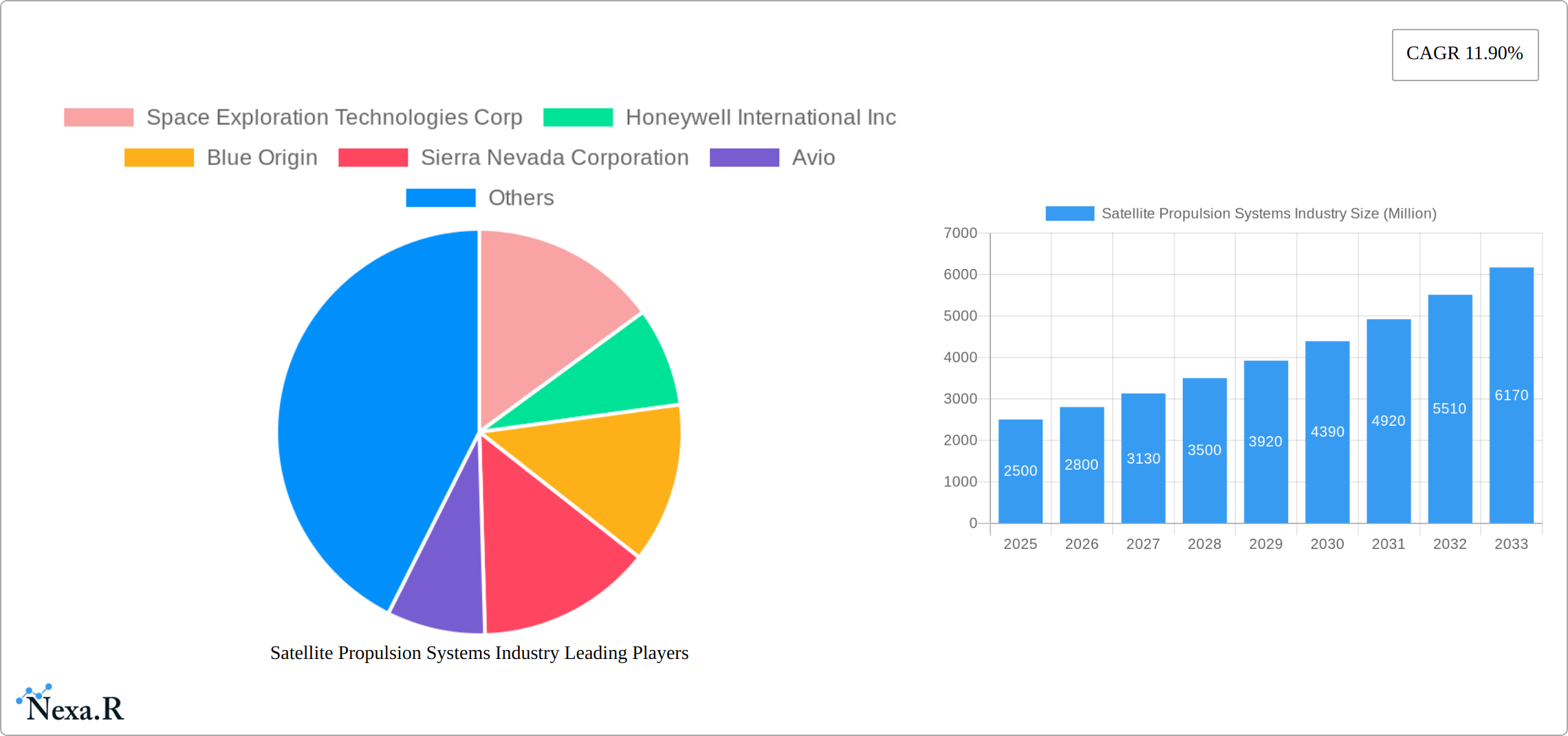

Key Insights

The satellite propulsion systems market is experiencing robust growth, driven by increasing demand for satellite launches and the expansion of satellite constellations for various applications, including communication, navigation, Earth observation, and defense. The market, valued at approximately $XX million in 2025, is projected to exhibit a Compound Annual Growth Rate (CAGR) of 11.90% from 2025 to 2033. This growth is fueled by advancements in propulsion technologies, particularly electric propulsion systems, which offer superior fuel efficiency and longer operational lifespans compared to traditional chemical propulsion. Miniaturization trends, enabling smaller and more cost-effective satellites, further contribute to market expansion. Key players like SpaceX, Blue Origin, and established aerospace giants like Honeywell and Northrop Grumman are heavily invested in research and development, driving innovation and competition within the sector. However, the market faces challenges, including the high cost of development and launch, stringent regulatory requirements, and the potential for technological disruptions.

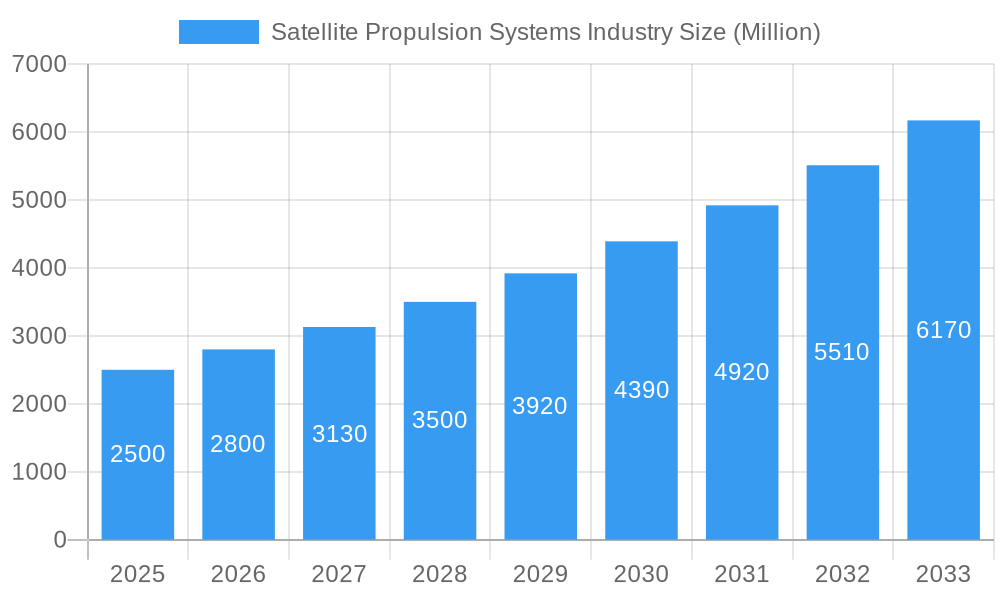

Satellite Propulsion Systems Industry Market Size (In Billion)

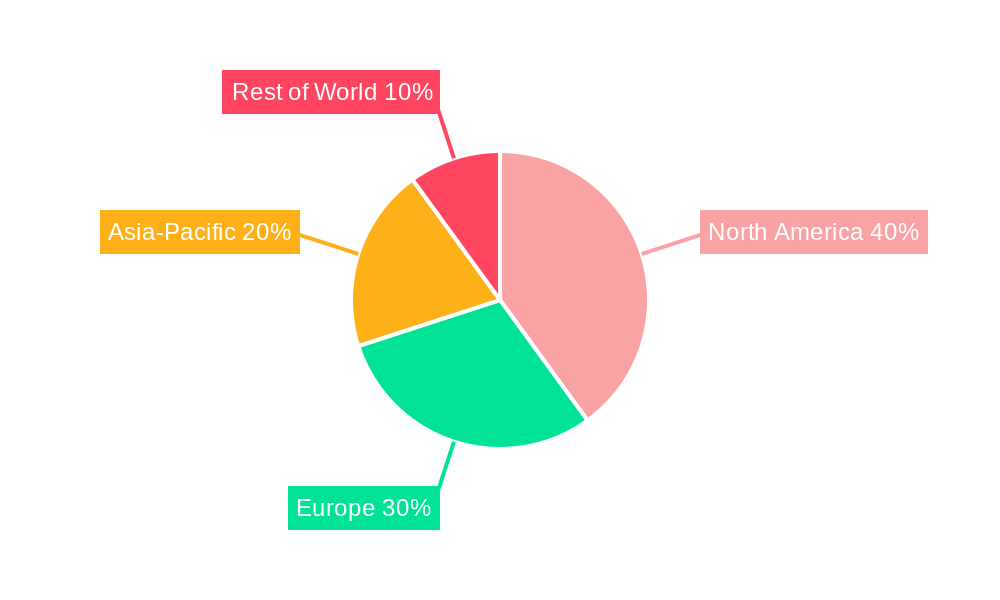

Despite these restraints, the market is poised for significant expansion. The shift towards larger satellite constellations requires efficient and reliable propulsion systems, creating a substantial demand for advanced technologies. The increasing adoption of electric propulsion across various satellite types and missions will be a key driver of market growth throughout the forecast period. Segmentation by propulsion technology (electric, gas-based, liquid fuel) highlights the diversity of the market and the potential for future growth in electric propulsion specifically, given its advantages in terms of cost-effectiveness and operational efficiency. Geographic regions such as North America and Europe are currently leading the market, but emerging economies in Asia and other regions are anticipated to show increasing participation in the coming years.

Satellite Propulsion Systems Industry Company Market Share

Satellite Propulsion Systems Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the Satellite Propulsion Systems industry, encompassing market dynamics, growth trends, regional analysis, product landscape, key players, and future outlook. The study period covers 2019-2033, with a base year of 2025 and a forecast period of 2025-2033. The report offers invaluable insights for industry professionals, investors, and stakeholders seeking to understand and capitalize on the opportunities within this dynamic sector. Market values are presented in millions of units.

Satellite Propulsion Systems Industry Market Dynamics & Structure

The satellite propulsion systems market is characterized by moderate concentration, with several key players dominating various segments. Technological innovation, particularly in electric propulsion, is a significant driver, alongside increasing demand for smaller, more efficient satellites. Regulatory frameworks, primarily driven by space agencies like NASA and ESA, influence technological advancements and market access. Competition from alternative technologies, including advancements in launch vehicle design, and increasing M&A activity are shaping the market landscape. End-user demographics are primarily focused on government agencies (space agencies and defense), commercial satellite operators, and research institutions.

- Market Concentration: Moderately concentrated, with top 5 players holding approximately xx% market share in 2025.

- Technological Innovation: Electric propulsion is experiencing rapid growth, driven by efficiency and cost advantages.

- Regulatory Frameworks: Stringent safety and reliability standards influence product development and market access.

- Competitive Product Substitutes: Advancements in launch vehicle design and alternative propulsion methods pose a competitive threat.

- M&A Activity: An average of xx M&A deals per year (2019-2024), indicating consolidation within the sector.

- Innovation Barriers: High R&D costs and stringent certification processes hinder innovation.

Satellite Propulsion Systems Industry Growth Trends & Insights

The global satellite propulsion systems market is experiencing robust growth, driven by several key factors. The increasing demand for large satellite constellations, the miniaturization trend in satellite technology, and the widespread adoption of electric propulsion are all significantly contributing to market expansion. By 2033, the market is projected to reach [Insert Updated Market Size in Million Units] , exhibiting a Compound Annual Growth Rate (CAGR) of [Insert Updated CAGR]% from 2025 to 2033. This follows a consistent upward trend during the historical period (2019-2024), which showed a CAGR of [Insert Updated Historical CAGR]%. Technological advancements, such as breakthroughs in electric propulsion and the development of environmentally friendly green propellants, are accelerating market adoption. Furthermore, a shift towards smaller, more cost-effective satellites is fueling this growth. Market penetration rates for electric propulsion are expected to rise from [Insert Updated 2025 Penetration Rate]% in 2025 to [Insert Updated 2033 Penetration Rate]% by 2033.

Dominant Regions, Countries, or Segments in Satellite Propulsion Systems Industry

North America currently holds the leading position in the satellite propulsion systems market, followed by Europe. This leadership is attributed to the presence of major industry players, robust national space programs, and substantial investments in space research and exploration. Within the propulsion technology segment, electric propulsion is experiencing the fastest growth, surpassing traditional liquid and gas-based systems due to its superior efficiency and cost-effectiveness. This trend is expected to continue, with electric propulsion systems capturing a significant market share.

- North America: Market leadership is driven by strong government support, advanced technological capabilities, and a thriving commercial space sector fostering innovation and competition.

- Europe: The substantial market share is a result of the significant presence of established aerospace companies and well-developed national space programs.

- Asia-Pacific: This region shows immense growth potential, fueled by increasing investments in satellite technologies and ambitious space exploration initiatives.

- Propulsion Technology: Electric propulsion is poised to dominate the market by 2033, driven by its efficiency and cost advantages. Further advancements in this area will solidify its position.

- Key Drivers: Government funding and private investments are crucial, along with continuous technological advancements and the ever-growing demand for diverse satellite services.

Satellite Propulsion Systems Industry Product Landscape

The satellite propulsion systems market offers a diverse range of products, including electric propulsion systems (ion thrusters, Hall-effect thrusters, gridded ion thrusters, etc.), gas-based systems (cold gas thrusters, resistojets), and liquid-fuel systems (monopropellant, bipropellant). Innovation is focused on enhancing efficiency, minimizing mass, and improving reliability. Key selling points for manufacturers include improved fuel efficiency, reduced operational costs, and extended system lifespan. Technological advancements are concentrated on the development of advanced materials, miniaturization techniques, and sophisticated control systems.

Key Drivers, Barriers & Challenges in Satellite Propulsion Systems Industry

Key Drivers:

- Increasing demand for satellite constellations for various applications (communication, Earth observation, navigation).

- Advancements in electric propulsion technology, offering higher efficiency and lower costs.

- Government investments in space exploration and research.

Key Challenges and Restraints:

- High R&D costs associated with developing new propulsion technologies.

- Stringent regulatory requirements and safety standards.

- Supply chain disruptions and component shortages impacting production timelines.

- Intense competition among established and emerging players.

Emerging Opportunities in Satellite Propulsion Systems Industry

- The increasing demand for smaller, more affordable satellites, especially CubeSats and nanosatellites, presents significant opportunities for specialized propulsion systems.

- Expansion into new applications, such as in-space servicing, active debris removal, and deep-space planetary exploration missions, is creating new market segments.

- The development and adoption of green propellants are crucial for reducing the environmental impact of satellite operations and meeting growing sustainability concerns. This is driving innovation in propellant chemistry and propulsion system design.

- The rise of NewSpace companies and increased private investment are creating a dynamic and competitive market landscape, offering numerous opportunities for innovation and growth.

Growth Accelerators in the Satellite Propulsion Systems Industry

Technological breakthroughs in electric propulsion, coupled with strategic partnerships between space agencies and private companies, are key catalysts for long-term growth. Market expansion into new applications and regions, along with the increasing adoption of smaller satellites, will significantly boost the market's trajectory.

Key Players Shaping the Satellite Propulsion Systems Industry Market

Notable Milestones in Satellite Propulsion Systems Industry Sector

- February 2023: Thales Alenia Space contracted with KARI to provide integrated electric propulsion for GEO-KOMPSAT-3 (GK3) satellite. This highlights growing adoption of electric propulsion technology.

- February 2023: NASA awarded Blue Origin the ESCAPADE contract, utilizing New Glenn reusable technology. This demonstrates the increasing importance of reusable launch vehicles.

- December 2023: NASA awarded Blue Origin a NASA Launch Services II IDIQ contract for launching various satellites aboard New Glenn. This signifies Blue Origin's growing role in the launch services market and strengthens the demand for related propulsion systems.

In-Depth Satellite Propulsion Systems Industry Market Outlook

The satellite propulsion systems market is poised for substantial growth, driven by a confluence of factors: rapid technological advancements, the escalating demand for diverse satellite services (communication, Earth observation, navigation, etc.), and significant investments in space exploration initiatives by both governments and private entities. Strategic collaborations between industry players and space agencies are further accelerating market expansion. Significant opportunities exist in developing innovative propulsion technologies that address emerging market needs, expanding into new applications, and meeting the growing demand for smaller, more cost-effective satellite propulsion systems. The future of the satellite propulsion systems market is bright, promising substantial opportunities for both established and emerging companies. The focus on sustainability and the development of environmentally friendly technologies will be a key driver of future innovation and growth.

Satellite Propulsion Systems Industry Segmentation

-

1. Propulsion Tech

- 1.1. Electric

- 1.2. Gas based

- 1.3. Liquid Fuel

Satellite Propulsion Systems Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Satellite Propulsion Systems Industry Regional Market Share

Geographic Coverage of Satellite Propulsion Systems Industry

Satellite Propulsion Systems Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.90% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 3.4.1. The growing interest of governments and private players in space exploration have fueled the expansion of this market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Satellite Propulsion Systems Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Propulsion Tech

- 5.1.1. Electric

- 5.1.2. Gas based

- 5.1.3. Liquid Fuel

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. South America

- 5.2.3. Europe

- 5.2.4. Middle East & Africa

- 5.2.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Propulsion Tech

- 6. North America Satellite Propulsion Systems Industry Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Propulsion Tech

- 6.1.1. Electric

- 6.1.2. Gas based

- 6.1.3. Liquid Fuel

- 6.1. Market Analysis, Insights and Forecast - by Propulsion Tech

- 7. South America Satellite Propulsion Systems Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Propulsion Tech

- 7.1.1. Electric

- 7.1.2. Gas based

- 7.1.3. Liquid Fuel

- 7.1. Market Analysis, Insights and Forecast - by Propulsion Tech

- 8. Europe Satellite Propulsion Systems Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Propulsion Tech

- 8.1.1. Electric

- 8.1.2. Gas based

- 8.1.3. Liquid Fuel

- 8.1. Market Analysis, Insights and Forecast - by Propulsion Tech

- 9. Middle East & Africa Satellite Propulsion Systems Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Propulsion Tech

- 9.1.1. Electric

- 9.1.2. Gas based

- 9.1.3. Liquid Fuel

- 9.1. Market Analysis, Insights and Forecast - by Propulsion Tech

- 10. Asia Pacific Satellite Propulsion Systems Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Propulsion Tech

- 10.1.1. Electric

- 10.1.2. Gas based

- 10.1.3. Liquid Fuel

- 10.1. Market Analysis, Insights and Forecast - by Propulsion Tech

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Space Exploration Technologies Corp

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Honeywell International Inc

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Blue Origin

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Sierra Nevada Corporation

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Avio

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Moog Inc

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Ariane Group

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 OHB SE

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Sitael S p A

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Thale

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Northrop Grumman Corporation

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 IHI Corporation

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 Space Exploration Technologies Corp

List of Figures

- Figure 1: Global Satellite Propulsion Systems Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Satellite Propulsion Systems Industry Revenue (Million), by Propulsion Tech 2025 & 2033

- Figure 3: North America Satellite Propulsion Systems Industry Revenue Share (%), by Propulsion Tech 2025 & 2033

- Figure 4: North America Satellite Propulsion Systems Industry Revenue (Million), by Country 2025 & 2033

- Figure 5: North America Satellite Propulsion Systems Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: South America Satellite Propulsion Systems Industry Revenue (Million), by Propulsion Tech 2025 & 2033

- Figure 7: South America Satellite Propulsion Systems Industry Revenue Share (%), by Propulsion Tech 2025 & 2033

- Figure 8: South America Satellite Propulsion Systems Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: South America Satellite Propulsion Systems Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Satellite Propulsion Systems Industry Revenue (Million), by Propulsion Tech 2025 & 2033

- Figure 11: Europe Satellite Propulsion Systems Industry Revenue Share (%), by Propulsion Tech 2025 & 2033

- Figure 12: Europe Satellite Propulsion Systems Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Satellite Propulsion Systems Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Middle East & Africa Satellite Propulsion Systems Industry Revenue (Million), by Propulsion Tech 2025 & 2033

- Figure 15: Middle East & Africa Satellite Propulsion Systems Industry Revenue Share (%), by Propulsion Tech 2025 & 2033

- Figure 16: Middle East & Africa Satellite Propulsion Systems Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Middle East & Africa Satellite Propulsion Systems Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Satellite Propulsion Systems Industry Revenue (Million), by Propulsion Tech 2025 & 2033

- Figure 19: Asia Pacific Satellite Propulsion Systems Industry Revenue Share (%), by Propulsion Tech 2025 & 2033

- Figure 20: Asia Pacific Satellite Propulsion Systems Industry Revenue (Million), by Country 2025 & 2033

- Figure 21: Asia Pacific Satellite Propulsion Systems Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Satellite Propulsion Systems Industry Revenue Million Forecast, by Propulsion Tech 2020 & 2033

- Table 2: Global Satellite Propulsion Systems Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Global Satellite Propulsion Systems Industry Revenue Million Forecast, by Propulsion Tech 2020 & 2033

- Table 4: Global Satellite Propulsion Systems Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 5: United States Satellite Propulsion Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 6: Canada Satellite Propulsion Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 7: Mexico Satellite Propulsion Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Global Satellite Propulsion Systems Industry Revenue Million Forecast, by Propulsion Tech 2020 & 2033

- Table 9: Global Satellite Propulsion Systems Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 10: Brazil Satellite Propulsion Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Argentina Satellite Propulsion Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Rest of South America Satellite Propulsion Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Global Satellite Propulsion Systems Industry Revenue Million Forecast, by Propulsion Tech 2020 & 2033

- Table 14: Global Satellite Propulsion Systems Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 15: United Kingdom Satellite Propulsion Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Germany Satellite Propulsion Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: France Satellite Propulsion Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Italy Satellite Propulsion Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Spain Satellite Propulsion Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Russia Satellite Propulsion Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Benelux Satellite Propulsion Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Nordics Satellite Propulsion Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Rest of Europe Satellite Propulsion Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Global Satellite Propulsion Systems Industry Revenue Million Forecast, by Propulsion Tech 2020 & 2033

- Table 25: Global Satellite Propulsion Systems Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 26: Turkey Satellite Propulsion Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Israel Satellite Propulsion Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: GCC Satellite Propulsion Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: North Africa Satellite Propulsion Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: South Africa Satellite Propulsion Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: Rest of Middle East & Africa Satellite Propulsion Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Global Satellite Propulsion Systems Industry Revenue Million Forecast, by Propulsion Tech 2020 & 2033

- Table 33: Global Satellite Propulsion Systems Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 34: China Satellite Propulsion Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: India Satellite Propulsion Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Japan Satellite Propulsion Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: South Korea Satellite Propulsion Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: ASEAN Satellite Propulsion Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 39: Oceania Satellite Propulsion Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Rest of Asia Pacific Satellite Propulsion Systems Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Satellite Propulsion Systems Industry?

The projected CAGR is approximately 11.90%.

2. Which companies are prominent players in the Satellite Propulsion Systems Industry?

Key companies in the market include Space Exploration Technologies Corp, Honeywell International Inc, Blue Origin, Sierra Nevada Corporation, Avio, Moog Inc, Ariane Group, OHB SE, Sitael S p A, Thale, Northrop Grumman Corporation, IHI Corporation.

3. What are the main segments of the Satellite Propulsion Systems Industry?

The market segments include Propulsion Tech.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

The growing interest of governments and private players in space exploration have fueled the expansion of this market.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

December 2023: NASA awarded Blue Origin a NASA Launch Services II Indefinite Delivery Indefinite Quantity (IDIQ) contract to launch planetary, Earth observation, exploration, and scientific satellites for the agency aboard New Glenn, Blue Origin's orbital reusable launch vehicle.February 2023: NASA's Launch Services Program (LSP) awarded Blue Origin the Escape and Plasma Acceleration and Dynamics Explorers (ESCAPADE) contract. Under the contract Blue Origin will provide its New Glenn reusable technology for the mission.February 2023: Thales Alenia Space has contracted with the Korea Aerospace Research Institute (KARI) to provide the integrated electric propulsion on their GEO-KOMPSAT-3 (GK3) satellite.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Satellite Propulsion Systems Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Satellite Propulsion Systems Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Satellite Propulsion Systems Industry?

To stay informed about further developments, trends, and reports in the Satellite Propulsion Systems Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence