Key Insights

The North American rotor blade market is experiencing robust growth, driven by the increasing demand for renewable energy sources and supportive government policies promoting wind power adoption. With a Compound Annual Growth Rate (CAGR) exceeding 6%, the market is projected to reach significant value by 2033. The onshore segment currently dominates, owing to established infrastructure and easier access for installation. However, the offshore segment is poised for rapid expansion, fueled by technological advancements enabling larger, more efficient turbines in deeper waters. The shift towards carbon fiber blade materials is a key trend, enhancing durability, lifespan, and energy capture efficiency compared to traditional glass fiber. While the high initial investment cost for these advanced materials presents a restraint, the long-term benefits outweigh the initial expenditure, contributing to overall market growth. Key players like Vestas, Siemens Gamesa, and GE Renewable Energy (through LM Wind Power) are actively engaged in research and development, driving innovation and competition within the sector. This competitive landscape fosters price optimization and technological advancements that benefit the entire market. The United States, as the largest market within North America, is experiencing the highest growth, followed by Canada and Mexico.

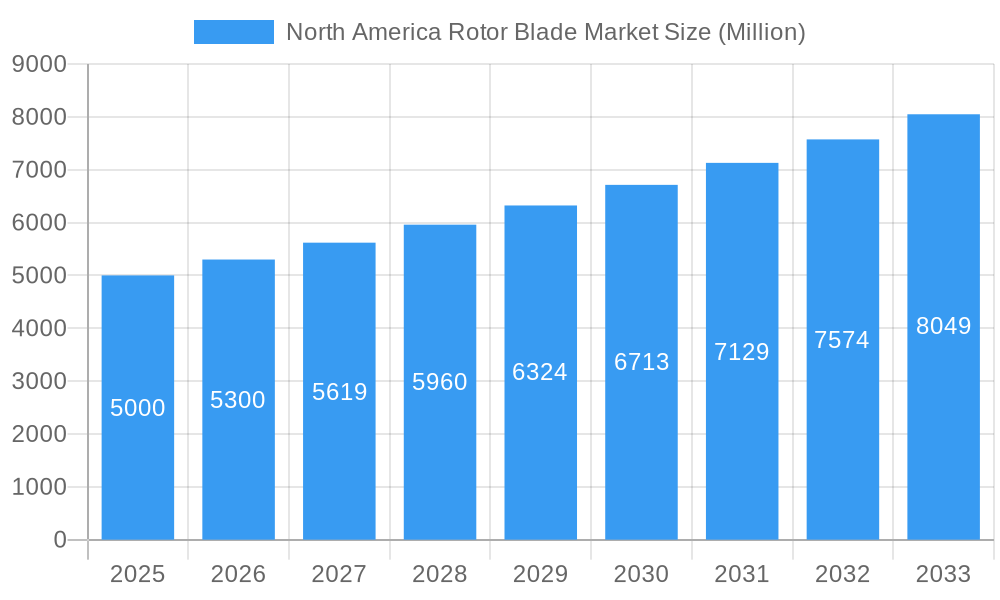

North America Rotor Blade Market Market Size (In Billion)

Market expansion is further propelled by favorable regulatory frameworks and tax incentives designed to encourage the widespread deployment of wind energy projects across North America. This regulatory support, combined with increasing electricity demand and the need for decarbonization efforts, creates a positive feedback loop, fueling further market expansion in the coming years. The ongoing development and refinement of blade designs, particularly those incorporating advanced materials and aerodynamic principles, are central to this growth story. Continuous improvement in manufacturing processes, along with economies of scale, are also anticipated to contribute to lower production costs, thus increasing market accessibility and ultimately bolstering the growth trajectory of the North American rotor blade market throughout the forecast period.

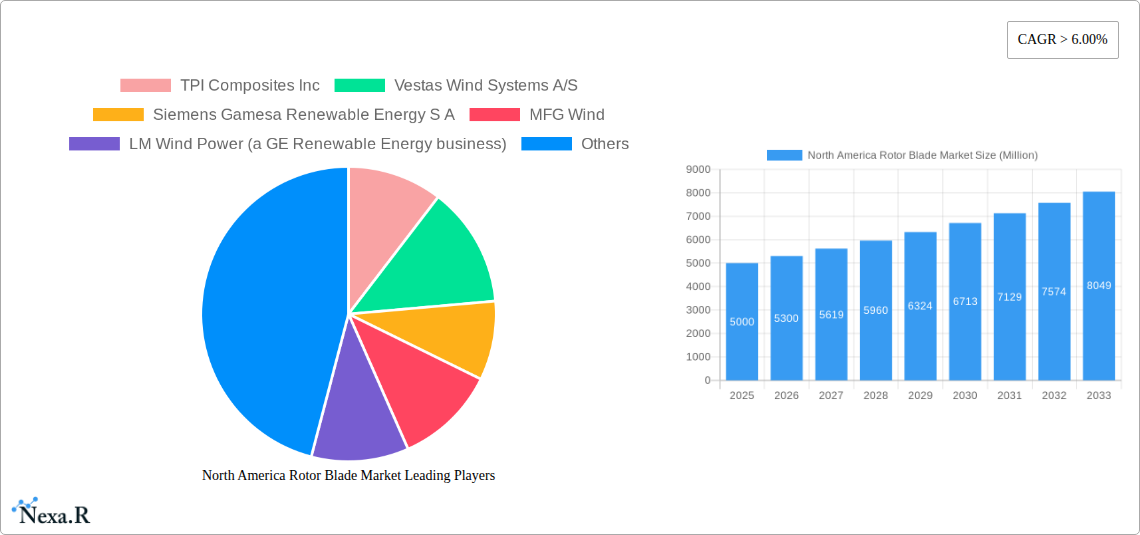

North America Rotor Blade Market Company Market Share

North America Rotor Blade Market: A Comprehensive Report (2019-2033)

This comprehensive report provides an in-depth analysis of the North America rotor blade market, encompassing market dynamics, growth trends, dominant segments, and key players. With a study period spanning 2019-2033 (base year 2025), this report offers valuable insights for industry professionals, investors, and strategic decision-makers. The report projects the market size to reach xx Million units by 2033.

North America Rotor Blade Market Dynamics & Structure

The North American rotor blade market is characterized by a moderately concentrated landscape, with key players such as TPI Composites Inc, Vestas Wind Systems A/S, Siemens Gamesa Renewable Energy S.A., and GE Renewable Energy (LM Wind Power) holding significant market share. Market concentration is influenced by technological advancements, economies of scale in manufacturing, and the increasing demand for larger and more efficient wind turbines. Regulatory frameworks, particularly those promoting renewable energy adoption, are crucial drivers. While glass fiber remains the dominant blade material, the increasing adoption of carbon fiber reflects a push for enhanced performance and longevity. The market witnesses consistent M&A activity, primarily focused on strengthening technological capabilities and expanding market reach. The total value of M&A deals in the sector during the historical period (2019-2024) is estimated at xx Million units.

- Market Concentration: Moderately concentrated, with top 5 players holding approximately xx% market share in 2024.

- Technological Innovation: Continuous R&D in blade design, materials, and manufacturing processes is driving efficiency gains and cost reductions. Key barriers include high R&D costs and the need for specialized expertise.

- Regulatory Landscape: Supportive government policies and incentives for renewable energy are crucial in driving market growth.

- Competitive Landscape: Intense competition exists among established players and new entrants, driven by technological innovation and price competition.

- End-User Demographics: The primary end-users are wind turbine manufacturers, with growing demand from both onshore and offshore wind farms.

- M&A Trends: Strategic acquisitions are common, focused on expanding production capacity and technological portfolios.

North America Rotor Blade Market Growth Trends & Insights

The North America rotor blade market has witnessed robust growth during the historical period (2019-2024), driven by the increasing adoption of wind energy as a cleaner alternative to fossil fuels. This growth is projected to continue through 2033, driven by supportive government policies, decreasing technology costs, and the increasing focus on decarbonization efforts. The market is expected to experience a CAGR of xx% during the forecast period (2025-2033), resulting in a substantial increase in market size. Technological advancements, such as the use of advanced materials and improved blade designs, are further boosting market growth. Consumer behavior shifts toward environmentally sustainable energy sources are also significantly influencing market adoption rates. Market penetration has increased from xx% in 2019 to xx% in 2024, and is projected to reach xx% by 2033.

Dominant Regions, Countries, or Segments in North America Rotor Blade Market

The onshore wind segment dominates the North American rotor blade market, owing to the extensive land availability and established infrastructure. However, the offshore wind segment is experiencing rapid growth due to the government's strong support and the substantial untapped potential in coastal regions. In terms of blade material, glass fiber currently holds the largest market share, although carbon fiber is rapidly gaining traction due to its superior performance capabilities. Specific regional dominance within North America may vary depending on the segment, however states with robust renewable energy policies and existing wind power projects tend to show higher adoption rates.

- Onshore Wind: High market share due to established infrastructure and readily available land.

- Offshore Wind: Rapid growth driven by government support and potential for large-scale projects.

- Glass Fiber: Dominates market share due to lower cost; however, carbon fiber adoption is increasing.

- Key Drivers: Favorable government policies, increasing demand for renewable energy, and decreasing costs of wind energy technologies.

North America Rotor Blade Market Product Landscape

The North American rotor blade market is characterized by a diverse range of products, including blades of varying sizes and designs, customized to meet the specific requirements of different wind turbine models. Technological advancements focus on improving blade efficiency, reducing weight, and enhancing durability through the use of advanced materials and design optimization techniques. Key innovations include lighter blades for reduced transportation and installation costs, improved aerodynamic designs for enhanced energy capture, and the use of advanced materials like carbon fiber for better performance and extended lifespan. The focus is on increasing the power output per unit area while reducing the overall cost of energy.

Key Drivers, Barriers & Challenges in North America Rotor Blade Market

Key Drivers:

- Increasing demand for renewable energy to meet climate change targets.

- Government support through subsidies and tax incentives.

- Technological advancements leading to improved blade efficiency and cost reductions.

- Expansion of offshore wind projects.

Key Challenges:

- Supply chain disruptions impacting the availability of raw materials and components.

- High upfront investment costs associated with wind turbine projects.

- Intense competition among blade manufacturers leading to price pressure.

- Regulatory hurdles and permitting delays for offshore wind projects. The estimated impact of supply chain issues is a xx% increase in blade costs in 2024.

Emerging Opportunities in North America Rotor Blade Market

- Growing demand for larger and more efficient blades for offshore wind farms.

- Development of innovative blade materials such as hybrid composites.

- Expansion into new markets in the United States and Canada.

- Increased focus on blade recycling and sustainability.

Growth Accelerators in the North America Rotor Blade Market Industry

The long-term growth of the North American rotor blade market will be significantly influenced by technological breakthroughs in material science and blade design, leading to more efficient and cost-effective solutions. Strategic partnerships between blade manufacturers, wind turbine OEMs, and energy companies will streamline supply chains and enhance market reach. Expansion into untapped markets, particularly within the offshore wind sector, will offer immense growth opportunities. Furthermore, government initiatives promoting renewable energy and improving grid infrastructure will play a pivotal role in boosting market expansion and adoption.

Key Players Shaping the North America Rotor Blade Market Market

- TPI Composites Inc

- Vestas Wind Systems A/S

- Siemens Gamesa Renewable Energy S.A.

- MFG Wind

- LM Wind Power (a GE Renewable Energy business)

- Sinoma wind power blade Co Ltd

- Enercon Gmb

- Nordex SE

- Aeris Energy

Notable Milestones in North America Rotor Blade Market Sector

- October 2022: Ventus launched TripleCMAS, a next-generation rotor monitoring system, enhancing wind turbine efficiency and maintenance.

- May 2022: GE launched its 3MW Sierra onshore wind turbine with a 140-meter rotor, boosting domestic manufacturing and capacity.

In-Depth North America Rotor Blade Market Outlook

The North America rotor blade market is poised for sustained growth over the forecast period, driven by ongoing investments in renewable energy infrastructure, supportive government policies, and technological advancements leading to more efficient and cost-effective wind energy solutions. Strategic partnerships and M&A activity will further consolidate the market and accelerate innovation. The expansion of the offshore wind sector, particularly in the United States, represents a major growth opportunity, while ongoing developments in blade materials and design will enhance performance and reduce costs, unlocking significant market potential.

North America Rotor Blade Market Segmentation

-

1. Location of Deployment

- 1.1. Onshore

- 1.2. Offshore

-

2. Blade Material

- 2.1. Carbon Fiber

- 2.2. Glass Fiber

- 2.3. Other Blade Materials

-

3. Geography

- 3.1. United States

- 3.2. Canada

- 3.3. Mexico

North America Rotor Blade Market Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Mexico

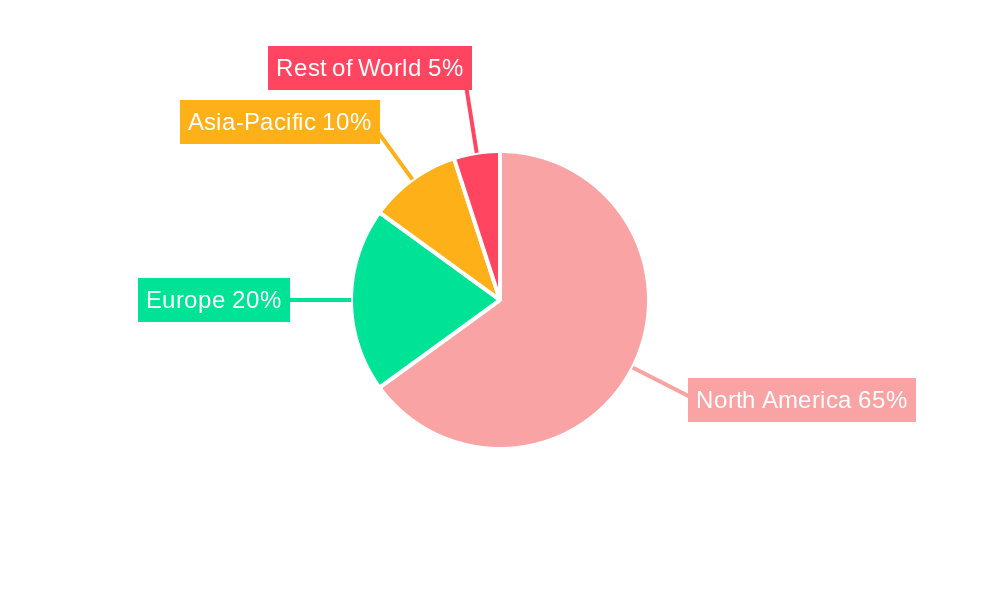

North America Rotor Blade Market Regional Market Share

Geographic Coverage of North America Rotor Blade Market

North America Rotor Blade Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of > 6.00% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 5.1.1. Onshore

- 5.1.2. Offshore

- 5.2. Market Analysis, Insights and Forecast - by Blade Material

- 5.2.1. Carbon Fiber

- 5.2.2. Glass Fiber

- 5.2.3. Other Blade Materials

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. United States

- 5.3.2. Canada

- 5.3.3. Mexico

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Mexico

- 5.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 6. North America Rotor Blade Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 6.1.1. Onshore

- 6.1.2. Offshore

- 6.2. Market Analysis, Insights and Forecast - by Blade Material

- 6.2.1. Carbon Fiber

- 6.2.2. Glass Fiber

- 6.2.3. Other Blade Materials

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. United States

- 6.3.2. Canada

- 6.3.3. Mexico

- 6.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 7. United States North America Rotor Blade Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 7.1.1. Onshore

- 7.1.2. Offshore

- 7.2. Market Analysis, Insights and Forecast - by Blade Material

- 7.2.1. Carbon Fiber

- 7.2.2. Glass Fiber

- 7.2.3. Other Blade Materials

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. United States

- 7.3.2. Canada

- 7.3.3. Mexico

- 7.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 8. Canada North America Rotor Blade Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 8.1.1. Onshore

- 8.1.2. Offshore

- 8.2. Market Analysis, Insights and Forecast - by Blade Material

- 8.2.1. Carbon Fiber

- 8.2.2. Glass Fiber

- 8.2.3. Other Blade Materials

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. United States

- 8.3.2. Canada

- 8.3.3. Mexico

- 8.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 9. Mexico North America Rotor Blade Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 9.1.1. Onshore

- 9.1.2. Offshore

- 9.2. Market Analysis, Insights and Forecast - by Blade Material

- 9.2.1. Carbon Fiber

- 9.2.2. Glass Fiber

- 9.2.3. Other Blade Materials

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. United States

- 9.3.2. Canada

- 9.3.3. Mexico

- 9.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 TPI Composites Inc

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Vestas Wind Systems A/S

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 Siemens Gamesa Renewable Energy S A

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 MFG Wind

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 LM Wind Power (a GE Renewable Energy business)

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 Sinoma wind power blade Co Ltd

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 Enercon Gmb

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 Nordex SE

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 Aeris Energy

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.1 TPI Composites Inc

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: North America Rotor Blade Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: North America Rotor Blade Market Share (%) by Company 2025

List of Tables

- Table 1: North America Rotor Blade Market Revenue Million Forecast, by Location of Deployment 2020 & 2033

- Table 2: North America Rotor Blade Market Volume K Units Forecast, by Location of Deployment 2020 & 2033

- Table 3: North America Rotor Blade Market Revenue Million Forecast, by Blade Material 2020 & 2033

- Table 4: North America Rotor Blade Market Volume K Units Forecast, by Blade Material 2020 & 2033

- Table 5: North America Rotor Blade Market Revenue Million Forecast, by Geography 2020 & 2033

- Table 6: North America Rotor Blade Market Volume K Units Forecast, by Geography 2020 & 2033

- Table 7: North America Rotor Blade Market Revenue Million Forecast, by Region 2020 & 2033

- Table 8: North America Rotor Blade Market Volume K Units Forecast, by Region 2020 & 2033

- Table 9: North America Rotor Blade Market Revenue Million Forecast, by Location of Deployment 2020 & 2033

- Table 10: North America Rotor Blade Market Volume K Units Forecast, by Location of Deployment 2020 & 2033

- Table 11: North America Rotor Blade Market Revenue Million Forecast, by Blade Material 2020 & 2033

- Table 12: North America Rotor Blade Market Volume K Units Forecast, by Blade Material 2020 & 2033

- Table 13: North America Rotor Blade Market Revenue Million Forecast, by Geography 2020 & 2033

- Table 14: North America Rotor Blade Market Volume K Units Forecast, by Geography 2020 & 2033

- Table 15: North America Rotor Blade Market Revenue Million Forecast, by Country 2020 & 2033

- Table 16: North America Rotor Blade Market Volume K Units Forecast, by Country 2020 & 2033

- Table 17: North America Rotor Blade Market Revenue Million Forecast, by Location of Deployment 2020 & 2033

- Table 18: North America Rotor Blade Market Volume K Units Forecast, by Location of Deployment 2020 & 2033

- Table 19: North America Rotor Blade Market Revenue Million Forecast, by Blade Material 2020 & 2033

- Table 20: North America Rotor Blade Market Volume K Units Forecast, by Blade Material 2020 & 2033

- Table 21: North America Rotor Blade Market Revenue Million Forecast, by Geography 2020 & 2033

- Table 22: North America Rotor Blade Market Volume K Units Forecast, by Geography 2020 & 2033

- Table 23: North America Rotor Blade Market Revenue Million Forecast, by Country 2020 & 2033

- Table 24: North America Rotor Blade Market Volume K Units Forecast, by Country 2020 & 2033

- Table 25: North America Rotor Blade Market Revenue Million Forecast, by Location of Deployment 2020 & 2033

- Table 26: North America Rotor Blade Market Volume K Units Forecast, by Location of Deployment 2020 & 2033

- Table 27: North America Rotor Blade Market Revenue Million Forecast, by Blade Material 2020 & 2033

- Table 28: North America Rotor Blade Market Volume K Units Forecast, by Blade Material 2020 & 2033

- Table 29: North America Rotor Blade Market Revenue Million Forecast, by Geography 2020 & 2033

- Table 30: North America Rotor Blade Market Volume K Units Forecast, by Geography 2020 & 2033

- Table 31: North America Rotor Blade Market Revenue Million Forecast, by Country 2020 & 2033

- Table 32: North America Rotor Blade Market Volume K Units Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Rotor Blade Market?

The projected CAGR is approximately > 6.00%.

2. Which companies are prominent players in the North America Rotor Blade Market?

Key companies in the market include TPI Composites Inc, Vestas Wind Systems A/S, Siemens Gamesa Renewable Energy S A, MFG Wind, LM Wind Power (a GE Renewable Energy business), Sinoma wind power blade Co Ltd, Enercon Gmb, Nordex SE, Aeris Energy.

3. What are the main segments of the North America Rotor Blade Market?

The market segments include Location of Deployment, Blade Material, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Declining Cost Of Lithium-ion Batteries4.; Increasing Adoption of Electric Vehicles.

6. What are the notable trends driving market growth?

Onshore Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Demand and Supply of Raw Materials for Battery Manufacturing.

8. Can you provide examples of recent developments in the market?

October 2022: Ventus launched TripleCMAS to convert the wind turbine rotor and swept area into a condition monitoring and alarm system. This next-generation data-driven rotor monitoring system is based on data collected wirelessly from the rotor. It will convert the rotor and the entire swept area into a measuring instrument for wind turbines.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Units.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Rotor Blade Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Rotor Blade Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Rotor Blade Market?

To stay informed about further developments, trends, and reports in the North America Rotor Blade Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence