Key Insights

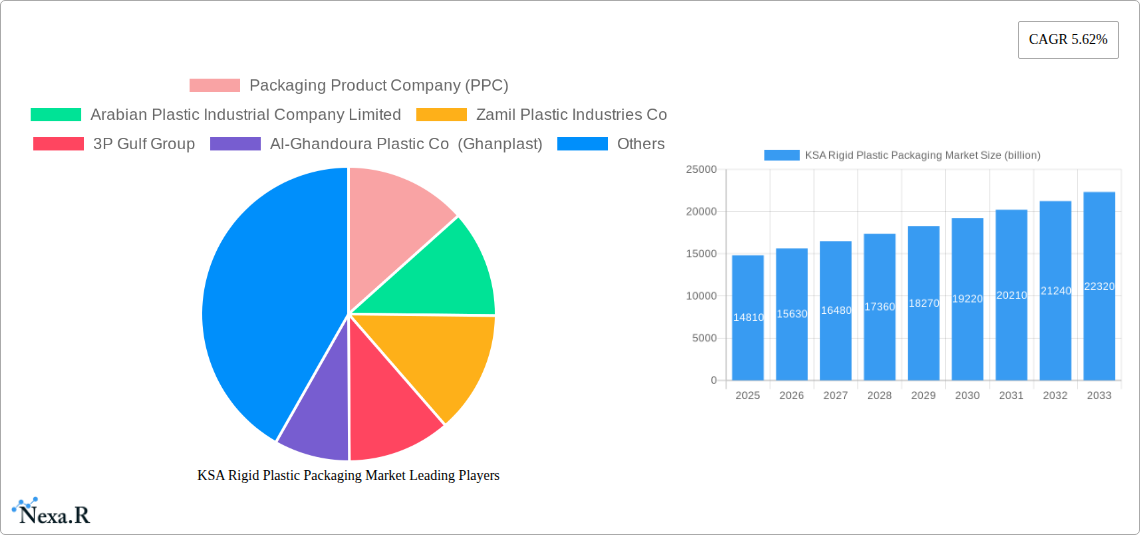

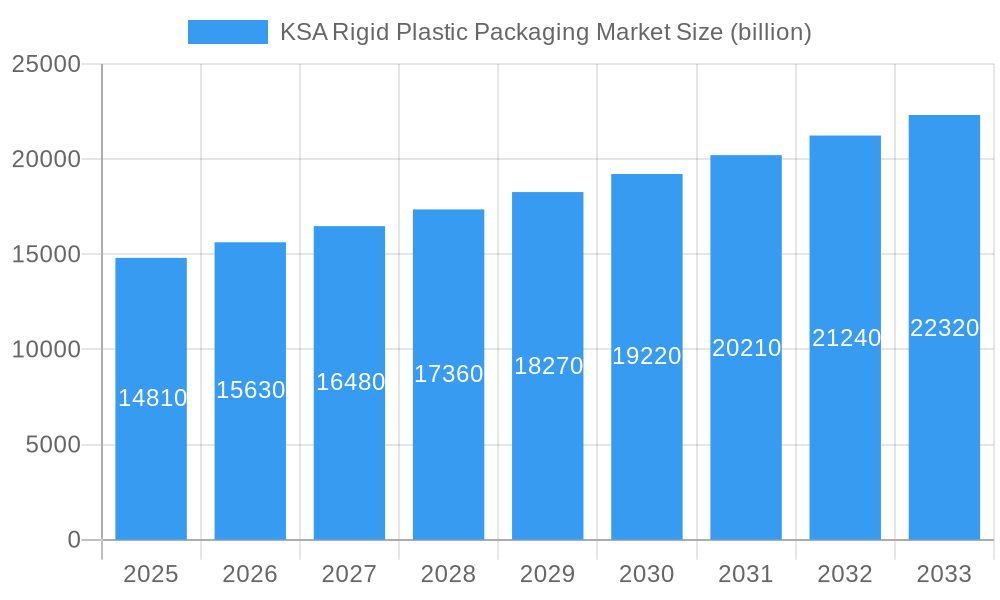

The Saudi Arabian rigid plastic packaging market is poised for robust expansion, projected to reach an estimated $14.81 billion by 2025. This growth is underpinned by a healthy Compound Annual Growth Rate (CAGR) of 5.62% over the forecast period, indicating sustained demand and increasing adoption of rigid plastic packaging solutions across diverse industries. The market's trajectory is propelled by several key drivers, including the burgeoning food and beverage sector, which relies heavily on rigid packaging for product preservation and consumer appeal. The expanding healthcare industry, with its stringent packaging requirements for pharmaceuticals and medical devices, also presents a significant growth avenue. Furthermore, the increasing disposable income and evolving consumer lifestyles in Saudi Arabia are fueling demand for packaged goods, thereby driving the need for effective and versatile rigid plastic packaging. The government's focus on economic diversification under Vision 2030 is also expected to stimulate industrial growth, leading to a higher uptake of packaging solutions.

KSA Rigid Plastic Packaging Market Market Size (In Billion)

The market's expansion is further supported by ongoing trends such as the increasing preference for lightweight and durable packaging materials, which rigid plastics readily offer. Innovations in plastic resin technology are leading to the development of more sustainable and functional packaging options, catering to growing environmental consciousness. Rigid plastic packaging plays a crucial role in protecting products during transit and storage, making it indispensable for industries like automotive and building & construction. While the market exhibits strong growth potential, certain restraints, such as fluctuating raw material prices and increasing regulatory scrutiny regarding plastic waste, could influence the pace of expansion. However, the widespread adoption of materials like Polyethylene (PE), Polyethylene Terephthalate (PET), and Polypropylene (PP), coupled with the diversification of end-use industries, including cosmetics and personal care, signifies a dynamic and resilient market. Leading companies are actively investing in advanced manufacturing technologies and sustainable practices to capitalize on these opportunities and address potential challenges.

KSA Rigid Plastic Packaging Market Company Market Share

Unlock the Lucrative KSA Rigid Plastic Packaging Market: Comprehensive Insights for Strategic Growth

This in-depth report provides a critical analysis of the KSA Rigid Plastic Packaging Market, a dynamic sector poised for substantial expansion. Covering a study period from 2019 to 2033, with a base and estimated year of 2025 and a forecast period of 2025–2033, this report offers unparalleled market intelligence for stakeholders. Delve into the intricate market dynamics, growth trends, dominant segments, product landscape, key drivers, emerging opportunities, and competitive strategies shaping the Saudi Arabian rigid plastic packaging industry. With meticulous research and data-driven insights, this report is your essential guide to navigating and capitalizing on this thriving market.

KSA Rigid Plastic Packaging Market Market Dynamics & Structure

The KSA Rigid Plastic Packaging Market is characterized by a moderately concentrated structure, with key players like SABIC and Zamil Plastic Industries Co. holding significant influence. Technological innovation is a primary driver, with ongoing advancements in material science and processing technologies enhancing product performance and sustainability. Regulatory frameworks, particularly those focused on environmental impact and recycling, are increasingly shaping market dynamics, encouraging the adoption of eco-friendly solutions. Competitive product substitutes, while present, are largely outweighed by the versatility and cost-effectiveness of rigid plastics. End-user demographics are evolving, with a growing demand for convenient, safe, and sustainable packaging across various sectors. Mergers and acquisitions (M&A) trends, such as Alpek's acquisition of OCTAL Holding SAOC, indicate a consolidation push and strategic integration to enhance market reach and product portfolios. Barriers to innovation include significant capital investment requirements for advanced manufacturing and stringent quality control standards. The market's growth is underpinned by robust economic development and increasing consumer spending power within the Kingdom.

- Market Concentration: Moderately concentrated, with key players focusing on strategic expansion and diversification.

- Technological Innovation: Driven by advancements in material science, lightweighting, and barrier properties.

- Regulatory Frameworks: Increasing emphasis on sustainability, recyclability, and waste reduction initiatives.

- Competitive Product Substitutes: Limited impact due to the cost-effectiveness and performance of rigid plastics.

- End-User Demographics: Shifting towards demand for premium, sustainable, and functional packaging.

- M&A Trends: Strategic acquisitions to gain market share, expand product offerings, and achieve vertical integration.

KSA Rigid Plastic Packaging Market Growth Trends & Insights

The KSA Rigid Plastic Packaging Market is projected to witness significant growth, driven by a confluence of economic development, population expansion, and evolving consumer preferences. The market size is expected to ascend from an estimated value of XX billion units in 2025 to XX billion units by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of XX% during the forecast period. Adoption rates for advanced rigid plastic packaging solutions are on an upward trajectory, fueled by the increasing demand for extended shelf-life products in the food and beverage sector, as well as the stringent requirements for sterile and secure packaging in healthcare. Technological disruptions, including the development of high-barrier materials, lightweighting innovations for reduced material consumption, and the integration of smart packaging features, are reshaping the market landscape. Consumer behavior shifts are profoundly impacting demand; there is a growing preference for single-serve portions, convenient dispensing mechanisms, and visually appealing packaging. The emphasis on sustainability is compelling manufacturers to invest in recycled content integration and explore biodegradable alternatives, though the primary focus remains on enhancing the recyclability of existing materials. The burgeoning e-commerce sector also presents a substantial opportunity for growth, demanding robust and protective packaging solutions. Furthermore, government initiatives aimed at boosting local manufacturing and reducing reliance on imports are providing a fertile ground for the expansion of the rigid plastic packaging industry in Saudi Arabia. The insights derived from this analysis will empower stakeholders to make informed strategic decisions, capitalizing on the burgeoning opportunities and navigating potential challenges within this dynamic market.

Dominant Regions, Countries, or Segments in KSA Rigid Plastic Packaging Market

Within the KSA Rigid Plastic Packaging Market, the Food and Beverage end-use industry unequivocally stands as the dominant segment, driving substantial market growth. This dominance is intrinsically linked to Saudi Arabia's large and growing population, coupled with a rapidly expanding food processing and consumption landscape. The demand for safe, durable, and aesthetically pleasing packaging to preserve product freshness, extend shelf life, and enhance consumer appeal is paramount in this sector. Rigid plastic packaging, particularly bottles, jars, trays, and containers, is indispensable for a vast array of food and beverage products, from dairy and juices to snacks and ready-to-eat meals.

Dominant Segment: Food and Beverage End-Use Industry

- Market Share: The Food and Beverage segment is estimated to hold XX% of the total KSA Rigid Plastic Packaging Market share in 2025.

- Growth Potential: Projected to grow at a CAGR of XX% during the forecast period (2025–2033), outpacing other end-use industries.

- Key Drivers:

- Population Growth & Urbanization: A young and growing population with increasing disposable incomes drives higher consumption of packaged goods.

- Food Security Initiatives: Government focus on enhancing food security necessitates robust packaging solutions for preservation and distribution.

- Evolving Consumer Lifestyles: Increased demand for convenience foods, ready-to-eat meals, and single-serving portions.

- Growth of the Retail Sector: Expansion of supermarkets, hypermarkets, and convenience stores, increasing the need for shelf-ready packaging.

- Product Innovation: Food manufacturers continuously innovate, requiring diverse and specialized packaging formats.

Dominant Product Segments within Food & Beverage:

- Bottles and Jars: Crucial for beverages (water, juices, carbonated drinks) and condiments, sauces, and jams. Material dominance includes PET and HDPE.

- Trays and Containers: Widely used for fresh produce, bakery items, dairy products, and ready meals. Materials like PP and PS are prevalent.

- Caps and Closures: Essential for product integrity and tamper-evidence across all food and beverage categories.

Dominant Material Segments within Food & Beverage:

- Polyethylene Terephthalate (PET): The leading material for beverage bottles and jars due to its clarity, strength, and recyclability.

- Polyethylene (PE) - HDPE & LLDPE: High-density polyethylene (HDPE) is crucial for milk jugs, detergent bottles, and some food containers, while linear low-density polyethylene (LLDPE) is used in films for some tray applications.

- Polypropylene (PP): Increasingly favored for its heat resistance, making it suitable for microwavable containers and food trays.

The Food and Beverage sector's inherent demand, coupled with supportive economic policies and evolving consumer habits, solidifies its position as the primary engine of growth for the KSA Rigid Plastic Packaging Market.

KSA Rigid Plastic Packaging Market Product Landscape

The KSA Rigid Plastic Packaging Market is defined by a diverse product landscape catering to multifaceted industry needs. Key product categories include Bottles and Jars, essential for the beverage, food, and healthcare sectors, manufactured primarily from PET and HDPE. Trays and Containers are vital for food preservation, logistics, and retail display, utilizing materials like PP and PS. Caps and Closures play a critical role in product integrity and safety across all segments. Intermediate Bulk Containers (IBCs) and Drums are integral to industrial and chemical applications, emphasizing durability and containment. Pallets, while primarily serving logistics, also utilize rigid plastic for their strength and reusability. Innovations are focused on lightweighting for reduced material usage and transportation costs, enhanced barrier properties to extend shelf life, and improved recyclability. The development of specialized finishes, tamper-evident features, and ergonomic designs further distinguishes product offerings, meeting the evolving demands for convenience, safety, and sustainability from end-users.

Key Drivers, Barriers & Challenges in KSA Rigid Plastic Packaging Market

Key Drivers:

The KSA Rigid Plastic Packaging Market is propelled by several significant drivers. Economic diversification and Vision 2030 initiatives are fostering industrial growth and increasing domestic manufacturing capabilities, leading to higher demand for packaging solutions. A growing and young population with increasing disposable income fuels consumption of packaged goods across food, beverage, and personal care sectors. Technological advancements in material science and processing, enabling lightweighting, enhanced barrier properties, and improved recyclability, are critical. Furthermore, the expansion of the retail and e-commerce sectors necessitates efficient, protective, and appealing packaging. Increasing awareness of food safety and hygiene standards also drives demand for robust plastic packaging.

Barriers & Challenges:

Despite strong growth prospects, the market faces certain barriers and challenges. Fluctuations in raw material prices, primarily crude oil derivatives, can impact manufacturing costs and profitability. Stringent environmental regulations and growing consumer demand for sustainability are pushing for greater adoption of recycled content and alternative materials, requiring significant investment in new technologies and infrastructure. Competition from alternative packaging materials, though often less cost-effective, remains a consideration. Supply chain disruptions and logistics complexities, especially for imported raw materials or exported finished goods, can pose challenges. Moreover, public perception regarding plastic waste and pollution can create reputational hurdles, necessitating proactive communication and commitment to circular economy principles.

Emerging Opportunities in KSA Rigid Plastic Packaging Market

Emerging opportunities in the KSA Rigid Plastic Packaging Market lie in the growing demand for sustainable packaging solutions. This includes the increased use of recycled PET (rPET) and other recycled polymers in bottles and containers, driven by both regulatory push and consumer preference. The healthcare sector's expansion, with a focus on pharmaceuticals and medical devices, presents a significant avenue for growth, requiring high-barrier, sterile, and tamper-evident rigid plastic packaging. Furthermore, the development of advanced functional packaging, such as those with improved shelf-life extension capabilities or active packaging technologies, offers a premium market segment. The increasing adoption of e-commerce is also creating opportunities for specialized, resilient, and easily stackable rigid plastic packaging solutions designed for online retail. Finally, government incentives for local manufacturing and R&D in material science and recycling technologies can foster innovation and create new market niches.

Growth Accelerators in the KSA Rigid Plastic Packaging Market Industry

Several catalysts are accelerating growth in the KSA Rigid Plastic Packaging Market. Significant government investments in infrastructure and industrial development are creating a more conducive environment for manufacturing and supply chain efficiency. The strategic focus on diversifying the economy away from oil, as outlined in Vision 2030, is boosting demand for packaged consumer goods and industrial products. Technological advancements in polymer science and manufacturing processes, leading to cost efficiencies, enhanced product performance, and greater sustainability, are key accelerators. Strategic partnerships and collaborations between local and international players are facilitating technology transfer and market expansion. Finally, the ever-increasing consumer demand for convenience, safety, and quality in packaged goods across all end-use industries is a fundamental growth engine.

Key Players Shaping the KSA Rigid Plastic Packaging Market Market

- Packaging Product Company (PPC)

- Arabian Plastic Industrial Company Limited

- Zamil Plastic Industries Co

- 3P Gulf Group

- Al-Ghandoura Plastic Co (Ghanplast)

- Takween Advanced Industries

- Octal Group

- ColoredSun

- Saudi Plastic Factory Company

- Arnon Plastic Industries Co Ltd

- KANR for Plastic Industries

- SABIC (Saudi Basic Industries Corporation)

Notable Milestones in KSA Rigid Plastic Packaging Market Sector

- February 2022: Alpek announced its agreement to acquire OCTAL Holding SAOC, forward-integrating Alpek into the high-value PET sheet business segment, enhancing its ESG goals and ability to serve growing PET resin needs.

- January 2022: The Saudi Deputy Minister of Industry and Mineral Resources highlighted a forum as a significant step in enhancing Saudi Arabia's industrial position in the plastic industry, with a total investment of SAR 35 billion (USD 9.31 Billion) and over 1300 factories.

In-Depth KSA Rigid Plastic Packaging Market Market Outlook

The KSA Rigid Plastic Packaging Market outlook is exceptionally positive, driven by a robust interplay of economic development, favorable demographics, and strategic government initiatives. The sustained economic diversification under Vision 2030 is a primary growth accelerator, fostering increased domestic production and consumption of packaged goods. Advancements in material science and processing technologies are enabling the creation of more sustainable, lightweight, and functional packaging solutions, meeting evolving consumer and regulatory demands. The expanding healthcare and e-commerce sectors present significant untapped potential for specialized rigid plastic packaging. Strategic investments in recycling infrastructure and the adoption of circular economy principles will further solidify the market's long-term viability and appeal. Stakeholders can anticipate a period of sustained growth, characterized by innovation, strategic collaborations, and a heightened focus on environmental responsibility.

KSA Rigid Plastic Packaging Market Segmentation

-

1. Product

- 1.1. Bottles and Jars

- 1.2. Trays and Containers

- 1.3. Caps and Closures

- 1.4. Intermediate Bulk Containers (IBCs)

- 1.5. Drums

- 1.6. Pallets

- 1.7. Other Pr

-

2. Material

-

2.1. Polyethylene (PE)

- 2.1.1. LDPE and LLDPE

- 2.1.2. HDPE

- 2.2. Polyethylene Terephthalate (PET)

- 2.3. Polypropylene (PP)

- 2.4. Polystyrene (PS) and Expanded Polystyrene (EPS)

- 2.5. Polyvinyl Chloride (PVC)

- 2.6. Other Ri

-

2.1. Polyethylene (PE)

-

3. End-use Industry

- 3.1. Food

- 3.2. Beverage

- 3.3. Healthcare

- 3.4. Cosmetics and Personal Care

- 3.5. Industri

- 3.6. Building and Construction

- 3.7. Automotive

- 3.8. Other En

KSA Rigid Plastic Packaging Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

KSA Rigid Plastic Packaging Market Regional Market Share

Geographic Coverage of KSA Rigid Plastic Packaging Market

KSA Rigid Plastic Packaging Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.62% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Bottles and Jars

- 5.1.2. Trays and Containers

- 5.1.3. Caps and Closures

- 5.1.4. Intermediate Bulk Containers (IBCs)

- 5.1.5. Drums

- 5.1.6. Pallets

- 5.1.7. Other Pr

- 5.2. Market Analysis, Insights and Forecast - by Material

- 5.2.1. Polyethylene (PE)

- 5.2.1.1. LDPE and LLDPE

- 5.2.1.2. HDPE

- 5.2.2. Polyethylene Terephthalate (PET)

- 5.2.3. Polypropylene (PP)

- 5.2.4. Polystyrene (PS) and Expanded Polystyrene (EPS)

- 5.2.5. Polyvinyl Chloride (PVC)

- 5.2.6. Other Ri

- 5.2.1. Polyethylene (PE)

- 5.3. Market Analysis, Insights and Forecast - by End-use Industry

- 5.3.1. Food

- 5.3.2. Beverage

- 5.3.3. Healthcare

- 5.3.4. Cosmetics and Personal Care

- 5.3.5. Industri

- 5.3.6. Building and Construction

- 5.3.7. Automotive

- 5.3.8. Other En

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. South America

- 5.4.3. Europe

- 5.4.4. Middle East & Africa

- 5.4.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. Global KSA Rigid Plastic Packaging Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Bottles and Jars

- 6.1.2. Trays and Containers

- 6.1.3. Caps and Closures

- 6.1.4. Intermediate Bulk Containers (IBCs)

- 6.1.5. Drums

- 6.1.6. Pallets

- 6.1.7. Other Pr

- 6.2. Market Analysis, Insights and Forecast - by Material

- 6.2.1. Polyethylene (PE)

- 6.2.1.1. LDPE and LLDPE

- 6.2.1.2. HDPE

- 6.2.2. Polyethylene Terephthalate (PET)

- 6.2.3. Polypropylene (PP)

- 6.2.4. Polystyrene (PS) and Expanded Polystyrene (EPS)

- 6.2.5. Polyvinyl Chloride (PVC)

- 6.2.6. Other Ri

- 6.2.1. Polyethylene (PE)

- 6.3. Market Analysis, Insights and Forecast - by End-use Industry

- 6.3.1. Food

- 6.3.2. Beverage

- 6.3.3. Healthcare

- 6.3.4. Cosmetics and Personal Care

- 6.3.5. Industri

- 6.3.6. Building and Construction

- 6.3.7. Automotive

- 6.3.8. Other En

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. North America KSA Rigid Plastic Packaging Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product

- 7.1.1. Bottles and Jars

- 7.1.2. Trays and Containers

- 7.1.3. Caps and Closures

- 7.1.4. Intermediate Bulk Containers (IBCs)

- 7.1.5. Drums

- 7.1.6. Pallets

- 7.1.7. Other Pr

- 7.2. Market Analysis, Insights and Forecast - by Material

- 7.2.1. Polyethylene (PE)

- 7.2.1.1. LDPE and LLDPE

- 7.2.1.2. HDPE

- 7.2.2. Polyethylene Terephthalate (PET)

- 7.2.3. Polypropylene (PP)

- 7.2.4. Polystyrene (PS) and Expanded Polystyrene (EPS)

- 7.2.5. Polyvinyl Chloride (PVC)

- 7.2.6. Other Ri

- 7.2.1. Polyethylene (PE)

- 7.3. Market Analysis, Insights and Forecast - by End-use Industry

- 7.3.1. Food

- 7.3.2. Beverage

- 7.3.3. Healthcare

- 7.3.4. Cosmetics and Personal Care

- 7.3.5. Industri

- 7.3.6. Building and Construction

- 7.3.7. Automotive

- 7.3.8. Other En

- 7.1. Market Analysis, Insights and Forecast - by Product

- 8. South America KSA Rigid Plastic Packaging Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product

- 8.1.1. Bottles and Jars

- 8.1.2. Trays and Containers

- 8.1.3. Caps and Closures

- 8.1.4. Intermediate Bulk Containers (IBCs)

- 8.1.5. Drums

- 8.1.6. Pallets

- 8.1.7. Other Pr

- 8.2. Market Analysis, Insights and Forecast - by Material

- 8.2.1. Polyethylene (PE)

- 8.2.1.1. LDPE and LLDPE

- 8.2.1.2. HDPE

- 8.2.2. Polyethylene Terephthalate (PET)

- 8.2.3. Polypropylene (PP)

- 8.2.4. Polystyrene (PS) and Expanded Polystyrene (EPS)

- 8.2.5. Polyvinyl Chloride (PVC)

- 8.2.6. Other Ri

- 8.2.1. Polyethylene (PE)

- 8.3. Market Analysis, Insights and Forecast - by End-use Industry

- 8.3.1. Food

- 8.3.2. Beverage

- 8.3.3. Healthcare

- 8.3.4. Cosmetics and Personal Care

- 8.3.5. Industri

- 8.3.6. Building and Construction

- 8.3.7. Automotive

- 8.3.8. Other En

- 8.1. Market Analysis, Insights and Forecast - by Product

- 9. Europe KSA Rigid Plastic Packaging Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product

- 9.1.1. Bottles and Jars

- 9.1.2. Trays and Containers

- 9.1.3. Caps and Closures

- 9.1.4. Intermediate Bulk Containers (IBCs)

- 9.1.5. Drums

- 9.1.6. Pallets

- 9.1.7. Other Pr

- 9.2. Market Analysis, Insights and Forecast - by Material

- 9.2.1. Polyethylene (PE)

- 9.2.1.1. LDPE and LLDPE

- 9.2.1.2. HDPE

- 9.2.2. Polyethylene Terephthalate (PET)

- 9.2.3. Polypropylene (PP)

- 9.2.4. Polystyrene (PS) and Expanded Polystyrene (EPS)

- 9.2.5. Polyvinyl Chloride (PVC)

- 9.2.6. Other Ri

- 9.2.1. Polyethylene (PE)

- 9.3. Market Analysis, Insights and Forecast - by End-use Industry

- 9.3.1. Food

- 9.3.2. Beverage

- 9.3.3. Healthcare

- 9.3.4. Cosmetics and Personal Care

- 9.3.5. Industri

- 9.3.6. Building and Construction

- 9.3.7. Automotive

- 9.3.8. Other En

- 9.1. Market Analysis, Insights and Forecast - by Product

- 10. Middle East & Africa KSA Rigid Plastic Packaging Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product

- 10.1.1. Bottles and Jars

- 10.1.2. Trays and Containers

- 10.1.3. Caps and Closures

- 10.1.4. Intermediate Bulk Containers (IBCs)

- 10.1.5. Drums

- 10.1.6. Pallets

- 10.1.7. Other Pr

- 10.2. Market Analysis, Insights and Forecast - by Material

- 10.2.1. Polyethylene (PE)

- 10.2.1.1. LDPE and LLDPE

- 10.2.1.2. HDPE

- 10.2.2. Polyethylene Terephthalate (PET)

- 10.2.3. Polypropylene (PP)

- 10.2.4. Polystyrene (PS) and Expanded Polystyrene (EPS)

- 10.2.5. Polyvinyl Chloride (PVC)

- 10.2.6. Other Ri

- 10.2.1. Polyethylene (PE)

- 10.3. Market Analysis, Insights and Forecast - by End-use Industry

- 10.3.1. Food

- 10.3.2. Beverage

- 10.3.3. Healthcare

- 10.3.4. Cosmetics and Personal Care

- 10.3.5. Industri

- 10.3.6. Building and Construction

- 10.3.7. Automotive

- 10.3.8. Other En

- 10.1. Market Analysis, Insights and Forecast - by Product

- 11. Asia Pacific KSA Rigid Plastic Packaging Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product

- 11.1.1. Bottles and Jars

- 11.1.2. Trays and Containers

- 11.1.3. Caps and Closures

- 11.1.4. Intermediate Bulk Containers (IBCs)

- 11.1.5. Drums

- 11.1.6. Pallets

- 11.1.7. Other Pr

- 11.2. Market Analysis, Insights and Forecast - by Material

- 11.2.1. Polyethylene (PE)

- 11.2.1.1. LDPE and LLDPE

- 11.2.1.2. HDPE

- 11.2.2. Polyethylene Terephthalate (PET)

- 11.2.3. Polypropylene (PP)

- 11.2.4. Polystyrene (PS) and Expanded Polystyrene (EPS)

- 11.2.5. Polyvinyl Chloride (PVC)

- 11.2.6. Other Ri

- 11.2.1. Polyethylene (PE)

- 11.3. Market Analysis, Insights and Forecast - by End-use Industry

- 11.3.1. Food

- 11.3.2. Beverage

- 11.3.3. Healthcare

- 11.3.4. Cosmetics and Personal Care

- 11.3.5. Industri

- 11.3.6. Building and Construction

- 11.3.7. Automotive

- 11.3.8. Other En

- 11.1. Market Analysis, Insights and Forecast - by Product

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Packaging Product Company (PPC)

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Arabian Plastic Industrial Company Limited

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Zamil Plastic Industries Co

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 3P Gulf Group

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Al-Ghandoura Plastic Co (Ghanplast)

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Takween Advanced Industries

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Octal Group

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 ColoredSun

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Saudi Plastic Factory Company

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Arnon Plastic Industries Co Ltd*List Not Exhaustive

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 KANR for Plastic Industries

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 SABIC (Saudi Basic Industries Corporation)

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Packaging Product Company (PPC)

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global KSA Rigid Plastic Packaging Market Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America KSA Rigid Plastic Packaging Market Revenue (billion), by Product 2025 & 2033

- Figure 3: North America KSA Rigid Plastic Packaging Market Revenue Share (%), by Product 2025 & 2033

- Figure 4: North America KSA Rigid Plastic Packaging Market Revenue (billion), by Material 2025 & 2033

- Figure 5: North America KSA Rigid Plastic Packaging Market Revenue Share (%), by Material 2025 & 2033

- Figure 6: North America KSA Rigid Plastic Packaging Market Revenue (billion), by End-use Industry 2025 & 2033

- Figure 7: North America KSA Rigid Plastic Packaging Market Revenue Share (%), by End-use Industry 2025 & 2033

- Figure 8: North America KSA Rigid Plastic Packaging Market Revenue (billion), by Country 2025 & 2033

- Figure 9: North America KSA Rigid Plastic Packaging Market Revenue Share (%), by Country 2025 & 2033

- Figure 10: South America KSA Rigid Plastic Packaging Market Revenue (billion), by Product 2025 & 2033

- Figure 11: South America KSA Rigid Plastic Packaging Market Revenue Share (%), by Product 2025 & 2033

- Figure 12: South America KSA Rigid Plastic Packaging Market Revenue (billion), by Material 2025 & 2033

- Figure 13: South America KSA Rigid Plastic Packaging Market Revenue Share (%), by Material 2025 & 2033

- Figure 14: South America KSA Rigid Plastic Packaging Market Revenue (billion), by End-use Industry 2025 & 2033

- Figure 15: South America KSA Rigid Plastic Packaging Market Revenue Share (%), by End-use Industry 2025 & 2033

- Figure 16: South America KSA Rigid Plastic Packaging Market Revenue (billion), by Country 2025 & 2033

- Figure 17: South America KSA Rigid Plastic Packaging Market Revenue Share (%), by Country 2025 & 2033

- Figure 18: Europe KSA Rigid Plastic Packaging Market Revenue (billion), by Product 2025 & 2033

- Figure 19: Europe KSA Rigid Plastic Packaging Market Revenue Share (%), by Product 2025 & 2033

- Figure 20: Europe KSA Rigid Plastic Packaging Market Revenue (billion), by Material 2025 & 2033

- Figure 21: Europe KSA Rigid Plastic Packaging Market Revenue Share (%), by Material 2025 & 2033

- Figure 22: Europe KSA Rigid Plastic Packaging Market Revenue (billion), by End-use Industry 2025 & 2033

- Figure 23: Europe KSA Rigid Plastic Packaging Market Revenue Share (%), by End-use Industry 2025 & 2033

- Figure 24: Europe KSA Rigid Plastic Packaging Market Revenue (billion), by Country 2025 & 2033

- Figure 25: Europe KSA Rigid Plastic Packaging Market Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East & Africa KSA Rigid Plastic Packaging Market Revenue (billion), by Product 2025 & 2033

- Figure 27: Middle East & Africa KSA Rigid Plastic Packaging Market Revenue Share (%), by Product 2025 & 2033

- Figure 28: Middle East & Africa KSA Rigid Plastic Packaging Market Revenue (billion), by Material 2025 & 2033

- Figure 29: Middle East & Africa KSA Rigid Plastic Packaging Market Revenue Share (%), by Material 2025 & 2033

- Figure 30: Middle East & Africa KSA Rigid Plastic Packaging Market Revenue (billion), by End-use Industry 2025 & 2033

- Figure 31: Middle East & Africa KSA Rigid Plastic Packaging Market Revenue Share (%), by End-use Industry 2025 & 2033

- Figure 32: Middle East & Africa KSA Rigid Plastic Packaging Market Revenue (billion), by Country 2025 & 2033

- Figure 33: Middle East & Africa KSA Rigid Plastic Packaging Market Revenue Share (%), by Country 2025 & 2033

- Figure 34: Asia Pacific KSA Rigid Plastic Packaging Market Revenue (billion), by Product 2025 & 2033

- Figure 35: Asia Pacific KSA Rigid Plastic Packaging Market Revenue Share (%), by Product 2025 & 2033

- Figure 36: Asia Pacific KSA Rigid Plastic Packaging Market Revenue (billion), by Material 2025 & 2033

- Figure 37: Asia Pacific KSA Rigid Plastic Packaging Market Revenue Share (%), by Material 2025 & 2033

- Figure 38: Asia Pacific KSA Rigid Plastic Packaging Market Revenue (billion), by End-use Industry 2025 & 2033

- Figure 39: Asia Pacific KSA Rigid Plastic Packaging Market Revenue Share (%), by End-use Industry 2025 & 2033

- Figure 40: Asia Pacific KSA Rigid Plastic Packaging Market Revenue (billion), by Country 2025 & 2033

- Figure 41: Asia Pacific KSA Rigid Plastic Packaging Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global KSA Rigid Plastic Packaging Market Revenue billion Forecast, by Product 2020 & 2033

- Table 2: Global KSA Rigid Plastic Packaging Market Revenue billion Forecast, by Material 2020 & 2033

- Table 3: Global KSA Rigid Plastic Packaging Market Revenue billion Forecast, by End-use Industry 2020 & 2033

- Table 4: Global KSA Rigid Plastic Packaging Market Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Global KSA Rigid Plastic Packaging Market Revenue billion Forecast, by Product 2020 & 2033

- Table 6: Global KSA Rigid Plastic Packaging Market Revenue billion Forecast, by Material 2020 & 2033

- Table 7: Global KSA Rigid Plastic Packaging Market Revenue billion Forecast, by End-use Industry 2020 & 2033

- Table 8: Global KSA Rigid Plastic Packaging Market Revenue billion Forecast, by Country 2020 & 2033

- Table 9: United States KSA Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Canada KSA Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Mexico KSA Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Global KSA Rigid Plastic Packaging Market Revenue billion Forecast, by Product 2020 & 2033

- Table 13: Global KSA Rigid Plastic Packaging Market Revenue billion Forecast, by Material 2020 & 2033

- Table 14: Global KSA Rigid Plastic Packaging Market Revenue billion Forecast, by End-use Industry 2020 & 2033

- Table 15: Global KSA Rigid Plastic Packaging Market Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Brazil KSA Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Argentina KSA Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Rest of South America KSA Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Global KSA Rigid Plastic Packaging Market Revenue billion Forecast, by Product 2020 & 2033

- Table 20: Global KSA Rigid Plastic Packaging Market Revenue billion Forecast, by Material 2020 & 2033

- Table 21: Global KSA Rigid Plastic Packaging Market Revenue billion Forecast, by End-use Industry 2020 & 2033

- Table 22: Global KSA Rigid Plastic Packaging Market Revenue billion Forecast, by Country 2020 & 2033

- Table 23: United Kingdom KSA Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Germany KSA Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: France KSA Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Italy KSA Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Spain KSA Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Russia KSA Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: Benelux KSA Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Nordics KSA Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Rest of Europe KSA Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Global KSA Rigid Plastic Packaging Market Revenue billion Forecast, by Product 2020 & 2033

- Table 33: Global KSA Rigid Plastic Packaging Market Revenue billion Forecast, by Material 2020 & 2033

- Table 34: Global KSA Rigid Plastic Packaging Market Revenue billion Forecast, by End-use Industry 2020 & 2033

- Table 35: Global KSA Rigid Plastic Packaging Market Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Turkey KSA Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Israel KSA Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: GCC KSA Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: North Africa KSA Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: South Africa KSA Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: Rest of Middle East & Africa KSA Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Global KSA Rigid Plastic Packaging Market Revenue billion Forecast, by Product 2020 & 2033

- Table 43: Global KSA Rigid Plastic Packaging Market Revenue billion Forecast, by Material 2020 & 2033

- Table 44: Global KSA Rigid Plastic Packaging Market Revenue billion Forecast, by End-use Industry 2020 & 2033

- Table 45: Global KSA Rigid Plastic Packaging Market Revenue billion Forecast, by Country 2020 & 2033

- Table 46: China KSA Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 47: India KSA Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Japan KSA Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 49: South Korea KSA Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: ASEAN KSA Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 51: Oceania KSA Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Rest of Asia Pacific KSA Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the KSA Rigid Plastic Packaging Market?

The projected CAGR is approximately 5.62%.

2. Which companies are prominent players in the KSA Rigid Plastic Packaging Market?

Key companies in the market include Packaging Product Company (PPC), Arabian Plastic Industrial Company Limited, Zamil Plastic Industries Co, 3P Gulf Group, Al-Ghandoura Plastic Co (Ghanplast), Takween Advanced Industries, Octal Group, ColoredSun, Saudi Plastic Factory Company, Arnon Plastic Industries Co Ltd*List Not Exhaustive, KANR for Plastic Industries, SABIC (Saudi Basic Industries Corporation).

3. What are the main segments of the KSA Rigid Plastic Packaging Market?

The market segments include Product, Material, End-use Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 14.81 billion as of 2022.

5. What are some drivers contributing to market growth?

Demand for Oxo-degradable Plastics is Expected to Increase with New Regulations Being Enforced; Increasing Rigid Plastic Packaging Solutions Demand Across the End-user Industry.

6. What are the notable trends driving market growth?

Increasing Demand across End-user Sectors to Drive the Market.

7. Are there any restraints impacting market growth?

Environmental Concerns Over Recycling and Safe Disposal and Price Volatility of Raw Materials.

8. Can you provide examples of recent developments in the market?

February 2022 - Alpek announced that it had signed an agreement to acquire OCTAL Holding SAOC. The acquisition forward-integrates Alpek into the high-value PET sheet business segment, which closes the gap towards achieving its ESG goals. It enhances its ability to serve its customers' growing PET resin needs.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "KSA Rigid Plastic Packaging Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the KSA Rigid Plastic Packaging Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the KSA Rigid Plastic Packaging Market?

To stay informed about further developments, trends, and reports in the KSA Rigid Plastic Packaging Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence