Key Insights

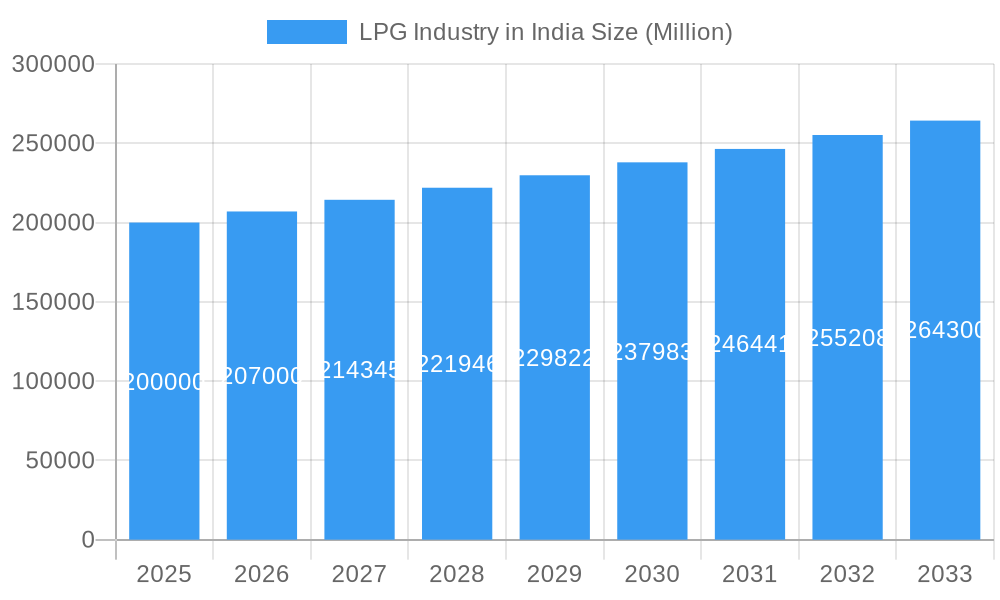

The Indian LPG market is forecasted to reach $136.548 billion by 2033, driven by a Compound Annual Growth Rate (CAGR) of 4.71% from the base year 2025. Key growth catalysts include rapid urbanization, rising disposable incomes boosting residential and commercial energy demand, and government-led initiatives promoting cleaner cooking fuels. The residential and commercial sectors are the primary demand drivers, supported by population growth and an expanding middle class. The industrial sector offers growth potential, particularly where natural gas infrastructure is limited. Market challenges include the volatility of crude oil prices impacting LPG affordability and competition from alternative fuels such as biogas and electricity. Leading companies like Indian Oil Corporation Ltd, Bharat Petroleum Corporation Limited, and Hindustan Petroleum Corporation Limited are enhancing distribution networks and exploring new growth avenues, including efficient LPG usage promotion and specialized industrial blends.

LPG Industry in India Market Size (In Billion)

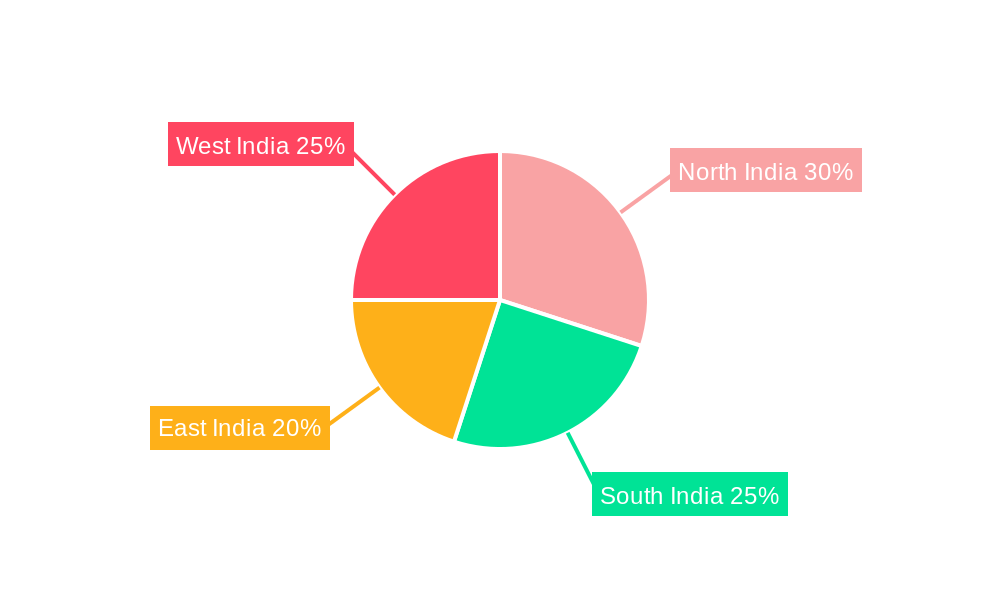

LPG's reliance on crude oil production underscores its susceptibility to global price volatility. Consumption patterns exhibit regional variations, with North and West India potentially leading due to higher population density and industrial activity. Future market expansion is anticipated in underdeveloped regions. Strategic imperatives for LPG providers will likely encompass targeted segment marketing, sustainable supply chain management, and proactive mitigation of crude oil price fluctuations. An increasing focus on environmental sustainability may foster innovation in alternative LPG production methods and promote efficient use technologies.

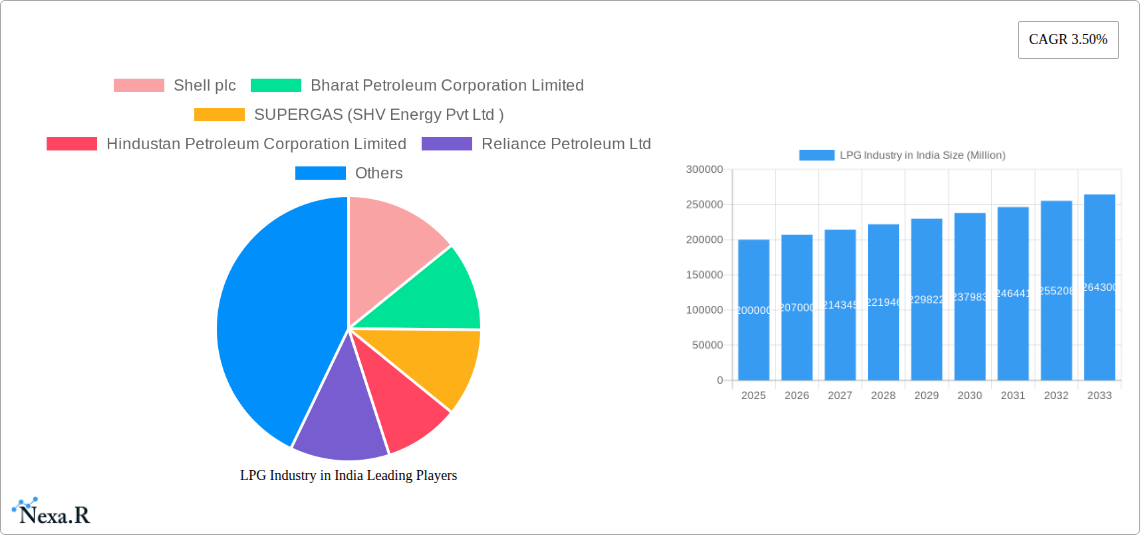

LPG Industry in India Company Market Share

LPG Industry in India: A Comprehensive Market Report (2019-2033)

This comprehensive report provides a detailed analysis of the LPG industry in India, covering market dynamics, growth trends, key players, and future outlook. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report is an essential resource for industry professionals, investors, and strategic decision-makers. The report utilizes high-impact keywords to enhance search engine optimization, ensuring maximum visibility and engagement. The report segments the market by source of production (Crude Oil, Natural Gas Liquids) and application (Residential & Commercial, Industrial, Autofuels, Other Applications), providing a granular view of the market landscape.

Key Topics Covered: Market size (Million Units), CAGR, Market Share, M&A activity, Technological advancements, Regulatory landscape, Key players and their strategies, and Future growth potential.

LPG Industry in India Market Dynamics & Structure

The Indian LPG market is characterized by a mix of public and private sector players, resulting in a moderately concentrated market structure. While Indian Oil Corporation Ltd, Bharat Petroleum Corporation Limited, and Hindustan Petroleum Corporation Limited dominate the market with a combined market share of approximately xx%, companies like Shell plc, SUPERGAS (SHV Energy Pvt Ltd), Reliance Petroleum Ltd, TotalEnergies SE, Eastern Gases Lt, and Jyothi Gas Pvt Ltd are increasingly contributing to market competitiveness. Technological innovation is driven by the need for improved efficiency in LPG production, distribution, and safety. Regulatory frameworks, including those related to pricing and safety standards, significantly impact market dynamics. The market also faces competition from alternative fuels, particularly CNG in the transportation sector. End-user demographics, notably the rising middle class and increased urbanization, are key growth drivers. M&A activity has been relatively limited in recent years, with xx major deals recorded between 2019 and 2024.

- Market Concentration: Moderately concentrated, with top 3 players holding approximately xx% market share.

- Technological Innovation: Focus on improving efficiency in production, distribution, and safety.

- Regulatory Framework: Significant influence on pricing and safety standards.

- Competitive Substitutes: CNG and other alternative fuels pose competition.

- End-User Demographics: Rising middle class and urbanization are key growth drivers.

- M&A Trends: xx major deals between 2019 and 2024.

- Innovation Barriers: High initial investment costs, stringent safety regulations.

LPG Industry in India Growth Trends & Insights

The Indian LPG market has witnessed robust growth over the historical period (2019-2024), with a CAGR of xx%. This growth is primarily attributed to rising energy demand, increasing household penetration of LPG, and government initiatives promoting LPG adoption in rural areas. The residential and commercial sector remains the largest segment, accounting for approximately xx% of total consumption in 2024. Technological disruptions, such as the introduction of smart meters and automated dispensing systems, are improving efficiency and consumer experience. Consumer behavior shifts towards safer and more convenient fuel options are also driving market expansion. The market is expected to continue its growth trajectory during the forecast period (2025-2033), with a projected CAGR of xx%, driven by factors such as sustained economic growth, increasing urbanization, and government initiatives to expand LPG infrastructure, particularly in rural areas. Market penetration is expected to reach xx% by 2033.

Dominant Regions, Countries, or Segments in LPG Industry in India

The Northern and Western regions of India are currently the dominant markets for LPG consumption, driven by higher population density, industrial activity, and robust infrastructure. The Residential & Commercial segment constitutes the largest application area, accounting for approximately xx% of the total market in 2024. Growth in this segment is fueled by rising household incomes and increasing urbanization. Crude oil remains the primary source of LPG production, although the share of Natural Gas Liquids is expected to increase in the coming years due to government initiatives promoting domestic gas production.

- Key Drivers for Northern & Western Regions: High population density, industrial activities, robust infrastructure.

- Key Drivers for Residential & Commercial Segment: Rising household incomes and urbanization.

- Key Drivers for Crude Oil Source: Established infrastructure and readily available feedstock.

- Growth Potential: Significant untapped potential exists in rural areas and the industrial sector.

LPG Industry in India Product Landscape

The LPG product landscape is relatively mature, with most players offering standard LPG cylinders of varying sizes. However, recent innovations include the introduction of enhanced safety features, such as improved valve technology, and smart meters for accurate consumption tracking. Further innovation focuses on developing more efficient and eco-friendly production processes. Unique selling propositions center around safety features, convenience, and cost-effectiveness.

Key Drivers, Barriers & Challenges in LPG Industry in India

Key Drivers:

- Increasing urbanization and rising disposable incomes.

- Government initiatives promoting LPG adoption in rural areas.

- Technological advancements leading to improved efficiency and safety.

Challenges:

- Fluctuations in crude oil prices impacting LPG pricing.

- Competition from alternative fuels like CNG.

- Infrastructure bottlenecks in LPG distribution, especially in rural areas.

Emerging Opportunities in LPG Industry in India

- Expanding LPG penetration in rural areas through targeted government initiatives.

- Growing demand for LPG in the industrial sector.

- Potential for innovative applications of LPG, such as in power generation.

- Rise of cleaner and more efficient LPG technologies.

Growth Accelerators in the LPG Industry in India Industry

Long-term growth will be driven by continued government support for LPG expansion, technological advancements in production and distribution, and strategic partnerships between LPG companies and infrastructure providers. Expanding into new applications, such as power generation in remote areas, presents a significant opportunity for growth.

Key Players Shaping the LPG Industry in India Market

- Shell plc

- Bharat Petroleum Corporation Limited

- SUPERGAS (SHV Energy Pvt Ltd)

- Hindustan Petroleum Corporation Limited

- Reliance Petroleum Ltd

- TotalEnergies SE

- Indian Oil Corporation Ltd

- Eastern Gases Lt

- Jyothi Gas Pvt Ltd

Notable Milestones in LPG Industry in India Sector

- February 2022: Indian Oil Corp (IOC) announced plans to construct three new plants in Northeast India, increasing LPG bottling capacity by 53% (8 crore cylinders annually by 2030); investment: INR 325-350 crore.

In-Depth LPG Industry in India Market Outlook

The Indian LPG market is poised for sustained growth driven by factors such as rising energy demand, increasing urbanization, and government support. Strategic partnerships, technological innovation, and expansion into new applications will play a key role in shaping future market dynamics. The market offers lucrative opportunities for both existing and new players, particularly those focusing on efficiency, safety, and sustainable practices.

LPG Industry in India Segmentation

-

1. Source of Production

- 1.1. Crude Oil

- 1.2. Natural Gas Liquids

-

2. Application

- 2.1. Residential & Commercial

- 2.2. Industrial

- 2.3. Autofuels

- 2.4. Other Applications

LPG Industry in India Segmentation By Geography

-

1. Asia Pacific

- 1.1. India

LPG Industry in India Regional Market Share

Geographic Coverage of LPG Industry in India

LPG Industry in India REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.71% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Source of Production

- 5.1.1. Crude Oil

- 5.1.2. Natural Gas Liquids

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Residential & Commercial

- 5.2.2. Industrial

- 5.2.3. Autofuels

- 5.2.4. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Source of Production

- 6. Global LPG Industry in India Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Source of Production

- 6.1.1. Crude Oil

- 6.1.2. Natural Gas Liquids

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Residential & Commercial

- 6.2.2. Industrial

- 6.2.3. Autofuels

- 6.2.4. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Source of Production

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Shell plc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Bharat Petroleum Corporation Limited

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 SUPERGAS (SHV Energy Pvt Ltd )

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Hindustan Petroleum Corporation Limited

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Reliance Petroleum Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 TotalEnergies SE

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Indian Oil Corporation Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Eastern Gases Lt

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Jyothi Gas Pvt Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Shell plc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Global LPG Industry in India Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Asia Pacific LPG Industry in India Revenue (billion), by Source of Production 2025 & 2033

- Figure 3: Asia Pacific LPG Industry in India Revenue Share (%), by Source of Production 2025 & 2033

- Figure 4: Asia Pacific LPG Industry in India Revenue (billion), by Application 2025 & 2033

- Figure 5: Asia Pacific LPG Industry in India Revenue Share (%), by Application 2025 & 2033

- Figure 6: Asia Pacific LPG Industry in India Revenue (billion), by Country 2025 & 2033

- Figure 7: Asia Pacific LPG Industry in India Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global LPG Industry in India Revenue billion Forecast, by Source of Production 2020 & 2033

- Table 2: Global LPG Industry in India Revenue billion Forecast, by Application 2020 & 2033

- Table 3: Global LPG Industry in India Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global LPG Industry in India Revenue billion Forecast, by Source of Production 2020 & 2033

- Table 5: Global LPG Industry in India Revenue billion Forecast, by Application 2020 & 2033

- Table 6: Global LPG Industry in India Revenue billion Forecast, by Country 2020 & 2033

- Table 7: India LPG Industry in India Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the LPG Industry in India?

The projected CAGR is approximately 4.71%.

2. Which companies are prominent players in the LPG Industry in India?

Key companies in the market include Shell plc, Bharat Petroleum Corporation Limited, SUPERGAS (SHV Energy Pvt Ltd ), Hindustan Petroleum Corporation Limited, Reliance Petroleum Ltd, TotalEnergies SE, Indian Oil Corporation Ltd, Eastern Gases Lt, Jyothi Gas Pvt Ltd.

3. What are the main segments of the LPG Industry in India?

The market segments include Source of Production, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 136.548 billion as of 2022.

5. What are some drivers contributing to market growth?

Declining Cost of Wind Energy. Increasing Investments in Wind Energy Power Generation Projects.

6. What are the notable trends driving market growth?

LPG Extracted From Natural Gas is Expected to Have Considerable Growth Rate.

7. Are there any restraints impacting market growth?

Increasing Adoption of Alternate Clean Power Sources.

8. Can you provide examples of recent developments in the market?

In February 2022, Indian Oil Corp (IOC) announced the plans to construct three new plants in Northeast India to increase its LPG bottling capacity by nearly 53% or to 8 crore cylinders annually by 2030, to meet the growing demand in the region. Furthermore, the total investment in the plant expansion is likely to range between INR 325-350 crore.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "LPG Industry in India," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the LPG Industry in India report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the LPG Industry in India?

To stay informed about further developments, trends, and reports in the LPG Industry in India, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence