Key Insights

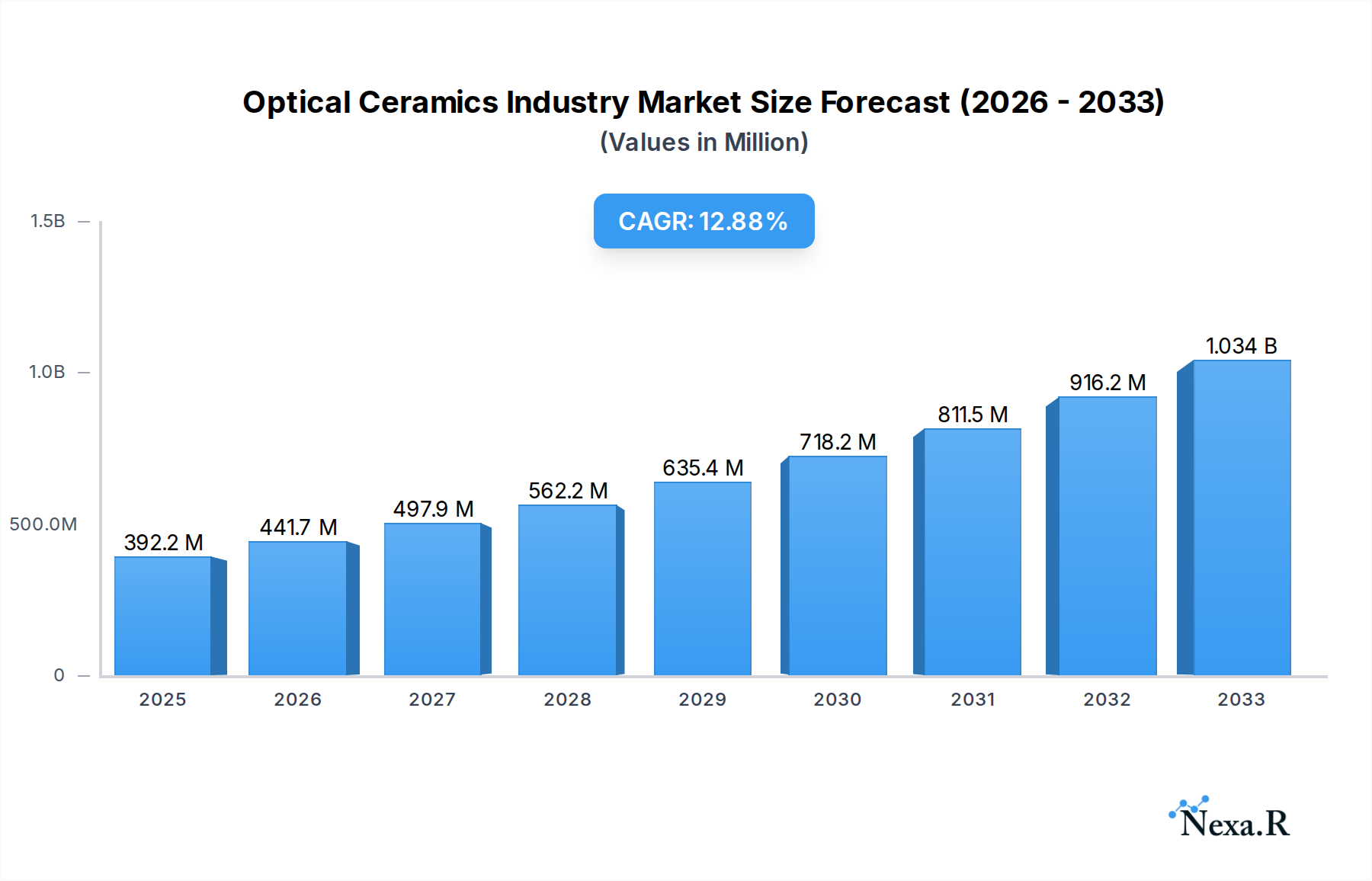

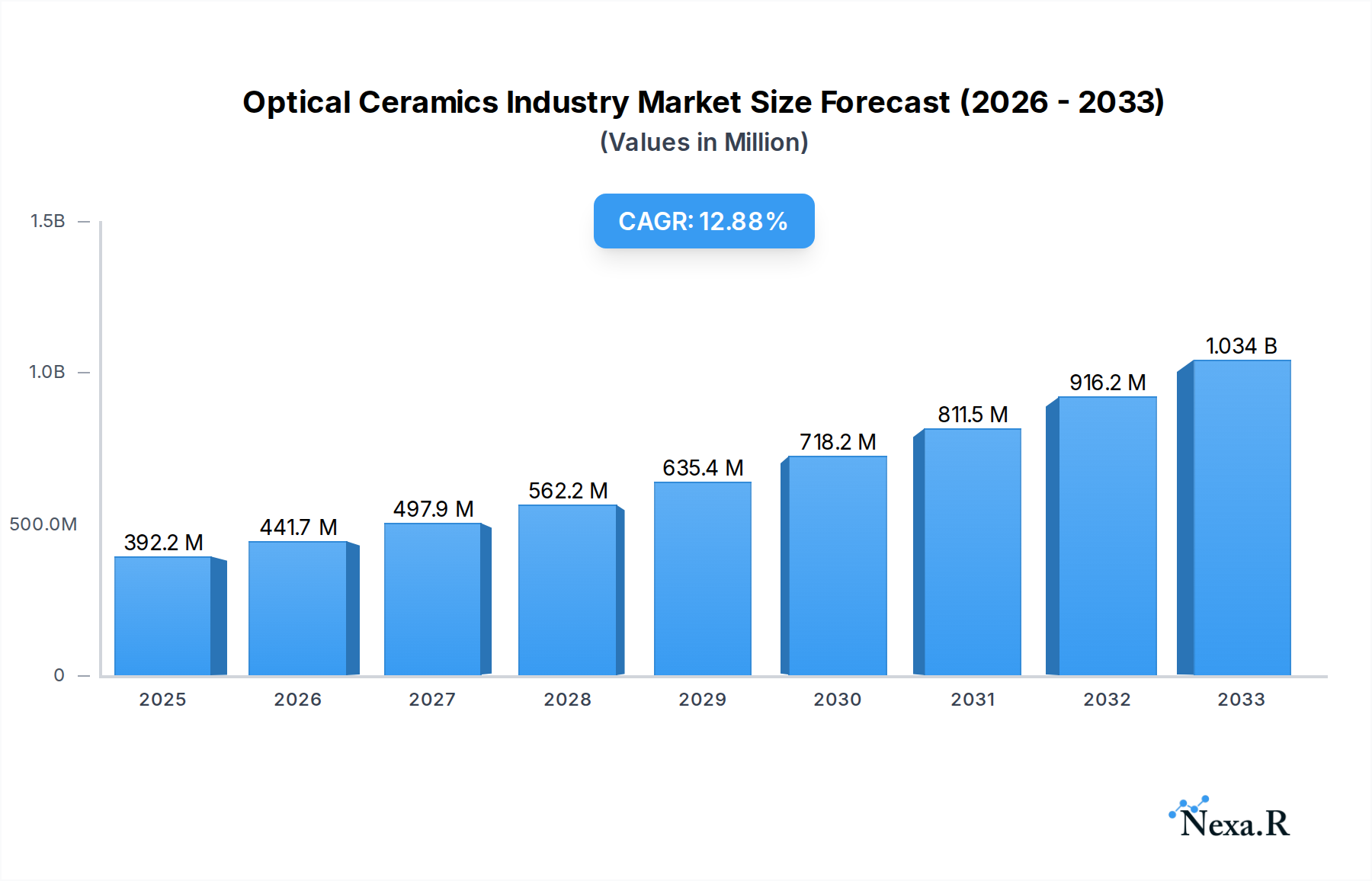

The global Optical Ceramics Market is poised for robust expansion, projected to reach USD 392.2 million by 2025, driven by an impressive Compound Annual Growth Rate (CAGR) of 12.6% during the forecast period of 2025-2033. This significant growth is propelled by escalating demand across various high-tech sectors. Key drivers include the increasing adoption of optical ceramics in advanced imaging systems within the aerospace and defense industries, where their durability, high refractive index, and thermal stability are paramount. The burgeoning renewable energy sector, particularly solar power, is also a substantial contributor, utilizing optical ceramics for efficient light transmission and protection. Furthermore, the healthcare industry's reliance on advanced diagnostic and therapeutic equipment, often incorporating specialized optical ceramic components, fuels market momentum. The consumer goods sector, with its growing demand for high-performance displays and optical lenses, further amplifies this upward trend.

Optical Ceramics Industry Market Size (In Million)

The market's trajectory is shaped by significant trends, including the continuous innovation in material science leading to enhanced optical properties and cost-effectiveness of polycrystalline and monocrystalline optical ceramics. Advancements in manufacturing techniques are also playing a crucial role in meeting the stringent quality and precision requirements of end-user industries. While the market presents substantial opportunities, certain restraints warrant consideration. The high initial investment costs associated with advanced manufacturing processes and raw material sourcing can pose challenges for market entry and expansion. Additionally, the development of alternative materials in some applications could present competitive pressure. However, the inherent superior performance characteristics of optical ceramics, such as their resistance to extreme temperatures, chemical inertness, and optical clarity, continue to solidify their position as indispensable materials in critical applications, ensuring sustained market growth.

Optical Ceramics Industry Company Market Share

This in-depth report offers a definitive analysis of the global Optical Ceramics Industry, providing critical insights into market dynamics, growth trajectories, technological advancements, and competitive landscapes from 2019 to 2033. Leveraging high-traffic keywords such as "optical ceramics market," "advanced ceramics," "laser optics," "photonics," "aerospace ceramics," "healthcare ceramics," and "energy ceramics," this report is meticulously designed to capture the attention of industry professionals, investors, and researchers. With a base year of 2025 and a detailed forecast period from 2025 to 2033, we present quantifiable data, including market size in million units, CAGR, and regional market shares, alongside qualitative factors that shape this rapidly evolving sector. Explore the parent market of Advanced Ceramics and its child market of Optical Ceramics, understanding their interconnected growth and investment potential.

Optical Ceramics Industry Market Dynamics & Structure

The Optical Ceramics Industry is characterized by a moderate market concentration, with leading players like Surmet Corporation, Konoshima Chemicals Co Ltd, CoorsTek Corporation, Schott AG, and Kyocera Corporation holding significant, albeit not dominant, market shares. Technological innovation remains a primary driver, fueled by advancements in material science, deposition techniques, and additive manufacturing, enabling the creation of ceramics with enhanced optical properties for demanding applications. Regulatory frameworks, particularly those related to material safety, environmental impact, and export controls in sectors like aerospace and defense, play a crucial role in shaping market access and product development. Competitive product substitutes, such as high-performance polymers and specialized glasses, present a challenge, but optical ceramics offer superior durability, thermal stability, and resistance to harsh environments, often justifying their premium cost. End-user demographics are increasingly skewed towards high-technology sectors, with significant demand stemming from the aerospace & defense, healthcare (medical imaging, surgical tools), energy (solar photovoltaics, LED lighting), and consumer electronics industries. Mergers and acquisitions (M&A) trends are observed, albeit at a steady pace, as companies seek to expand their technological capabilities and market reach.

- Market Concentration: Moderate, with key players focusing on specialized niches and advanced material development.

- Technological Innovation Drivers: Nanotechnology, material sintering advancements, precision polishing, and the demand for materials with tailored refractive indices and low loss.

- Regulatory Frameworks: Increasing emphasis on environmental compliance (e.g., REACH, RoHS) and export restrictions for sensitive applications.

- Competitive Product Substitutes: High-performance polymers, specialized optical glasses, and sapphire.

- End-User Demographics: Growing reliance on advanced materials in defense systems, sophisticated medical devices, renewable energy infrastructure, and next-generation consumer electronics.

- M&A Trends: Strategic acquisitions for technology integration and market expansion.

Optical Ceramics Industry Growth Trends & Insights

The global Optical Ceramics Industry is poised for robust growth, projected to witness a Compound Annual Growth Rate (CAGR) of approximately 8.5% during the forecast period of 2025–2033. This expansion is primarily driven by the escalating demand for high-performance optical components across a spectrum of critical industries. The market size, estimated at USD 3,500 million in the base year of 2025, is expected to reach USD 6,800 million by 2033. Adoption rates are accelerating, particularly in sectors where conventional materials fall short. Technological disruptions, such as the development of novel ceramic compositions with ultra-low optical loss and high laser damage threshold, are continuously expanding the application horizons for optical ceramics. Consumer behavior shifts are indirectly influencing this growth; for instance, the increasing consumer demand for higher resolution displays and advanced imaging technologies in consumer electronics and healthcare applications fuels the need for superior optical materials. Furthermore, the growing emphasis on renewable energy solutions, like advanced solar concentrators and efficient LED lighting systems, presents a significant market penetration opportunity. The inherent advantages of optical ceramics – exceptional hardness, chemical inertness, thermal stability, and precise optical control – make them indispensable in environments where other materials fail. The study period of 2019–2024 witnessed steady growth, laying a strong foundation for the accelerated expansion anticipated in the coming years.

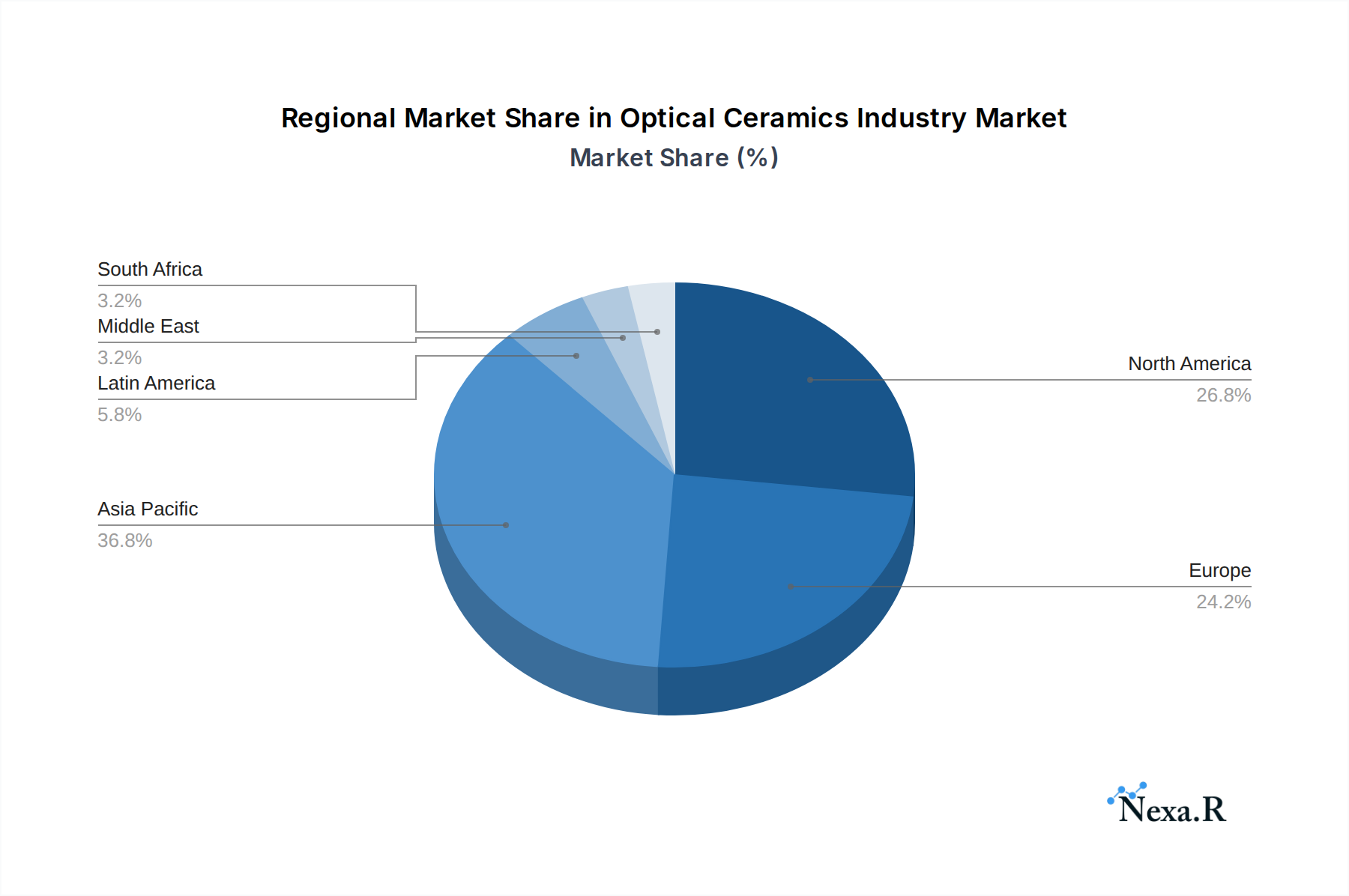

Dominant Regions, Countries, or Segments in Optical Ceramics Industry

The Aerospace & Defense end-user industry is a pivotal segment driving the growth of the global Optical Ceramics Industry. This segment is projected to command a substantial market share, estimated at over 25% of the total market value in 2025, with a forecast growth rate that outpaces many other sectors. The unique material properties of optical ceramics – their ability to withstand extreme temperatures, radiation, and mechanical stress – make them indispensable for a wide array of defense and aerospace applications. This includes high-performance lenses for missile guidance systems, robust optical windows for aircraft and spacecraft, specialized components for directed energy weapons, and advanced sensors for surveillance and reconnaissance. The stringent performance requirements and the critical nature of these applications necessitate the use of advanced materials like optical ceramics, where reliability and durability are paramount. Countries with strong aerospace and defense manufacturing bases, such as the United States, Europe (particularly Germany, France, and the UK), and to an increasing extent, China and India, are major consumers and innovators in this segment.

- Key Drivers in Aerospace & Defense:

- National Security Imperatives: Continuous investment in advanced military technologies and defense systems.

- Space Exploration Initiatives: Growing demand for lightweight, durable optical components for satellites, telescopes, and deep-space probes.

- Harsh Environment Resilience: Superior performance in extreme conditions encountered in aerospace applications.

- Miniaturization Trends: The need for compact yet high-performance optical systems.

- Dominance Factors:

- Market Share: Approximately 25% in 2025, projected to grow at a CAGR of 9.2% from 2025-2033.

- Growth Potential: Driven by ongoing R&D in next-generation defense platforms and expanding commercial space ventures.

- Technological Advancements: Development of ceramic-matrix composites and sapphire-like optical ceramics for enhanced performance.

- Economic Policies: Government funding for defense research and development, alongside incentives for domestic manufacturing.

Beyond Aerospace & Defense, the Healthcare segment is also a significant growth engine, driven by the demand for precision optics in medical imaging (e.g., MRI, CT scanners), surgical lasers, endoscopes, and diagnostic devices. The Energy sector, with its focus on solar energy (photovoltaic cell covers, concentrators) and advanced lighting solutions (high-efficiency LEDs), presents substantial growth opportunities. While Consumer Goods (e.g., camera lenses, displays) represent a mature market, innovations in this segment continue to contribute to overall demand.

Optical Ceramics Industry Product Landscape

The product landscape of the optical ceramics industry is defined by continuous innovation, leading to the development of specialized materials with tailored optical and mechanical properties. Key products include high-purity polycrystalline and monocrystalline alumina (Al2O3), yttria-stabilized zirconia (YSZ), silicon carbide (SiC), and advanced sapphire, manufactured through processes like sintering, hot pressing, and chemical vapor deposition. These materials are critical for applications requiring exceptional transparency, refractive index control, low absorption, high laser damage threshold, and resistance to harsh environments. Innovations focus on achieving higher transparency in specific wavelengths, improved thermal conductivity, and enhanced wear resistance. Unique selling propositions lie in their ability to outperform traditional optical materials in extreme conditions, enabling advancements in fields such as high-power lasers, advanced microscopy, and robust optical sensors.

Key Drivers, Barriers & Challenges in Optical Ceramics Industry

The Optical Ceramics Industry is propelled by several key drivers. Technological advancements in material science and manufacturing processes enable the creation of ceramics with superior optical performance, meeting the stringent demands of high-tech sectors. The growing demand for advanced solutions in aerospace & defense, healthcare, and energy applications, where durability and precision are paramount, further fuels market growth. The increasing miniaturization of electronic devices also necessitates compact, high-performance optical components.

However, the industry faces significant barriers and challenges. High manufacturing costs associated with precision processing and quality control can limit widespread adoption, particularly in price-sensitive markets. The complexity of ceramic fabrication, requiring specialized expertise and equipment, acts as another restraint. Supply chain vulnerabilities for rare earth elements and precursor materials can impact production stability and costs. Intense competition from alternative materials like specialized glasses and polymers, which may offer a lower cost-performance ratio for certain applications, poses a continuous challenge. Regulatory hurdles related to material sourcing, environmental impact, and end-of-life disposal also require careful navigation.

Emerging Opportunities in Optical Ceramics Industry

Emerging opportunities in the Optical Ceramics Industry are abundant, driven by ongoing research and evolving market needs. The burgeoning field of quantum computing and advanced photonics presents a significant avenue for specialized optical ceramics, particularly those with ultra-low optical loss and high purity. The increasing adoption of augmented reality (AR) and virtual reality (VR) technologies will drive demand for advanced optical elements with superior refractive properties and lightweight designs. Furthermore, the development of optical ceramics for next-generation sensing technologies, including environmental monitoring and advanced industrial inspection, offers untapped market potential. The growing emphasis on sustainable energy solutions is also creating opportunities for novel ceramic materials in advanced solar concentrators and high-efficiency lighting systems.

Growth Accelerators in the Optical Ceramics Industry Industry

Several catalysts are accelerating the growth of the Optical Ceramics Industry. Significant investment in research and development by leading companies and academic institutions is continuously pushing the boundaries of material performance, leading to the creation of novel ceramic compositions and processing techniques. Strategic partnerships and collaborations between material manufacturers, equipment providers, and end-users are crucial for co-developing customized solutions and streamlining the adoption of optical ceramics in new applications. Market expansion strategies, including a focus on emerging economies and the diversification of product portfolios to cater to a wider range of industries, are also significant growth accelerators. The increasing recognition of the long-term cost-effectiveness and superior performance of optical ceramics in demanding applications is also driving their adoption over conventional materials.

Key Players Shaping the Optical Ceramics Industry Market

- Surmet Corporation

- Konoshima Chemicals Co Ltd

- Coorstek Corporation

- Schott AG

- Kyocera Corporation

- CeraNova Corporation

- Ceramtec GmbH

- Ceradyne Inc

- Murata Manufacturing Co Ltd

- Saint-Gobain S A

Notable Milestones in Optical Ceramics Industry Sector

- 2019: Introduction of new sapphire-based optical windows for high-power laser systems by Schott AG, enhancing durability and laser damage resistance.

- 2020: Kyocera Corporation develops advanced transparent alumina (ALON) for defense applications, offering superior optical clarity and ballistic protection.

- 2021: CoorsTek Corporation announces expansion of its optical ceramic manufacturing capabilities to meet growing demand from the aerospace sector.

- 2022: Ceramtec GmbH develops novel ceramic components for advanced medical imaging devices, improving diagnostic accuracy and patient comfort.

- 2023: Saint-Gobain S.A. launches a new range of optical ceramic substrates for high-efficiency LED lighting, contributing to energy conservation efforts.

- 2024: Surmet Corporation patents a novel process for producing ultra-smooth ceramic optical surfaces, reducing light scattering and improving signal integrity.

In-Depth Optical Ceramics Industry Market Outlook

The future outlook for the Optical Ceramics Industry is exceptionally bright, characterized by sustained high growth and expanding application frontiers. The continuous push for technological innovation across key sectors like aerospace, defense, healthcare, and energy will remain the primary growth accelerator, driving demand for materials with unparalleled performance characteristics. Strategic collaborations between manufacturers and end-users will further refine product development, ensuring that optical ceramics precisely meet evolving application needs. The increasing focus on advanced photonics, quantum technologies, and enhanced consumer electronics will unlock new market segments. As manufacturing processes mature and economies of scale are realized, the cost-effectiveness of optical ceramics is expected to improve, facilitating broader market penetration. The industry is well-positioned to capitalize on global trends towards miniaturization, increased efficiency, and the need for robust solutions in challenging environments.

Optical Ceramics Industry Segmentation

-

1. Type

- 1.1. Polycrystalline

- 1.2. Monocrystalline

-

2. End-user Industry

- 2.1. Aerospace & Defense

- 2.2. Energy

- 2.3. Healthcare

- 2.4. Consumer Goods

- 2.5. Other End-user Industries

Optical Ceramics Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. Germany

- 2.2. France

- 2.3. United Kingdom

- 2.4. Spain

- 2.5. Italy

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. South Korea

- 3.4. India

- 3.5. Japan

- 3.6. Rest of Asia Pacific

-

4. Latin America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of Latin America

- 5. Middle East

-

6. Saudi Arabia

- 6.1. South Africa

- 6.2. Rest of Middle East

Optical Ceramics Industry Regional Market Share

Geographic Coverage of Optical Ceramics Industry

Optical Ceramics Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Polycrystalline

- 5.1.2. Monocrystalline

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Aerospace & Defense

- 5.2.2. Energy

- 5.2.3. Healthcare

- 5.2.4. Consumer Goods

- 5.2.5. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East

- 5.3.6. Saudi Arabia

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Optical Ceramics Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Polycrystalline

- 6.1.2. Monocrystalline

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Aerospace & Defense

- 6.2.2. Energy

- 6.2.3. Healthcare

- 6.2.4. Consumer Goods

- 6.2.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Optical Ceramics Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Polycrystalline

- 7.1.2. Monocrystalline

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Aerospace & Defense

- 7.2.2. Energy

- 7.2.3. Healthcare

- 7.2.4. Consumer Goods

- 7.2.5. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Optical Ceramics Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Polycrystalline

- 8.1.2. Monocrystalline

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Aerospace & Defense

- 8.2.2. Energy

- 8.2.3. Healthcare

- 8.2.4. Consumer Goods

- 8.2.5. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific Optical Ceramics Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Polycrystalline

- 9.1.2. Monocrystalline

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Aerospace & Defense

- 9.2.2. Energy

- 9.2.3. Healthcare

- 9.2.4. Consumer Goods

- 9.2.5. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Latin America Optical Ceramics Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Polycrystalline

- 10.1.2. Monocrystalline

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. Aerospace & Defense

- 10.2.2. Energy

- 10.2.3. Healthcare

- 10.2.4. Consumer Goods

- 10.2.5. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Middle East Optical Ceramics Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Polycrystalline

- 11.1.2. Monocrystalline

- 11.2. Market Analysis, Insights and Forecast - by End-user Industry

- 11.2.1. Aerospace & Defense

- 11.2.2. Energy

- 11.2.3. Healthcare

- 11.2.4. Consumer Goods

- 11.2.5. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Saudi Arabia Optical Ceramics Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Type

- 12.1.1. Polycrystalline

- 12.1.2. Monocrystalline

- 12.2. Market Analysis, Insights and Forecast - by End-user Industry

- 12.2.1. Aerospace & Defense

- 12.2.2. Energy

- 12.2.3. Healthcare

- 12.2.4. Consumer Goods

- 12.2.5. Other End-user Industries

- 12.1. Market Analysis, Insights and Forecast - by Type

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Surmet Corporation

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Konoshima Chemicals Co Ltd

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Coorstek Corporation

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Schott AG

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Kyocera Corporation

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 CeraNova Corporation

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Ceramtec GmbH

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Ceradyne Inc

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Murata Manufacturing Co Ltd

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 Saint-Gobain S A

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.1 Surmet Corporation

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Optical Ceramics Industry Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Optical Ceramics Industry Revenue (million), by Type 2025 & 2033

- Figure 3: North America Optical Ceramics Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Optical Ceramics Industry Revenue (million), by End-user Industry 2025 & 2033

- Figure 5: North America Optical Ceramics Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 6: North America Optical Ceramics Industry Revenue (million), by Country 2025 & 2033

- Figure 7: North America Optical Ceramics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Optical Ceramics Industry Revenue (million), by Type 2025 & 2033

- Figure 9: Europe Optical Ceramics Industry Revenue Share (%), by Type 2025 & 2033

- Figure 10: Europe Optical Ceramics Industry Revenue (million), by End-user Industry 2025 & 2033

- Figure 11: Europe Optical Ceramics Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 12: Europe Optical Ceramics Industry Revenue (million), by Country 2025 & 2033

- Figure 13: Europe Optical Ceramics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Optical Ceramics Industry Revenue (million), by Type 2025 & 2033

- Figure 15: Asia Pacific Optical Ceramics Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Asia Pacific Optical Ceramics Industry Revenue (million), by End-user Industry 2025 & 2033

- Figure 17: Asia Pacific Optical Ceramics Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 18: Asia Pacific Optical Ceramics Industry Revenue (million), by Country 2025 & 2033

- Figure 19: Asia Pacific Optical Ceramics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America Optical Ceramics Industry Revenue (million), by Type 2025 & 2033

- Figure 21: Latin America Optical Ceramics Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: Latin America Optical Ceramics Industry Revenue (million), by End-user Industry 2025 & 2033

- Figure 23: Latin America Optical Ceramics Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: Latin America Optical Ceramics Industry Revenue (million), by Country 2025 & 2033

- Figure 25: Latin America Optical Ceramics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East Optical Ceramics Industry Revenue (million), by Type 2025 & 2033

- Figure 27: Middle East Optical Ceramics Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: Middle East Optical Ceramics Industry Revenue (million), by End-user Industry 2025 & 2033

- Figure 29: Middle East Optical Ceramics Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 30: Middle East Optical Ceramics Industry Revenue (million), by Country 2025 & 2033

- Figure 31: Middle East Optical Ceramics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: Saudi Arabia Optical Ceramics Industry Revenue (million), by Type 2025 & 2033

- Figure 33: Saudi Arabia Optical Ceramics Industry Revenue Share (%), by Type 2025 & 2033

- Figure 34: Saudi Arabia Optical Ceramics Industry Revenue (million), by End-user Industry 2025 & 2033

- Figure 35: Saudi Arabia Optical Ceramics Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 36: Saudi Arabia Optical Ceramics Industry Revenue (million), by Country 2025 & 2033

- Figure 37: Saudi Arabia Optical Ceramics Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Optical Ceramics Industry Revenue million Forecast, by Type 2020 & 2033

- Table 2: Global Optical Ceramics Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 3: Global Optical Ceramics Industry Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Optical Ceramics Industry Revenue million Forecast, by Type 2020 & 2033

- Table 5: Global Optical Ceramics Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 6: Global Optical Ceramics Industry Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Optical Ceramics Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Optical Ceramics Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Global Optical Ceramics Industry Revenue million Forecast, by Type 2020 & 2033

- Table 10: Global Optical Ceramics Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 11: Global Optical Ceramics Industry Revenue million Forecast, by Country 2020 & 2033

- Table 12: Germany Optical Ceramics Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 13: France Optical Ceramics Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: United Kingdom Optical Ceramics Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Spain Optical Ceramics Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Italy Optical Ceramics Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 17: Rest of Europe Optical Ceramics Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 18: Global Optical Ceramics Industry Revenue million Forecast, by Type 2020 & 2033

- Table 19: Global Optical Ceramics Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 20: Global Optical Ceramics Industry Revenue million Forecast, by Country 2020 & 2033

- Table 21: China Optical Ceramics Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Japan Optical Ceramics Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: South Korea Optical Ceramics Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: India Optical Ceramics Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Japan Optical Ceramics Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Rest of Asia Pacific Optical Ceramics Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Global Optical Ceramics Industry Revenue million Forecast, by Type 2020 & 2033

- Table 28: Global Optical Ceramics Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 29: Global Optical Ceramics Industry Revenue million Forecast, by Country 2020 & 2033

- Table 30: Brazil Optical Ceramics Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 31: Argentina Optical Ceramics Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Rest of Latin America Optical Ceramics Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: Global Optical Ceramics Industry Revenue million Forecast, by Type 2020 & 2033

- Table 34: Global Optical Ceramics Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 35: Global Optical Ceramics Industry Revenue million Forecast, by Country 2020 & 2033

- Table 36: Global Optical Ceramics Industry Revenue million Forecast, by Type 2020 & 2033

- Table 37: Global Optical Ceramics Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 38: Global Optical Ceramics Industry Revenue million Forecast, by Country 2020 & 2033

- Table 39: South Africa Optical Ceramics Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 40: Rest of Middle East Optical Ceramics Industry Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Optical Ceramics Industry?

The projected CAGR is approximately 12.6%.

2. Which companies are prominent players in the Optical Ceramics Industry?

Key companies in the market include Surmet Corporation, Konoshima Chemicals Co Ltd, Coorstek Corporation, Schott AG, Kyocera Corporation, CeraNova Corporation, Ceramtec GmbH, Ceradyne Inc , Murata Manufacturing Co Ltd, Saint-Gobain S A.

3. What are the main segments of the Optical Ceramics Industry?

The market segments include Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 392.2 million as of 2022.

5. What are some drivers contributing to market growth?

; Substitute to Glass. Metals. and Plastics; Increasing Defense Expenditure on Advanced Materials and Technologies.

6. What are the notable trends driving market growth?

Aerospace & Defense Expected to Witness Significant Growth.

7. Are there any restraints impacting market growth?

; High Cost of Optical Ceramics.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Optical Ceramics Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Optical Ceramics Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Optical Ceramics Industry?

To stay informed about further developments, trends, and reports in the Optical Ceramics Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence