Key Insights

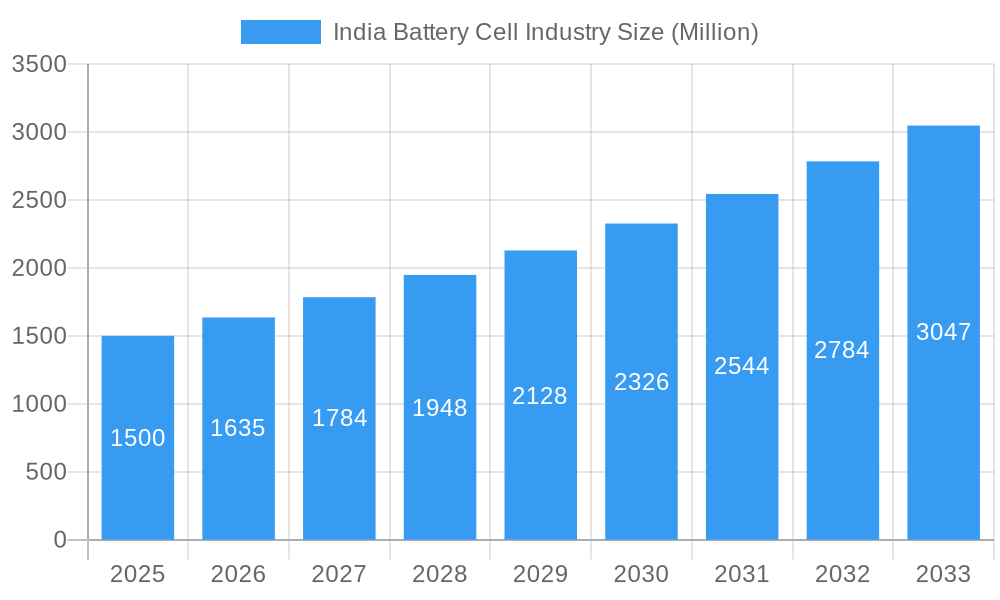

India's battery cell market is poised for substantial growth, driven by the rapid expansion of the electric vehicle (EV) sector, increasing demand for energy storage in renewable energy systems, and government initiatives promoting domestic manufacturing. The market is expected to achieve a Compound Annual Growth Rate (CAGR) of 11.48%, with a projected market size of 10.45 billion by 2033. Key growth drivers include the widespread adoption of EVs across two-wheelers, three-wheelers, passenger vehicles, and commercial segments. The growing integration of renewable energy sources like solar and wind power also necessitates efficient energy storage solutions, further boosting demand for battery cells. The market is segmented by cell type, including prismatic, cylindrical, and pouch cells, serving diverse applications such as automotive, industrial, and portable batteries. While the automotive segment leads, significant growth potential is observed in power tools and stationary energy storage. Leading global players like BYD, CATL, LG Energy Solution, Panasonic, and local participants are actively shaping the competitive landscape through innovation.

India Battery Cell Industry Market Size (In Billion)

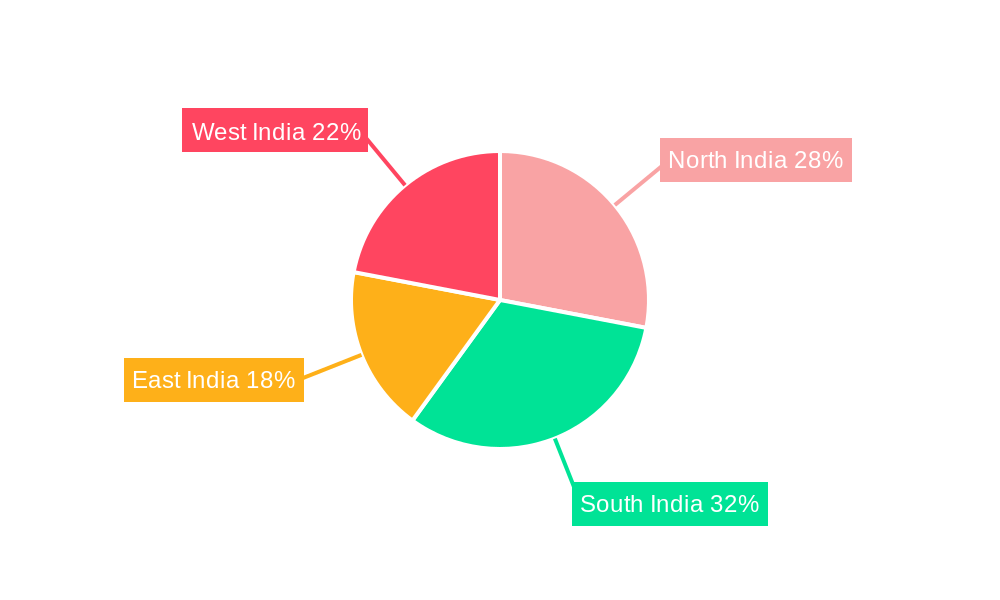

Geographically, all regions within India, including North, South, East, and West, exhibit promising growth trends, though infrastructure development and consumer adoption rates may lead to regional variations. Despite challenges such as raw material price volatility and the need for robust battery recycling infrastructure, the market outlook remains highly optimistic. Supportive government policies encouraging domestic production and electric mobility adoption are further strengthening market expansion. The forecast period, from the base year of 2025, projects significant market expansion, offering lucrative opportunities for both domestic and international companies. Strategic investments in R&D and a focus on sustainable manufacturing practices will be critical for sustained success.

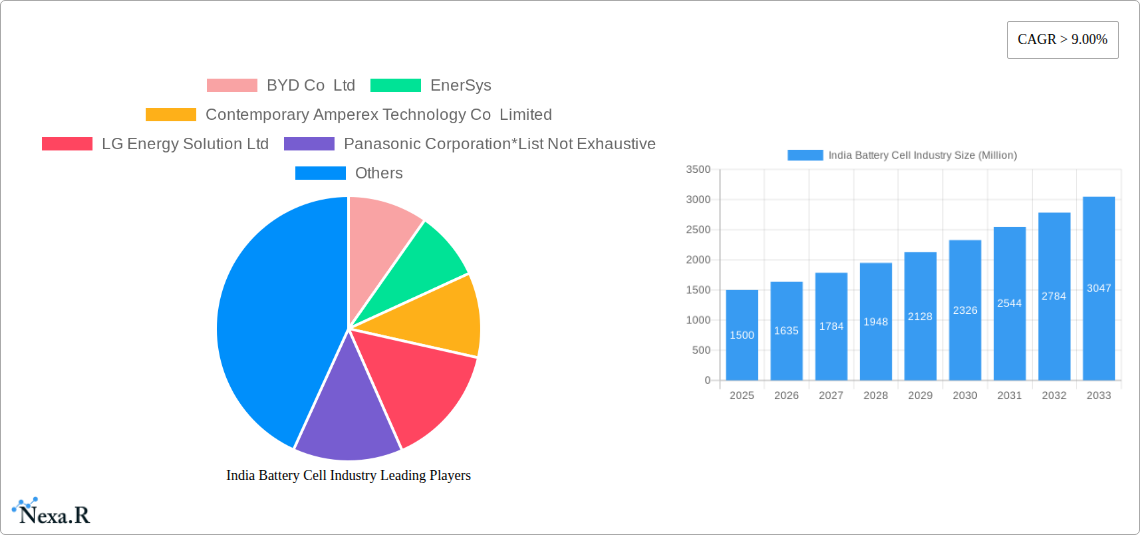

India Battery Cell Industry Company Market Share

This report offers an in-depth analysis of the Indian battery cell industry, covering market dynamics, growth trends, key players, and future projections. It examines prismatic, cylindrical, and pouch cell types across automotive, industrial, portable, power tools, and SLI battery applications. This research is an indispensable resource for industry professionals, investors, and stakeholders navigating this dynamic market. The analysis covers the period from 2019 to 2033, with the base year as 2025 and a forecast period extending to 2033. Market valuations are presented in units of billion.

India Battery Cell Industry Market Dynamics & Structure

The Indian battery cell market is experiencing significant growth driven by increasing demand for electric vehicles (EVs), renewable energy storage, and portable electronic devices. Market concentration is currently moderate, with a few dominant players and several emerging startups. Technological innovation, particularly in lithium-ion battery chemistry and solid-state battery technology, is a key driver. Favorable government policies promoting domestic manufacturing and adoption of EVs are further boosting the market. However, high raw material costs, supply chain disruptions, and a lack of skilled workforce present challenges. The competitive landscape includes both domestic and international players engaged in mergers and acquisitions (M&A) to expand their market share and technological capabilities. The estimated number of M&A deals in the period 2019-2024 is xx.

- Market Concentration: Moderate, with a few large players holding significant market share (estimated at xx% combined in 2024).

- Technological Innovation: Focus on improving energy density, lifespan, safety, and reducing costs. Solid-state batteries are emerging as a key area of focus.

- Regulatory Framework: Government initiatives promoting EV adoption and domestic manufacturing are creating a favorable environment.

- Competitive Product Substitutes: Nickel-metal hydride (NiMH) and lead-acid batteries still hold a significant share in certain applications, but are being gradually replaced by lithium-ion batteries.

- End-User Demographics: Growth is fueled by rising disposable incomes, increasing urbanization, and a growing awareness of environmental concerns.

- M&A Trends: Strategic acquisitions and joint ventures are common, reflecting the need for technological advancements and market expansion.

India Battery Cell Industry Growth Trends & Insights

The Indian battery cell market exhibits robust growth, driven by a confluence of factors. The market size increased from xx million units in 2019 to xx million units in 2024, experiencing a Compound Annual Growth Rate (CAGR) of xx%. This growth is primarily driven by the increasing adoption of EVs, propelled by government incentives and rising fuel prices. Technological advancements, such as improved battery chemistry and energy density, further enhance market appeal. Consumer behavior is shifting towards greener and more sustainable options, boosting demand for electric vehicles and, consequently, battery cells. Market penetration in the EV segment is expected to reach xx% by 2033. Further technological disruptions, such as solid-state batteries, are poised to revolutionize the sector in the coming years.

Dominant Regions, Countries, or Segments in India Battery Cell Industry

The automotive battery segment dominates the Indian battery cell market, driven by the government's push for electric vehicle adoption and rapid growth in the automotive sector. Within battery types, lithium-ion batteries, particularly prismatic and cylindrical cells, hold the largest market share due to their high energy density and suitability for various applications. The major growth drivers include government policies encouraging domestic manufacturing (Production Linked Incentive schemes) and supportive infrastructure developments such as charging stations and battery swapping networks. States like Maharashtra, Tamil Nadu, and Gujarat are leading the way in attracting battery cell manufacturing investments due to existing industrial infrastructure and favorable policies.

- Key Drivers:

- Government policies promoting EV adoption (FAME II scheme).

- Increasing demand for EVs due to rising fuel prices and environmental concerns.

- Growth in the renewable energy sector requiring energy storage solutions.

- Dominant Segments: Automotive Batteries (xx million units in 2024), Prismatic cells (xx million units in 2024), and Cylindrical cells (xx million units in 2024).

India Battery Cell Industry Product Landscape

The Indian battery cell market showcases a diverse range of products catering to various applications. Technological advancements focus on improving energy density, cycle life, safety, and fast-charging capabilities. Key innovations include the incorporation of advanced materials such as graphene and silicon in electrode materials to enhance performance. Product differentiation strategies emphasize cost-effectiveness, tailored solutions for specific applications (e.g., high-power batteries for EVs, long-life batteries for stationary storage), and improved safety features.

Key Drivers, Barriers & Challenges in India Battery Cell Industry

Key Drivers:

- Government Policies: Incentive schemes for EV adoption and domestic manufacturing are driving market growth.

- Technological Advancements: Improvements in battery chemistry and manufacturing processes are leading to enhanced performance and reduced costs.

- Rising Demand for EVs: Increasing fuel prices and environmental concerns are boosting the demand for electric vehicles.

Challenges & Restraints:

- Raw Material Dependence: India's reliance on imports for key raw materials like lithium poses a significant supply chain challenge.

- Regulatory Hurdles: Complex regulatory processes and standardization issues can slow down market development.

- High Capital Investment: Setting up battery manufacturing facilities requires substantial capital investment, acting as a barrier to entry for some players.

Emerging Opportunities in India Battery Cell Industry

- Growth in Renewable Energy Storage: The expanding renewable energy sector creates a significant opportunity for battery storage solutions.

- Demand for E-mobility Solutions: The burgeoning two-wheeler and three-wheeler electric vehicle market presents an untapped market.

- Innovation in Battery Technologies: Opportunities exist for developing next-generation battery technologies, such as solid-state and sodium-ion batteries.

Growth Accelerators in the India Battery Cell Industry

Technological breakthroughs in battery chemistry and manufacturing techniques, coupled with strategic partnerships between domestic and international players, are driving long-term growth. Expansion into new applications, such as grid-scale energy storage and microgrids, also presents lucrative opportunities. Government support for infrastructure development and skill development further accelerates the market's upward trajectory.

Key Players Shaping the India Battery Cell Industry Market

- BYD Co Ltd

- EnerSys

- Contemporary Amperex Technology Co Limited

- LG Energy Solution Ltd

- Panasonic Corporation

- GS Yuasa Corporation

- Duracell Inc

Notable Milestones in India Battery Cell Industry Sector

- May 2022: Nordische Technologies launched an Aluminium-Graphene pouch cell battery.

- Jan 2022: Reliance Industries acquired Faradion, a UK-based sodium-ion battery developer.

In-Depth India Battery Cell Industry Market Outlook

The future of the Indian battery cell industry is bright, with significant growth potential driven by continued government support, technological innovations, and increasing demand for EVs and energy storage solutions. Strategic partnerships and investments in domestic manufacturing will be crucial for realizing this potential. The market is poised for substantial expansion, driven by the adoption of advanced battery technologies and the increasing focus on sustainability.

India Battery Cell Industry Segmentation

-

1. Type

- 1.1. Prismatic

- 1.2. Cylindrical

- 1.3. Pouch

-

2. Application

- 2.1. Automotive Batteries

- 2.2. Industrial Batteries

- 2.3. Portable Batteries

- 2.4. Power Tools Batteries

- 2.5. SLI Batteries

- 2.6. Others

India Battery Cell Industry Segmentation By Geography

- 1. India

India Battery Cell Industry Regional Market Share

Geographic Coverage of India Battery Cell Industry

India Battery Cell Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.48% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Prismatic

- 5.1.2. Cylindrical

- 5.1.3. Pouch

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Automotive Batteries

- 5.2.2. Industrial Batteries

- 5.2.3. Portable Batteries

- 5.2.4. Power Tools Batteries

- 5.2.5. SLI Batteries

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. India

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. India Battery Cell Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Prismatic

- 6.1.2. Cylindrical

- 6.1.3. Pouch

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Automotive Batteries

- 6.2.2. Industrial Batteries

- 6.2.3. Portable Batteries

- 6.2.4. Power Tools Batteries

- 6.2.5. SLI Batteries

- 6.2.6. Others

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 BYD Co Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 EnerSys

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Contemporary Amperex Technology Co Limited

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 LG Energy Solution Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Panasonic Corporation*List Not Exhaustive

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 GS Yuasa Corporation

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Duracell Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.1 BYD Co Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: India Battery Cell Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: India Battery Cell Industry Share (%) by Company 2025

List of Tables

- Table 1: India Battery Cell Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: India Battery Cell Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 3: India Battery Cell Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: India Battery Cell Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 5: India Battery Cell Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 6: India Battery Cell Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Battery Cell Industry?

The projected CAGR is approximately 11.48%.

2. Which companies are prominent players in the India Battery Cell Industry?

Key companies in the market include BYD Co Ltd, EnerSys, Contemporary Amperex Technology Co Limited, LG Energy Solution Ltd, Panasonic Corporation*List Not Exhaustive, GS Yuasa Corporation, Duracell Inc.

3. What are the main segments of the India Battery Cell Industry?

The market segments include Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 10.45 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Demand for Natural Gas and Developing Gas Infrastructure 4.; Increasing Offshore Oil & Gas Exploration Activities.

6. What are the notable trends driving market growth?

Prismatic cell Segment is Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Adoption of Cleaner Alternatives4.; High Volatility of Crude Oil Prices.

8. Can you provide examples of recent developments in the market?

In May 2022, India-based start-up, Nordische Technologies, have launched an Aluminium-Graphene pouch cell battery for consumer electronics, gadgets, and future EV technology in association with the Central Institute of Petrochemicals Engineering and Technology (CIPET), Bengaluru.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Battery Cell Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Battery Cell Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Battery Cell Industry?

To stay informed about further developments, trends, and reports in the India Battery Cell Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence