Key Insights

The High Density Packaging (HDP) market is projected for significant expansion, expected to reach $200.005 billion by 2025, with a Compound Annual Growth Rate (CAGR) of 5.7%. This growth is propelled by the increasing demand for miniaturization and superior performance in advanced electronic devices. Key drivers include continuous innovation in consumer electronics, the adoption of sophisticated technologies in aerospace and defense, and the rising reliance on HDP solutions in medical devices. The IT & Telecom and automotive sectors, with their needs for high-speed data processing and integrated electronics, also contribute to market expansion.

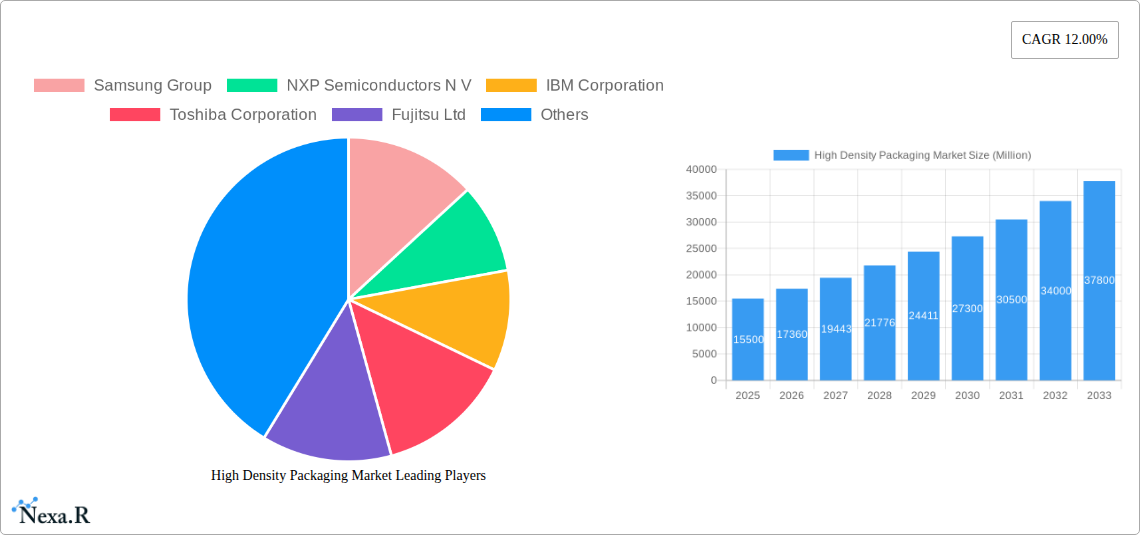

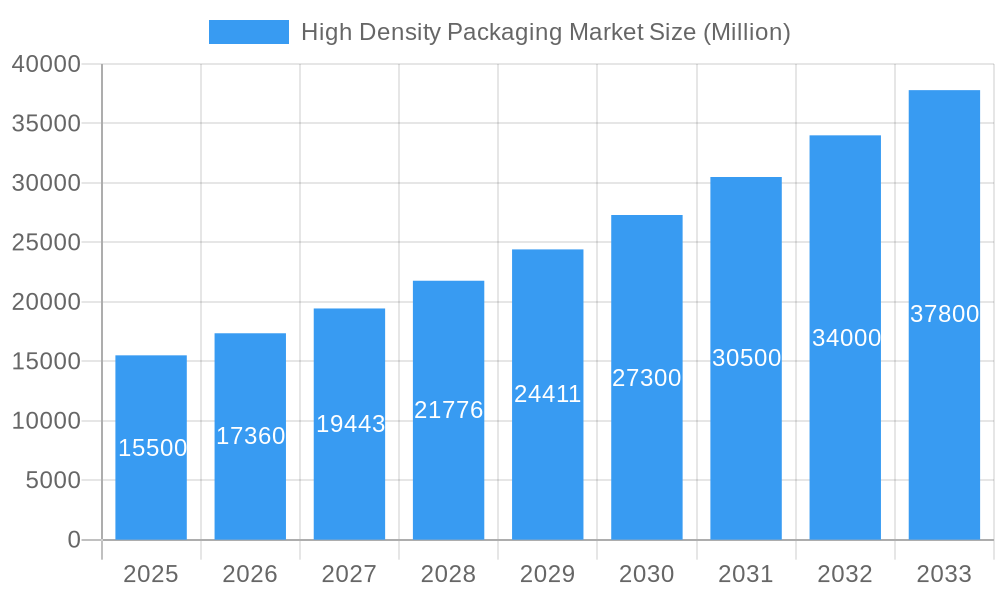

High Density Packaging Market Market Size (In Billion)

The HDP market is segmented by packaging techniques, with advanced solutions like 3D - TSV (Through-Silicon Via) leading due to their vertical stacking capabilities for enhanced performance and miniaturization. Other notable techniques include Multi-Chip Module (MCM), Multi-Chip Package (MCP), and System-in-Package (SIP). Market restraints include the high cost of advanced manufacturing and design complexity. However, ongoing R&D efforts focusing on cost reduction and yield improvement are expected to address these challenges. Major players such as Samsung Group, NXP Semiconductors N.V., and IBM Corporation are actively investing in R&D and strategic partnerships to capitalize on opportunities, particularly in high-growth regions like Asia Pacific.

High Density Packaging Market Company Market Share

High Density Packaging Market: Comprehensive Market Intelligence Report (2019-2033)

This in-depth report provides a detailed analysis of the global High Density Packaging Market, a critical sector driving advancements across consumer electronics, IT & telecom, automotive, medical devices, and aerospace & defense industries. With unprecedented miniaturization and performance demands, the market is experiencing rapid evolution. Our analysis covers key market dynamics, growth trends, regional dominance, product landscape, drivers, challenges, opportunities, and a comprehensive outlook for stakeholders from 2019 to 2033, with a base year of 2025. Values are presented in Million units.

High Density Packaging Market Market Dynamics & Structure

The High Density Packaging Market is characterized by a moderately concentrated structure, with key players like Samsung Group, NXP Semiconductors N.V., IBM Corporation, Toshiba Corporation, and Micron Technology holding significant market influence. Technological innovation is the primary driver, with constant advancements in packaging techniques such as 3D - TSV (Through-Silicon Via) and System-in-Package (SIP) pushing the boundaries of semiconductor integration. Emerging trends like advanced packaging for AI accelerators and high-performance computing further fuel this innovation. Regulatory frameworks, particularly those focused on environmental sustainability and supply chain security, are also shaping market strategies. Competitive product substitutes, while present in simpler packaging solutions, are largely outmatched by the performance and miniaturization benefits offered by high-density packaging for advanced applications. End-user demographics are increasingly sophisticated, demanding smaller, more powerful, and energy-efficient electronic devices, thereby creating sustained demand for high-density packaging solutions. Mergers and acquisitions (M&A) are a recurring theme, as companies seek to consolidate expertise, expand their technology portfolios, and secure market share. For instance, there have been approximately 5-7 significant M&A deals within the semiconductor packaging sector annually over the past few years, often involving smaller, specialized packaging houses being acquired by larger corporations. Innovation barriers include the high capital investment required for advanced manufacturing equipment and the complex R&D processes involved in developing next-generation packaging technologies.

- Market Concentration: Moderately concentrated with key players like Samsung Group, NXP Semiconductors N.V., IBM Corporation, Toshiba Corporation, Micron Technology.

- Technological Innovation Drivers: Advancements in 3D - TSV, SIP, MCM, and MCP technologies; demand for AI, HPC, and IoT devices.

- Regulatory Frameworks: Increasing focus on environmental sustainability (e.g., RoHS, REACH compliance) and supply chain resilience.

- Competitive Product Substitutes: Limited for high-performance, miniaturized applications; traditional packaging for less demanding uses.

- End-User Demographics: Demand for smaller, powerful, energy-efficient, and feature-rich electronic devices.

- M&A Trends: Ongoing consolidation and strategic acquisitions to gain market share and technological capabilities; estimated 5-7 significant deals annually.

- Innovation Barriers: High R&D costs, complex manufacturing processes, need for specialized equipment, skilled workforce requirements.

High Density Packaging Market Growth Trends & Insights

The global High Density Packaging Market is poised for robust expansion, driven by an insatiable demand for more compact, powerful, and energy-efficient electronic devices. The market size is projected to witness a significant upward trajectory, evolving from approximately XX Million units in 2024 to an estimated XX Million units by 2033. This growth is fueled by increasing adoption rates across burgeoning sectors such as the Internet of Things (IoT), artificial intelligence (AI), and 5G telecommunications, all of which necessitate advanced semiconductor packaging solutions for optimal performance and reduced form factors. The CAGR is estimated to be around XX% during the forecast period of 2025–2033.

Technological disruptions are continuously reshaping the market landscape. The progression from Multi-Chip Modules (MCM) and Multi-Chip Packages (MCP) to more sophisticated System-in-Package (SIP) and cutting-edge 3D - TSV technologies is a testament to this rapid evolution. 3D - TSV, in particular, is emerging as a critical enabler for high-performance computing and advanced memory solutions, allowing for vertical integration of multiple dies and significantly enhancing processing power and bandwidth.

Consumer behavior shifts further underscore the market's growth potential. The demand for thinner smartphones, more integrated wearables, advanced automotive electronics, and compact medical devices is pushing manufacturers to adopt high-density packaging solutions. The increasing complexity of integrated circuits (ICs) also necessitates advanced packaging to manage heat dissipation and signal integrity, thereby improving device reliability and lifespan. Market penetration of high-density packaging techniques is expected to deepen as their cost-effectiveness for complex applications becomes more evident, and as the limitations of traditional packaging become more pronounced. Furthermore, the proliferation of edge computing devices, which require significant processing power in localized environments, will be a key driver, demanding smaller and more efficient packaging solutions. The automotive sector's electrification and the increasing integration of advanced driver-assistance systems (ADAS) are also creating substantial demand for high-density packaged components that can withstand harsh operating conditions and offer superior performance. The push for smaller, lighter, and more powerful consumer electronics continues to be a primary engine of growth, with manufacturers consistently seeking innovative packaging to integrate more functionality into ever-shrinking spaces.

Dominant Regions, Countries, or Segments in High Density Packaging Market

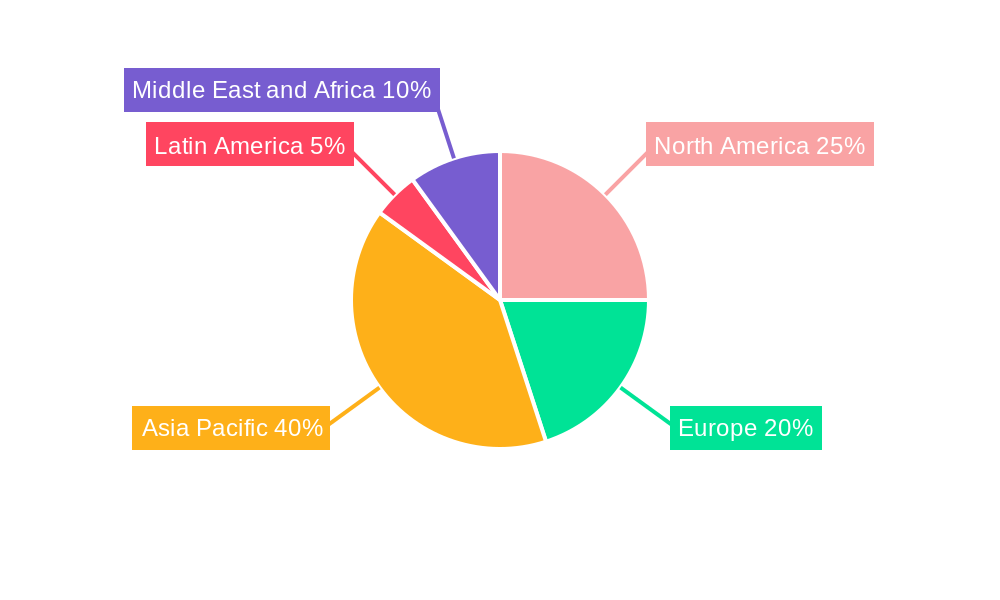

The High Density Packaging Market is experiencing its most significant growth and innovation within the Asia Pacific region, primarily driven by the robust manufacturing capabilities and the immense consumer electronics market in countries like China, South Korea, and Taiwan. This region's dominance is underpinned by several key factors, including a concentrated presence of leading semiconductor foundries and packaging houses, a highly skilled workforce, and substantial government support for the semiconductor industry. The economic policies in these nations actively encourage investment in advanced manufacturing technologies and R&D, fostering an environment conducive to the development and adoption of high-density packaging techniques. Infrastructure development, including advanced logistics and supply chain networks, further supports the efficient production and distribution of these critical components.

Within the Packaging Technique segment, 3D - TSV is emerging as the leading driver of market growth. Its ability to enable vertical stacking of multiple semiconductor dies offers unprecedented levels of integration, performance, and miniaturization. This is particularly crucial for applications in high-performance computing, artificial intelligence, and advanced memory solutions, where increased bandwidth and reduced latency are paramount. The growth potential for 3D - TSV is substantial, with market share expected to expand significantly as manufacturing yields improve and costs decrease.

In terms of Application, Consumer Electronics continues to hold a commanding position in driving demand for high-density packaging. The relentless pursuit of thinner, lighter, and more powerful smartphones, tablets, wearables, and smart home devices necessitates sophisticated packaging solutions that can integrate more functionality into smaller footprints. However, rapid growth is also being observed in the IT & Telecom sector, fueled by the expansion of 5G networks, data centers, and cloud computing infrastructure, all of which require high-density packaged processors and memory components. The Automotive sector is another significant growth area, with the increasing adoption of electric vehicles (EVs), autonomous driving technologies, and advanced infotainment systems demanding high-density, reliable, and high-performance semiconductor packaging solutions that can operate in challenging environments. The Aerospace & Defence and Medical Devices sectors, while smaller in volume, represent high-value markets with stringent performance and reliability requirements, further contributing to the demand for advanced high-density packaging.

- Dominant Region: Asia Pacific (China, South Korea, Taiwan)

- Key Drivers: Concentrated semiconductor manufacturing, strong consumer electronics market, government support, skilled workforce, advanced infrastructure.

- Leading Packaging Technique: 3D - TSV

- Growth Potential: High, driven by HPC, AI, advanced memory, and improving manufacturing efficiencies.

- Dominant Application Segment: Consumer Electronics

- Growth Accelerators: Demand for miniaturization, increased functionality, and performance in smartphones, wearables, and smart devices.

- High-Growth Application Segments: IT & Telecom (5G, data centers), Automotive (EVs, ADAS), Aerospace & Defence, Medical Devices.

High Density Packaging Market Product Landscape

The product landscape of the High Density Packaging Market is characterized by continuous innovation aimed at enhancing semiconductor performance, miniaturization, and power efficiency. Leading product developments include advanced System-in-Package (SIP) solutions that integrate multiple heterogeneous ICs into a single module, offering tailored functionalities for specific applications like AI accelerators and advanced communication chips. 3D - TSV technology continues to be a cornerstone, enabling the vertical stacking of memory and logic dies to achieve unprecedented density and bandwidth for high-performance computing. Multi-Chip Packages (MCP) are evolving to incorporate more complex combinations of memory and logic, catering to the stringent requirements of mobile devices and networking equipment. Performance metrics such as improved signal integrity, reduced power consumption (e.g., XX% lower power consumption in advanced packages compared to traditional ones), enhanced thermal management, and increased interconnect density (e.g., achieving XX interconnects per square millimeter) are key selling propositions for these advanced packaging solutions. Unique selling propositions often lie in the ability to enable smaller device footprints without compromising performance, or to achieve breakthrough levels of processing power and speed.

Key Drivers, Barriers & Challenges in High Density Packaging Market

Key Drivers: The High Density Packaging Market is propelled by several critical factors. The insatiable demand for miniaturization and higher performance across all electronic devices, from smartphones to supercomputers, is a primary driver. The rapid growth of emerging technologies like Artificial Intelligence (AI), the Internet of Things (IoT), 5G, and autonomous driving necessitates advanced packaging solutions to handle increased data processing and connectivity. Furthermore, the pursuit of enhanced power efficiency and improved thermal management in electronic systems directly fuels the adoption of sophisticated packaging techniques. Government initiatives supporting semiconductor manufacturing and R&D in key regions also play a significant role.

Barriers & Challenges: Despite the strong growth prospects, the market faces significant challenges. The extremely high capital expenditure required for advanced packaging manufacturing facilities and R&D is a major barrier to entry for smaller players. The complexity of the manufacturing processes for technologies like 3D - TSV leads to potential yield issues and higher initial production costs. Supply chain disruptions, exacerbated by geopolitical factors and the global shortage of raw materials and components, pose a constant threat to production continuity and cost stability. Stringent regulatory requirements, particularly concerning environmental compliance and material sourcing, add another layer of complexity. Intense competition among established players and emerging technologies also puts pressure on profit margins. The need for a highly skilled workforce trained in advanced semiconductor manufacturing and packaging techniques presents a long-term challenge.

Emerging Opportunities in High Density Packaging Market

Emerging opportunities within the High Density Packaging Market are vast and diverse. The growing demand for advanced packaging solutions in the burgeoning field of advanced driver-assistance systems (ADAS) and autonomous vehicles presents a significant untapped market. The miniaturization and integration requirements for medical devices, particularly in areas like wearable health monitors and implantable electronics, offer another lucrative avenue. The expansion of edge computing, which requires powerful processing capabilities at the network's edge, is creating demand for compact and efficient packaging. Furthermore, the increasing focus on sustainable electronics is creating opportunities for packaging solutions that offer improved energy efficiency and are manufactured with environmentally friendly materials. The development of novel materials and interconnect technologies for next-generation packaging also represents a significant area for innovation and market growth.

Growth Accelerators in the High Density Packaging Market Industry

Several catalysts are accelerating the growth of the High Density Packaging Market. Technological breakthroughs, such as advancements in wafer-level packaging, heterogeneous integration, and advanced interconnect technologies, are continuously expanding the capabilities and applications of high-density packaging. Strategic partnerships and collaborations between semiconductor manufacturers, foundries, and packaging houses are crucial for sharing expertise, reducing R&D costs, and accelerating the commercialization of new technologies. Market expansion strategies, including the penetration into new application areas like advanced sensing and augmented reality, are also driving growth. The ongoing digitalization across industries, leading to an increased reliance on data processing and connectivity, ensures a sustained demand for the high-performance solutions that advanced packaging enables.

Key Players Shaping the High Density Packaging Market Market

- Samsung Group

- NXP Semiconductors N.V.

- IBM Corporation

- Toshiba Corporation

- Fujitsu Ltd

- Micron Technology

- Hitachi Ltd

- Siliconware Precision Industries

- STMicroelectronics

- Amkor Technology

- Mentor - a Siemens Business

Notable Milestones in High Density Packaging Market Sector

- 2019: Increased adoption of 3D-TSV for high-bandwidth memory (HBM) in data center GPUs.

- 2020: Advancements in heterogeneous integration enabling the combination of different chip technologies within a single package.

- 2021: Growing investment in advanced packaging solutions for AI and machine learning accelerators.

- 2022: Innovations in wafer-level packaging (WLP) leading to further miniaturization and cost reductions.

- 2023: Emergence of new materials and manufacturing processes for improved thermal management in high-density packages.

- 2024: Increased focus on supply chain resilience and regionalization of advanced packaging manufacturing.

In-Depth High Density Packaging Market Market Outlook

The outlook for the High Density Packaging Market remains exceptionally positive, driven by the persistent demand for enhanced performance, miniaturization, and power efficiency across a diverse range of industries. Growth accelerators such as ongoing technological breakthroughs in areas like fan-out wafer-level packaging and advanced interconnects, coupled with strategic alliances among key industry players, are expected to propel the market forward. The increasing adoption of high-density packaging in high-growth sectors like automotive (especially EVs and ADAS), 5G infrastructure, and AI-powered edge devices will continue to expand market penetration. The market's future trajectory hinges on continued innovation to address challenges like manufacturing cost, yield optimization, and supply chain stability, presenting significant strategic opportunities for companies capable of delivering cutting-edge, reliable, and cost-effective high-density packaging solutions.

High Density Packaging Market Segmentation

-

1. Packaging Technique

- 1.1. MCM

- 1.2. MCP

- 1.3. SIP

- 1.4. 3D - TSV

-

2. Application

- 2.1. Consumer Electronics

- 2.2. Aerospace & Defence

- 2.3. Medical Devices

- 2.4. IT & Telecom

- 2.5. Automotive

- 2.6. Other Applications

High Density Packaging Market Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

High Density Packaging Market Regional Market Share

Geographic Coverage of High Density Packaging Market

High Density Packaging Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Packaging Technique

- 5.1.1. MCM

- 5.1.2. MCP

- 5.1.3. SIP

- 5.1.4. 3D - TSV

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Consumer Electronics

- 5.2.2. Aerospace & Defence

- 5.2.3. Medical Devices

- 5.2.4. IT & Telecom

- 5.2.5. Automotive

- 5.2.6. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Packaging Technique

- 6. Global High Density Packaging Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Packaging Technique

- 6.1.1. MCM

- 6.1.2. MCP

- 6.1.3. SIP

- 6.1.4. 3D - TSV

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Consumer Electronics

- 6.2.2. Aerospace & Defence

- 6.2.3. Medical Devices

- 6.2.4. IT & Telecom

- 6.2.5. Automotive

- 6.2.6. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Packaging Technique

- 7. North America High Density Packaging Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Packaging Technique

- 7.1.1. MCM

- 7.1.2. MCP

- 7.1.3. SIP

- 7.1.4. 3D - TSV

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Consumer Electronics

- 7.2.2. Aerospace & Defence

- 7.2.3. Medical Devices

- 7.2.4. IT & Telecom

- 7.2.5. Automotive

- 7.2.6. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Packaging Technique

- 8. Europe High Density Packaging Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Packaging Technique

- 8.1.1. MCM

- 8.1.2. MCP

- 8.1.3. SIP

- 8.1.4. 3D - TSV

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Consumer Electronics

- 8.2.2. Aerospace & Defence

- 8.2.3. Medical Devices

- 8.2.4. IT & Telecom

- 8.2.5. Automotive

- 8.2.6. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Packaging Technique

- 9. Asia Pacific High Density Packaging Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Packaging Technique

- 9.1.1. MCM

- 9.1.2. MCP

- 9.1.3. SIP

- 9.1.4. 3D - TSV

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Consumer Electronics

- 9.2.2. Aerospace & Defence

- 9.2.3. Medical Devices

- 9.2.4. IT & Telecom

- 9.2.5. Automotive

- 9.2.6. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Packaging Technique

- 10. Latin America High Density Packaging Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Packaging Technique

- 10.1.1. MCM

- 10.1.2. MCP

- 10.1.3. SIP

- 10.1.4. 3D - TSV

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Consumer Electronics

- 10.2.2. Aerospace & Defence

- 10.2.3. Medical Devices

- 10.2.4. IT & Telecom

- 10.2.5. Automotive

- 10.2.6. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Packaging Technique

- 11. Middle East and Africa High Density Packaging Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Packaging Technique

- 11.1.1. MCM

- 11.1.2. MCP

- 11.1.3. SIP

- 11.1.4. 3D - TSV

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Consumer Electronics

- 11.2.2. Aerospace & Defence

- 11.2.3. Medical Devices

- 11.2.4. IT & Telecom

- 11.2.5. Automotive

- 11.2.6. Other Applications

- 11.1. Market Analysis, Insights and Forecast - by Packaging Technique

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Samsung Group

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 NXP Semiconductors N V

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 IBM Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Toshiba Corporation

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Fujitsu Ltd

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Micron Technology

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Hitachi Ltd

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Siliconware Precision Industries

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 STMicroelectronics

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Amkor Technology

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Mentor - a Siemens Business*List Not Exhaustive

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 Samsung Group

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global High Density Packaging Market Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America High Density Packaging Market Revenue (billion), by Packaging Technique 2025 & 2033

- Figure 3: North America High Density Packaging Market Revenue Share (%), by Packaging Technique 2025 & 2033

- Figure 4: North America High Density Packaging Market Revenue (billion), by Application 2025 & 2033

- Figure 5: North America High Density Packaging Market Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America High Density Packaging Market Revenue (billion), by Country 2025 & 2033

- Figure 7: North America High Density Packaging Market Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe High Density Packaging Market Revenue (billion), by Packaging Technique 2025 & 2033

- Figure 9: Europe High Density Packaging Market Revenue Share (%), by Packaging Technique 2025 & 2033

- Figure 10: Europe High Density Packaging Market Revenue (billion), by Application 2025 & 2033

- Figure 11: Europe High Density Packaging Market Revenue Share (%), by Application 2025 & 2033

- Figure 12: Europe High Density Packaging Market Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe High Density Packaging Market Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific High Density Packaging Market Revenue (billion), by Packaging Technique 2025 & 2033

- Figure 15: Asia Pacific High Density Packaging Market Revenue Share (%), by Packaging Technique 2025 & 2033

- Figure 16: Asia Pacific High Density Packaging Market Revenue (billion), by Application 2025 & 2033

- Figure 17: Asia Pacific High Density Packaging Market Revenue Share (%), by Application 2025 & 2033

- Figure 18: Asia Pacific High Density Packaging Market Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific High Density Packaging Market Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America High Density Packaging Market Revenue (billion), by Packaging Technique 2025 & 2033

- Figure 21: Latin America High Density Packaging Market Revenue Share (%), by Packaging Technique 2025 & 2033

- Figure 22: Latin America High Density Packaging Market Revenue (billion), by Application 2025 & 2033

- Figure 23: Latin America High Density Packaging Market Revenue Share (%), by Application 2025 & 2033

- Figure 24: Latin America High Density Packaging Market Revenue (billion), by Country 2025 & 2033

- Figure 25: Latin America High Density Packaging Market Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa High Density Packaging Market Revenue (billion), by Packaging Technique 2025 & 2033

- Figure 27: Middle East and Africa High Density Packaging Market Revenue Share (%), by Packaging Technique 2025 & 2033

- Figure 28: Middle East and Africa High Density Packaging Market Revenue (billion), by Application 2025 & 2033

- Figure 29: Middle East and Africa High Density Packaging Market Revenue Share (%), by Application 2025 & 2033

- Figure 30: Middle East and Africa High Density Packaging Market Revenue (billion), by Country 2025 & 2033

- Figure 31: Middle East and Africa High Density Packaging Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global High Density Packaging Market Revenue billion Forecast, by Packaging Technique 2020 & 2033

- Table 2: Global High Density Packaging Market Revenue billion Forecast, by Application 2020 & 2033

- Table 3: Global High Density Packaging Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global High Density Packaging Market Revenue billion Forecast, by Packaging Technique 2020 & 2033

- Table 5: Global High Density Packaging Market Revenue billion Forecast, by Application 2020 & 2033

- Table 6: Global High Density Packaging Market Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global High Density Packaging Market Revenue billion Forecast, by Packaging Technique 2020 & 2033

- Table 8: Global High Density Packaging Market Revenue billion Forecast, by Application 2020 & 2033

- Table 9: Global High Density Packaging Market Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Global High Density Packaging Market Revenue billion Forecast, by Packaging Technique 2020 & 2033

- Table 11: Global High Density Packaging Market Revenue billion Forecast, by Application 2020 & 2033

- Table 12: Global High Density Packaging Market Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global High Density Packaging Market Revenue billion Forecast, by Packaging Technique 2020 & 2033

- Table 14: Global High Density Packaging Market Revenue billion Forecast, by Application 2020 & 2033

- Table 15: Global High Density Packaging Market Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global High Density Packaging Market Revenue billion Forecast, by Packaging Technique 2020 & 2033

- Table 17: Global High Density Packaging Market Revenue billion Forecast, by Application 2020 & 2033

- Table 18: Global High Density Packaging Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the High Density Packaging Market?

The projected CAGR is approximately 5.7%.

2. Which companies are prominent players in the High Density Packaging Market?

Key companies in the market include Samsung Group, NXP Semiconductors N V, IBM Corporation, Toshiba Corporation, Fujitsu Ltd, Micron Technology, Hitachi Ltd, Siliconware Precision Industries, STMicroelectronics, Amkor Technology, Mentor - a Siemens Business*List Not Exhaustive.

3. What are the main segments of the High Density Packaging Market?

The market segments include Packaging Technique, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 200.005 billion as of 2022.

5. What are some drivers contributing to market growth?

; Growing Advancements in Consumer Electronic Products; Favourable Government Policies and Regulations in Developing Countries.

6. What are the notable trends driving market growth?

High Application in Consumer Electronics Segment to Augment the Market Growth.

7. Are there any restraints impacting market growth?

; High Initial Investment and Increasing Complexity of IC Designs.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "High Density Packaging Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the High Density Packaging Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the High Density Packaging Market?

To stay informed about further developments, trends, and reports in the High Density Packaging Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence