advancements: Driving efficiency, safety, and passenger experience.

Barriers & Challenges:

- High Operating Costs: Fuel prices, maintenance, and airport charges.

- Infrastructure Constraints: Limited airport capacity and air traffic control congestion.

- Skilled Workforce Shortage: Demand for pilots, engineers, and technicians.

- Regulatory Hurdles: Complex approval processes and policy changes.

- Global Supply Chain Disruptions: Impacting aircraft and component delivery timelines.

- Environmental Regulations: Growing pressure for sustainable aviation solutions.

Emerging Opportunities in Indian Aviation Industry

Emerging opportunities in the Indian aviation industry lie in the untapped potential of Tier 2 and Tier 3 cities, where demand for air travel is poised for exponential growth. The increasing focus on sustainable aviation fuels (SAF) and electric aircraft presents a significant opportunity for innovation and investment. The expansion of air cargo services, driven by the burgeoning e-commerce sector, offers avenues for growth in freighter operations and associated logistics. Furthermore, the defense sector's modernization plans create demand for advanced indigenous military aircraft and rotorcraft. The development of specialized aviation services, such as aeromedical evacuation and drone-based logistics, also represents a promising frontier.

Growth Accelerators in the Indian Aviation Industry Industry

Several key catalysts are driving long-term growth in the Indian aviation industry. Technological breakthroughs in engine efficiency, lightweight materials, and digital systems are enhancing operational performance and reducing environmental impact. Strategic partnerships between airlines, manufacturers, and technology providers are fostering innovation and expanding market reach. The Indian government's proactive approach to policy reforms, including the simplification of regulations and incentives for manufacturing, is a significant growth accelerator. Market expansion strategies, such as the introduction of new routes and the development of ancillary aviation services, are further bolstering the industry's growth trajectory.

Key Players Shaping the Indian Aviation Industry Market

- Textron Inc.

- Dassault Aviation

- General Dynamics Corporation

- Lockheed Martin Corporation

- Airbus SE

- The Boeing Company

- Leonardo S p A

- Bombardier Inc.

- ATR

- Hindustan Aeronautics Limited

Notable Milestones in Indian Aviation Industry Sector

- June 2023: Delta Air Lines Inc. is in talks with Airbus SE to order wide-body aircraft, focusing on A350 and A330neo twin-aisle aircraft.

- March 2023: Boeing was awarded a contract by Air India for 220 aircraft, including 190 737 Max, 20 787, and 10 777X.

- December 2022: The US Army awarded a contract to Textron Inc.'s Bell unit for next-generation helicopters to replace UH-60 Black Hawks.

In-Depth Indian Aviation Industry Market Outlook

The Indian aviation industry is set for a period of sustained and robust growth, driven by a confluence of economic prosperity, demographic shifts, and technological advancements. The market's future potential is immense, with opportunities in expanding regional connectivity, embracing sustainable aviation, and modernizing both commercial and defense fleets. Strategic investments in airport infrastructure, pilot training, and indigenous manufacturing capabilities will be crucial in realizing this potential. The industry is on a trajectory to become a global aviation powerhouse, offering significant strategic opportunities for stakeholders looking to capitalize on India's burgeoning aerospace sector.

Indian Aviation Industry Segmentation

-

1. Aircraft Type

-

1.1. Commercial Aviation

-

1.1.1. By Sub Aircraft Type

- 1.1.1.1. Freighter Aircraft

-

1.1.1.2. Passenger Aircraft

-

1.1.1.2.1. By Body Type

- 1.1.1.2.1.1. Narrowbody Aircraft

- 1.1.1.2.1.2. Widebody Aircraft

-

1.1.1.2.1. By Body Type

-

1.1.1. By Sub Aircraft Type

-

1.2. General Aviation

-

1.2.1. Business Jets

- 1.2.1.1. Large Jet

- 1.2.1.2. Light Jet

- 1.2.1.3. Mid-Size Jet

- 1.2.2. Piston Fixed-Wing Aircraft

- 1.2.3. Others

-

1.2.1. Business Jets

-

1.3. Military Aviation

- 1.3.1. Multi-Role Aircraft

- 1.3.2. Training Aircraft

- 1.3.3. Transport Aircraft

-

1.3.4. Rotorcraft

- 1.3.4.1. Multi-Mission Helicopter

- 1.3.4.2. Transport Helicopter

-

1.1. Commercial Aviation

Indian Aviation Industry Segmentation By Geography

- 1. India

Indian Aviation Industry Regional Market Share

Geographic Coverage of Indian Aviation Industry

Indian Aviation Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.21% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 5.1.1. Commercial Aviation

- 5.1.1.1. By Sub Aircraft Type

- 5.1.1.1.1. Freighter Aircraft

- 5.1.1.1.2. Passenger Aircraft

- 5.1.1.1.2.1. By Body Type

- 5.1.1.1.2.1.1. Narrowbody Aircraft

- 5.1.1.1.2.1.2. Widebody Aircraft

- 5.1.1.1.2.1. By Body Type

- 5.1.1.1. By Sub Aircraft Type

- 5.1.2. General Aviation

- 5.1.2.1. Business Jets

- 5.1.2.1.1. Large Jet

- 5.1.2.1.2. Light Jet

- 5.1.2.1.3. Mid-Size Jet

- 5.1.2.2. Piston Fixed-Wing Aircraft

- 5.1.2.3. Others

- 5.1.2.1. Business Jets

- 5.1.3. Military Aviation

- 5.1.3.1. Multi-Role Aircraft

- 5.1.3.2. Training Aircraft

- 5.1.3.3. Transport Aircraft

- 5.1.3.4. Rotorcraft

- 5.1.3.4.1. Multi-Mission Helicopter

- 5.1.3.4.2. Transport Helicopter

- 5.1.1. Commercial Aviation

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. India

- 5.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 6. Indian Aviation Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 6.1.1. Commercial Aviation

- 6.1.1.1. By Sub Aircraft Type

- 6.1.1.1.1. Freighter Aircraft

- 6.1.1.1.2. Passenger Aircraft

- 6.1.1.1.2.1. By Body Type

- 6.1.1.1.2.1.1. Narrowbody Aircraft

- 6.1.1.1.2.1.2. Widebody Aircraft

- 6.1.1.1.2.1. By Body Type

- 6.1.1.1. By Sub Aircraft Type

- 6.1.2. General Aviation

- 6.1.2.1. Business Jets

- 6.1.2.1.1. Large Jet

- 6.1.2.1.2. Light Jet

- 6.1.2.1.3. Mid-Size Jet

- 6.1.2.2. Piston Fixed-Wing Aircraft

- 6.1.2.3. Others

- 6.1.2.1. Business Jets

- 6.1.3. Military Aviation

- 6.1.3.1. Multi-Role Aircraft

- 6.1.3.2. Training Aircraft

- 6.1.3.3. Transport Aircraft

- 6.1.3.4. Rotorcraft

- 6.1.3.4.1. Multi-Mission Helicopter

- 6.1.3.4.2. Transport Helicopter

- 6.1.1. Commercial Aviation

- 6.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Textron Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Dassault Aviation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 General Dynamics Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Lockheed Martin Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Airbus SE

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 The Boeing Compan

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Leonardo S p A

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Bombardier Inc

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 ATR

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Hindustan Aeronautics Limited

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Textron Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Indian Aviation Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Indian Aviation Industry Share (%) by Company 2025

List of Tables

- Table 1: Indian Aviation Industry Revenue billion Forecast, by Aircraft Type 2020 & 2033

- Table 2: Indian Aviation Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Indian Aviation Industry Revenue billion Forecast, by Aircraft Type 2020 & 2033

- Table 4: Indian Aviation Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Indian Aviation Industry?

The projected CAGR is approximately 12.21%.

2. Which companies are prominent players in the Indian Aviation Industry?

Key companies in the market include Textron Inc, Dassault Aviation, General Dynamics Corporation, Lockheed Martin Corporation, Airbus SE, The Boeing Compan, Leonardo S p A, Bombardier Inc, ATR, Hindustan Aeronautics Limited.

3. What are the main segments of the Indian Aviation Industry?

The market segments include Aircraft Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 14.47 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

June 2023: Delta Air Lines Inc. is in talks with Airbus SE to order wide-body aircraft, Bloomberg News reported Monday, citing people familiar with the matter. The discussion focuses on A350 and A330neo hai twin-aisle aircraft.March 2023: Boeing was awarded a contract by Air India for 220 Boeing aircraft, including 190 737 Max, 20 787, and 10 777X.December 2022: The US Army was awarded a contract to supply next-generation helicopters to Textron Inc.'s Bell unit. The Army`s "Future Vertical Lift" competition aimed at finding a replacement as the Army looks to retire more than 2,000 medium-class UH-60 Black Hawk utility helicopters.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Indian Aviation Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Indian Aviation Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Indian Aviation Industry?

To stay informed about further developments, trends, and reports in the Indian Aviation Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence