Key Insights

The China automotive parts aluminum die casting market is poised for significant expansion, driven by robust demand from the burgeoning automotive sector. With a current market size of approximately USD 10.41 billion, the industry is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.26% during the forecast period of 2025-2033. This growth is primarily fueled by the increasing adoption of lightweight materials in vehicles to enhance fuel efficiency and reduce emissions, a critical factor in meeting stringent environmental regulations. Aluminum die casting offers superior strength-to-weight ratios, corrosion resistance, and design flexibility, making it an ideal choice for various automotive components. Key applications such as engine parts, transmission components, and body parts are expected to witness substantial demand. The "Other Application Types" segment is also anticipated to grow as manufacturers explore new uses for aluminum die-cast parts in evolving vehicle architectures, including advanced driver-assistance systems (ADAS) and electric vehicle (EV) components. Emerging trends like the integration of smart manufacturing technologies and the development of more sustainable die casting processes will further shape the market landscape.

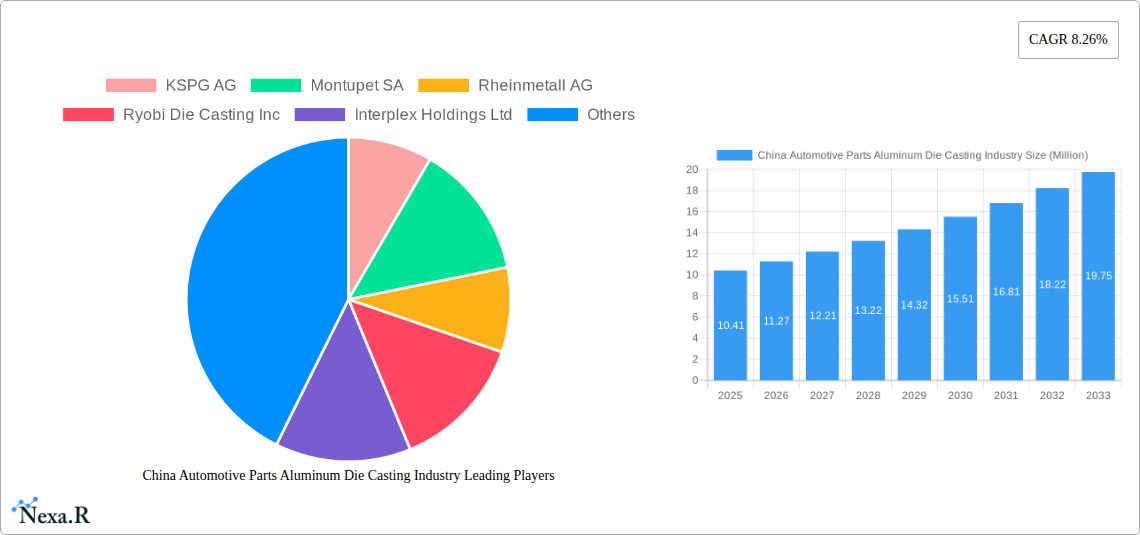

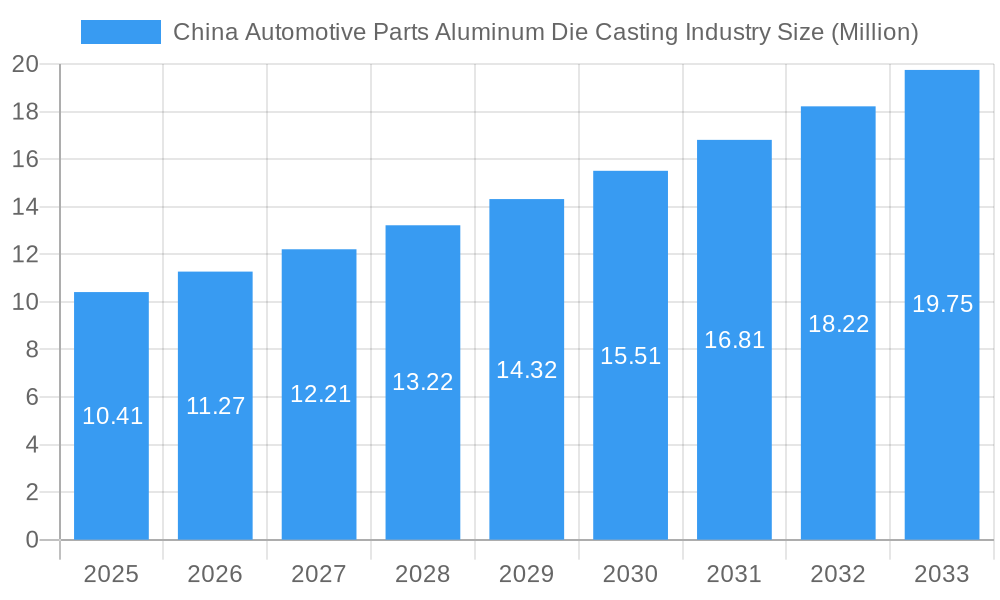

China Automotive Parts Aluminum Die Casting Industry Market Size (In Million)

The market's growth trajectory is supported by a dynamic production landscape, encompassing Pressure Die Casting, Vacuum Die Casting, Squeeze Die Casting, and Semi-solid Die Casting, each offering distinct advantages for specific applications. Pressure die casting remains a dominant method due to its efficiency and cost-effectiveness for high-volume production of complex parts. Vacuum die casting and squeeze die casting are gaining traction for their ability to produce parts with improved mechanical properties and reduced porosity, crucial for high-performance automotive components. Semi-solid die casting is emerging as a promising technology for intricate designs and superior material integrity. Key players like KSPG AG, Montupet SA, Rheinmetall AG, and Ryobi Die Casting Inc. are actively investing in research and development to innovate and expand their product portfolios, catering to the evolving needs of both domestic and international automotive manufacturers. While the market shows immense potential, challenges such as fluctuating raw material prices and the need for advanced technological adoption could pose moderate restraints. Nevertheless, the strategic importance of China as a global automotive hub, coupled with government support for advanced manufacturing, underpins a very positive outlook for the automotive parts aluminum die casting industry in the region.

China Automotive Parts Aluminum Die Casting Industry Company Market Share

China Automotive Parts Aluminum Die Casting Industry Market Report 2024-2033: Unveiling Growth Drivers, Segments, and Key Players

This comprehensive report delivers an in-depth analysis of the China Automotive Parts Aluminum Die Casting industry, a vital sector for the global automotive supply chain. Covering the period from 2019 to 2033, with a base year of 2025, this report provides critical insights into market dynamics, growth trends, dominant segments, technological advancements, and the competitive landscape. We meticulously examine the evolution of aluminum die casting for automotive parts in China, from historical performance to future projections, utilizing high-traffic keywords for maximum SEO visibility and engaging industry professionals. Explore the parent and child market segments with detailed quantitative and qualitative analysis. All values are presented in Million units.

China Automotive Parts Aluminum Die Casting Industry Market Dynamics & Structure

The China automotive parts aluminum die casting market is characterized by a moderately concentrated structure, with a few leading players holding significant market share. Technological innovation is a primary driver, fueled by the increasing demand for lightweight, high-strength aluminum components for electric vehicles (EVs) and improved fuel efficiency in internal combustion engine (ICE) vehicles. The regulatory framework, particularly evolving environmental standards and government support for EV production, plays a crucial role in shaping industry development. Competitive product substitutes, such as magnesium and advanced plastics, present a continuous challenge, necessitating ongoing advancements in aluminum alloy performance and casting techniques. End-user demographics are shifting towards a younger, more tech-savvy consumer base that demands sophisticated automotive features, directly influencing the types of aluminum die-cast parts required. Mergers and acquisitions (M&A) trends are active, with companies seeking to expand their capabilities, gain market access, and consolidate their positions.

- Market Concentration: Dominated by a blend of global and domestic players, with ongoing consolidation through strategic partnerships and acquisitions.

- Technological Innovation Drivers:

- Demand for lightweighting in EVs to enhance range.

- Development of advanced aluminum alloys for superior strength-to-weight ratios.

- Advancements in die casting technologies like vacuum and semi-solid die casting for complex geometries and improved surface finish.

- Regulatory Frameworks: Government policies promoting EVs, emissions reduction targets, and stricter safety standards directly impact the demand for specific aluminum die-cast components.

- Competitive Product Substitutes: Continuous R&D efforts are needed to counter the adoption of magnesium alloys and high-strength plastics in certain applications.

- End-User Demographics: Evolving consumer preferences for sophisticated features, safety, and sustainability are driving demand for precision-engineered aluminum parts.

- M&A Trends: Strategic acquisitions and joint ventures are prevalent to enhance production capacity, secure raw material access, and expand technological expertise. Expected M&A deal volumes in the forecast period are estimated to be in the range of 5-8 significant transactions annually.

China Automotive Parts Aluminum Die Casting Industry Growth Trends & Insights

The China automotive parts aluminum die casting industry is poised for robust growth, driven by the surging electric vehicle (EV) market and the ongoing evolution of conventional automotive manufacturing. The market size is projected to expand significantly from an estimated value of USD XX billion in 2025 to USD YY billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 8.5%. This expansion is underpinned by the increasing adoption rates of advanced aluminum alloys and sophisticated die casting processes, which are crucial for producing lightweight yet durable components essential for modern vehicle performance. Technological disruptions, such as the integration of Industry 4.0 principles in die casting operations, including automation, AI-driven process optimization, and advanced simulation tools, are further enhancing efficiency and product quality. Consumer behavior shifts, particularly the growing preference for eco-friendly transportation and vehicles equipped with advanced safety and performance features, directly translate into higher demand for precision-engineered aluminum die-cast parts like battery enclosures, motor housings, and structural components. The industry is witnessing a paradigm shift from traditional internal combustion engine (ICE) parts to critical EV components, reflecting the broader automotive industry's transformation. Historical data from 2019-2024 indicates a steady growth trajectory, with a particular acceleration observed in the last two years due to the intensified focus on new energy vehicles. Market penetration of aluminum die-cast parts in the EV segment is expected to reach over 75% by 2033, a substantial increase from an estimated 55% in 2025. This growth is not merely incremental; it represents a fundamental reshaping of the automotive supply chain, where lightweighting and material efficiency are paramount. The integration of advanced alloys and innovative casting techniques will be crucial for manufacturers to maintain a competitive edge.

Dominant Regions, Countries, or Segments in China Automotive Parts Aluminum Die Casting Industry

Within the China automotive parts aluminum die casting industry, certain segments and regions exhibit exceptional dominance due to a confluence of economic policies, robust infrastructure, and concentrated automotive manufacturing hubs. From a Production Process Type perspective, Pressure Die Casting remains the undisputed leader, accounting for an estimated 80% of the market share in 2025. This dominance stems from its efficiency, high production rates, and suitability for mass-producing a wide range of automotive components, from engine blocks to intricate structural parts. While Vacuum Die Casting and Squeeze Die Casting are gaining traction for specialized applications requiring higher precision and reduced porosity, their market share remains considerably smaller. Semi-solid Die Casting is an emerging technology with significant potential for complex geometries and improved material properties, but its widespread adoption is still in its nascent stages.

In terms of Application Type, Engine Parts historically held the largest share. However, with the rapid electrification of vehicles, Transmission Components (specifically for EVs, including motor housings and inverter casings) and Body Parts (such as structural components for enhanced safety and lightweighting) are experiencing exponential growth, rapidly closing the gap and, in some areas, surpassing traditional engine part demand. By 2025, it is projected that EV-related transmission components will account for 25% of the total market share, while body parts will command 20%.

Geographically, the Eastern China region, particularly provinces like Jiangsu, Zhejiang, and Shanghai, stands out as the dominant hub. This dominance is driven by:

- Concentration of Automotive Manufacturing: Major automotive OEMs and Tier-1 suppliers have established extensive production facilities in these regions, creating a high demand for local aluminum die-cast parts.

- Developed Industrial Ecosystem: A mature supply chain, including raw material suppliers, equipment manufacturers, and skilled labor, is readily available.

- Government Support and Incentives: Provincial governments actively promote advanced manufacturing, innovation, and the development of the new energy vehicle sector through favorable policies and financial incentives.

- Logistical Advantages: Proximity to major ports and excellent transportation networks facilitate efficient inbound logistics of raw materials and outbound distribution of finished components.

The market share of this region is estimated to be over 45% of the total China automotive parts aluminum die casting market. The growth potential in these dominant regions is further amplified by ongoing investments in advanced manufacturing technologies and the continuous expansion of EV production lines.

China Automotive Parts Aluminum Die Casting Industry Product Landscape

The product landscape of the China automotive parts aluminum die casting industry is dynamic, driven by innovation and the evolving demands of vehicle manufacturers. Key product categories include intricate engine components such as cylinder blocks and heads, complex transmission housings, and increasingly, lightweight body structural parts and battery enclosures for electric vehicles. Advanced aluminum alloys, including high-silicon aluminum and aluminum-magnesium alloys, are being utilized to achieve superior strength-to-weight ratios, enhanced corrosion resistance, and improved thermal management properties. Technologies like low-pressure die casting and vacuum die casting are enabling the production of components with finer detail, improved surface finish, and reduced internal defects, crucial for high-performance applications. Unique selling propositions often lie in the ability to produce larger, more complex single-piece components, reducing assembly time and overall vehicle weight. Technological advancements focus on precision, material efficiency, and the development of specialized alloys tailored for specific automotive functions, such as heat dissipation in EV powertrains or crashworthiness in structural components.

Key Drivers, Barriers & Challenges in China Automotive Parts Aluminum Die Casting Industry

Key Drivers:

- Booming EV Market: The rapid growth of electric vehicle production in China is a primary catalyst, driving demand for lightweight aluminum components like battery enclosures, motor housings, and thermal management parts.

- Lightweighting Initiatives: Global and domestic pressure to improve fuel efficiency and EV range mandates the use of lighter materials, with aluminum die casting being a key solution.

- Technological Advancements: Continuous improvements in die casting processes and alloy development enable the production of more complex, stronger, and lighter parts.

- Government Support for EVs: Favorable policies, subsidies, and targets for new energy vehicle adoption directly stimulate the demand for related components.

- Cost-Effectiveness: Compared to some other lightweighting materials, aluminum die casting offers a compelling balance of performance and cost for mass production.

Barriers & Challenges:

- Raw Material Price Volatility: Fluctuations in aluminum prices can impact manufacturing costs and profitability, posing a significant challenge for cost-sensitive automotive supply chains.

- Intense Competition: The market is highly competitive, with numerous domestic and international players vying for market share, leading to price pressures.

- Skilled Labor Shortage: The increasing complexity of advanced die casting technologies and automation requires a skilled workforce, which can be a bottleneck.

- Environmental Regulations: Stricter environmental regulations regarding emissions and waste management necessitate significant investment in cleaner production technologies.

- Supply Chain Disruptions: Geopolitical events, trade tensions, and logistical challenges can disrupt the supply of raw materials and the distribution of finished goods. The estimated impact of supply chain disruptions on production lead times can be up to 15-20% in critical periods.

Emerging Opportunities in China Automotive Parts Aluminum Die Casting Industry

Emerging opportunities in the China automotive parts aluminum die casting industry are predominantly centered around the burgeoning electric vehicle ecosystem. The demand for integrated battery thermal management systems, intricate e-motor components, and structural parts for new EV platforms presents significant growth avenues. The adoption of advanced casting techniques for large, single-piece structural components, aiming to simplify assembly and enhance vehicle rigidity, is another key opportunity. Furthermore, the growing trend towards autonomous driving necessitates specialized housings and structural elements for sensors and electronic components, which can be met through precise aluminum die casting. Untapped markets within specialized vehicle segments, such as commercial EVs and performance-oriented vehicles, also offer potential for tailored aluminum die-cast solutions. The increasing focus on sustainability is also driving opportunities for companies that can offer recycled aluminum solutions and energy-efficient casting processes.

Growth Accelerators in the China Automotive Parts Aluminum Die Casting Industry Industry

Several critical growth accelerators are propelling the China automotive parts aluminum die casting industry forward. The relentless pace of technological innovation, particularly in areas like high-pressure die casting for large structural parts and the development of advanced aluminum alloys, is a significant catalyst. Strategic partnerships and joint ventures between global OEMs, Tier-1 suppliers, and local Chinese manufacturers are accelerating technology transfer and market penetration. The expansion of production capacities, driven by both established players and new entrants responding to the EV surge, is crucial for meeting escalating demand. Moreover, a concerted push towards smart manufacturing and Industry 4.0 adoption, including AI-powered process optimization and robotic automation, is enhancing efficiency, reducing costs, and improving product quality, thereby acting as a powerful growth accelerator. Market expansion strategies, including penetrating emerging automotive markets within China and exploring export opportunities, are also contributing to sustained growth.

Key Players Shaping the China Automotive Parts Aluminum Die Casting Industry Market

- KSPG AG

- Montupet SA

- Rheinmetall AG

- Ryobi Die Casting Inc

- Interplex Holdings Ltd

- Nemak

- Sandhar Group

- Linamar Corporation

- Shiloh Industries

- Alcoa Inc

- Faist Group

- George Fischer Ltd

- Koch Enterprises

Notable Milestones in China Automotive Parts Aluminum Die Casting Industry Sector

- August 2023: Dongfeng Electronic Technology Co., Ltd. announced its plans to raise CNY 1.4 billion (USD 192.4 million). The fund is scheduled to transform 3-in-1 and 5-in-1 die-casting technology and improve the manufacturing capacity of EV powertrain and core components.

- April 2023: Rheinmetall AG announced a partnership with Xiaomi to produce triangular beams for supporting the suspension strut mountings and associated assembly plates, starting production in 2024. The parts will likely be produced using high-pressure Die Casting and undergo special thermal processing. The Castings business unit is a 50:50 JV of Rheinmetall and HUAYU Automotive Systems (HASCO), a subsidiary of the SAIC Group.

- March 2022: Georg Fischer Casting Solutions, a subsidiary of GF Group, announced that the construction of its new plant in Shenyang, China, is progressing according to the schedule, and production will start by the end of 2022.

In-Depth China Automotive Parts Aluminum Die Casting Industry Market Outlook

The outlook for the China automotive parts aluminum die casting industry remains exceptionally strong, driven by sustained growth in electric vehicle production and the global imperative for vehicle lightweighting. Future market potential is immense, with significant opportunities arising from the demand for integrated lightweight structures, advanced battery components, and sophisticated powertrain parts. Strategic opportunities lie in companies that can leverage advanced manufacturing technologies like AI-driven process control and sustainable casting practices. The industry is poised for continued expansion, with an increasing focus on high-value, precision-engineered components. Investments in R&D for novel aluminum alloys and next-generation die casting techniques will be crucial for maintaining a competitive edge and capitalizing on the evolving automotive landscape.

China Automotive Parts Aluminum Die Casting Industry Segmentation

-

1. Production Process Type

- 1.1. Pressure Die Casting

- 1.2. Vacuum Die Casting

- 1.3. Squeeze Die Casting

- 1.4. Semi-solid Die Casting

-

2. Application Type

- 2.1. Engine Parts

- 2.2. Transmission Components

- 2.3. Body Parts

- 2.4. Other Application Types

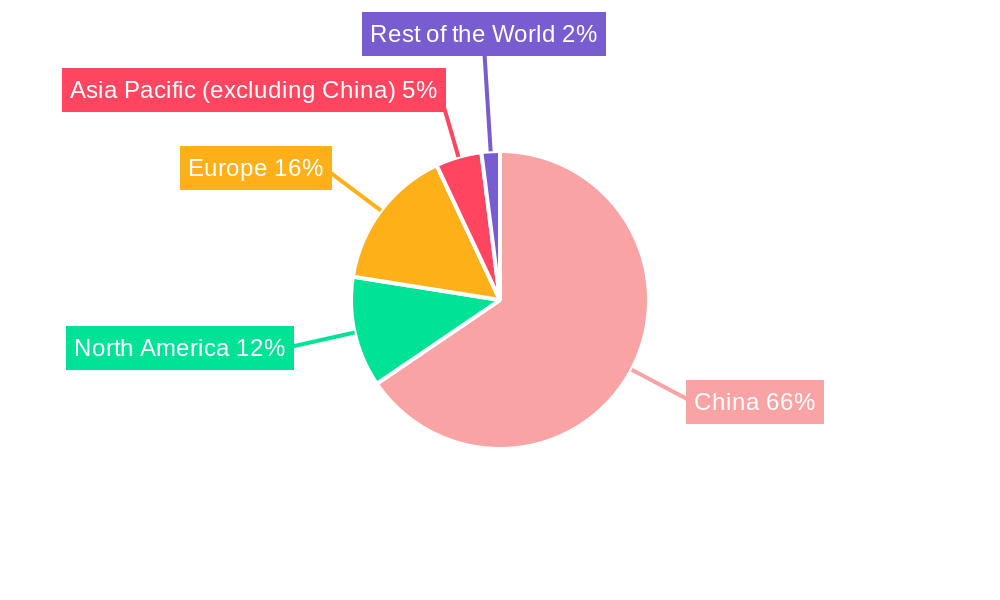

China Automotive Parts Aluminum Die Casting Industry Segmentation By Geography

- 1. China

China Automotive Parts Aluminum Die Casting Industry Regional Market Share

Geographic Coverage of China Automotive Parts Aluminum Die Casting Industry

China Automotive Parts Aluminum Die Casting Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.26% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Production Process Type

- 5.1.1. Pressure Die Casting

- 5.1.2. Vacuum Die Casting

- 5.1.3. Squeeze Die Casting

- 5.1.4. Semi-solid Die Casting

- 5.2. Market Analysis, Insights and Forecast - by Application Type

- 5.2.1. Engine Parts

- 5.2.2. Transmission Components

- 5.2.3. Body Parts

- 5.2.4. Other Application Types

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. China

- 5.1. Market Analysis, Insights and Forecast - by Production Process Type

- 6. China Automotive Parts Aluminum Die Casting Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Production Process Type

- 6.1.1. Pressure Die Casting

- 6.1.2. Vacuum Die Casting

- 6.1.3. Squeeze Die Casting

- 6.1.4. Semi-solid Die Casting

- 6.2. Market Analysis, Insights and Forecast - by Application Type

- 6.2.1. Engine Parts

- 6.2.2. Transmission Components

- 6.2.3. Body Parts

- 6.2.4. Other Application Types

- 6.1. Market Analysis, Insights and Forecast - by Production Process Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 KSPG AG

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Montupet SA

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Rheinmetall AG

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Ryobi Die Casting Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Interplex Holdings Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Nemak

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Sandhar Group*List Not Exhaustive

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Linamar Corporation

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Shiloh Industries

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Alcoa Inc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Faist Group

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 George Fischer Ltd

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Koch Enterprises

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.1 KSPG AG

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Automotive Parts Aluminum Die Casting Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: China Automotive Parts Aluminum Die Casting Industry Share (%) by Company 2025

List of Tables

- Table 1: China Automotive Parts Aluminum Die Casting Industry Revenue Million Forecast, by Production Process Type 2020 & 2033

- Table 2: China Automotive Parts Aluminum Die Casting Industry Revenue Million Forecast, by Application Type 2020 & 2033

- Table 3: China Automotive Parts Aluminum Die Casting Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: China Automotive Parts Aluminum Die Casting Industry Revenue Million Forecast, by Production Process Type 2020 & 2033

- Table 5: China Automotive Parts Aluminum Die Casting Industry Revenue Million Forecast, by Application Type 2020 & 2033

- Table 6: China Automotive Parts Aluminum Die Casting Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Automotive Parts Aluminum Die Casting Industry?

The projected CAGR is approximately 8.26%.

2. Which companies are prominent players in the China Automotive Parts Aluminum Die Casting Industry?

Key companies in the market include KSPG AG, Montupet SA, Rheinmetall AG, Ryobi Die Casting Inc, Interplex Holdings Ltd, Nemak, Sandhar Group*List Not Exhaustive, Linamar Corporation, Shiloh Industries, Alcoa Inc, Faist Group, George Fischer Ltd, Koch Enterprises.

3. What are the main segments of the China Automotive Parts Aluminum Die Casting Industry?

The market segments include Production Process Type, Application Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 10.41 Million as of 2022.

5. What are some drivers contributing to market growth?

Increase in the Use of Lightweight Material in the Automotive Industry to Drives the Market.

6. What are the notable trends driving market growth?

Body Parts Segment is Expected to Register High Growth Rate Over the Forecast Period.

7. Are there any restraints impacting market growth?

Rising Aluminum Prices Hindering the Market Growth -.

8. Can you provide examples of recent developments in the market?

August 2023: Dongfeng Electronic Technology Co., Ltd. announced its plans to raise CNY 1.4 billion (USD 192.4 million). The fund is scheduled to transform 3-in-1 and 5-in-1 die-casting technology and improve the manufacturing capacity of EV powertrain and core components.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Automotive Parts Aluminum Die Casting Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Automotive Parts Aluminum Die Casting Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Automotive Parts Aluminum Die Casting Industry?

To stay informed about further developments, trends, and reports in the China Automotive Parts Aluminum Die Casting Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence