Key Insights

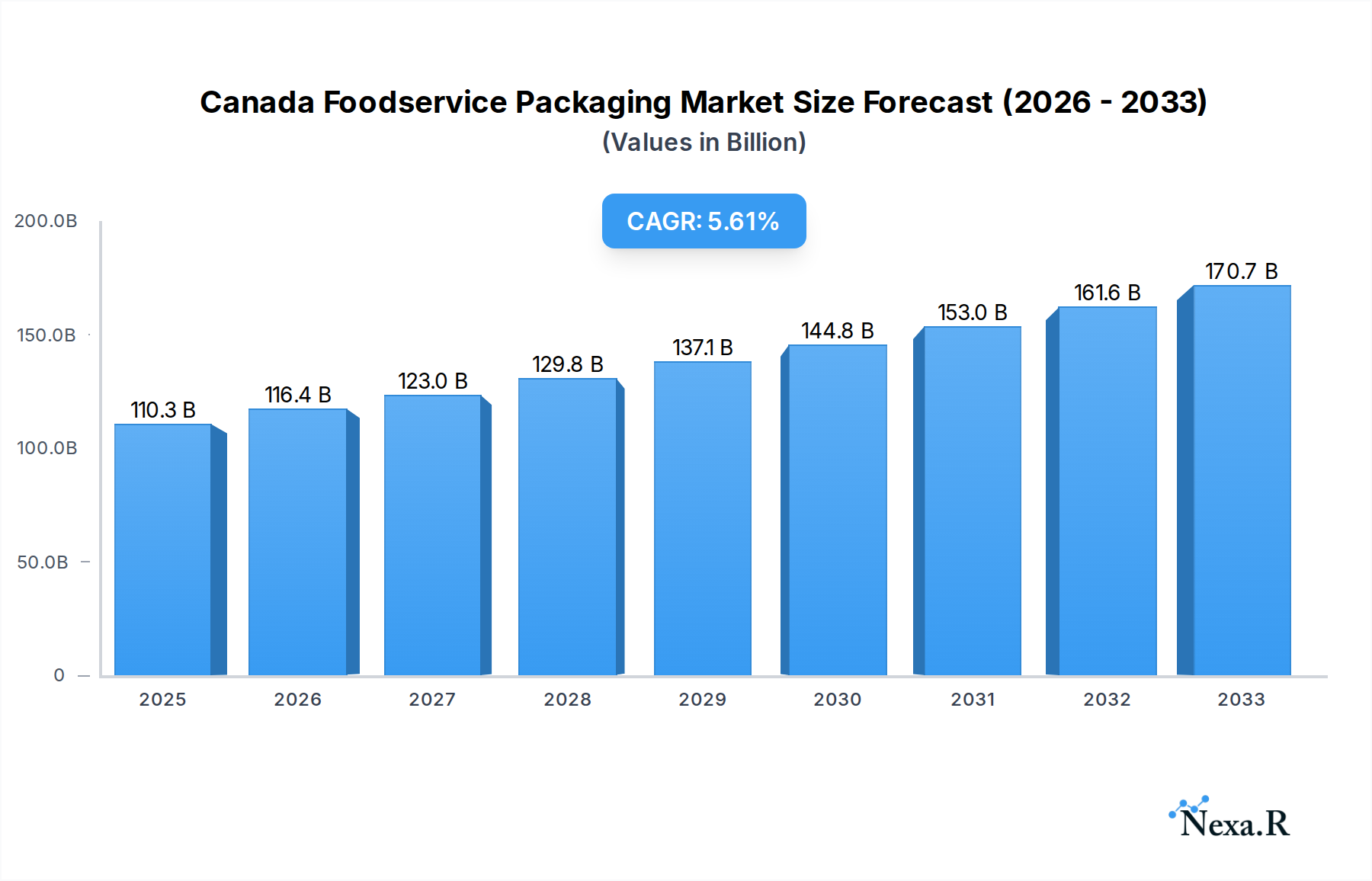

The Canadian foodservice packaging market is poised for robust expansion, with an estimated market size of $110.29 billion in 2025, growing at a Compound Annual Growth Rate (CAGR) of 5.5% through 2033. This significant growth is propelled by a confluence of factors, primarily driven by the escalating demand for convenient and ready-to-eat food options, a direct consequence of increasingly busy lifestyles and a growing urban population across Canada. The burgeoning food delivery and takeaway sector, further accelerated by recent global events, plays a pivotal role in this market's upward trajectory. Furthermore, a heightened consumer awareness regarding sustainability and environmental impact is steering the market towards eco-friendly and recyclable packaging solutions, creating significant opportunities for innovation and market differentiation. The demand for packaging that ensures food safety and maintains product integrity throughout the supply chain, from preparation to consumption, remains a foundational element driving market performance.

Canada Foodservice Packaging Market Market Size (In Billion)

This dynamic market landscape is characterized by a strong preference for both rigid and flexible packaging formats, catering to a diverse range of food applications including fruits and vegetables, baked goods, dairy products, and meat and poultry. Specialty processed foods also represent a growing segment, demanding specialized packaging to preserve freshness and enhance presentation. Key end-user industries such as restaurants, encompassing quick-service, full-service, and institutional and hospitality sectors, are significant contributors to this market's volume. Leading companies like Amhil North America, Ronpak Inc., Genpak Corporation, Novolex, and Pactiv Evergreen Inc. are actively shaping this market through strategic investments in advanced manufacturing technologies and the development of sustainable packaging alternatives, responding to evolving consumer preferences and regulatory landscapes in Canada.

Canada Foodservice Packaging Market Company Market Share

Canada Foodservice Packaging Market Report 2024-2033: Sustainable Solutions & Growth Trajectories

This comprehensive report provides an in-depth analysis of the Canadian foodservice packaging market, encompassing its current dynamics, growth trends, dominant segments, and future outlook. Leveraging extensive data from 2019–2033, with a base and estimated year of 2025, this report offers critical insights for stakeholders seeking to navigate this evolving landscape. Discover key market drivers, emerging opportunities, and the strategies of leading players in the quest for sustainable and efficient foodservice packaging solutions. The market is analyzed across various material types, applications, and end-user industries, including crucial parent and child market segments to provide a holistic view of the Canadian foodservice packaging ecosystem. All values are presented in billion units.

Canada Foodservice Packaging Market Market Dynamics & Structure

The Canadian foodservice packaging market is characterized by a moderately concentrated structure, with key players like Novolex, Pactiv Evergreen Inc., and Berry Global Inc. holding significant market shares. However, the growing emphasis on sustainability is fostering a more dynamic competitive environment, with smaller, innovative companies emerging to offer specialized eco-friendly solutions. Technological innovation is a primary driver, pushing for advancements in biodegradable, compostable, and recyclable materials, alongside improved functionality and cost-effectiveness. Regulatory frameworks, particularly those aimed at reducing single-use plastics and promoting a circular economy, are shaping market trends and influencing product development. Competitive product substitutes, ranging from traditional plastic containers to paper-based alternatives and reusable systems, are readily available, forcing manufacturers to constantly innovate and differentiate their offerings. End-user demographics, with a growing preference for convenience and environmentally conscious choices, are also a significant factor. Mergers and acquisitions (M&A) remain an active trend, with companies consolidating to expand their product portfolios, gain market access, and enhance their sustainability credentials. For instance, the push towards recycled content in paperboard packaging is a key M&A driver.

- Market Concentration: Moderate, with a few dominant players and an increasing number of specialized niche providers.

- Technological Innovation: Focused on biodegradable, compostable, and recyclable materials, as well as enhanced barrier properties and convenience features.

- Regulatory Frameworks: Driven by government initiatives to reduce waste and promote sustainability, impacting material choices and product design.

- Competitive Substitutes: Wide array, from conventional plastics to eco-friendly alternatives and reusable packaging systems.

- End-User Demographics: Shifting towards convenience, health consciousness, and environmental responsibility.

- M&A Trends: Active consolidation to enhance market reach, product offerings, and sustainability commitments.

Canada Foodservice Packaging Market Growth Trends & Insights

The Canadian foodservice packaging market has witnessed a steady growth trajectory driven by evolving consumer preferences and increasing demand for convenience. The market size is projected to experience a Compound Annual Growth Rate (CAGR) of approximately 5.2% from 2025 to 2033, reaching an estimated xx billion units by the end of the forecast period. This growth is underpinned by a significant shift in consumer behavior, with an increasing preference for on-the-go meals and takeout services, directly impacting the volume of foodservice packaging required. Adoption rates for sustainable packaging solutions are rapidly accelerating, spurred by both consumer awareness and government regulations aiming to curb environmental impact. Technological disruptions are playing a crucial role, with advancements in material science leading to the development of innovative biodegradable, compostable, and high-barrier recyclable packaging. These innovations are not only addressing environmental concerns but also enhancing product shelf-life and user experience.

The "foodservice packaging" market is a parent market encompassing various child markets. Within the "rigid packaging" child market, plastic containers and paperboard boxes are leading segments due to their versatility and widespread application across various food types. The "flexible packaging" child market is also experiencing robust growth, particularly in pouches and films for convenience foods and individual servings. The "application" segment analysis reveals a strong demand for packaging solutions for fruits and vegetables, baked goods, and dairy products, driven by the rising popularity of pre-packaged meals and snacks. Furthermore, the "end-user industry" perspective highlights the dominance of restaurants, particularly quick-service restaurants (QSRs), which account for a substantial portion of the market's volume due to their high turnover and extensive takeout operations. Institutional and hospitality sectors also contribute significantly, driven by the need for efficient and hygienic food delivery solutions. Consumer demand for visually appealing and functional packaging is influencing product design, with manufacturers investing in research and development to offer aesthetically pleasing and performance-optimized solutions. The integration of smart packaging technologies, offering features like temperature indication and traceability, represents a future growth avenue.

Dominant Regions, Countries, or Segments in Canada Foodservice Packaging Market

The Canadian foodservice packaging market's dominance is multifaceted, with specific segments and regions exhibiting superior growth and penetration. Within the Material Type segment, Rigid packaging continues to hold a substantial market share, driven by its protective qualities and versatility. Specifically, Plastic Containers (a child market of rigid packaging) are highly prevalent due to their cost-effectiveness, durability, and clarity, making them ideal for a wide array of food products. However, the Flexible packaging segment, particularly Pouches and Paper-based materials, is experiencing accelerated growth due to increasing consumer demand for convenience and the industry's push towards sustainable alternatives. These flexible solutions offer reduced material usage and often boast lower carbon footprints.

In terms of Application, Fruits and Vegetables and Baked Goods are leading segments. The growing consumer interest in healthy eating and ready-to-eat options fuels the demand for specialized packaging that preserves freshness and extends shelf life for produce. Similarly, the convenience associated with pre-packaged baked goods in retail and foodservice settings contributes to its strong market performance. The Dairy Products segment also demonstrates consistent growth, driven by the popularity of yogurt cups, cheese trays, and milk cartons.

From an End-user Industry perspective, Restaurants, especially Quick-service Restaurants (QSRs), represent the most dominant segment. The high volume of takeout and delivery orders in QSRs directly translates to a massive demand for disposable foodservice packaging. Full-service restaurants also contribute significantly, with a growing emphasis on presentation and sustainable packaging options for dine-in and takeaway. The Institutional and Hospitality sector, including catering services, hospitals, and corporate cafeterias, is another key driver, requiring bulk packaging solutions that prioritize hygiene and efficiency.

The dominance factors include economic policies supporting local manufacturing and sustainable material development, robust supply chain infrastructure facilitating efficient distribution, and evolving consumer preferences leaning towards convenience and eco-conscious purchasing. Market share within these dominant segments is influenced by brand recognition, product innovation, and competitive pricing strategies employed by major players. The growth potential within these segments remains high, driven by ongoing urbanization, changing lifestyle patterns, and the continuous innovation in packaging materials and designs aimed at enhancing functionality and environmental performance.

Canada Foodservice Packaging Market Product Landscape

The Canadian foodservice packaging market is characterized by a dynamic product landscape focused on enhancing functionality, convenience, and sustainability. Innovations range from advanced biodegradable and compostable materials derived from plant-based sources, offering alternatives to traditional plastics, to high-performance paperboard packaging with enhanced barrier properties for hot and cold food applications. Rigid plastic containers are evolving with improved recyclability and design features for better stacking and portability. Flexible packaging, such as stand-up pouches and retort bags, is gaining traction for its space-saving benefits and ability to extend shelf life. Unique selling propositions often revolve around a brand's commitment to environmental responsibility, highlighted through certifications for compostability or recycled content. Technological advancements are also enabling features like improved tamper-evidence, microwave-safe materials, and aesthetically pleasing finishes.

Key Drivers, Barriers & Challenges in Canada Foodservice Packaging Market

Key Drivers: The Canadian foodservice packaging market is propelled by several key drivers. Technological advancements in sustainable materials, such as biodegradable and compostable polymers, are creating new product avenues. Growing consumer awareness regarding environmental issues is creating strong demand for eco-friendly packaging solutions, compelling businesses to adopt sustainable practices. Supportive government policies and initiatives promoting waste reduction and circular economy principles provide a favorable regulatory environment. The increasing prevalence of food delivery and takeout services, particularly post-pandemic, directly fuels the demand for single-use packaging. Economic growth and a rising disposable income contribute to increased spending on convenience foods and dining out, further boosting packaging consumption.

Barriers & Challenges: Supply chain disruptions and the volatility of raw material prices pose significant challenges, impacting production costs and availability. Stringent and evolving regulatory frameworks regarding plastic use and waste management can create compliance hurdles for manufacturers. The high cost associated with developing and implementing new sustainable packaging technologies can be a barrier to entry for smaller players. Intense competition from both domestic and international players necessitates continuous innovation and cost optimization. Consumer perception and the practical implementation of recycling and composting programs across the country present challenges in achieving true circularity.

Emerging Opportunities in Canada Foodservice Packaging Market

Emerging opportunities in the Canadian foodservice packaging market are abundant, driven by innovation and evolving consumer needs. The growing demand for plant-based and compostable packaging presents a significant opportunity for manufacturers to develop and market a wider range of eco-friendly alternatives. Innovations in reusable packaging systems, supported by robust collection and sanitation infrastructure, offer a sustainable long-term solution. The expanding e-commerce and food delivery sectors create demand for specialized, durable, and temperature-controlled packaging. Furthermore, opportunities lie in developing packaging solutions with integrated smart technologies, such as track-and-trace capabilities and enhanced tamper-evidence features, catering to the increasing demand for food safety and transparency. The development of localized, bio-based material sources also presents a potential growth avenue, reducing reliance on imported materials and supporting the Canadian bioeconomy.

Growth Accelerators in the Canada Foodservice Packaging Market Industry

Several catalysts are accelerating the growth of the Canada Foodservice Packaging Market industry. Technological breakthroughs in bioplastics and advanced paper-based materials are making sustainable options more performant and cost-competitive. Strategic partnerships between packaging manufacturers, food businesses, and waste management companies are fostering collaborative efforts towards a circular economy. Market expansion strategies by key players, focusing on underserved regions or specific application segments like specialty processed foods, are unlocking new revenue streams. The increasing consumer willingness to pay a premium for sustainably packaged products acts as a significant demand accelerator. Furthermore, government incentives and grants supporting R&D in sustainable packaging are encouraging innovation and faster adoption rates.

Key Players Shaping the Canada Foodservice Packaging Market Market

- Amhil North America

- Ronpak Inc

- Genpak Corporation

- Novolex

- Plastic Ingenuity Inc

- Pactiv Evergreen Inc

- Berry Global Inc

- Tellus Product

- Huhtamaki Americas Inc

- Dart Container Corporation

Notable Milestones in Canada Foodservice Packaging Market Sector

- April 2022: The Canadian government announced an investment to help Canada's fresh produce industry transition to sustainable food and produce packaging. The government aimed to reduce packaging waste and increase food and produce packaging sustainability. Agriculture and Agri-Food Minister Marie-Claude Bibeau stated the government would invest up to CAD 376,200 (USD 299,869) in the Canadian Produce Marketing Association (CPMA), supporting the development of a new packaging circular economy, leveraging composting systems across Canada, and enhancing industry alignment with leading sustainable packaging in food and produce.

- April 2022: Swiss Chalet launched sustainable packaging across Canada, executing this crucial step in their food service operations. The company noted that by its completion, 100% of the packaging line would come from recyclable, renewable, and recycled resources, including their paper-based products, which will only come from sources certified in their forest conservation commitments.

In-Depth Canada Foodservice Packaging Market Market Outlook

The future outlook for the Canada Foodservice Packaging Market is exceptionally promising, driven by a confluence of sustained demand, robust innovation, and increasing regulatory impetus towards sustainability. Growth accelerators like the widespread adoption of advanced biodegradable and compostable materials, coupled with strategic market expansion by key players targeting niche segments, will continue to fuel market expansion. The ongoing shift in consumer preference towards eco-conscious choices, coupled with the expanding food delivery and takeout ecosystem, ensures a consistent demand for efficient and responsible packaging solutions. Further developments in reusable packaging systems and the integration of smart technologies are poised to redefine the market landscape, presenting significant strategic opportunities for stakeholders willing to invest in future-forward solutions. The market is expected to see continued growth, driven by a commitment to environmental stewardship and operational excellence.

Canada Foodservice Packaging Market Segmentation

-

1. Material Type

-

1.1. Rigid

- 1.1.1. Corrugated Boxes

- 1.1.2. Paperbaord Boxes

- 1.1.3. Plastic Containers

- 1.1.4. Metal Cans

- 1.1.5. Other Ri

-

1.2. Flexible

- 1.2.1. Pouches

- 1.2.2. Paper, Film, and Foil

- 1.2.3. Bags and Sacks

- 1.2.4. Trays, Plates, and Food Bowls

- 1.2.5. Other Flexible Material Types

-

1.1. Rigid

-

2. Application

- 2.1. Fruits and Vegetables

- 2.2. Baked Goods

- 2.3. Dairy Products

- 2.4. Meat and Poultry

- 2.5. Specialty Processed Foods

- 2.6. Other Applications

-

3. End-user Industry

-

3.1. Restaurants

- 3.1.1. Quick-service

- 3.1.2. Full-service

- 3.1.3. Other Restaurants

- 3.2. Institutional and Hospitality

-

3.1. Restaurants

Canada Foodservice Packaging Market Segmentation By Geography

- 1. Canada

Canada Foodservice Packaging Market Regional Market Share

Geographic Coverage of Canada Foodservice Packaging Market

Canada Foodservice Packaging Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 5.1.1. Rigid

- 5.1.1.1. Corrugated Boxes

- 5.1.1.2. Paperbaord Boxes

- 5.1.1.3. Plastic Containers

- 5.1.1.4. Metal Cans

- 5.1.1.5. Other Ri

- 5.1.2. Flexible

- 5.1.2.1. Pouches

- 5.1.2.2. Paper, Film, and Foil

- 5.1.2.3. Bags and Sacks

- 5.1.2.4. Trays, Plates, and Food Bowls

- 5.1.2.5. Other Flexible Material Types

- 5.1.1. Rigid

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Fruits and Vegetables

- 5.2.2. Baked Goods

- 5.2.3. Dairy Products

- 5.2.4. Meat and Poultry

- 5.2.5. Specialty Processed Foods

- 5.2.6. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Restaurants

- 5.3.1.1. Quick-service

- 5.3.1.2. Full-service

- 5.3.1.3. Other Restaurants

- 5.3.2. Institutional and Hospitality

- 5.3.1. Restaurants

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Canada

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 6. Canada Foodservice Packaging Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 6.1.1. Rigid

- 6.1.1.1. Corrugated Boxes

- 6.1.1.2. Paperbaord Boxes

- 6.1.1.3. Plastic Containers

- 6.1.1.4. Metal Cans

- 6.1.1.5. Other Ri

- 6.1.2. Flexible

- 6.1.2.1. Pouches

- 6.1.2.2. Paper, Film, and Foil

- 6.1.2.3. Bags and Sacks

- 6.1.2.4. Trays, Plates, and Food Bowls

- 6.1.2.5. Other Flexible Material Types

- 6.1.1. Rigid

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Fruits and Vegetables

- 6.2.2. Baked Goods

- 6.2.3. Dairy Products

- 6.2.4. Meat and Poultry

- 6.2.5. Specialty Processed Foods

- 6.2.6. Other Applications

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Restaurants

- 6.3.1.1. Quick-service

- 6.3.1.2. Full-service

- 6.3.1.3. Other Restaurants

- 6.3.2. Institutional and Hospitality

- 6.3.1. Restaurants

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Amhil North America

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Ronpak Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Genpak Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Novolex

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Plastic Ingenuity Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Pactiv Evergreen Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Berry Global Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Tellus Product

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Huhtamaki Americas Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Dart Container Corporation

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Amhil North America

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Canada Foodservice Packaging Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Canada Foodservice Packaging Market Share (%) by Company 2025

List of Tables

- Table 1: Canada Foodservice Packaging Market Revenue billion Forecast, by Material Type 2020 & 2033

- Table 2: Canada Foodservice Packaging Market Revenue billion Forecast, by Application 2020 & 2033

- Table 3: Canada Foodservice Packaging Market Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 4: Canada Foodservice Packaging Market Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Canada Foodservice Packaging Market Revenue billion Forecast, by Material Type 2020 & 2033

- Table 6: Canada Foodservice Packaging Market Revenue billion Forecast, by Application 2020 & 2033

- Table 7: Canada Foodservice Packaging Market Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 8: Canada Foodservice Packaging Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canada Foodservice Packaging Market?

The projected CAGR is approximately 5.5%.

2. Which companies are prominent players in the Canada Foodservice Packaging Market?

Key companies in the market include Amhil North America, Ronpak Inc, Genpak Corporation, Novolex, Plastic Ingenuity Inc, Pactiv Evergreen Inc, Berry Global Inc, Tellus Product, Huhtamaki Americas Inc, Dart Container Corporation.

3. What are the main segments of the Canada Foodservice Packaging Market?

The market segments include Material Type, Application, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 110.29 billion as of 2022.

5. What are some drivers contributing to market growth?

Demand for Convenience Food Remains High in Canada; Growing Demand for Sustainable Packaging Solution.

6. What are the notable trends driving market growth?

Demand for Convenience Food Remains High in Canada.

7. Are there any restraints impacting market growth?

Environmental Concerns Regarding Usage of Plastic; Stringent Government Regulations.

8. Can you provide examples of recent developments in the market?

April 2022: The Canadian government announced an investment to help Canada's fresh produce industry transition to sustainable food and produce packaging. The government aimed to reduce packaging waste and increase food and produce packaging sustainability. Agriculture and Agri-Food Minister Marie-Claude Bibeau said the government would invest up to CAD 376,200 (USD 299,869) in the Canadian Produce Marketing Association (CPMA). They were developing a new packaging circular economy, leveraging composting systems across Canada, and enhancing industry alignment with leading sustainable packaging in food and produce.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canada Foodservice Packaging Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canada Foodservice Packaging Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canada Foodservice Packaging Market?

To stay informed about further developments, trends, and reports in the Canada Foodservice Packaging Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence