Key Insights

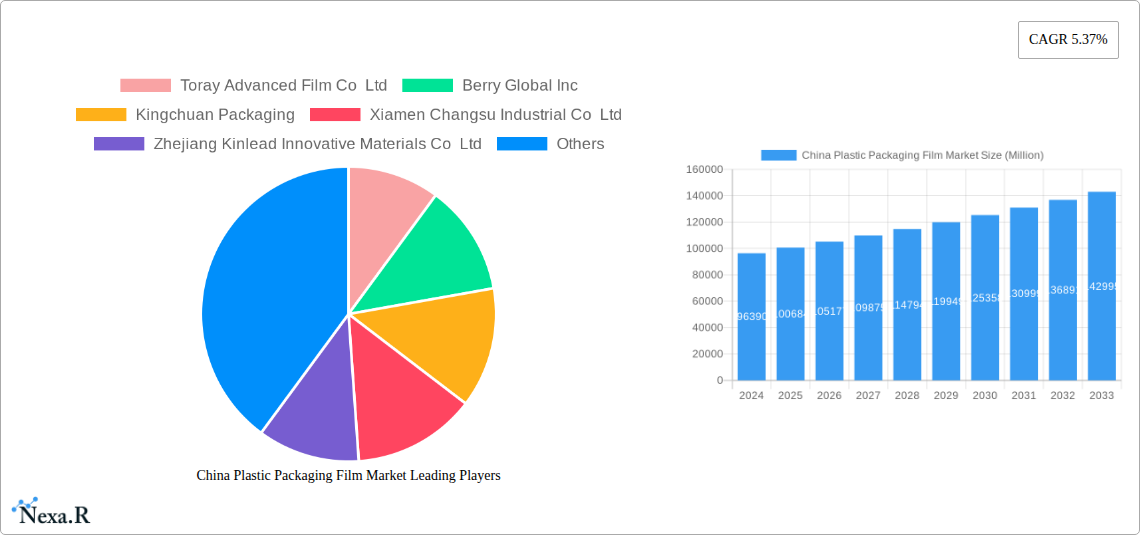

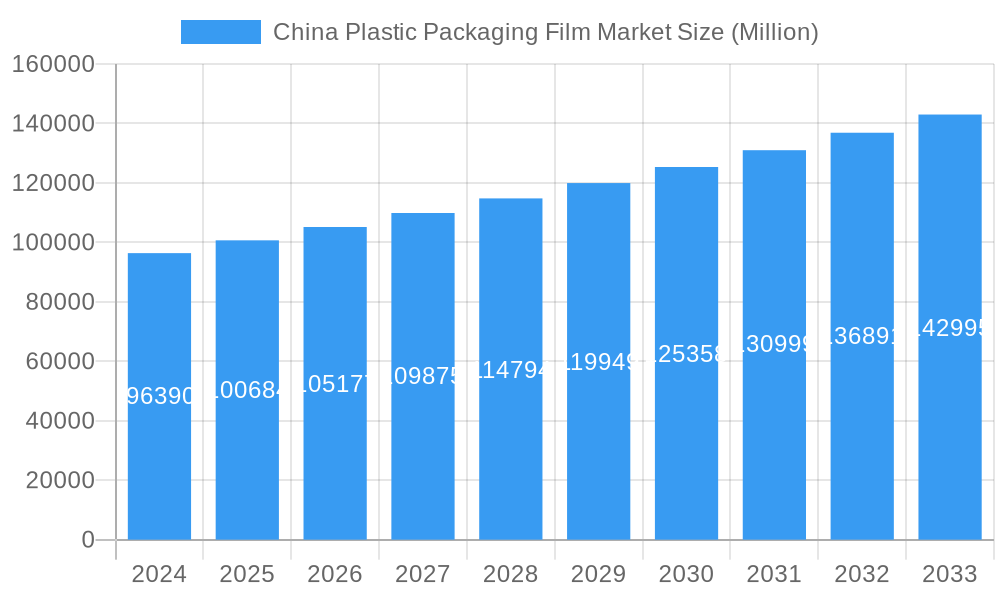

The China plastic packaging film market is poised for robust growth, estimated at USD 96.39 billion in 2024, and is projected to expand at a Compound Annual Growth Rate (CAGR) of 4.5% from 2025 to 2033. This significant market value underscores the indispensable role of plastic packaging films in China's diverse and rapidly evolving economy. The market is propelled by the burgeoning demand from the food industry, particularly in segments like candy & confectionery, frozen foods, and fresh produce, where enhanced shelf life, product protection, and visual appeal are paramount. Furthermore, the expanding healthcare sector, driven by an aging population and increased healthcare spending, along with the consistent demand from personal care & home care products, are key contributors to this growth. Industrial packaging also plays a crucial role, supporting China's manufacturing and export prowess.

China Plastic Packaging Film Market Market Size (In Billion)

The dynamic landscape of the China plastic packaging film market is shaped by several key drivers, including ongoing urbanization, a rising middle class with increased disposable income, and a growing consumer preference for convenient and safely packaged goods. Innovations in film technology, such as the development of advanced barrier properties, improved recyclability, and the increasing adoption of bio-based and sustainable film alternatives, are also shaping market trends. While the market enjoys strong growth, potential restraints could include increasing environmental regulations and a growing consumer awareness driving a shift towards more sustainable packaging solutions. The market is segmented across various film types including Polypropylene (PP), Polyethylene (PE), Polystyrene (PS), Bio-Based films, PVC, EVOH, and PETG, each catering to specific application needs and end-user requirements.

China Plastic Packaging Film Market Company Market Share

Here's a comprehensive, SEO-optimized report description for the China Plastic Packaging Film Market, meticulously crafted without placeholders and adhering to all your specified requirements:

Report Title: China Plastic Packaging Film Market: Growth, Trends, and Forecast 2019-2033 | Dominant Segments, Key Players, and Innovations

Report Description:

Uncover the dynamic landscape of the China Plastic Packaging Film Market with our in-depth analysis. This report provides a definitive outlook on the China plastic packaging film market size, plastic film market trends, and growth forecasts from 2019 to 2033, with a focus on the base year 2025. Dive into the intricate market dynamics, identify dominant regions and segments, and understand the product innovations shaping the future of packaging. We meticulously examine the parent market and key child markets, offering unparalleled insights into flexible packaging film market growth and adoption rates.

This report is essential for packaging material suppliers, food and beverage manufacturers, healthcare companies, personal care brands, and industrial packaging solution providers seeking to capitalize on the burgeoning opportunities in China. Gain a competitive edge by understanding the evolving consumer behavior, regulatory frameworks, and technological disruptions impacting the China plastic packaging film industry.

Key Market Segments Covered:

Leading Companies Analyzed (List Not Exhaustive):

Toray Advanced Film Co Ltd, Berry Global Inc, Kingchuan Packaging, Xiamen Changsu Industrial Co Ltd, Zhejiang Kinlead Innovative Materials Co Ltd, Innovia Films (CCL Industries Inc), Cosmo Films Limited, Sealed Air Corporation, Zhejiang Jiutong Packaging Co Ltd, Logos Pack.

Industry Developments:

- Types: Polypropylene (Polyprop) Film, Polyethylene (Polyethy) Film, Polystyrene Film, Bio-Based Film, PVC Film, EVOH Film, PETG Film, and Other Film Types.

- End Users: Food (Candy & Confectionery, Frozen Foods, Fresh Produce, Dairy Products, Dry Foods, Meat, Poultry, And Seafood, Pet Food, Other Food Products), Healthcare, Personal Care & Home Care, Industrial Packaging, and Other End-use Industry Applications.

- November 2023: Mars China introduced sustainable, recyclable packaging for Snickers, a testament to the food industry's pivot towards eco-friendly flexible packaging solutions and the adoption of mono-material films.

- June 2023: Ascend Performance Materials launched HiDura LUX amorphous nylon packaging films at ProPak China 2023, addressing the increasing demand for advanced films to reduce food wastage by enhancing product protection.

China Plastic Packaging Film Market Dynamics & Structure

The China plastic packaging film market is characterized by its vast scale and increasing complexity, driven by a burgeoning domestic demand and a shift towards higher-value, sustainable solutions. Market concentration varies across different film types, with polyethylene and polypropylene films holding significant market share due to their widespread applications and cost-effectiveness. Technological innovation is a pivotal driver, with companies investing heavily in research and development to create films with enhanced barrier properties, improved recyclability, and reduced environmental impact. Regulatory frameworks, particularly those promoting sustainability and waste reduction, are increasingly influencing product development and market entry strategies. Competitive product substitutes, such as paper-based packaging and alternative film materials, are also gaining traction, forcing plastic film manufacturers to innovate. End-user demographics are evolving, with a growing middle class demanding higher quality and more convenient packaging, especially in the food and beverage sectors. Mergers and acquisitions (M&A) activity plays a crucial role in market consolidation and expansion, with larger players acquiring smaller, specialized companies to broaden their product portfolios and geographical reach.

- Market Concentration: Moderate to High in commodity films, evolving towards fragmentation in specialized and sustainable films.

- Technological Innovation Drivers: Demand for extended shelf life, enhanced product protection, recyclability, and biodegradable alternatives.

- Regulatory Frameworks: Government initiatives promoting circular economy, reduced plastic waste, and sustainable packaging standards.

- Competitive Product Substitutes: Paper-based packaging, compostable films, and other novel materials.

- End-User Demographics: Growing disposable income, urbanization, and increased consumption of packaged goods.

- M&A Trends: Strategic acquisitions to enhance technological capabilities, expand product offerings, and gain market share.

China Plastic Packaging Film Market Growth Trends & Insights

The China plastic packaging film market has witnessed substantial growth over the historical period (2019-2024), fueled by robust economic expansion and evolving consumer lifestyles. The market size, estimated at approximately $35.8 billion in 2025, is projected to expand significantly in the forecast period (2025-2033) with a Compound Annual Growth Rate (CAGR) of 6.8%. This growth is underpinned by increasing adoption rates of advanced packaging solutions across various end-use industries. Technological disruptions are playing a transformative role, with the development of high-performance films that offer superior barrier properties, heat resistance, and printability. For instance, the increasing demand for multi-layer barrier films in the food industry, driven by the need to preserve freshness and extend shelf life, contributes significantly to market expansion. Consumer behavior shifts are also a major catalyst; consumers are increasingly prioritizing convenience, safety, and sustainability in their purchasing decisions, which directly influences the demand for specialized plastic packaging films. The rapid growth of e-commerce further propends the demand for durable and protective packaging films. The penetration of innovative film types, such as bio-based and recyclable mono-material films, is expected to accelerate as environmental consciousness rises. This dynamic interplay of market size evolution, adoption rates, technological advancements, and shifting consumer preferences paints a clear picture of a market poised for continued expansion and innovation.

Dominant Regions, Countries, or Segments in China Plastic Packaging Film Market

The Food and Beverage end-use segment is unequivocally the dominant force driving the China Plastic Packaging Film Market, representing an estimated 45% of the total market revenue in the base year 2025. Within this vast segment, Candy & Confectionery, Frozen Foods, and Dairy Products are particularly significant, owing to China's massive consumer base and its rapidly evolving food processing industry. The country's economic policies, which have consistently supported the growth of its manufacturing and consumer goods sectors, have created a fertile ground for packaging solutions. Infrastructure development, including advanced logistics and cold chain networks, further bolsters the demand for high-quality, protective packaging films essential for preserving food integrity and extending shelf life.

From a regional perspective, East China consistently emerges as the leading region, accounting for over 35% of the market share. This dominance is attributed to its high population density, developed industrial base, and significant concentration of food processing and manufacturing hubs. Cities like Shanghai, Jiangsu, and Zhejiang are key contributors.

Among the film types, Polyethylene (Polyethy) Film remains a cornerstone of the market, driven by its versatility, cost-effectiveness, and extensive use in a wide array of applications, from flexible food packaging to industrial wraps. Its market share is estimated to be around 30% in 2025. However, segments like EVOH (Ethylene Vinyl Alcohol Copolymer) Film and Bio-Based Film are experiencing accelerated growth rates due to increasing demand for advanced barrier properties and sustainable alternatives, respectively. EVOH films are crucial for applications requiring superior oxygen and moisture barrier capabilities, vital for extending the shelf life of sensitive food products. The growing consumer and regulatory pressure for environmentally friendly packaging solutions is propelling the adoption of bio-based films, signaling a significant shift in market preferences.

- Dominant End User Segment: Food (especially Candy & Confectionery, Frozen Foods, Dairy Products).

- Leading Region: East China.

- Dominant Film Type: Polyethylene (Polyethy) Film.

- High Growth Potential Segments: EVOH Film, Bio-Based Film.

China Plastic Packaging Film Market Product Landscape

The China plastic packaging film market is witnessing a surge in product innovation, with manufacturers focusing on developing films that offer superior performance and enhanced sustainability. Key innovations include multi-layer barrier films with improved oxygen, moisture, and aroma retention properties, crucial for extending the shelf life of perishable goods. The development of recyclable mono-material films is a significant trend, addressing the growing environmental concerns and regulatory push towards a circular economy. For instance, advancements in extrusion technology have enabled the creation of sophisticated co-extruded films that combine different polymer layers to achieve specific functionalities, such as enhanced puncture resistance or heat sealability, without compromising recyclability. Applications range from delicate confectionery wraps and retort pouches for ready-to-eat meals to robust films for industrial goods and medical supplies. Performance metrics like tensile strength, tear resistance, and light transmission are continuously being optimized to meet the stringent demands of various end-use industries. Unique selling propositions often revolve around enhanced product protection, reduced material usage, and improved aesthetic appeal.

Key Drivers, Barriers & Challenges in China Plastic Packaging Film Market

Key Drivers:

The China plastic packaging film market is propelled by several formidable drivers. A primary force is the escalating consumer demand for convenience and longer shelf life in food products, directly fueling the need for advanced barrier films. The rapid growth of China's e-commerce sector also necessitates robust and protective packaging solutions. Government initiatives promoting industrial upgrades and sustainable development are encouraging innovation in eco-friendly packaging alternatives. Furthermore, technological advancements in film manufacturing, leading to improved performance characteristics and reduced material consumption, act as significant growth catalysts. The rising disposable incomes and the expanding middle class also contribute to increased consumption of packaged goods, thereby boosting the overall market.

Barriers & Challenges:

Despite its strong growth trajectory, the market faces significant barriers and challenges. Fluctuations in raw material prices, such as crude oil and natural gas, can impact production costs and profit margins for plastic film manufacturers. Stringent environmental regulations, while driving innovation, also pose compliance challenges and can increase operational expenses. The intense competition within the market, from both domestic and international players, can lead to price pressures and necessitate continuous investment in product differentiation. Furthermore, the consumer perception and ongoing global debate surrounding plastic waste and its environmental impact can create market hesitancy for certain applications. Supply chain disruptions, as evidenced by recent global events, can also affect the availability of raw materials and finished goods.

Emerging Opportunities in China Plastic Packaging Film Market

Emerging opportunities in the China plastic packaging film market lie in the burgeoning demand for sustainable and advanced packaging solutions. The increasing focus on reducing food waste presents a significant avenue for high-barrier films that extend product shelf life. The development and adoption of bio-based and compostable packaging films represent a substantial untapped market, driven by both consumer preference and regulatory mandates. Innovations in smart packaging, incorporating features like active components to extend freshness or sensors for tracking product condition, also hold immense potential. Furthermore, the expansion of niche markets, such as specialized medical packaging and high-end cosmetic packaging, offers avenues for growth through premium product offerings. The ongoing "dual carbon" goals in China are also driving opportunities for manufacturers developing and implementing solutions that contribute to carbon reduction throughout the packaging lifecycle.

Growth Accelerators in the China Plastic Packaging Film Market Industry

Several catalysts are accelerating long-term growth within the China plastic packaging film industry. Technological breakthroughs in polymer science are enabling the creation of films with unprecedented performance characteristics, such as enhanced recyclability without compromising functionality. Strategic partnerships between film manufacturers, raw material suppliers, and end-users are fostering collaborative innovation and faster market penetration of new products. The increasing integration of digital technologies, including AI and IoT in manufacturing processes, is driving efficiency and cost reductions. Furthermore, market expansion strategies, including the exploration of less developed regions within China and the burgeoning Southeast Asian markets, are opening up new revenue streams. The growing emphasis on a circular economy is also a significant accelerator, pushing the industry towards closed-loop systems and the increased use of recycled content.

Key Players Shaping the China Plastic Packaging Film Market Market

- Toray Advanced Film Co Ltd

- Berry Global Inc

- Kingchuan Packaging

- Xiamen Changsu Industrial Co Ltd

- Zhejiang Kinlead Innovative Materials Co Ltd

- Innovia Films (CCL Industries Inc)

- Cosmo Films Limited

- Sealed Air Corporation

- Zhejiang Jiuteng Packaging Co Ltd

- Logos Pack

Notable Milestones in China Plastic Packaging Film Market Sector

- November 2023: Mars China unveiled new eco-friendly packaging for Snickers, marking a significant stride toward sustainability by utilizing recyclable films. Transitioning toward sustainable packaging in the food industry, particularly in flexible formats like films and pouches, began by moving away from non-recyclable multilayer barrier films. This shift involved adopting recyclable mono-material films, a move exemplified by Mars China's recent introduction of a dark chocolate cereal Snickers bar.

- June 2023: During ProPak China 2023, Ascend Performance Materials unveiled its HiDura LUX amorphous nylon packaging films for the Asian market. Ascend's Asia commercial director for engineered plastics highlighted the increased need for advanced packaging films in the Chinese market. These films were designed to curtail food wastage by safeguarding products from spoilage and damage, ensuring a higher percentage reaches end consumers.

In-Depth China Plastic Packaging Film Market Market Outlook

The future market outlook for China's plastic packaging film industry is exceptionally promising, driven by a confluence of sustained consumer demand, technological advancements, and a strong governmental push towards sustainability. Growth accelerators, such as the increasing adoption of high-barrier, lightweight, and recyclable films for the food and beverage sector, will continue to underpin market expansion. The ongoing transition towards a circular economy presents a significant opportunity for manufacturers focused on developing and commercializing bio-based and post-consumer recycled (PCR) content films. Strategic collaborations aimed at improving recycling infrastructure and developing innovative end-of-life solutions will be crucial. As China continues its path toward higher living standards and increased consumption of packaged goods, the demand for diverse and advanced plastic packaging films is set to surge, offering substantial strategic opportunities for market players who can adapt to evolving consumer preferences and regulatory landscapes.

China Plastic Packaging Film Market Segmentation

-

1. Type

- 1.1. Polyprop

- 1.2. Polyethy

- 1.3. Polyethy

- 1.4. Polystyrene

- 1.5. Bio-Based

- 1.6. PVC, EVOH, PETG, and Other Film Types

-

2. End User

-

2.1. Food

- 2.1.1. Candy & Confectionery

- 2.1.2. Frozen Foods

- 2.1.3. Fresh Produce

- 2.1.4. Dairy Products

- 2.1.5. Dry Foods

- 2.1.6. Meat, Poultry, And Seafood

- 2.1.7. Pet Food

- 2.1.8. Other Food Products

- 2.2. Healthcare

- 2.3. Personal Care & Home Care

- 2.4. Industrial Packaging

- 2.5. Other End-use Industry Applications

-

2.1. Food

China Plastic Packaging Film Market Segmentation By Geography

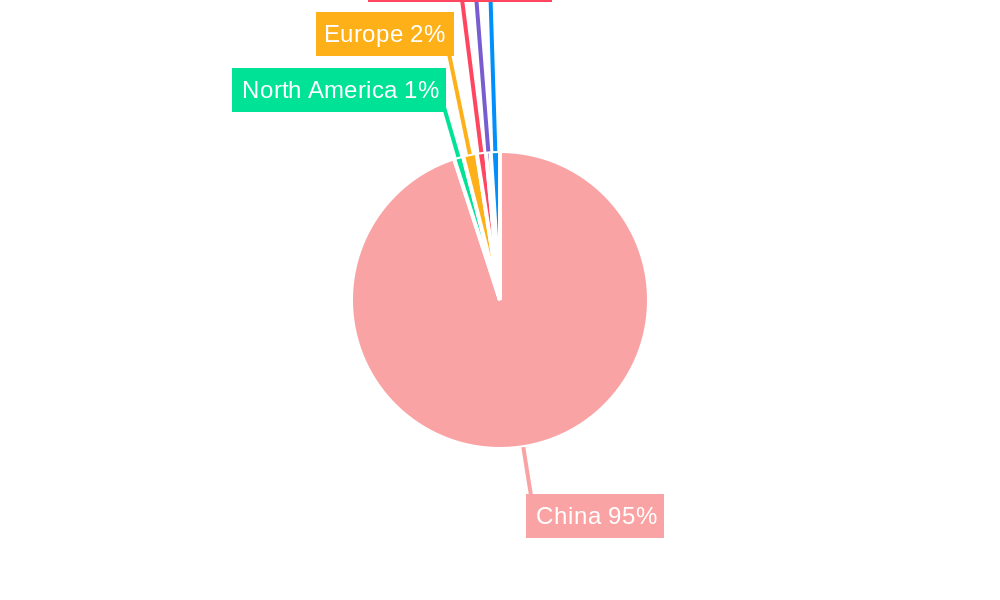

- 1. China

China Plastic Packaging Film Market Regional Market Share

Geographic Coverage of China Plastic Packaging Film Market

China Plastic Packaging Film Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.37% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Polyprop

- 5.1.2. Polyethy

- 5.1.3. Polyethy

- 5.1.4. Polystyrene

- 5.1.5. Bio-Based

- 5.1.6. PVC, EVOH, PETG, and Other Film Types

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Food

- 5.2.1.1. Candy & Confectionery

- 5.2.1.2. Frozen Foods

- 5.2.1.3. Fresh Produce

- 5.2.1.4. Dairy Products

- 5.2.1.5. Dry Foods

- 5.2.1.6. Meat, Poultry, And Seafood

- 5.2.1.7. Pet Food

- 5.2.1.8. Other Food Products

- 5.2.2. Healthcare

- 5.2.3. Personal Care & Home Care

- 5.2.4. Industrial Packaging

- 5.2.5. Other End-use Industry Applications

- 5.2.1. Food

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. China

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. China Plastic Packaging Film Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Polyprop

- 6.1.2. Polyethy

- 6.1.3. Polyethy

- 6.1.4. Polystyrene

- 6.1.5. Bio-Based

- 6.1.6. PVC, EVOH, PETG, and Other Film Types

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Food

- 6.2.1.1. Candy & Confectionery

- 6.2.1.2. Frozen Foods

- 6.2.1.3. Fresh Produce

- 6.2.1.4. Dairy Products

- 6.2.1.5. Dry Foods

- 6.2.1.6. Meat, Poultry, And Seafood

- 6.2.1.7. Pet Food

- 6.2.1.8. Other Food Products

- 6.2.2. Healthcare

- 6.2.3. Personal Care & Home Care

- 6.2.4. Industrial Packaging

- 6.2.5. Other End-use Industry Applications

- 6.2.1. Food

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Toray Advanced Film Co Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Berry Global Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Kingchuan Packaging

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Xiamen Changsu Industrial Co Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Zhejiang Kinlead Innovative Materials Co Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Innovia Films (CCL Industries Inc )

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Cosmo Films Limited

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Sealed Air Corporation

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Zhejiang Jiuteng Packaging Co Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Logos Pack*List Not Exhaustive

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Toray Advanced Film Co Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Plastic Packaging Film Market Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: China Plastic Packaging Film Market Share (%) by Company 2025

List of Tables

- Table 1: China Plastic Packaging Film Market Revenue million Forecast, by Type 2020 & 2033

- Table 2: China Plastic Packaging Film Market Revenue million Forecast, by End User 2020 & 2033

- Table 3: China Plastic Packaging Film Market Revenue million Forecast, by Region 2020 & 2033

- Table 4: China Plastic Packaging Film Market Revenue million Forecast, by Type 2020 & 2033

- Table 5: China Plastic Packaging Film Market Revenue million Forecast, by End User 2020 & 2033

- Table 6: China Plastic Packaging Film Market Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Plastic Packaging Film Market?

The projected CAGR is approximately 5.37%.

2. Which companies are prominent players in the China Plastic Packaging Film Market?

Key companies in the market include Toray Advanced Film Co Ltd, Berry Global Inc, Kingchuan Packaging, Xiamen Changsu Industrial Co Ltd, Zhejiang Kinlead Innovative Materials Co Ltd, Innovia Films (CCL Industries Inc ), Cosmo Films Limited, Sealed Air Corporation, Zhejiang Jiuteng Packaging Co Ltd, Logos Pack*List Not Exhaustive.

3. What are the main segments of the China Plastic Packaging Film Market?

The market segments include Type, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.33 million as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand For Light-Weight and Sustainable Packaging Across Industries; Robust Demand From the Increasing FMCG Sector Aids Growth.

6. What are the notable trends driving market growth?

BOPET Films are Expected to Witness Robust Market Demand.

7. Are there any restraints impacting market growth?

Rising Demand For Light-Weight and Sustainable Packaging Across Industries; Robust Demand From the Increasing FMCG Sector Aids Growth.

8. Can you provide examples of recent developments in the market?

November 2023: Mars China unveiled new eco-friendly packaging for Snickers, marking a significant stride toward sustainability by utilizing recyclable films. Transitioning toward sustainable packaging in the food industry, particularly in flexible formats like films and pouches, began by moving away from non-recyclable multilayer barrier films. This shift involved adopting recyclable mono-material films, a move exemplified by Mars China's recent introduction of a dark chocolate cereal Snickers bar.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Plastic Packaging Film Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Plastic Packaging Film Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Plastic Packaging Film Market?

To stay informed about further developments, trends, and reports in the China Plastic Packaging Film Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence