Key Insights

The small satellite industry is experiencing robust growth, driven by increasing demand for cost-effective Earth observation, communication, and navigation solutions. The market, currently valued at approximately $XX million (assuming a reasonable market size based on industry reports and the given CAGR), is projected to expand at a Compound Annual Growth Rate (CAGR) exceeding 3% from 2025 to 2033. This growth is fueled by several key factors. Advancements in miniaturization and cheaper launch options have made deploying constellations of small satellites significantly more affordable and accessible, opening the market to a wider range of both commercial and governmental entities. The rising adoption of electric propulsion technology offers greater maneuverability and longer mission lifetimes, further enhancing the appeal of these versatile platforms. Key market segments include commercial applications (e.g., IoT, environmental monitoring), military and government operations (e.g., reconnaissance, surveillance), and diverse propulsion technologies like electric, gas-based, and liquid fuel systems. The LEO (Low Earth Orbit) segment is currently the most dominant, but MEO (Medium Earth Orbit) and GEO (Geostationary Earth Orbit) segments are expected to witness considerable growth, especially with the advancements in propulsion systems that extend the operational lifespan of satellites and enable more targeted missions.

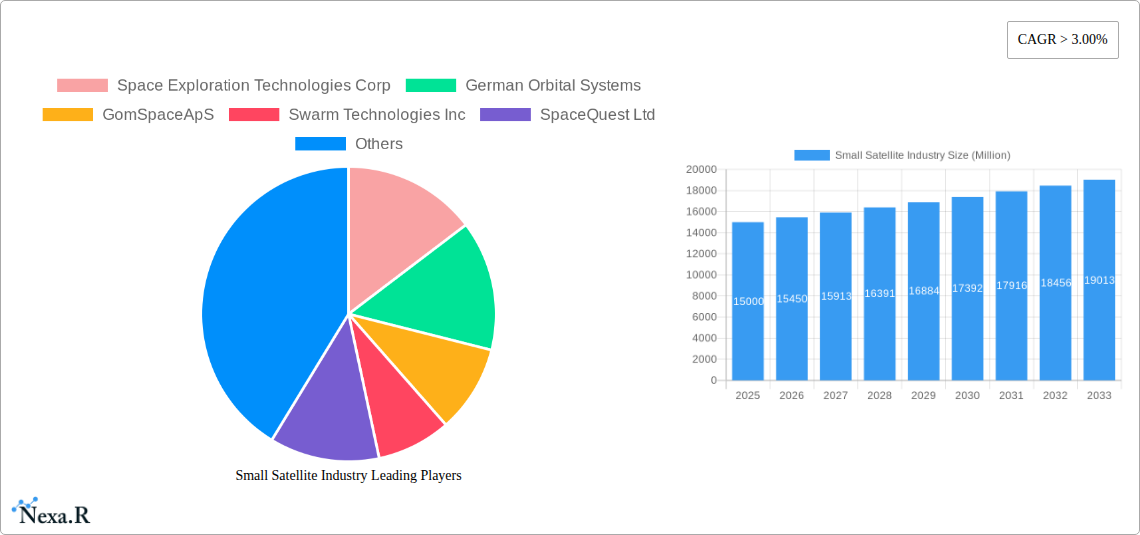

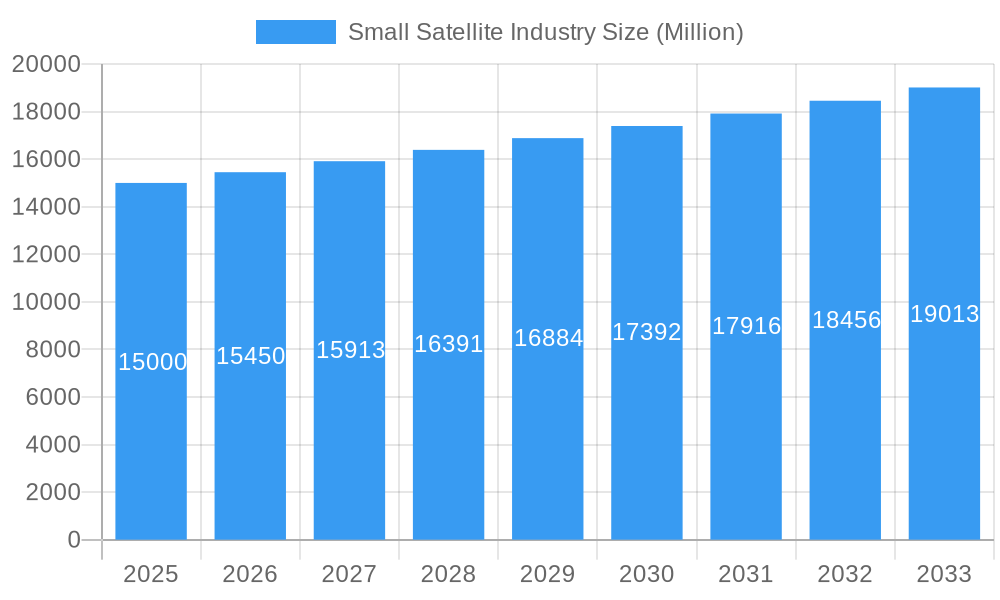

Small Satellite Industry Market Size (In Billion)

Competition in the small satellite market is intense, with established aerospace giants like Airbus SE and emerging innovative players like SpaceX, GomSpace, and Planet Labs vying for market share. While the industry faces challenges such as regulatory hurdles and the need for robust space debris mitigation strategies, the overall outlook remains positive. The continuous development of advanced sensors, improved communication technologies, and the growing need for real-time data acquisition across various sectors ensure that the demand for small satellites will continue to rise. This positive trajectory is projected to sustain the industry's growth well into the next decade and beyond, as more sophisticated applications and capabilities emerge.

Small Satellite Industry Company Market Share

Small Satellite Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the Small Satellite Industry, encompassing market dynamics, growth trends, key players, and future outlook. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report is an invaluable resource for industry professionals, investors, and strategists. The report segments the market by end-user (Commercial, Military & Government, Other), propulsion technology (Electric, Gas-based, Liquid Fuel), application (Communication, Earth Observation, Navigation, Space Observation, Others), and orbit class (GEO, LEO, MEO). The total market size in 2025 is estimated at xx Million.

Small Satellite Industry Market Dynamics & Structure

The small satellite industry is characterized by a dynamic interplay of technological innovation, evolving regulatory landscapes, and intense competition. Market concentration is relatively low, with a multitude of players vying for market share. However, larger companies like SpaceX and Airbus are consolidating their position through acquisitions and strategic partnerships. Technological advancements in miniaturization, propulsion systems, and sensor technologies are driving industry growth. Regulatory frameworks, particularly concerning spectrum allocation and orbital debris mitigation, significantly impact market expansion. The industry faces competition from traditional large satellite systems, particularly in communication applications. The increasing demand for high-resolution Earth observation data and the proliferation of IoT devices fuel market expansion. M&A activity is brisk, with larger companies acquiring smaller, specialized firms to expand their product portfolios and technological capabilities.

- Market Concentration: Moderately fragmented, with xx% market share held by the top 5 players in 2025.

- Technological Innovation Drivers: Miniaturization, advanced propulsion, AI-powered data analytics.

- Regulatory Framework: Evolving regulations concerning spectrum allocation and space debris pose challenges.

- Competitive Product Substitutes: Traditional large satellites, terrestrial communication networks.

- End-User Demographics: Growing demand from commercial sectors (Earth observation, IoT), government (defense, intelligence), and research institutions.

- M&A Trends: Increasing consolidation, with xx major M&A deals recorded between 2019 and 2024.

Small Satellite Industry Growth Trends & Insights

The small satellite industry is experiencing exponential growth, fueled by a potent combination of technological innovation, expanding market applications, and a shift towards more agile and cost-effective space solutions. The market size has surged dramatically, evolving from approximately XX Million in 2019 to an estimated XX Million by 2025. This expansion is largely attributable to the increasing adoption of small satellites across a diverse spectrum of sectors, with a particular emphasis on the commercial domain. Here, the demand for sophisticated yet affordable Earth observation data and reliable communication services is a primary catalyst.

Key technological breakthroughs, most notably the advent and widespread adoption of CubeSats and nanosatellites, have significantly lowered the barrier to entry. This democratization of space access has fostered an environment of rapid innovation and heightened competition. Furthermore, evolving consumer and enterprise behaviors, characterized by a strong preference for smaller, highly adaptable platforms that enable swift data acquisition and processing, are actively propelling industry expansion.

Looking ahead, the Compound Annual Growth Rate (CAGR) for the forecast period of 2025-2033 is projected to be an impressive XX%, signaling sustained and substantial future growth for the small satellite sector.

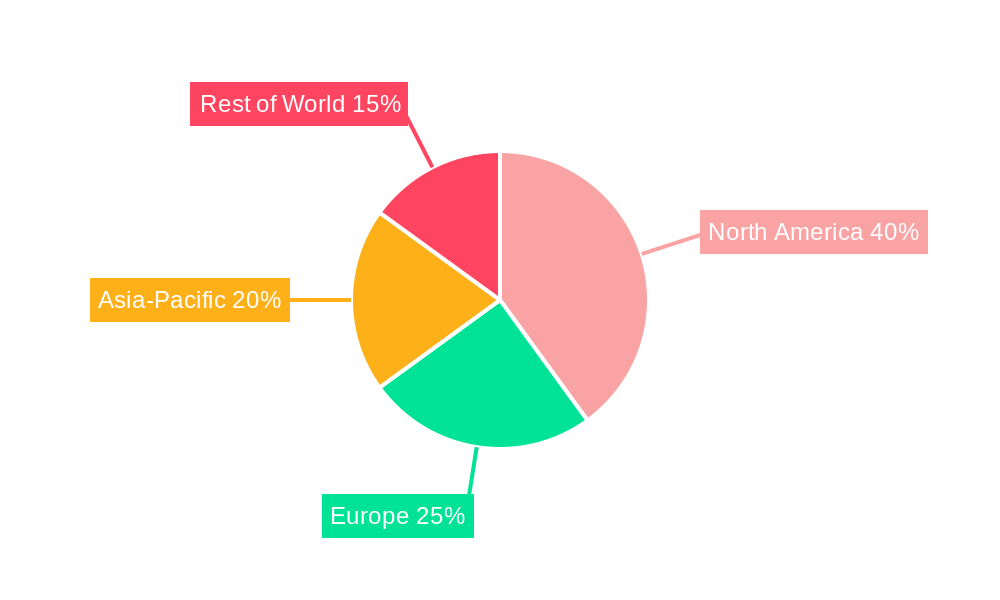

Dominant Regions, Countries, or Segments in Small Satellite Industry

Geographically, the North American region, with the United States at its forefront, commands a dominant position in the small satellite market. This leadership is underpinned by substantial government investment in ambitious space exploration initiatives, a vibrant and dynamic private sector, and a remarkably supportive and enabling regulatory framework.

Analyzing market segments, the Commercial sector stands out as the largest end-user segment. This dominance is driven by the escalating demand for high-quality Earth observation data across critical applications such as precision agriculture, real-time environmental monitoring, and sophisticated urban planning.

In terms of propulsion technology, Electric propulsion systems have captured a significant market share. This preference is due to their inherent cost-effectiveness, superior energy efficiency, and extended operational lifespan. Within the satellite orbit classes, Low Earth Orbit (LEO) satellites represent the most prevalent choice. LEO orbits are favored for their comparatively lower launch costs and their ability to facilitate faster data transmission, enhancing responsiveness and operational agility.

The Earth Observation application segment continues to lead, propelled by an ever-increasing demand for detailed and timely data from both commercial enterprises and government entities worldwide.

- Key Drivers (North America): Robust government backing for space initiatives, a flourishing private space ecosystem, and forward-thinking regulatory policies.

- Key Drivers (Commercial Segment): Surging demand for granular Earth observation data, the rapid expansion of IoT applications, and the increasing need for affordable, reliable global communication services.

- Key Drivers (Electric Propulsion): Excellent cost-efficiency, high operational efficiency, and the ability to significantly extend satellite mission duration.

- Key Drivers (LEO): Reduced launch expenses, minimized data latency, and enhanced operational flexibility for satellite constellations.

- Key Drivers (Earth Observation): Growing need for high-resolution imagery and actionable insights across a multitude of commercial and scientific applications.

Small Satellite Industry Product Landscape

The small satellite industry showcases continuous product innovation, driven by advancements in miniaturization, improved sensor technology, and enhanced propulsion systems. CubeSats, nanosatellites, and picosatellites are proliferating, enabling a wider range of applications. Key innovations include improved communication payloads, enhanced Earth observation sensors (hyperspectral, LiDAR), and miniaturized propulsion systems. These advancements improve satellite performance, extending their operational lifespan and improving data acquisition capabilities. Unique selling propositions focus on cost-effectiveness, rapid deployment capabilities, and tailored solutions for specific applications.

Key Drivers, Barriers & Challenges in Small Satellite Industry

Key Drivers:

- Technological advancements (miniaturization, improved sensors, AI).

- Increased demand for Earth observation and communication services across diverse sectors.

- Government initiatives and funding for space exploration and national security.

- Reduced launch costs due to reusable launch vehicles.

Challenges:

- Supply chain disruptions: Increased lead times and cost volatility for components impact production.

- Regulatory hurdles: Complex licensing processes and orbital debris mitigation regulations.

- Competitive pressures: Intense competition for market share and funding.

Emerging Opportunities in Small Satellite Industry

The small satellite industry is ripe with burgeoning opportunities. A significant growth area lies in the expansion of extensive satellite constellations designed to deliver ubiquitous global internet access, bridging digital divides and enhancing connectivity worldwide. The development of novel and advanced Earth observation applications, including precision agriculture for optimized crop yields, rapid disaster response, and detailed climate change monitoring, represents another exciting frontier.

Emerging economies are also presenting new markets for satellite services, offering opportunities for tailored solutions to local needs. The transformative power of Artificial Intelligence (AI) and Machine Learning (ML) is poised to revolutionize data processing and analysis from small satellites, unlocking unprecedented insights and growth potential. Furthermore, the utilization of small satellites for cutting-edge scientific research and ambitious space exploration missions is opening up fascinating new avenues for discovery and innovation.

Growth Accelerators in the Small Satellite Industry Industry

Technological breakthroughs in propulsion, communication, and sensor technologies significantly accelerate growth. Strategic partnerships between established aerospace companies and innovative startups are fostering collaborative innovation. The expansion of the small satellite industry into new markets, particularly in emerging economies with limited terrestrial infrastructure, creates substantial growth potential.

Key Players Shaping the Small Satellite Industry Market

- Space Exploration Technologies Corp (SpaceX)

- German Orbital Systems GmbH

- GomSpace ApS

- Swarm Technologies Inc.

- SpaceQuest Ltd.

- Airbus SE

- Axelspace Corporation

- Astrocast SA

- China Aerospace Science and Technology Corporation (CASC)

- ICEYE Ltd.

- Chang Guang Satellite Technology Co., Ltd.

- Satellogic

- Thales Alenia Space

- Planet Labs Inc.

- Spire Global Inc.

Notable Milestones in Small Satellite Industry Sector

- June 2022: Falcon 9 launched Globalstar FM15 to low-Earth orbit.

- May 2022: Five ICEYE satellites launched as part of the Transporter-5 mission.

- April 2022: Swarm Technologies launched 12 picosatellites on the Transporter 4 mission.

In-Depth Small Satellite Industry Market Outlook

The small satellite industry is firmly on a trajectory of continued, robust expansion. This growth will be significantly propelled by ongoing technological advancements that enhance capabilities and reduce costs, an ever-increasing global demand for space-based data and services, and the strategic penetration into new and underserved markets.

The landscape is expected to witness an increase in strategic partnerships and collaborations, fostering synergy and accelerating development. Substantial investments in research and development (R&D) will remain critical for maintaining a competitive edge, driving innovation in areas like miniaturization, advanced sensor technology, and resilient communication systems. A stable and supportive regulatory environment will continue to be a crucial enabler for market expansion, reducing uncertainty and encouraging investment.

The industry is also likely to experience further consolidation through mergers and acquisitions. This trend will lead to the emergence of larger, more integrated entities possessing enhanced technological capabilities, broader service offerings, and greater operational efficiencies. The long-term potential of the small satellite sector is immense, particularly in revolutionizing critical fields such as Earth observation for environmental stewardship and resource management, enabling the Internet of Things (IoT) on a global scale, and building out resilient, next-generation global communication infrastructure.

Small Satellite Industry Segmentation

-

1. Application

- 1.1. Communication

- 1.2. Earth Observation

- 1.3. Navigation

- 1.4. Space Observation

- 1.5. Others

-

2. Orbit Class

- 2.1. GEO

- 2.2. LEO

- 2.3. MEO

-

3. End User

- 3.1. Commercial

- 3.2. Military & Government

- 3.3. Other

-

4. Propulsion Tech

- 4.1. Electric

- 4.2. Gas based

- 4.3. Liquid Fuel

Small Satellite Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Small Satellite Industry Regional Market Share

Geographic Coverage of Small Satellite Industry

Small Satellite Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Communication

- 5.1.2. Earth Observation

- 5.1.3. Navigation

- 5.1.4. Space Observation

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Orbit Class

- 5.2.1. GEO

- 5.2.2. LEO

- 5.2.3. MEO

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Commercial

- 5.3.2. Military & Government

- 5.3.3. Other

- 5.4. Market Analysis, Insights and Forecast - by Propulsion Tech

- 5.4.1. Electric

- 5.4.2. Gas based

- 5.4.3. Liquid Fuel

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. South America

- 5.5.3. Europe

- 5.5.4. Middle East & Africa

- 5.5.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Small Satellite Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Communication

- 6.1.2. Earth Observation

- 6.1.3. Navigation

- 6.1.4. Space Observation

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Orbit Class

- 6.2.1. GEO

- 6.2.2. LEO

- 6.2.3. MEO

- 6.3. Market Analysis, Insights and Forecast - by End User

- 6.3.1. Commercial

- 6.3.2. Military & Government

- 6.3.3. Other

- 6.4. Market Analysis, Insights and Forecast - by Propulsion Tech

- 6.4.1. Electric

- 6.4.2. Gas based

- 6.4.3. Liquid Fuel

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Small Satellite Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Communication

- 7.1.2. Earth Observation

- 7.1.3. Navigation

- 7.1.4. Space Observation

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Orbit Class

- 7.2.1. GEO

- 7.2.2. LEO

- 7.2.3. MEO

- 7.3. Market Analysis, Insights and Forecast - by End User

- 7.3.1. Commercial

- 7.3.2. Military & Government

- 7.3.3. Other

- 7.4. Market Analysis, Insights and Forecast - by Propulsion Tech

- 7.4.1. Electric

- 7.4.2. Gas based

- 7.4.3. Liquid Fuel

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Small Satellite Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Communication

- 8.1.2. Earth Observation

- 8.1.3. Navigation

- 8.1.4. Space Observation

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Orbit Class

- 8.2.1. GEO

- 8.2.2. LEO

- 8.2.3. MEO

- 8.3. Market Analysis, Insights and Forecast - by End User

- 8.3.1. Commercial

- 8.3.2. Military & Government

- 8.3.3. Other

- 8.4. Market Analysis, Insights and Forecast - by Propulsion Tech

- 8.4.1. Electric

- 8.4.2. Gas based

- 8.4.3. Liquid Fuel

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Small Satellite Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Communication

- 9.1.2. Earth Observation

- 9.1.3. Navigation

- 9.1.4. Space Observation

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Orbit Class

- 9.2.1. GEO

- 9.2.2. LEO

- 9.2.3. MEO

- 9.3. Market Analysis, Insights and Forecast - by End User

- 9.3.1. Commercial

- 9.3.2. Military & Government

- 9.3.3. Other

- 9.4. Market Analysis, Insights and Forecast - by Propulsion Tech

- 9.4.1. Electric

- 9.4.2. Gas based

- 9.4.3. Liquid Fuel

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Small Satellite Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Communication

- 10.1.2. Earth Observation

- 10.1.3. Navigation

- 10.1.4. Space Observation

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Orbit Class

- 10.2.1. GEO

- 10.2.2. LEO

- 10.2.3. MEO

- 10.3. Market Analysis, Insights and Forecast - by End User

- 10.3.1. Commercial

- 10.3.2. Military & Government

- 10.3.3. Other

- 10.4. Market Analysis, Insights and Forecast - by Propulsion Tech

- 10.4.1. Electric

- 10.4.2. Gas based

- 10.4.3. Liquid Fuel

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Small Satellite Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Communication

- 11.1.2. Earth Observation

- 11.1.3. Navigation

- 11.1.4. Space Observation

- 11.1.5. Others

- 11.2. Market Analysis, Insights and Forecast - by Orbit Class

- 11.2.1. GEO

- 11.2.2. LEO

- 11.2.3. MEO

- 11.3. Market Analysis, Insights and Forecast - by End User

- 11.3.1. Commercial

- 11.3.2. Military & Government

- 11.3.3. Other

- 11.4. Market Analysis, Insights and Forecast - by Propulsion Tech

- 11.4.1. Electric

- 11.4.2. Gas based

- 11.4.3. Liquid Fuel

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Space Exploration Technologies Corp

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 German Orbital Systems

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 GomSpaceApS

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Swarm Technologies Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 SpaceQuest Ltd

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Airbus SE

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Axelspace Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Astrocast

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 China Aerospace Science and Technology Corporation (CASC)

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 ICEYE Ltd

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Chang Guang Satellite Technology Co Ltd

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Satellogic

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Thale

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Planet Labs Inc

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Spire Global Inc

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 Space Exploration Technologies Corp

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Small Satellite Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Small Satellite Industry Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Small Satellite Industry Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Small Satellite Industry Revenue (billion), by Orbit Class 2025 & 2033

- Figure 5: North America Small Satellite Industry Revenue Share (%), by Orbit Class 2025 & 2033

- Figure 6: North America Small Satellite Industry Revenue (billion), by End User 2025 & 2033

- Figure 7: North America Small Satellite Industry Revenue Share (%), by End User 2025 & 2033

- Figure 8: North America Small Satellite Industry Revenue (billion), by Propulsion Tech 2025 & 2033

- Figure 9: North America Small Satellite Industry Revenue Share (%), by Propulsion Tech 2025 & 2033

- Figure 10: North America Small Satellite Industry Revenue (billion), by Country 2025 & 2033

- Figure 11: North America Small Satellite Industry Revenue Share (%), by Country 2025 & 2033

- Figure 12: South America Small Satellite Industry Revenue (billion), by Application 2025 & 2033

- Figure 13: South America Small Satellite Industry Revenue Share (%), by Application 2025 & 2033

- Figure 14: South America Small Satellite Industry Revenue (billion), by Orbit Class 2025 & 2033

- Figure 15: South America Small Satellite Industry Revenue Share (%), by Orbit Class 2025 & 2033

- Figure 16: South America Small Satellite Industry Revenue (billion), by End User 2025 & 2033

- Figure 17: South America Small Satellite Industry Revenue Share (%), by End User 2025 & 2033

- Figure 18: South America Small Satellite Industry Revenue (billion), by Propulsion Tech 2025 & 2033

- Figure 19: South America Small Satellite Industry Revenue Share (%), by Propulsion Tech 2025 & 2033

- Figure 20: South America Small Satellite Industry Revenue (billion), by Country 2025 & 2033

- Figure 21: South America Small Satellite Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Europe Small Satellite Industry Revenue (billion), by Application 2025 & 2033

- Figure 23: Europe Small Satellite Industry Revenue Share (%), by Application 2025 & 2033

- Figure 24: Europe Small Satellite Industry Revenue (billion), by Orbit Class 2025 & 2033

- Figure 25: Europe Small Satellite Industry Revenue Share (%), by Orbit Class 2025 & 2033

- Figure 26: Europe Small Satellite Industry Revenue (billion), by End User 2025 & 2033

- Figure 27: Europe Small Satellite Industry Revenue Share (%), by End User 2025 & 2033

- Figure 28: Europe Small Satellite Industry Revenue (billion), by Propulsion Tech 2025 & 2033

- Figure 29: Europe Small Satellite Industry Revenue Share (%), by Propulsion Tech 2025 & 2033

- Figure 30: Europe Small Satellite Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Europe Small Satellite Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: Middle East & Africa Small Satellite Industry Revenue (billion), by Application 2025 & 2033

- Figure 33: Middle East & Africa Small Satellite Industry Revenue Share (%), by Application 2025 & 2033

- Figure 34: Middle East & Africa Small Satellite Industry Revenue (billion), by Orbit Class 2025 & 2033

- Figure 35: Middle East & Africa Small Satellite Industry Revenue Share (%), by Orbit Class 2025 & 2033

- Figure 36: Middle East & Africa Small Satellite Industry Revenue (billion), by End User 2025 & 2033

- Figure 37: Middle East & Africa Small Satellite Industry Revenue Share (%), by End User 2025 & 2033

- Figure 38: Middle East & Africa Small Satellite Industry Revenue (billion), by Propulsion Tech 2025 & 2033

- Figure 39: Middle East & Africa Small Satellite Industry Revenue Share (%), by Propulsion Tech 2025 & 2033

- Figure 40: Middle East & Africa Small Satellite Industry Revenue (billion), by Country 2025 & 2033

- Figure 41: Middle East & Africa Small Satellite Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Asia Pacific Small Satellite Industry Revenue (billion), by Application 2025 & 2033

- Figure 43: Asia Pacific Small Satellite Industry Revenue Share (%), by Application 2025 & 2033

- Figure 44: Asia Pacific Small Satellite Industry Revenue (billion), by Orbit Class 2025 & 2033

- Figure 45: Asia Pacific Small Satellite Industry Revenue Share (%), by Orbit Class 2025 & 2033

- Figure 46: Asia Pacific Small Satellite Industry Revenue (billion), by End User 2025 & 2033

- Figure 47: Asia Pacific Small Satellite Industry Revenue Share (%), by End User 2025 & 2033

- Figure 48: Asia Pacific Small Satellite Industry Revenue (billion), by Propulsion Tech 2025 & 2033

- Figure 49: Asia Pacific Small Satellite Industry Revenue Share (%), by Propulsion Tech 2025 & 2033

- Figure 50: Asia Pacific Small Satellite Industry Revenue (billion), by Country 2025 & 2033

- Figure 51: Asia Pacific Small Satellite Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Small Satellite Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Small Satellite Industry Revenue billion Forecast, by Orbit Class 2020 & 2033

- Table 3: Global Small Satellite Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 4: Global Small Satellite Industry Revenue billion Forecast, by Propulsion Tech 2020 & 2033

- Table 5: Global Small Satellite Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Small Satellite Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 7: Global Small Satellite Industry Revenue billion Forecast, by Orbit Class 2020 & 2033

- Table 8: Global Small Satellite Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 9: Global Small Satellite Industry Revenue billion Forecast, by Propulsion Tech 2020 & 2033

- Table 10: Global Small Satellite Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 11: United States Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Canada Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Mexico Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Global Small Satellite Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 15: Global Small Satellite Industry Revenue billion Forecast, by Orbit Class 2020 & 2033

- Table 16: Global Small Satellite Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 17: Global Small Satellite Industry Revenue billion Forecast, by Propulsion Tech 2020 & 2033

- Table 18: Global Small Satellite Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 19: Brazil Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Argentina Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Rest of South America Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Global Small Satellite Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 23: Global Small Satellite Industry Revenue billion Forecast, by Orbit Class 2020 & 2033

- Table 24: Global Small Satellite Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 25: Global Small Satellite Industry Revenue billion Forecast, by Propulsion Tech 2020 & 2033

- Table 26: Global Small Satellite Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 27: United Kingdom Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Germany Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: France Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Italy Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Spain Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Russia Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: Benelux Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Nordics Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: Rest of Europe Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Global Small Satellite Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 37: Global Small Satellite Industry Revenue billion Forecast, by Orbit Class 2020 & 2033

- Table 38: Global Small Satellite Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 39: Global Small Satellite Industry Revenue billion Forecast, by Propulsion Tech 2020 & 2033

- Table 40: Global Small Satellite Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 41: Turkey Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Israel Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: GCC Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: North Africa Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: South Africa Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Middle East & Africa Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 47: Global Small Satellite Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 48: Global Small Satellite Industry Revenue billion Forecast, by Orbit Class 2020 & 2033

- Table 49: Global Small Satellite Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 50: Global Small Satellite Industry Revenue billion Forecast, by Propulsion Tech 2020 & 2033

- Table 51: Global Small Satellite Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 52: China Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 53: India Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Japan Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 55: South Korea Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 56: ASEAN Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 57: Oceania Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 58: Rest of Asia Pacific Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Small Satellite Industry?

The projected CAGR is approximately 11%.

2. Which companies are prominent players in the Small Satellite Industry?

Key companies in the market include Space Exploration Technologies Corp, German Orbital Systems, GomSpaceApS, Swarm Technologies Inc, SpaceQuest Ltd, Airbus SE, Axelspace Corporation, Astrocast, China Aerospace Science and Technology Corporation (CASC), ICEYE Ltd, Chang Guang Satellite Technology Co Ltd, Satellogic, Thale, Planet Labs Inc, Spire Global Inc.

3. What are the main segments of the Small Satellite Industry?

The market segments include Application, Orbit Class, End User, Propulsion Tech.

4. Can you provide details about the market size?

The market size is estimated to be USD 98.28 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

North America may witness significant growth during the forecast period.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

June 2022: Falcon 9 launched Globalstar FM15 to low-Earth orbit from Space Launch Complex 40 (SLC-40) at Cape Canaveral Space Force Station in Florida.May 2022: As part of the Transporter-5 mission another five satellitesnamely ICEYE-X17, -X18, -X19, -X20 and -X24 were launched.April 2022: Swarm Technologies 12 'picosatellites' on the Transporter 4 mission for low-data-rate communications network have been launched.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Small Satellite Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Small Satellite Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Small Satellite Industry?

To stay informed about further developments, trends, and reports in the Small Satellite Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence