Key Insights

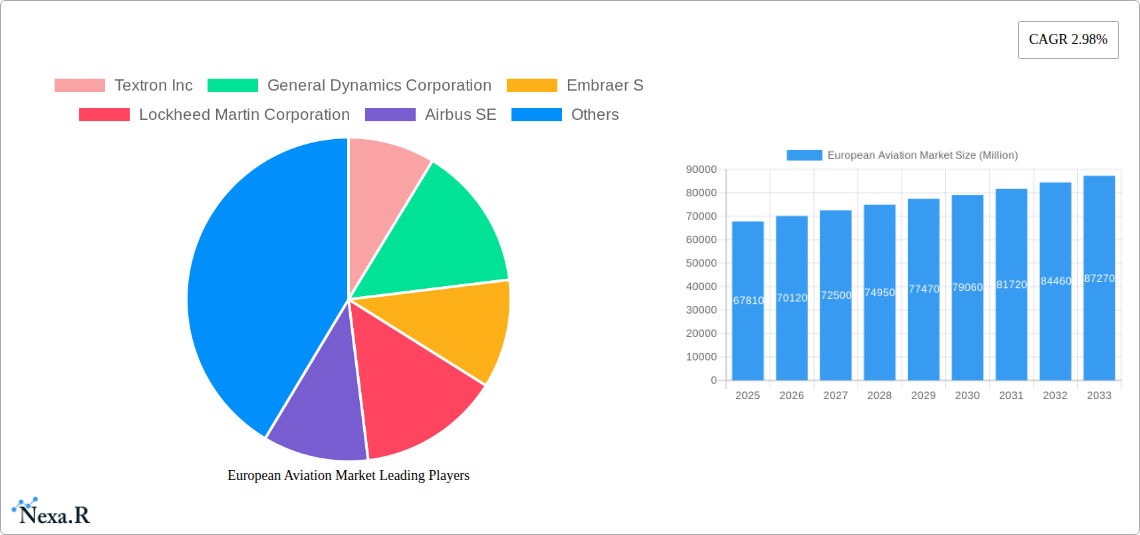

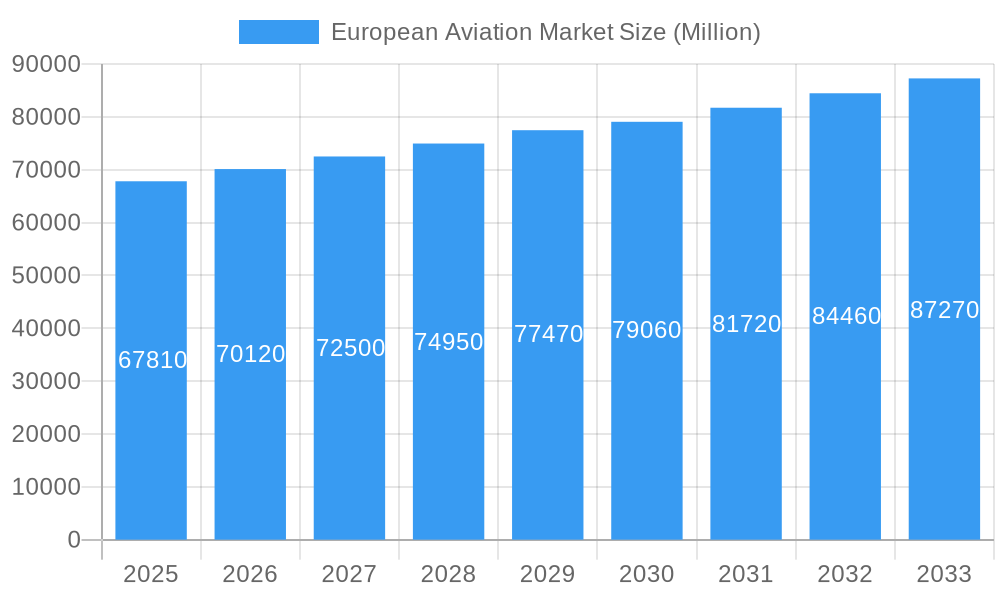

The European aviation market, valued at €67.81 billion in 2025, is projected to experience steady growth, driven by increasing passenger traffic, robust tourism, and the expansion of air cargo operations across the region. The 2.98% CAGR (Compound Annual Growth Rate) indicates a consistent, albeit moderate, expansion over the forecast period (2025-2033). Key segments contributing to this growth include commercial aviation, fueled by the increasing demand for air travel within Europe and beyond, and the general aviation sector, encompassing private and business jets, which benefits from economic growth and a rising high-net-worth individual population. While military aviation remains a significant contributor, its growth is expected to be more moderate compared to the commercial and general aviation segments. The market is influenced by several factors. Economic fluctuations and potential fuel price volatility present challenges. Government regulations and environmental concerns, such as the push for sustainable aviation fuels (SAFs) and quieter aircraft, will shape technological advancements and operational strategies in the coming years. Germany, France, the United Kingdom, and Italy are expected to be the major contributors to the European market, driven by their established aviation infrastructure and strong economies. Competition among established players like Airbus, Boeing, and Embraer, alongside smaller regional aircraft manufacturers, will intensify, driving innovation and potentially leading to consolidation within the industry.

European Aviation Market Market Size (In Billion)

The growth trajectory for the European aviation market is intricately linked to broader macroeconomic conditions. Factors such as post-pandemic recovery, ongoing investments in airport infrastructure, and the adoption of advanced technologies like AI and IoT in flight operations will significantly influence the market's performance. The increasing focus on sustainability will necessitate investments in new technologies and operational efficiencies to reduce carbon emissions. Furthermore, geopolitical stability and potential regulatory changes across the European Union and individual member states will impact market expansion. The ongoing competition between manufacturers and the emergence of new business models, such as air taxi services and drone-based delivery systems, will continue to reshape the landscape of the European aviation industry. The market's resilience and growth potential will hinge on the effective management of these interconnected factors.

European Aviation Market Company Market Share

European Aviation Market: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the European aviation market, encompassing market dynamics, growth trends, key players, and future outlook. The study period covers 2019-2033, with a base year of 2025 and a forecast period of 2025-2033. The report segments the market by aircraft type (Commercial Aviation, Freighter Aircraft, Military Aviation, Non-combat Aircraft, General Aviation), providing granular insights into each segment's performance and future potential. This report is invaluable for industry professionals, investors, and anyone seeking to understand the intricacies of this dynamic market. The market size is predicted to reach xx Million by 2033.

European Aviation Market Dynamics & Structure

The European aviation market exhibits a moderately concentrated structure, with a few dominant players like Airbus SE and Boeing Company holding significant market share. However, smaller players like Embraer S.A. and Dassault Aviation SA also contribute substantially, especially within niche segments. Technological innovation, driven by factors such as increasing fuel efficiency demands and sustainability concerns, plays a crucial role. Stringent regulatory frameworks imposed by the European Union Aviation Safety Agency (EASA) significantly shape market dynamics. Competitive pressures are intense, with manufacturers constantly seeking to improve aircraft performance, reduce operational costs, and offer innovative features. The rise of sustainable aviation fuels (SAFs) and electric/hybrid-electric propulsion systems presents both opportunities and challenges. M&A activity within the European aviation sector remains relatively active, although deal volumes fluctuated in the recent past.

- Market Concentration: Moderately concentrated, with a few major players dominating but significant contributions from smaller companies. Airbus and Boeing combined hold approximately xx% of the market.

- Technological Innovation: Driven by fuel efficiency, sustainability, and advanced avionics. Barriers include high R&D costs and regulatory approvals.

- Regulatory Frameworks: Stringent EASA regulations significantly influence design, certification, and operational aspects.

- Competitive Product Substitutes: Limited direct substitutes exist, but pressure exists from alternative transportation modes (high-speed rail).

- End-User Demographics: Primarily airlines, military branches, and general aviation operators. Market segments exhibit distinct demands and preferences.

- M&A Trends: Fluctuating activity, driven by consolidation efforts and the acquisition of specialized technologies. Approximate deal volume in the period 2019-2024 was xx Million.

European Aviation Market Growth Trends & Insights

The European aviation market experienced significant growth in the historical period (2019-2024), albeit with fluctuations due to the COVID-19 pandemic. Post-pandemic recovery is underway, with a projected compound annual growth rate (CAGR) of xx% from 2025 to 2033. Market size in 2025 is estimated at xx Million. The market is witnessing significant technological disruptions, such as the adoption of advanced materials, improved engine technologies, and the integration of digital technologies. These factors are improving fuel efficiency, reducing emissions, and enhancing operational capabilities. Consumer behavior is shifting towards increased preference for environmentally friendly travel options and a rising demand for enhanced passenger experience, which is directly influencing aircraft design and features. The adoption rate of new technologies is gradually increasing, while market penetration for sustainable aviation fuel is still nascent.

Dominant Regions, Countries, or Segments in European Aviation Market

The Commercial Aviation segment dominates the European aviation market, accounting for approximately xx% of the total market value in 2025. Germany, France, and the UK are leading countries, driven by strong domestic airline industries, significant military spending, and established aerospace manufacturing bases.

Key Drivers for Commercial Aviation:

- Strong air passenger traffic growth (pre-pandemic trends indicate a xx% increase).

- Significant investments in airport infrastructure.

- Government support for airline operations.

- Growing demand for fuel-efficient aircraft.

Dominance Factors:

- High aircraft order backlog from major airlines in these regions.

- Robust aerospace manufacturing capabilities.

- Strong economic growth in these regions supporting demand.

- Strategic geographical location facilitating intercontinental travel.

The Military Aviation segment shows significant growth prospects, spurred by defense modernization programs and geopolitical factors. General Aviation remains a smaller but resilient segment.

European Aviation Market Product Landscape

The European aviation market showcases a diverse product landscape, including narrow-body and wide-body commercial aircraft, various military aircraft, and general aviation aircraft. Recent innovations focus on enhanced fuel efficiency, reduced emissions, advanced avionics, and improved passenger comfort. Many manufacturers are integrating digital technologies to optimize flight operations, enhance maintenance efficiency, and improve passenger experience. Unique selling propositions often include enhanced safety features, customized designs, and advanced technological integration. The integration of sustainable aviation fuel and electric propulsion systems represents a major frontier in product innovation.

Key Drivers, Barriers & Challenges in European Aviation Market

Key Drivers:

- Growing air passenger traffic (pre-pandemic levels were xx Million per year).

- Investments in airport infrastructure improvements.

- Technological advancements (fuel efficiency and automation).

- Government support and policies promoting growth (e.g., tax incentives).

Key Barriers & Challenges:

- High initial investment costs associated with aircraft acquisition and operation.

- Stringent safety regulations and certification processes.

- Volatility in fuel prices.

- Supply chain disruptions affecting aircraft manufacturing and maintenance. The impact of these disruptions in 2022 led to approximately xx Million in lost revenue across the industry.

- Intense competition among manufacturers.

Emerging Opportunities in European Aviation Market

The burgeoning market for sustainable aviation fuels (SAFs) and the development of electric/hybrid-electric propulsion systems present significant opportunities. The growing demand for regional aircraft and the increasing focus on air cargo transportation (driven by e-commerce growth) also offer considerable prospects. Untapped market potential exists in underserved regions and in emerging technologies such as autonomous flight systems. Furthermore, opportunities exist in the provision of comprehensive aviation maintenance, repair, and overhaul (MRO) services.

Growth Accelerators in the European Aviation Market Industry

Technological breakthroughs in engine technology, materials science, and avionics are driving long-term growth. Strategic partnerships between manufacturers, airlines, and technology providers are fostering innovation and market expansion. The expansion of air traffic management systems and investments in modernized airport infrastructure are also crucial factors. The increasing adoption of data analytics and digital transformation initiatives are enhancing operational efficiency and optimizing resource allocation, further accelerating growth.

Key Players Shaping the European Aviation Market Market

Notable Milestones in European Aviation Market Sector

- October 2023: The UK announces trials for 16 Protector surveillance aircraft, expected to enter service in late 2024. This signifies advancements in unmanned aerial vehicle (UAV) technology and their integration into defense operations.

- October 2022: Jet2 orders 35 A320neo aircraft (USD 3.9 billion), with an option for 36 more (USD 8 billion total). This reflects the continued strong demand for fuel-efficient aircraft in the commercial sector.

- July 2022: The US approves the sale of 35 F-35A aircraft to Germany (USD 8.4 billion). This highlights significant investment in military aviation modernization and the geopolitical implications of such deals.

In-Depth European Aviation Market Market Outlook

The future of the European aviation market is promising, fueled by strong growth drivers and emerging opportunities. Sustainable aviation technologies, advanced aircraft designs, and increasing air travel demand will propel market expansion. Strategic partnerships and technological breakthroughs will further accelerate growth, particularly within the segments of sustainable aviation fuels and electric/hybrid-electric aircraft. However, managing challenges like supply chain disruptions and regulatory complexities will be crucial for realizing the market's full potential. The market is poised for substantial growth, with projections indicating a significant increase in market value over the forecast period.

European Aviation Market Segmentation

-

1. Type

-

1.1. Commercial Aviation

- 1.1.1. Passenger Aircraft

- 1.1.2. Freighter Aircraft

-

1.2. Military Aviation

- 1.2.1. Combat Aircraft

- 1.2.2. Non-combat Aircraft

-

1.3. General Aviation

- 1.3.1. Helicopters

- 1.3.2. Piston Fixed-wing Aircraft

- 1.3.3. Turboprop Aircraft

- 1.3.4. Business Jet

-

1.1. Commercial Aviation

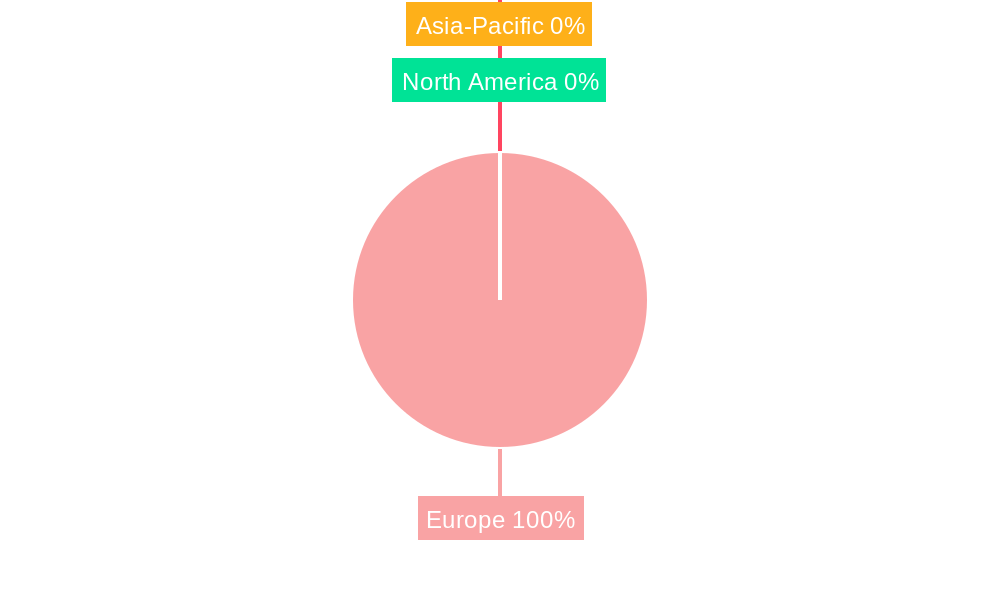

European Aviation Market Segmentation By Geography

- 1. United Kingdom

- 2. Germany

- 3. France

- 4. Italy

- 5. Spain

- 6. Russia

- 7. Rest of Europe

European Aviation Market Regional Market Share

Geographic Coverage of European Aviation Market

European Aviation Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.98% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 3.4.1. Military Segment to Showcase Remarkable Growth During the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. European Aviation Market Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Commercial Aviation

- 5.1.1.1. Passenger Aircraft

- 5.1.1.2. Freighter Aircraft

- 5.1.2. Military Aviation

- 5.1.2.1. Combat Aircraft

- 5.1.2.2. Non-combat Aircraft

- 5.1.3. General Aviation

- 5.1.3.1. Helicopters

- 5.1.3.2. Piston Fixed-wing Aircraft

- 5.1.3.3. Turboprop Aircraft

- 5.1.3.4. Business Jet

- 5.1.1. Commercial Aviation

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. United Kingdom

- 5.2.2. Germany

- 5.2.3. France

- 5.2.4. Italy

- 5.2.5. Spain

- 5.2.6. Russia

- 5.2.7. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. United Kingdom European Aviation Market Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Commercial Aviation

- 6.1.1.1. Passenger Aircraft

- 6.1.1.2. Freighter Aircraft

- 6.1.2. Military Aviation

- 6.1.2.1. Combat Aircraft

- 6.1.2.2. Non-combat Aircraft

- 6.1.3. General Aviation

- 6.1.3.1. Helicopters

- 6.1.3.2. Piston Fixed-wing Aircraft

- 6.1.3.3. Turboprop Aircraft

- 6.1.3.4. Business Jet

- 6.1.1. Commercial Aviation

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Germany European Aviation Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Commercial Aviation

- 7.1.1.1. Passenger Aircraft

- 7.1.1.2. Freighter Aircraft

- 7.1.2. Military Aviation

- 7.1.2.1. Combat Aircraft

- 7.1.2.2. Non-combat Aircraft

- 7.1.3. General Aviation

- 7.1.3.1. Helicopters

- 7.1.3.2. Piston Fixed-wing Aircraft

- 7.1.3.3. Turboprop Aircraft

- 7.1.3.4. Business Jet

- 7.1.1. Commercial Aviation

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. France European Aviation Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Commercial Aviation

- 8.1.1.1. Passenger Aircraft

- 8.1.1.2. Freighter Aircraft

- 8.1.2. Military Aviation

- 8.1.2.1. Combat Aircraft

- 8.1.2.2. Non-combat Aircraft

- 8.1.3. General Aviation

- 8.1.3.1. Helicopters

- 8.1.3.2. Piston Fixed-wing Aircraft

- 8.1.3.3. Turboprop Aircraft

- 8.1.3.4. Business Jet

- 8.1.1. Commercial Aviation

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Italy European Aviation Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Commercial Aviation

- 9.1.1.1. Passenger Aircraft

- 9.1.1.2. Freighter Aircraft

- 9.1.2. Military Aviation

- 9.1.2.1. Combat Aircraft

- 9.1.2.2. Non-combat Aircraft

- 9.1.3. General Aviation

- 9.1.3.1. Helicopters

- 9.1.3.2. Piston Fixed-wing Aircraft

- 9.1.3.3. Turboprop Aircraft

- 9.1.3.4. Business Jet

- 9.1.1. Commercial Aviation

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Spain European Aviation Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Commercial Aviation

- 10.1.1.1. Passenger Aircraft

- 10.1.1.2. Freighter Aircraft

- 10.1.2. Military Aviation

- 10.1.2.1. Combat Aircraft

- 10.1.2.2. Non-combat Aircraft

- 10.1.3. General Aviation

- 10.1.3.1. Helicopters

- 10.1.3.2. Piston Fixed-wing Aircraft

- 10.1.3.3. Turboprop Aircraft

- 10.1.3.4. Business Jet

- 10.1.1. Commercial Aviation

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Russia European Aviation Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Commercial Aviation

- 11.1.1.1. Passenger Aircraft

- 11.1.1.2. Freighter Aircraft

- 11.1.2. Military Aviation

- 11.1.2.1. Combat Aircraft

- 11.1.2.2. Non-combat Aircraft

- 11.1.3. General Aviation

- 11.1.3.1. Helicopters

- 11.1.3.2. Piston Fixed-wing Aircraft

- 11.1.3.3. Turboprop Aircraft

- 11.1.3.4. Business Jet

- 11.1.1. Commercial Aviation

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Rest of Europe European Aviation Market Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Type

- 12.1.1. Commercial Aviation

- 12.1.1.1. Passenger Aircraft

- 12.1.1.2. Freighter Aircraft

- 12.1.2. Military Aviation

- 12.1.2.1. Combat Aircraft

- 12.1.2.2. Non-combat Aircraft

- 12.1.3. General Aviation

- 12.1.3.1. Helicopters

- 12.1.3.2. Piston Fixed-wing Aircraft

- 12.1.3.3. Turboprop Aircraft

- 12.1.3.4. Business Jet

- 12.1.1. Commercial Aviation

- 12.1. Market Analysis, Insights and Forecast - by Type

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2025

- 13.2. Company Profiles

- 13.2.1 Textron Inc

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 General Dynamics Corporation

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Embraer S

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Lockheed Martin Corporation

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Airbus SE

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Dassult Aviation SA

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Pilatus Aircraft Ltd

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 Daher

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Leonardo S p A

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 Bombardier Inc

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.11 Saab AB

- 13.2.11.1. Overview

- 13.2.11.2. Products

- 13.2.11.3. SWOT Analysis

- 13.2.11.4. Recent Developments

- 13.2.11.5. Financials (Based on Availability)

- 13.2.12 The Boeing Company

- 13.2.12.1. Overview

- 13.2.12.2. Products

- 13.2.12.3. SWOT Analysis

- 13.2.12.4. Recent Developments

- 13.2.12.5. Financials (Based on Availability)

- 13.2.1 Textron Inc

List of Figures

- Figure 1: European Aviation Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: European Aviation Market Share (%) by Company 2025

List of Tables

- Table 1: European Aviation Market Revenue Million Forecast, by Type 2020 & 2033

- Table 2: European Aviation Market Revenue Million Forecast, by Region 2020 & 2033

- Table 3: European Aviation Market Revenue Million Forecast, by Type 2020 & 2033

- Table 4: European Aviation Market Revenue Million Forecast, by Country 2020 & 2033

- Table 5: European Aviation Market Revenue Million Forecast, by Type 2020 & 2033

- Table 6: European Aviation Market Revenue Million Forecast, by Country 2020 & 2033

- Table 7: European Aviation Market Revenue Million Forecast, by Type 2020 & 2033

- Table 8: European Aviation Market Revenue Million Forecast, by Country 2020 & 2033

- Table 9: European Aviation Market Revenue Million Forecast, by Type 2020 & 2033

- Table 10: European Aviation Market Revenue Million Forecast, by Country 2020 & 2033

- Table 11: European Aviation Market Revenue Million Forecast, by Type 2020 & 2033

- Table 12: European Aviation Market Revenue Million Forecast, by Country 2020 & 2033

- Table 13: European Aviation Market Revenue Million Forecast, by Type 2020 & 2033

- Table 14: European Aviation Market Revenue Million Forecast, by Country 2020 & 2033

- Table 15: European Aviation Market Revenue Million Forecast, by Type 2020 & 2033

- Table 16: European Aviation Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the European Aviation Market?

The projected CAGR is approximately 2.98%.

2. Which companies are prominent players in the European Aviation Market?

Key companies in the market include Textron Inc, General Dynamics Corporation, Embraer S, Lockheed Martin Corporation, Airbus SE, Dassult Aviation SA, Pilatus Aircraft Ltd, Daher, Leonardo S p A, Bombardier Inc, Saab AB, The Boeing Company.

3. What are the main segments of the European Aviation Market?

The market segments include Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 67.81 Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Military Segment to Showcase Remarkable Growth During the Forecast Period.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

October 2023: The UK announced that the country will likely start trials of new 16 Protector aircraft surveillance aircraft. Aircraft is expected to undergo test flights until entering service in late 2024. A new uncrewed RAF aircraft is capable of global surveillance operations.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "European Aviation Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the European Aviation Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the European Aviation Market?

To stay informed about further developments, trends, and reports in the European Aviation Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence