Key Insights

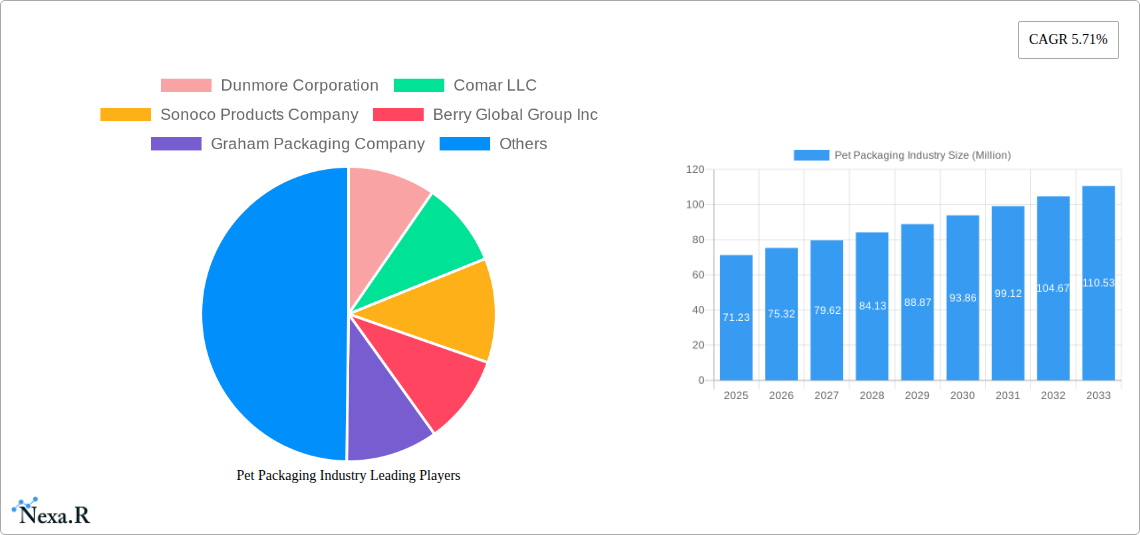

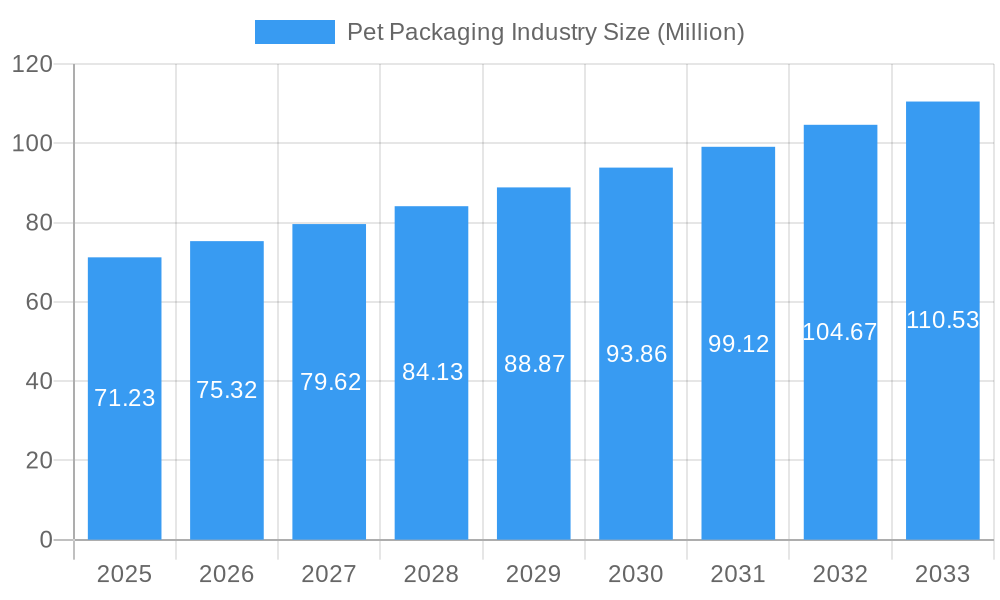

The global Pet Packaging market is poised for substantial growth, reaching an estimated USD 71.23 million by 2025 and is projected to expand at a robust Compound Annual Growth Rate (CAGR) of 5.71% during the forecast period of 2025-2033. This upward trajectory is primarily driven by the increasing demand for sustainable and lightweight packaging solutions, especially within the burgeoning food and beverage and pharmaceutical sectors. As consumers become more health-conscious and environmentally aware, the preference for PET (Polyethylene Terephthalate) packaging, known for its recyclability and barrier properties, is set to surge. Furthermore, advancements in manufacturing technologies are leading to innovative PET packaging designs, including enhanced barrier properties and aesthetically appealing finishes, catering to the evolving needs of end-users. The convenience and safety offered by PET packaging for various products, from everyday consumables to sensitive pharmaceutical formulations, also contribute significantly to its market dominance.

Pet Packaging Industry Market Size (In Million)

The market's expansion is further bolstered by trends such as the growing adoption of flexible PET packaging, offering greater versatility and reduced material usage, particularly in the form of bags and pouches for snacks and personal care items. The industrial goods and household products segments are also witnessing a steady demand for PET packaging due to its durability and cost-effectiveness. While the market presents significant opportunities, certain restraints, such as fluctuating raw material prices and increasing regulatory scrutiny regarding plastic waste, require strategic navigation. Key players like Amcor Ltd, Berry Global Group Inc., and Sonoco Products Company are actively investing in research and development to introduce eco-friendly PET packaging alternatives and enhance their production capabilities. Geographically, the Asia Pacific region is anticipated to be a significant growth engine, driven by rapid industrialization and a growing middle class.

Pet Packaging Industry Company Market Share

This in-depth report provides an exhaustive overview of the global Pet Packaging Industry, meticulously analyzing market dynamics, growth trends, and future opportunities. Delve into the intricate landscape of parent and child markets, understanding how evolving consumer demands and technological advancements are reshaping the industry. With a study period spanning from 2019 to 2033, our analysis offers unparalleled insights into market evolution and strategic foresight.

Pet Packaging Industry Market Dynamics & Structure

The Pet Packaging Industry is characterized by a moderately concentrated market structure, with a mix of large multinational corporations and specialized regional players. Technological innovation is a significant driver, focusing on sustainable materials, enhanced barrier properties, and smart packaging solutions. Regulatory frameworks, particularly those concerning food safety and environmental impact, are increasingly influencing product development and material choices. Competitive product substitutes, while present, often fall short of the unique combination of durability, transparency, and cost-effectiveness offered by PET. End-user demographics are shifting towards younger, environmentally conscious consumers who demand sustainable and convenient packaging options. Mergers and acquisitions (M&A) are active, aimed at consolidating market share, expanding product portfolios, and gaining access to new technologies.

- Market Concentration: Dominated by a few key players, but with significant room for niche specialists.

- Technological Innovation Drivers: Focus on recyclability, biodegradability, lightweighting, and barrier enhancement.

- Regulatory Frameworks: Strict adherence to food contact regulations and increasing pressure for circular economy solutions.

- Competitive Product Substitutes: Glass, metal, and certain bioplastics present challenges but often lack PET's specific advantages.

- End-user Demographics: Growing demand for convenience, eco-friendly options, and transparent product information.

- M&A Trends: Strategic acquisitions to strengthen market position, acquire innovative technologies, and broaden geographical reach.

Pet Packaging Industry Growth Trends & Insights

The Pet Packaging Industry is poised for robust growth, fueled by increasing demand across diverse end-user sectors and a growing emphasis on sustainable packaging solutions. The market size is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 6.2% from 2025 to 2033, reaching an estimated value of $220,500 Million units by 2033. This expansion is underpinned by rising disposable incomes globally, leading to increased consumption of packaged goods. Adoption rates for advanced PET formulations, including those with enhanced recyclability and barrier properties, are accelerating. Technological disruptions, such as innovations in chemical recycling and the development of bio-based PET alternatives, are poised to further revolutionize the industry. Consumer behavior shifts, particularly the heightened awareness of environmental impact and a preference for brands demonstrating sustainability commitments, are acting as significant market accelerators. The flexibility and versatility of PET packaging make it an ideal choice for a wide array of products, from beverages and food to personal care items and pharmaceuticals, ensuring its continued relevance.

- Market Size Evolution: From an estimated $135,800 Million units in 2025, the market is projected to reach $220,500 Million units by 2033.

- Adoption Rates: Increasing adoption of recycled PET (rPET) and innovative PET blends for enhanced sustainability.

- Technological Disruptions: Advancements in chemical recycling, laser etching for traceability, and lightweighting technologies.

- Consumer Behavior Shifts: Growing preference for transparent packaging, sustainable materials, and brands with strong environmental credentials.

- CAGR (2025-2033): Projected at 6.2%, indicating sustained and healthy market expansion.

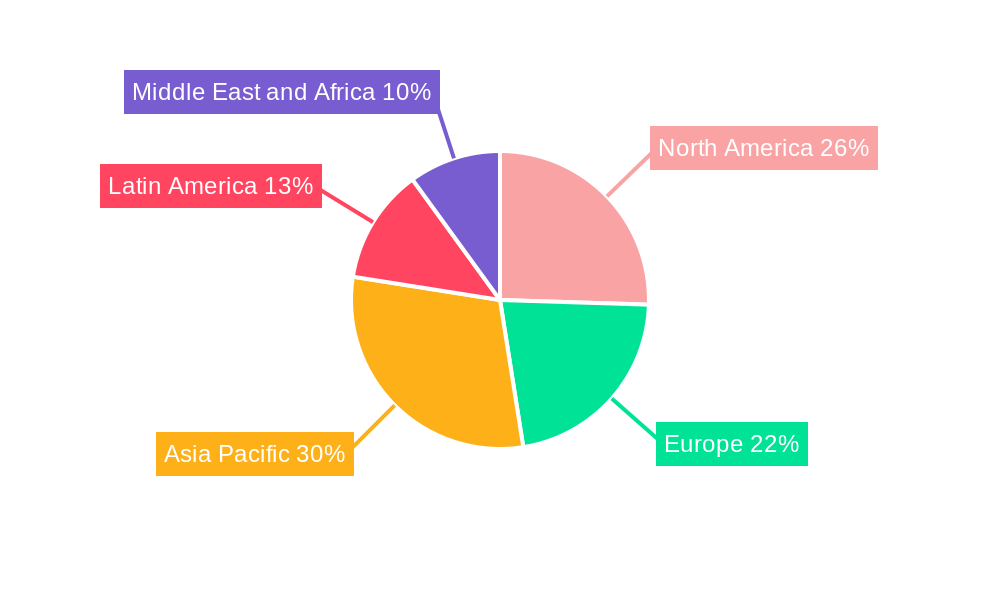

Dominant Regions, Countries, or Segments in Pet Packaging Industry

The Asia Pacific region is emerging as the dominant force in the Pet Packaging Industry, driven by rapid economic expansion, a burgeoning middle class, and significant investments in manufacturing and infrastructure. Within this region, China stands out as a key market, propelled by its massive consumer base and its role as a global manufacturing hub. The Food and Beverage end-user industry is the largest segment, accounting for a substantial portion of PET packaging consumption due to the inherent properties of PET, such as its clarity, strength, and barrier capabilities, making it ideal for preserving product freshness and extending shelf life. Among product types, Bottles and Jars represent the leading segment, particularly for carbonated and non-carbonated beverages, edible oils, and sauces, with an estimated market share of 35%. The Rigid packaging segment also holds a dominant position, favored for its protective qualities and structural integrity. Economic policies in emerging economies, such as favorable trade agreements and investments in industrial zones, coupled with the continuous development of advanced recycling infrastructure, are further cementing the dominance of these regions and segments.

- Dominant Region: Asia Pacific, particularly China.

- Leading End-user Industry: Food and Beverage.

- Dominant Product Type: Bottles and Jars, estimated at 35% market share.

- Dominant Packaging Type: Rigid packaging.

- Key Drivers of Dominance: Rapid economic growth, large consumer bases, favorable government policies, and evolving recycling infrastructure.

- Growth Potential: Significant untapped markets and increasing demand for premium and convenience products in emerging economies.

Pet Packaging Industry Product Landscape

The PET packaging product landscape is characterized by continuous innovation aimed at enhancing functionality, sustainability, and aesthetic appeal. Bottles and jars, crucial for the beverage and food sectors, are seeing advancements in lightweighting and improved barrier properties to extend shelf life. Bags and pouches are evolving with enhanced seal integrity and retort capabilities for wider food applications. Trays are increasingly designed for recyclability and microwave-friendliness, catering to the convenience food market. Lids, caps, and closures are benefiting from child-resistant features and tamper-evident designs, prioritizing safety and security. Unique selling propositions revolve around superior transparency, excellent impact resistance, and chemical inertness, ensuring product integrity. Technological advancements are enabling the incorporation of smart features, such as temperature indicators and traceability markers, to enhance consumer experience and supply chain efficiency.

Key Drivers, Barriers & Challenges in Pet Packaging Industry

Key Drivers:

- Growing Demand for Packaged Goods: Rising global population and urbanization are increasing the consumption of convenience and pre-packaged products.

- Sustainability Initiatives: The push for recyclability and the use of recycled PET (rPET) is a major driver, aligning with corporate ESG goals and consumer preferences.

- Versatility and Cost-Effectiveness: PET offers an excellent balance of properties, including clarity, strength, and barrier protection, at a competitive price point.

- Innovation in Design and Functionality: Development of lightweighting, enhanced barrier technologies, and smart packaging solutions.

Barriers & Challenges:

- Competition from Alternative Materials: While PET is dominant, materials like glass, metal, and emerging bioplastics offer competitive alternatives in specific applications.

- Recycling Infrastructure Gaps: Inconsistent and underdeveloped recycling infrastructure in certain regions can limit the effective collection and reprocessing of PET.

- Fluctuations in Raw Material Prices: Volatility in the prices of crude oil and ethylene, key feedstocks for PET production, can impact manufacturing costs.

- Regulatory Scrutiny on Plastic Use: Increasing global regulations and public perception regarding plastic pollution can create challenges for PET manufacturers.

- Supply Chain Disruptions: Global events can impact the availability and cost of raw materials and finished products, affecting market stability.

Emerging Opportunities in Pet Packaging Industry

Emerging opportunities in the Pet Packaging Industry lie in the advancement and widespread adoption of chemical recycling technologies, which can process mixed plastic waste and create high-quality recycled PET. The development and integration of bio-based PET alternatives, derived from renewable resources, present a significant avenue for growth, appealing to environmentally conscious consumers and brands. Furthermore, the increasing demand for personalized and on-the-go consumption patterns is driving opportunities for innovative, smaller-format PET packaging solutions with enhanced portability and convenience. The integration of smart packaging features, such as NFC tags for enhanced product information and supply chain traceability, also represents a burgeoning area of growth, offering added value to consumers and manufacturers alike.

Growth Accelerators in the Pet Packaging Industry Industry

Long-term growth in the Pet Packaging Industry will be significantly accelerated by breakthroughs in sustainable material science, including the development of advanced bio-PET and highly efficient chemical recycling processes that enable a truly circular economy for PET. Strategic partnerships between PET resin producers, packaging converters, and major brand owners are crucial for driving innovation and ensuring market adoption of new technologies and sustainable solutions. Market expansion into developing economies, driven by increasing consumer purchasing power and a growing demand for packaged goods, will also act as a key growth accelerator. Furthermore, the ongoing development of lightweighting technologies will continue to reduce material usage and transportation costs, enhancing the overall economic and environmental attractiveness of PET packaging.

Key Players Shaping the Pet Packaging Industry Market

- Amcor Ltd

- Berry Global Group Inc

- Comar LLC

- Dunmore Corporation

- Gerresheimer AG

- Graham Packaging Company

- GTX Hanex Plastic Sp z o o

- Huhtamaki OYJ

- Nampak Limited

- Resilux NV

- Silgan Holdings Inc

- Sonoco Products Company

Notable Milestones in Pet Packaging Industry Sector

- April 2022: Mondi launched new packaging solutions for the food industry at AnugaFoodTec in Cologne, Germany. Two-tray packaging products provide recyclable options for fresh food manufacturers, which will help to reduce food waste. High-barrier food protection will be provided by PerFORMing Monoloop and Mono Formable PP, illustrating the crucial role that packaging plays throughout the supply chain.

- January 2022: Sonoco Products Company completed the acquisition of Ball Metalpack, a manufacturer of sustainable tinplate food; the collaboration will expand the sustainable packaging portfolio to include tinplate packaging.

In-Depth Pet Packaging Industry Market Outlook

The Pet Packaging Industry is on a trajectory of sustained growth, driven by a confluence of factors including rising global demand for packaged goods, escalating consumer preference for sustainable solutions, and continuous technological advancements. The outlook for the market is exceptionally positive, with significant opportunities arising from the widespread adoption of recycled PET (rPET) and the development of novel bio-based PET materials. Innovations in chemical recycling are set to unlock new avenues for material circularity, addressing environmental concerns and bolstering the industry's sustainable credentials. Strategic collaborations and market expansions into emerging economies will further fuel this growth, solidifying PET packaging's indispensable role across various end-user sectors. The industry is well-positioned to capitalize on these trends, offering a robust and evolving packaging solution for the future.

Pet Packaging Industry Segmentation

-

1. Product Types

- 1.1. Bottles and Jars

- 1.2. Bags and Pouches

- 1.3. Trays

- 1.4. Lids/Caps and Closures

- 1.5. Other Product Types

-

2. Packaging

- 2.1. Rigid

- 2.2. Flexible

-

3. End-user Industry

- 3.1. Food and Beverage

- 3.2. Pharmaceuticals

- 3.3. Personal Care and Cosmetic Industry

- 3.4. Industrial Goods

- 3.5. Household Products

- 3.6. Other End-user Industries

Pet Packaging Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

-

4. Latin America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of Latin America

-

5. Middle East and Africa

- 5.1. United Arab Emirates

- 5.2. Saudi Arabia

- 5.3. South Africa

- 5.4. Rest of Middle East and Africa

Pet Packaging Industry Regional Market Share

Geographic Coverage of Pet Packaging Industry

Pet Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.71% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Types

- 5.1.1. Bottles and Jars

- 5.1.2. Bags and Pouches

- 5.1.3. Trays

- 5.1.4. Lids/Caps and Closures

- 5.1.5. Other Product Types

- 5.2. Market Analysis, Insights and Forecast - by Packaging

- 5.2.1. Rigid

- 5.2.2. Flexible

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Food and Beverage

- 5.3.2. Pharmaceuticals

- 5.3.3. Personal Care and Cosmetic Industry

- 5.3.4. Industrial Goods

- 5.3.5. Household Products

- 5.3.6. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Latin America

- 5.4.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Product Types

- 6. Global Pet Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Types

- 6.1.1. Bottles and Jars

- 6.1.2. Bags and Pouches

- 6.1.3. Trays

- 6.1.4. Lids/Caps and Closures

- 6.1.5. Other Product Types

- 6.2. Market Analysis, Insights and Forecast - by Packaging

- 6.2.1. Rigid

- 6.2.2. Flexible

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Food and Beverage

- 6.3.2. Pharmaceuticals

- 6.3.3. Personal Care and Cosmetic Industry

- 6.3.4. Industrial Goods

- 6.3.5. Household Products

- 6.3.6. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Product Types

- 7. North America Pet Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Types

- 7.1.1. Bottles and Jars

- 7.1.2. Bags and Pouches

- 7.1.3. Trays

- 7.1.4. Lids/Caps and Closures

- 7.1.5. Other Product Types

- 7.2. Market Analysis, Insights and Forecast - by Packaging

- 7.2.1. Rigid

- 7.2.2. Flexible

- 7.3. Market Analysis, Insights and Forecast - by End-user Industry

- 7.3.1. Food and Beverage

- 7.3.2. Pharmaceuticals

- 7.3.3. Personal Care and Cosmetic Industry

- 7.3.4. Industrial Goods

- 7.3.5. Household Products

- 7.3.6. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Product Types

- 8. Europe Pet Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Types

- 8.1.1. Bottles and Jars

- 8.1.2. Bags and Pouches

- 8.1.3. Trays

- 8.1.4. Lids/Caps and Closures

- 8.1.5. Other Product Types

- 8.2. Market Analysis, Insights and Forecast - by Packaging

- 8.2.1. Rigid

- 8.2.2. Flexible

- 8.3. Market Analysis, Insights and Forecast - by End-user Industry

- 8.3.1. Food and Beverage

- 8.3.2. Pharmaceuticals

- 8.3.3. Personal Care and Cosmetic Industry

- 8.3.4. Industrial Goods

- 8.3.5. Household Products

- 8.3.6. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Product Types

- 9. Asia Pacific Pet Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Types

- 9.1.1. Bottles and Jars

- 9.1.2. Bags and Pouches

- 9.1.3. Trays

- 9.1.4. Lids/Caps and Closures

- 9.1.5. Other Product Types

- 9.2. Market Analysis, Insights and Forecast - by Packaging

- 9.2.1. Rigid

- 9.2.2. Flexible

- 9.3. Market Analysis, Insights and Forecast - by End-user Industry

- 9.3.1. Food and Beverage

- 9.3.2. Pharmaceuticals

- 9.3.3. Personal Care and Cosmetic Industry

- 9.3.4. Industrial Goods

- 9.3.5. Household Products

- 9.3.6. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Product Types

- 10. Latin America Pet Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Types

- 10.1.1. Bottles and Jars

- 10.1.2. Bags and Pouches

- 10.1.3. Trays

- 10.1.4. Lids/Caps and Closures

- 10.1.5. Other Product Types

- 10.2. Market Analysis, Insights and Forecast - by Packaging

- 10.2.1. Rigid

- 10.2.2. Flexible

- 10.3. Market Analysis, Insights and Forecast - by End-user Industry

- 10.3.1. Food and Beverage

- 10.3.2. Pharmaceuticals

- 10.3.3. Personal Care and Cosmetic Industry

- 10.3.4. Industrial Goods

- 10.3.5. Household Products

- 10.3.6. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Product Types

- 11. Middle East and Africa Pet Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Types

- 11.1.1. Bottles and Jars

- 11.1.2. Bags and Pouches

- 11.1.3. Trays

- 11.1.4. Lids/Caps and Closures

- 11.1.5. Other Product Types

- 11.2. Market Analysis, Insights and Forecast - by Packaging

- 11.2.1. Rigid

- 11.2.2. Flexible

- 11.3. Market Analysis, Insights and Forecast - by End-user Industry

- 11.3.1. Food and Beverage

- 11.3.2. Pharmaceuticals

- 11.3.3. Personal Care and Cosmetic Industry

- 11.3.4. Industrial Goods

- 11.3.5. Household Products

- 11.3.6. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Product Types

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Dunmore Corporation

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Comar LLC

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Sonoco Products Company

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Berry Global Group Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Graham Packaging Company

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Huhtamaki OYJ

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Nampak Limited*List Not Exhaustive

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Resilux NV

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Silgan Holdings Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Gerresheimer AG

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 GTX Hanex Plastic Sp z o o

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Amcor Ltd

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Dunmore Corporation

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Pet Packaging Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Pet Packaging Industry Revenue (Million), by Product Types 2025 & 2033

- Figure 3: North America Pet Packaging Industry Revenue Share (%), by Product Types 2025 & 2033

- Figure 4: North America Pet Packaging Industry Revenue (Million), by Packaging 2025 & 2033

- Figure 5: North America Pet Packaging Industry Revenue Share (%), by Packaging 2025 & 2033

- Figure 6: North America Pet Packaging Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 7: North America Pet Packaging Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 8: North America Pet Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: North America Pet Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Pet Packaging Industry Revenue (Million), by Product Types 2025 & 2033

- Figure 11: Europe Pet Packaging Industry Revenue Share (%), by Product Types 2025 & 2033

- Figure 12: Europe Pet Packaging Industry Revenue (Million), by Packaging 2025 & 2033

- Figure 13: Europe Pet Packaging Industry Revenue Share (%), by Packaging 2025 & 2033

- Figure 14: Europe Pet Packaging Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 15: Europe Pet Packaging Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 16: Europe Pet Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Europe Pet Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Pet Packaging Industry Revenue (Million), by Product Types 2025 & 2033

- Figure 19: Asia Pacific Pet Packaging Industry Revenue Share (%), by Product Types 2025 & 2033

- Figure 20: Asia Pacific Pet Packaging Industry Revenue (Million), by Packaging 2025 & 2033

- Figure 21: Asia Pacific Pet Packaging Industry Revenue Share (%), by Packaging 2025 & 2033

- Figure 22: Asia Pacific Pet Packaging Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 23: Asia Pacific Pet Packaging Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: Asia Pacific Pet Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Asia Pacific Pet Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Latin America Pet Packaging Industry Revenue (Million), by Product Types 2025 & 2033

- Figure 27: Latin America Pet Packaging Industry Revenue Share (%), by Product Types 2025 & 2033

- Figure 28: Latin America Pet Packaging Industry Revenue (Million), by Packaging 2025 & 2033

- Figure 29: Latin America Pet Packaging Industry Revenue Share (%), by Packaging 2025 & 2033

- Figure 30: Latin America Pet Packaging Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 31: Latin America Pet Packaging Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 32: Latin America Pet Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: Latin America Pet Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Middle East and Africa Pet Packaging Industry Revenue (Million), by Product Types 2025 & 2033

- Figure 35: Middle East and Africa Pet Packaging Industry Revenue Share (%), by Product Types 2025 & 2033

- Figure 36: Middle East and Africa Pet Packaging Industry Revenue (Million), by Packaging 2025 & 2033

- Figure 37: Middle East and Africa Pet Packaging Industry Revenue Share (%), by Packaging 2025 & 2033

- Figure 38: Middle East and Africa Pet Packaging Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 39: Middle East and Africa Pet Packaging Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 40: Middle East and Africa Pet Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Middle East and Africa Pet Packaging Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Pet Packaging Industry Revenue Million Forecast, by Product Types 2020 & 2033

- Table 2: Global Pet Packaging Industry Revenue Million Forecast, by Packaging 2020 & 2033

- Table 3: Global Pet Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 4: Global Pet Packaging Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Pet Packaging Industry Revenue Million Forecast, by Product Types 2020 & 2033

- Table 6: Global Pet Packaging Industry Revenue Million Forecast, by Packaging 2020 & 2033

- Table 7: Global Pet Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 8: Global Pet Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: United States Pet Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Canada Pet Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Global Pet Packaging Industry Revenue Million Forecast, by Product Types 2020 & 2033

- Table 12: Global Pet Packaging Industry Revenue Million Forecast, by Packaging 2020 & 2033

- Table 13: Global Pet Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 14: Global Pet Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 15: Germany Pet Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: United Kingdom Pet Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: France Pet Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Italy Pet Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Spain Pet Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Rest of Europe Pet Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Global Pet Packaging Industry Revenue Million Forecast, by Product Types 2020 & 2033

- Table 22: Global Pet Packaging Industry Revenue Million Forecast, by Packaging 2020 & 2033

- Table 23: Global Pet Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 24: Global Pet Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 25: China Pet Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Japan Pet Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: India Pet Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: South Korea Pet Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: Rest of Asia Pacific Pet Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Global Pet Packaging Industry Revenue Million Forecast, by Product Types 2020 & 2033

- Table 31: Global Pet Packaging Industry Revenue Million Forecast, by Packaging 2020 & 2033

- Table 32: Global Pet Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 33: Global Pet Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 34: Brazil Pet Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: Argentina Pet Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Latin America Pet Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: Global Pet Packaging Industry Revenue Million Forecast, by Product Types 2020 & 2033

- Table 38: Global Pet Packaging Industry Revenue Million Forecast, by Packaging 2020 & 2033

- Table 39: Global Pet Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 40: Global Pet Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 41: United Arab Emirates Pet Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Saudi Arabia Pet Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 43: South Africa Pet Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: Rest of Middle East and Africa Pet Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Pet Packaging Industry?

The projected CAGR is approximately 5.71%.

2. Which companies are prominent players in the Pet Packaging Industry?

Key companies in the market include Dunmore Corporation, Comar LLC, Sonoco Products Company, Berry Global Group Inc, Graham Packaging Company, Huhtamaki OYJ, Nampak Limited*List Not Exhaustive, Resilux NV, Silgan Holdings Inc, Gerresheimer AG, GTX Hanex Plastic Sp z o o, Amcor Ltd.

3. What are the main segments of the Pet Packaging Industry?

The market segments include Product Types, Packaging, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 71.23 Million as of 2022.

5. What are some drivers contributing to market growth?

Outstanding Properties of PET; Rising Demand for Environment-friendly Packaging.

6. What are the notable trends driving market growth?

Bottles to Have Significant Growth.

7. Are there any restraints impacting market growth?

Regulations Against the Use of Plastics in Some Regions.

8. Can you provide examples of recent developments in the market?

April 2022: Mondi launched new packaging solutions for the food industry at AnugaFoodTec in Cologne, Germany. Two-tray packaging products provide recyclable options for fresh food manufacturers, which will help to reduce food waste. High-barrier food protection will be provided by PerFORMing Monoloopand Mono Formable PP, illustrating the crucial role that packaging plays throughout the supply chain.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Pet Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Pet Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Pet Packaging Industry?

To stay informed about further developments, trends, and reports in the Pet Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence