Key Insights

The Asia-Pacific satellite manufacturing market is poised for substantial expansion, driven by escalating demand for advanced communication, earth observation, and navigation satellite solutions. The market is projected to reach a size of 3.79 billion by 2025, with a significant compound annual growth rate (CAGR) of 31% during the forecast period. This growth is underpinned by the widespread adoption of satellite-based technologies across telecommunications, defense, and environmental monitoring sectors, alongside proactive government initiatives supporting space exploration and private sector investment in space-related ventures. Market segmentation includes satellite mass, orbit class, end-user, satellite subsystem, propulsion technology, and country, highlighting the industry's diverse applications and technological sophistication. Leading companies such as Mitsubishi Heavy Industries, CASC, and ISRO are at the forefront of this dynamic market.

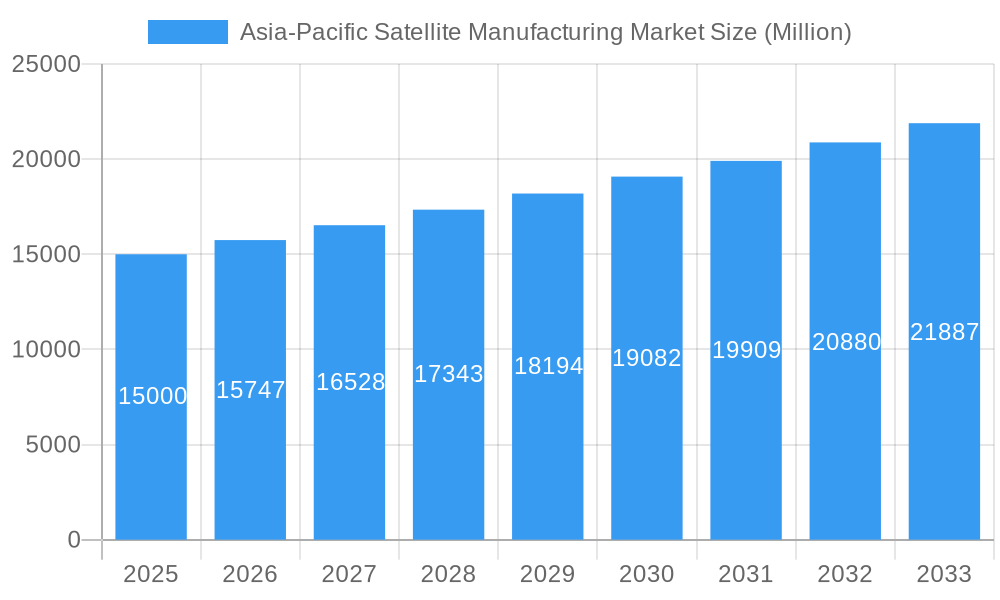

Asia-Pacific Satellite Manufacturing Market Market Size (In Billion)

Future market growth will be propelled by continuous innovation in satellite miniaturization, electric propulsion systems, and advanced subsystems. The increasing affordability and accessibility of satellite technology are expanding its application scope, catering to both government and commercial entities. While challenges such as high manufacturing costs and complex regulatory environments persist, the Asia-Pacific region, with key growth hubs in China, Japan, India, and South Korea, is strategically positioned for significant advancement. Emerging space programs and collaborations in countries like Australia and Singapore further contribute to the market's evolution.

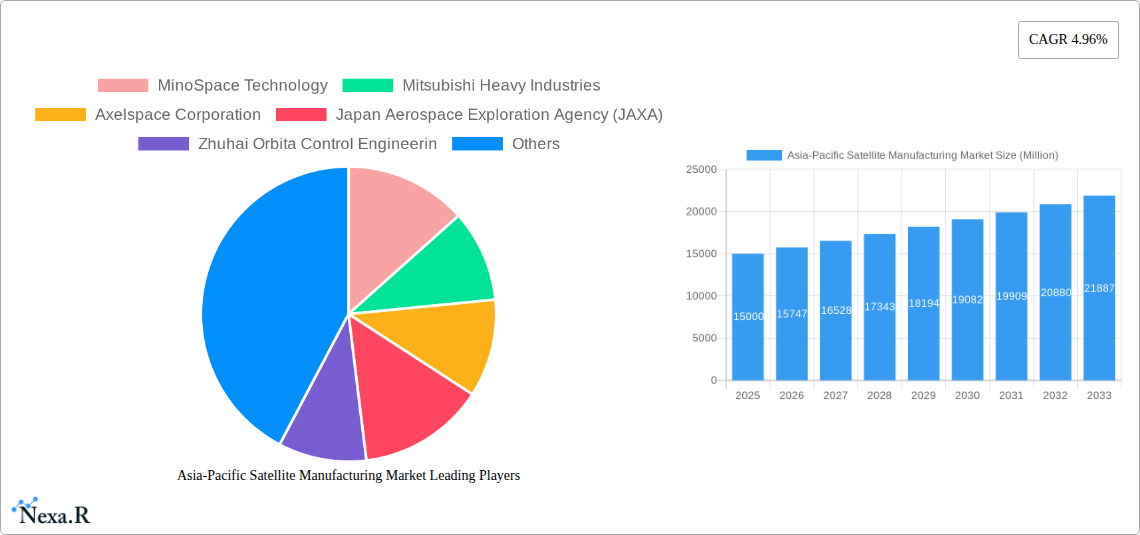

Asia-Pacific Satellite Manufacturing Market Company Market Share

Asia-Pacific Satellite Manufacturing Market: In-Depth Analysis and Forecast (2025-2033)

This comprehensive report offers an in-depth analysis of the Asia-Pacific satellite manufacturing market, detailing market dynamics, growth trajectories, dominant segments, key players, and future projections. The study period spans from 2019 to 2033, with 2025 serving as the base year. The market is meticulously segmented by satellite mass, orbit class, end-user, satellite subsystem, propulsion technology, country, and application. The analysis covers market size evolution, adoption rates, technological advancements, and shifts in consumer behavior, providing critical insights for industry stakeholders, investors, and strategic planners.

Asia-Pacific Satellite Manufacturing Market Dynamics & Structure

The Asia-Pacific satellite manufacturing market is characterized by a moderately concentrated landscape, with a few large players and numerous smaller, specialized companies. Market concentration is driven by factors such as technological advancements, high capital investment requirements, and stringent regulatory frameworks. The market is highly dynamic, witnessing significant technological innovations, including miniaturization, improved propulsion systems, and advanced communication technologies. This drives the demand for smaller, more efficient satellites. Mergers and acquisitions (M&A) activity is also considerable, with large companies seeking to expand their market share and product portfolios. For example, the acquisition of Maxar Technologies by Advent International in December 2022 signifies a considerable consolidation trend.

- Market Concentration: Moderately concentrated, with xx% market share held by the top 5 players in 2025.

- Technological Innovation: Strong emphasis on miniaturization, improved propulsion systems, and advanced communication technologies.

- Regulatory Frameworks: Varying regulatory landscapes across different countries within the Asia-Pacific region, influencing market dynamics.

- Competitive Product Substitutes: Limited direct substitutes, but alternative communication and data transmission technologies pose indirect competition.

- End-User Demographics: Growing demand from commercial, military & government, and other sectors, fueling market expansion.

- M&A Trends: Increasing M&A activity, indicating market consolidation and strategic expansion by major players. The number of M&A deals increased by xx% from 2021 to 2022.

Asia-Pacific Satellite Manufacturing Market Growth Trends & Insights

The Asia-Pacific satellite manufacturing market is experiencing robust growth, driven by factors such as increasing demand for communication, earth observation, and navigation services. The market size is expected to witness significant expansion during the forecast period. Adoption rates of satellite technology are rising across various sectors, including commercial, government, and military. Technological disruptions, particularly in miniaturization and advanced propulsion systems, are enabling the development of more affordable and efficient satellites. Consumer behavior shifts towards increased reliance on satellite-based services, coupled with supportive government policies, are further propelling market growth. The growth is also fueled by increased investment in space exploration and research.

Dominant Regions, Countries, or Segments in Asia-Pacific Satellite Manufacturing Market

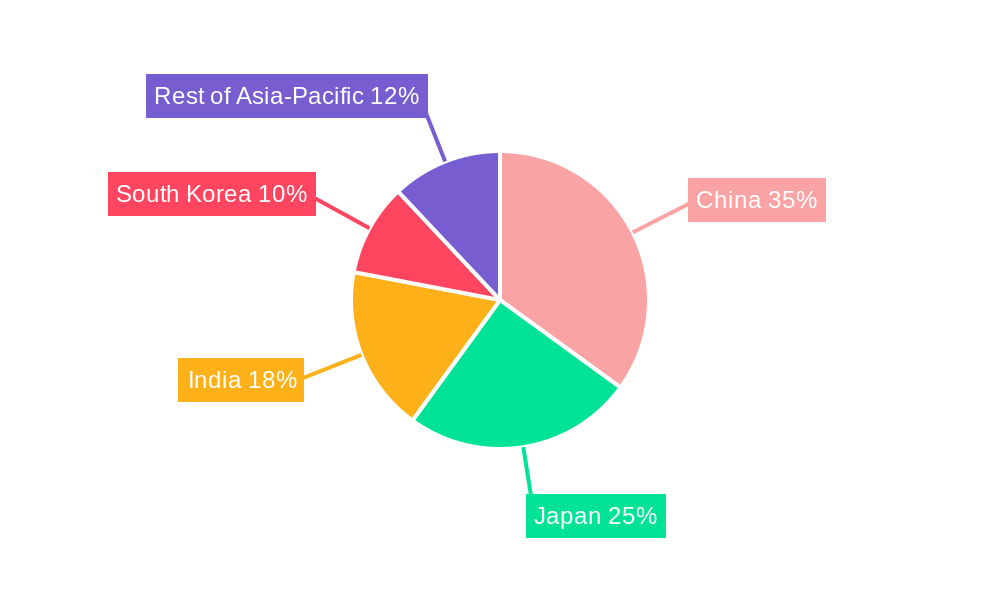

China and Japan are currently the leading countries in the Asia-Pacific satellite manufacturing market, contributing xx% and xx% of the total market share in 2025, respectively. Their dominance is attributed to strong government support, substantial investments in space programs, and a robust technological base. The LEO (Low Earth Orbit) segment holds the largest market share (xx%) due to the growing demand for high-resolution imagery and improved communication coverage. Within satellite mass, the 100-500 kg segment dominates, followed by the 10-100 kg segment. The commercial sector is the leading end-user segment.

- Key Drivers:

- Government Support: Significant investments in space exploration and research.

- Technological advancements: Miniaturization and advanced propulsion systems.

- Growing Demand: Increasing need for satellite-based services across various sectors.

- Dominance Factors:

- Strong Technological Base: Presence of advanced technology and skilled workforce in China and Japan.

- Government Initiatives: Favorable policies and funding for space research.

- Market Size & Growth Potential: Large and rapidly expanding market in China and other emerging economies.

Asia-Pacific Satellite Manufacturing Market Product Landscape

The Asia-Pacific satellite manufacturing market is witnessing continuous product innovation, with a focus on smaller, lighter, and more efficient satellites. Advanced materials, innovative propulsion technologies, and improved satellite subsystems are key features of the latest products. These advancements are enabling the development of constellations of smaller satellites, providing enhanced capabilities at lower costs. Unique selling propositions often center around superior performance, reduced launch costs, and customized configurations to meet specific mission requirements.

Key Drivers, Barriers & Challenges in Asia-Pacific Satellite Manufacturing Market

Key Drivers:

- Increasing demand for satellite-based services across various sectors.

- Government initiatives to promote space exploration and research.

- Technological advancements in satellite technology.

Challenges & Restraints:

- High capital investment requirements for satellite manufacturing.

- Stringent regulatory frameworks and licensing processes.

- Intense competition from established and emerging players.

- Supply chain disruptions impacting the availability of components. The impact of the semiconductor shortage reduced production by approximately xx% in 2022.

Emerging Opportunities in Asia-Pacific Satellite Manufacturing Market

Emerging opportunities lie in the development of small satellite constellations for various applications, including IoT, Earth observation, and communication. There is considerable potential for expansion into underserved markets and the development of innovative applications like space-based AI and deep-space exploration. The increasing adoption of new space technologies and commercial space launches creates further opportunities.

Growth Accelerators in the Asia-Pacific Satellite Manufacturing Market Industry

Technological breakthroughs in miniaturization, advanced propulsion systems, and improved satellite subsystems are driving long-term growth. Strategic partnerships between government agencies, private companies, and research institutions are crucial for accelerating innovation and market expansion. The emergence of NewSpace companies is further accelerating market growth and competition.

Key Players Shaping the Asia-Pacific Satellite Manufacturing Market Market

- MinoSpace Technology

- Mitsubishi Heavy Industries

- Axelspace Corporation

- Japan Aerospace Exploration Agency (JAXA)

- Zhuhai Orbita Control Engineering

- China Aerospace Science and Technology Corporation (CASC)

- Maxar Technologies Inc

- Chang Guang Satellite Technology Co Ltd

- Spacety Aerospace Co

- Indian Space Research Organisation (ISRO)

- Guodian Gaoke

Notable Milestones in Asia-Pacific Satellite Manufacturing Market Sector

- January 2023: Minospace Technology secured Pre-B funding of USD 47 million, enabling increased mass production capacity for 500 kg class satellites.

- December 2022: Maxar Technologies' acquisition by Advent International for USD 6.4 billion signifies significant market consolidation.

- November 2022: EchoStar Corporation and Maxar Technologies finalized an agreement to manufacture the EchoStar XXIV satellite (JUPITER™ 3).

In-Depth Asia-Pacific Satellite Manufacturing Market Outlook

The Asia-Pacific satellite manufacturing market is poised for sustained growth, driven by technological advancements, increasing demand for satellite-based services, and supportive government policies. Strategic partnerships, investments in research and development, and the expansion of NewSpace activities will further propel market expansion. The market presents significant opportunities for both established players and new entrants, particularly in the small satellite and constellation markets.

Asia-Pacific Satellite Manufacturing Market Segmentation

-

1. Application

- 1.1. Communication

- 1.2. Earth Observation

- 1.3. Navigation

- 1.4. Space Observation

- 1.5. Others

-

2. Satellite Mass

- 2.1. 10-100kg

- 2.2. 100-500kg

- 2.3. 500-1000kg

- 2.4. Below 10 Kg

- 2.5. above 1000kg

-

3. Orbit Class

- 3.1. GEO

- 3.2. LEO

- 3.3. MEO

-

4. End User

- 4.1. Commercial

- 4.2. Military & Government

- 4.3. Other

-

5. Satellite Subsystem

- 5.1. Propulsion Hardware and Propellant

- 5.2. Satellite Bus & Subsystems

- 5.3. Solar Array & Power Hardware

- 5.4. Structures, Harness & Mechanisms

-

6. Propulsion Tech

- 6.1. Electric

- 6.2. Gas based

- 6.3. Liquid Fuel

Asia-Pacific Satellite Manufacturing Market Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. Japan

- 1.3. South Korea

- 1.4. India

- 1.5. Australia

- 1.6. New Zealand

- 1.7. Indonesia

- 1.8. Malaysia

- 1.9. Singapore

- 1.10. Thailand

- 1.11. Vietnam

- 1.12. Philippines

Asia-Pacific Satellite Manufacturing Market Regional Market Share

Geographic Coverage of Asia-Pacific Satellite Manufacturing Market

Asia-Pacific Satellite Manufacturing Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 31% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Communication

- 5.1.2. Earth Observation

- 5.1.3. Navigation

- 5.1.4. Space Observation

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Satellite Mass

- 5.2.1. 10-100kg

- 5.2.2. 100-500kg

- 5.2.3. 500-1000kg

- 5.2.4. Below 10 Kg

- 5.2.5. above 1000kg

- 5.3. Market Analysis, Insights and Forecast - by Orbit Class

- 5.3.1. GEO

- 5.3.2. LEO

- 5.3.3. MEO

- 5.4. Market Analysis, Insights and Forecast - by End User

- 5.4.1. Commercial

- 5.4.2. Military & Government

- 5.4.3. Other

- 5.5. Market Analysis, Insights and Forecast - by Satellite Subsystem

- 5.5.1. Propulsion Hardware and Propellant

- 5.5.2. Satellite Bus & Subsystems

- 5.5.3. Solar Array & Power Hardware

- 5.5.4. Structures, Harness & Mechanisms

- 5.6. Market Analysis, Insights and Forecast - by Propulsion Tech

- 5.6.1. Electric

- 5.6.2. Gas based

- 5.6.3. Liquid Fuel

- 5.7. Market Analysis, Insights and Forecast - by Region

- 5.7.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Asia-Pacific Satellite Manufacturing Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Communication

- 6.1.2. Earth Observation

- 6.1.3. Navigation

- 6.1.4. Space Observation

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Satellite Mass

- 6.2.1. 10-100kg

- 6.2.2. 100-500kg

- 6.2.3. 500-1000kg

- 6.2.4. Below 10 Kg

- 6.2.5. above 1000kg

- 6.3. Market Analysis, Insights and Forecast - by Orbit Class

- 6.3.1. GEO

- 6.3.2. LEO

- 6.3.3. MEO

- 6.4. Market Analysis, Insights and Forecast - by End User

- 6.4.1. Commercial

- 6.4.2. Military & Government

- 6.4.3. Other

- 6.5. Market Analysis, Insights and Forecast - by Satellite Subsystem

- 6.5.1. Propulsion Hardware and Propellant

- 6.5.2. Satellite Bus & Subsystems

- 6.5.3. Solar Array & Power Hardware

- 6.5.4. Structures, Harness & Mechanisms

- 6.6. Market Analysis, Insights and Forecast - by Propulsion Tech

- 6.6.1. Electric

- 6.6.2. Gas based

- 6.6.3. Liquid Fuel

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 MinoSpace Technology

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Mitsubishi Heavy Industries

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Axelspace Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Japan Aerospace Exploration Agency (JAXA)

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Zhuhai Orbita Control Engineerin

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 China Aerospace Science and Technology Corporation (CASC)

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Maxar Technologies Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Chang Guang Satellite Technology Co Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Spacety Aerospace Co

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Indian Space Research Organisation (ISRO)

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Guodian Gaoke

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 MinoSpace Technology

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Asia-Pacific Satellite Manufacturing Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Asia-Pacific Satellite Manufacturing Market Share (%) by Company 2025

List of Tables

- Table 1: Asia-Pacific Satellite Manufacturing Market Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Asia-Pacific Satellite Manufacturing Market Revenue billion Forecast, by Satellite Mass 2020 & 2033

- Table 3: Asia-Pacific Satellite Manufacturing Market Revenue billion Forecast, by Orbit Class 2020 & 2033

- Table 4: Asia-Pacific Satellite Manufacturing Market Revenue billion Forecast, by End User 2020 & 2033

- Table 5: Asia-Pacific Satellite Manufacturing Market Revenue billion Forecast, by Satellite Subsystem 2020 & 2033

- Table 6: Asia-Pacific Satellite Manufacturing Market Revenue billion Forecast, by Propulsion Tech 2020 & 2033

- Table 7: Asia-Pacific Satellite Manufacturing Market Revenue billion Forecast, by Region 2020 & 2033

- Table 8: Asia-Pacific Satellite Manufacturing Market Revenue billion Forecast, by Application 2020 & 2033

- Table 9: Asia-Pacific Satellite Manufacturing Market Revenue billion Forecast, by Satellite Mass 2020 & 2033

- Table 10: Asia-Pacific Satellite Manufacturing Market Revenue billion Forecast, by Orbit Class 2020 & 2033

- Table 11: Asia-Pacific Satellite Manufacturing Market Revenue billion Forecast, by End User 2020 & 2033

- Table 12: Asia-Pacific Satellite Manufacturing Market Revenue billion Forecast, by Satellite Subsystem 2020 & 2033

- Table 13: Asia-Pacific Satellite Manufacturing Market Revenue billion Forecast, by Propulsion Tech 2020 & 2033

- Table 14: Asia-Pacific Satellite Manufacturing Market Revenue billion Forecast, by Country 2020 & 2033

- Table 15: China Asia-Pacific Satellite Manufacturing Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Japan Asia-Pacific Satellite Manufacturing Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: South Korea Asia-Pacific Satellite Manufacturing Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: India Asia-Pacific Satellite Manufacturing Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Australia Asia-Pacific Satellite Manufacturing Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: New Zealand Asia-Pacific Satellite Manufacturing Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Indonesia Asia-Pacific Satellite Manufacturing Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Malaysia Asia-Pacific Satellite Manufacturing Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Singapore Asia-Pacific Satellite Manufacturing Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Thailand Asia-Pacific Satellite Manufacturing Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Vietnam Asia-Pacific Satellite Manufacturing Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Philippines Asia-Pacific Satellite Manufacturing Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia-Pacific Satellite Manufacturing Market?

The projected CAGR is approximately 31%.

2. Which companies are prominent players in the Asia-Pacific Satellite Manufacturing Market?

Key companies in the market include MinoSpace Technology, Mitsubishi Heavy Industries, Axelspace Corporation, Japan Aerospace Exploration Agency (JAXA), Zhuhai Orbita Control Engineerin, China Aerospace Science and Technology Corporation (CASC), Maxar Technologies Inc, Chang Guang Satellite Technology Co Ltd, Spacety Aerospace Co, Indian Space Research Organisation (ISRO), Guodian Gaoke.

3. What are the main segments of the Asia-Pacific Satellite Manufacturing Market?

The market segments include Application, Satellite Mass, Orbit Class, End User, Satellite Subsystem, Propulsion Tech.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.79 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

January 2023: Minospace Technology Co. Ltd announced that it had closed a Pre-B funding round of approximately USD 47 million in August 2021. Following this funding round, MinoSpace announced that it would scale its mass production capacity for 500 kg class satellites.December 2022: Maxar Technologies entered into a definitive merger agreement to be acquired by Advent International (Advent), one of the largest and most experienced companies in the world, with an enterprise value of approximately USD 6.4 billion.November 2022: EchoStar Corporation announced a revised agreement with Maxar Technologies to manufacture the EchoStar XXIV satellite, also known as JUPITER™ 3. The satellite, designed for EchoStar's Hughes Network Systems division, is being manufactured at Maxar's facility in Palo Alto, California.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia-Pacific Satellite Manufacturing Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia-Pacific Satellite Manufacturing Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia-Pacific Satellite Manufacturing Market?

To stay informed about further developments, trends, and reports in the Asia-Pacific Satellite Manufacturing Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence