Key Insights

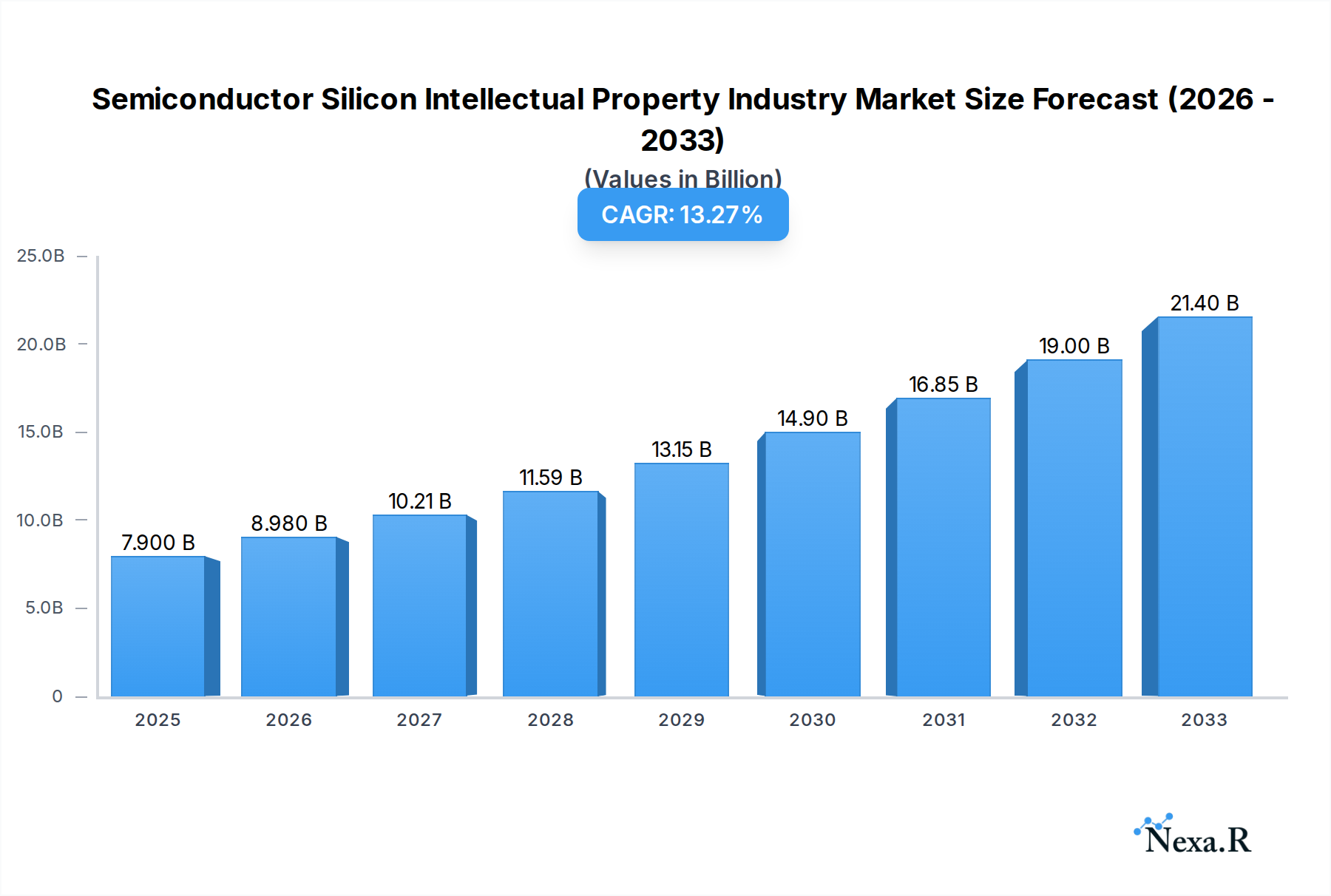

The Semiconductor Silicon Intellectual Property (IP) market is poised for substantial growth, driven by the relentless demand for sophisticated chips across a myriad of end-user verticals. Valued at an estimated $7.9 billion in 2025, the market is projected to expand at a robust Compound Annual Growth Rate (CAGR) of 13.9% through 2033. This impressive expansion is fueled by the increasing complexity of semiconductor designs and the growing need for specialized IP cores. Key market drivers include the escalating adoption of AI and machine learning in edge devices, the proliferation of 5G infrastructure, and the growing sophistication of automotive electronics, particularly in areas like autonomous driving and advanced driver-assistance systems (ADAS). The consumer electronics segment continues to be a dominant force, with smart devices, wearables, and advanced display technologies demanding more power-efficient and high-performance IP solutions. Furthermore, the burgeoning IoT ecosystem necessitates innovative IP for connectivity, security, and processing in a wide array of connected devices.

Semiconductor Silicon Intellectual Property Industry Market Size (In Billion)

The market is segmented by revenue type into licenses, royalties, and services, with each contributing significantly to the overall revenue. Processor IP and wired and wireless interface IP represent critical segments, underpinning the functionality of most modern electronic devices. Emerging IP types, such as those for specialized AI accelerators and advanced security functions, are also gaining traction. While market growth is strong, potential restraints such as the high cost of IP development and the increasing complexity of IP integration into system-on-chip (SoC) designs present challenges. However, the strategic partnerships and collaborations between IP providers and semiconductor manufacturers, alongside the continuous innovation in IP architectures, are expected to mitigate these challenges. Geographically, Asia, led by China, Taiwan, Japan, and South Korea, is anticipated to be the largest and fastest-growing region due to its strong manufacturing base and significant investments in semiconductor R&D. North America and Europe are also key markets, driven by innovation in automotive, industrial, and consumer electronics sectors.

Semiconductor Silicon Intellectual Property Industry Company Market Share

Unveiling the Future: Semiconductor Silicon Intellectual Property Industry Report 2024-2033

This comprehensive report offers an in-depth analysis of the global Semiconductor Silicon Intellectual Property (IP) market, a critical component driving innovation across the digital landscape. We dissect the intricate dynamics, growth trajectories, and competitive forces shaping this vital industry, providing actionable insights for stakeholders. With a meticulous Study Period of 2019–2033, a Base Year of 2025, and a detailed Forecast Period of 2025–2033, this report leverages extensive data from the Historical Period (2019–2024) to predict future market evolution. Explore the lucrative opportunities within the parent market of semiconductor IP and its diverse child markets, including processor IP, interface IP, and specialized IPs for automotive and AI applications. This report is essential for understanding the technological advancements, market segmentation, and strategic imperatives of the semiconductor IP ecosystem.

Semiconductor Silicon Intellectual Property Industry Market Dynamics & Structure

The global Semiconductor Silicon Intellectual Property (IP) market is characterized by a dynamic and evolving landscape, driven by rapid technological advancements and increasing demand for specialized chip designs. Market concentration is moderately high, with a few key players dominating the supply of core IP blocks. However, the rise of specialized IP providers catering to niche applications like AI, automotive, and IoT is fostering a more fragmented yet innovative environment. Technological innovation is the primary driver, fueled by the relentless pursuit of higher performance, lower power consumption, and advanced functionalities in semiconductors. Regulatory frameworks, while generally supportive of innovation, can introduce complexities related to intellectual property protection and cross-border licensing. Competitive product substitutes are limited for highly specialized and patented IP cores, but the availability of open-source alternatives and in-house IP development by large semiconductor giants presents indirect competition. End-user demographics are expanding beyond traditional consumer electronics and computing to encompass the burgeoning automotive, industrial, and medical sectors, each with unique IP requirements. Mergers and acquisitions (M&A) trends are significant, with larger IP vendors acquiring smaller, innovative companies to broaden their portfolio and strengthen their market position.

- Market Concentration: Moderate to high, with a few dominant players for foundational IP, alongside a growing number of specialized IP providers.

- Technological Innovation Drivers: Demand for AI/ML acceleration, advanced connectivity (5G/6G), power efficiency, miniaturization, and specialized functionalities for emerging markets.

- Regulatory Frameworks: Primarily focused on IP protection, trade regulations, and increasingly, on national security concerns related to semiconductor supply chains.

- Competitive Product Substitutes: Open-source IP alternatives, in-house IP development by large foundries and fabless companies.

- End-User Demographics: Diversifying from Consumer Electronics and Computers & Peripherals to significant growth in Automobile, Industrial, and Healthcare sectors.

- M&A Trends: Strategic acquisitions to expand IP portfolios, gain access to new markets, and consolidate market share. For instance, the acquisition of specialized AI IP by larger players to bolster their AI platform offerings.

Semiconductor Silicon Intellectual Property Industry Growth Trends & Insights

The Semiconductor Silicon Intellectual Property (IP) market is poised for robust growth, projected to reach a substantial market size by 2025. This expansion is fueled by the ever-increasing complexity and specialization required in modern semiconductor designs. The adoption rates of third-party IP are accelerating as chip designers increasingly focus on core competencies and leverage pre-designed IP blocks to reduce development time and costs. Market size evolution indicates a consistent upward trajectory, driven by the proliferation of connected devices, the surge in artificial intelligence and machine learning applications, and the stringent requirements of the automotive sector for advanced driver-assistance systems (ADAS) and autonomous driving. Technological disruptions, such as the advancements in chiplet architectures and heterogeneous integration, are creating new opportunities for specialized IP. Furthermore, shifts in consumer behavior, demanding more powerful, efficient, and feature-rich electronic devices, are directly translating into higher demand for innovative semiconductor IP. The CAGR is expected to remain strong throughout the forecast period, reflecting the indispensable role of IP in enabling next-generation semiconductors. Market penetration is high in established segments like processors and interfaces, with significant growth potential in emerging areas like AI accelerators and specialized automotive IPs.

The market size for the Semiconductor Silicon Intellectual Property industry is estimated to reach approximately $7.2$ billion in 2025, with projections indicating a substantial increase to $12.8$ billion by 2033, representing a significant CAGR of xx% during the forecast period. This growth is underpinned by several key trends. Firstly, the escalating demand for high-performance computing (HPC) and specialized processing units for AI and machine learning workloads is a primary catalyst. Companies are increasingly relying on licensable IP for AI accelerators, neural processing units (NPUs), and specialized DSPs to gain a competitive edge. Secondly, the automotive industry's transformation towards electrification and autonomous driving is driving unprecedented demand for automotive-grade IP. This includes IP for ADAS, in-vehicle infotainment systems, and power management solutions, with the market penetration in this vertical showing rapid acceleration. Thirdly, the continued expansion of the Internet of Things (IoT) ecosystem, encompassing smart homes, industrial automation, and wearables, necessitates energy-efficient and highly integrated IP solutions. Processor IP, particularly for embedded systems and microcontrollers, remains a cornerstone of this segment.

Moreover, the wired and wireless interface IP segment is experiencing robust growth due to the increasing bandwidth requirements for 5G, Wi-Fi 6/7, and high-speed data transfer protocols. The complexity of designing these interfaces in-house often makes licensing a more cost-effective and time-efficient solution for many semiconductor companies. The ongoing miniaturization of electronic devices and the push for ultra-low power consumption in battery-operated systems are also significant growth drivers for specialized IP in areas like power management and signal processing. The competitive landscape is characterized by continuous innovation, with IP providers investing heavily in R&D to offer cutting-edge solutions that meet the evolving needs of chip designers. Strategic partnerships and collaborations between IP vendors, foundries, and fabless semiconductor companies are becoming increasingly common, fostering a more integrated and efficient ecosystem. Consumer behavior shifts, such as the demand for immersive gaming experiences and advanced virtual/augmented reality applications, are also indirectly fueling the need for more powerful and specialized processor and graphics IP.

Dominant Regions, Countries, or Segments in Semiconductor Silicon Intellectual Property Industry

The global Semiconductor Silicon Intellectual Property (IP) industry is experiencing significant growth, with its dominance segmented across various revenue types, IP types, and end-user verticals. Analyzing these segments reveals key drivers and growth potential.

Dominance by Revenue Type:

- License: This segment, accounting for an estimated $3.5$ billion in 2025, remains the most dominant revenue stream. The licensing of pre-designed IP blocks allows semiconductor companies to accelerate their design cycles and reduce upfront development costs, making it a fundamental part of the industry.

- Royalty: Projected to reach $2.7$ billion in 2025, royalties are a crucial revenue source, typically tied to the volume of chips manufactured using licensed IP. The increasing volume of semiconductor production globally directly fuels this segment's growth.

- Services: Valued at approximately $1.0$ billion in 2025, the services segment, encompassing customization, integration, and verification support, is crucial for ensuring the successful implementation of IP blocks. Its growth is closely linked to the complexity of new chip designs.

Dominance by IP Type:

- Processor IP: This remains the cornerstone of the industry, estimated at $4.0$ billion in 2025. The pervasive need for central processing units (CPUs), graphics processing units (GPUs), and specialized digital signal processors (DSPs) across all electronic devices drives its continued dominance.

- Wired and Wireless Interface IP: With an estimated market size of $2.0$ billion in 2025, this segment is experiencing rapid growth. The proliferation of high-speed communication standards like 5G, Wi-Fi 6/7, and USB 4.0 necessitates advanced interface IP, making it a critical growth area.

- Other IP Types: This category, including IPs for AI/ML acceleration, security, analog and mixed-signal, and specialized peripherals, is projected to reach $1.2$ billion in 2025. This segment is characterized by high innovation and rapid growth, driven by emerging technologies.

Dominance by End-user Vertical:

- Consumer Electronics: Historically the largest segment, projected to reach $3.0$ billion in 2025. While mature, the continuous demand for new smartphones, tablets, wearables, and home entertainment devices ensures sustained growth.

- Computers and Peripherals: Valued at approximately $1.8$ billion in 2025, this segment includes PCs, laptops, servers, and associated peripherals, all of which require increasingly sophisticated processor and interface IP.

- Automobile: This vertical is the fastest-growing, with an estimated market size of $1.5$ billion in 2025. The increasing integration of electronics for ADAS, infotainment, and powertrain management in vehicles is a significant driver.

- Industrial: Expected to reach $0.7$ billion in 2025, the industrial sector's adoption of automation, IoT, and smart manufacturing technologies fuels demand for reliable and specialized IP.

- Other End-user Verticals: Including medical devices and telecommunications infrastructure, this segment is projected to reach $0.2$ billion in 2025, with high growth potential in specialized applications.

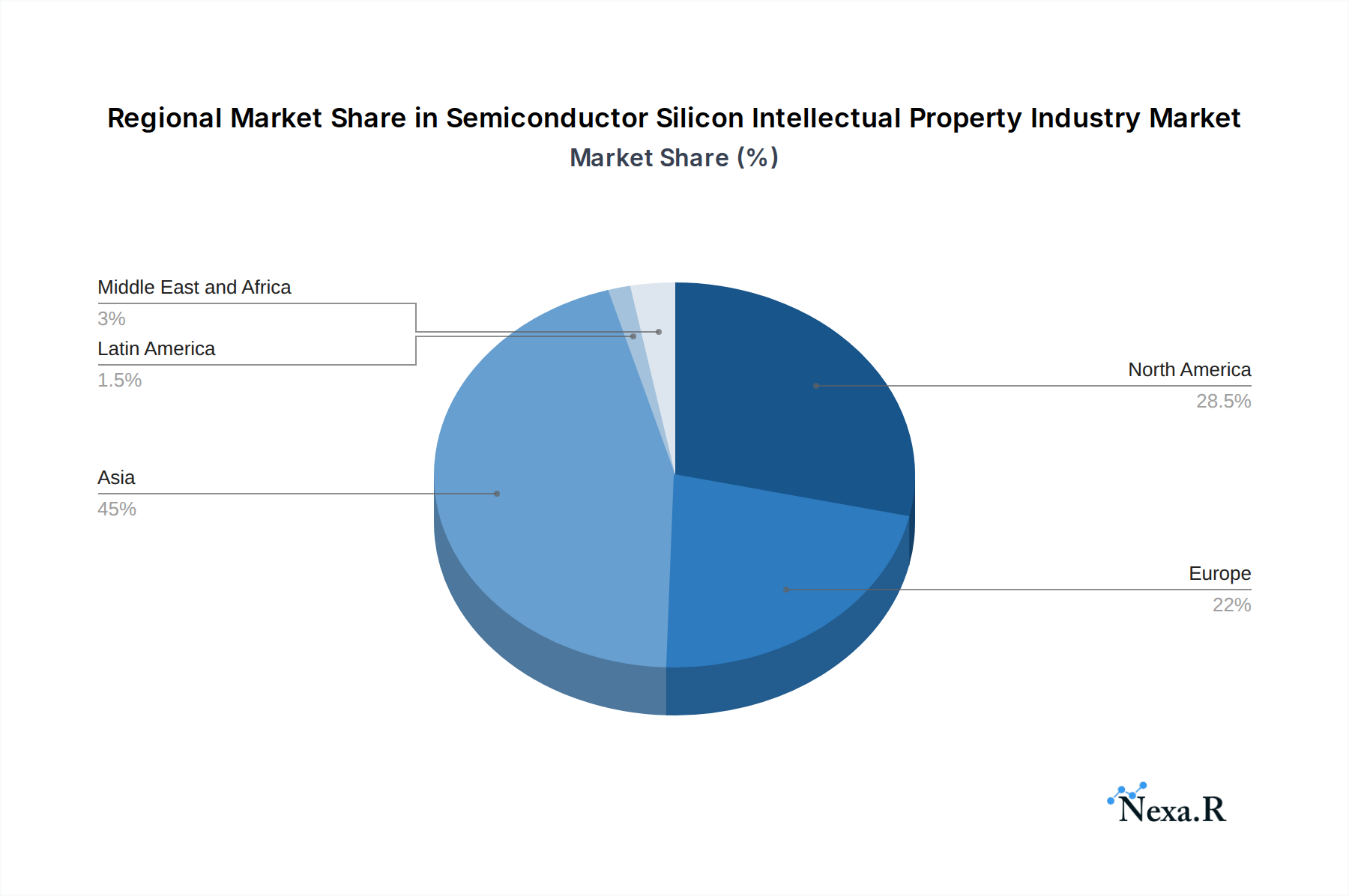

Dominant Regions:

While the report focuses on global market dynamics, it's important to note that Asia Pacific is emerging as a dominant region due to its significant role in semiconductor manufacturing and a rapidly growing consumer electronics market. North America and Europe remain strong in IP research and development and for their automotive and industrial applications.

Semiconductor Silicon Intellectual Property Industry Product Landscape

The product landscape of the Semiconductor Silicon Intellectual Property (IP) industry is defined by innovation and specialization. Key products include robust Processor IP (CPUs, GPUs, NPUs), high-speed Wired and Wireless Interface IP (USB, PCIe, Ethernet, Wi-Fi, 5G), and a rapidly expanding array of Other IP Types such as security cores, AI/ML accelerators, and analog/mixed-signal IPs. These IPs are designed to meet stringent performance, power, and area (PPA) requirements for diverse applications. Unique selling propositions lie in their proven track record, comprehensive verification, and expert support, enabling faster time-to-market for chip manufacturers. Technological advancements focus on increasing core efficiency, reducing power consumption, enhancing security features, and enabling seamless integration into complex System-on-Chips (SoCs).

Key Drivers, Barriers & Challenges in Semiconductor Silicon Intellectual Property Industry

Key Drivers

The Semiconductor Silicon Intellectual Property (IP) market is propelled by several critical drivers:

- Accelerating Demand for Advanced Functionality: The relentless pursuit of higher performance, lower power consumption, and specialized features for AI, IoT, 5G, and automotive applications is a primary growth catalyst.

- Time-to-Market Pressure: Semiconductor companies face intense pressure to bring new products to market quickly. Licensable IP significantly reduces design cycles and associated R&D costs, offering a substantial competitive advantage.

- Increasing Chip Complexity: Modern SoCs integrate an ever-growing number of functionalities. Leveraging pre-verified IP blocks is essential to manage this complexity and ensure design success.

- Cost Optimization: Developing complex IP blocks in-house can be prohibitively expensive. IP licensing offers a more cost-effective solution, especially for smaller and medium-sized enterprises.

- Innovation in Emerging Technologies: The rapid evolution of AI, machine learning, autonomous driving, and edge computing creates a continuous demand for novel and specialized IP solutions.

Barriers & Challenges

Despite the strong growth, the industry faces several significant barriers and challenges:

- Intellectual Property Protection and Security: Ensuring the security and integrity of licensed IP is paramount. The risk of IP theft or unauthorized use poses a significant challenge, requiring robust legal frameworks and technical safeguards.

- Integration Complexity: While IP blocks are designed for reusability, integrating them into a complex SoC can still be challenging. Thorough verification and compatibility checks are crucial, often requiring significant engineering effort.

- Talent Shortage: The demand for highly skilled semiconductor design engineers, verification specialists, and IP architects continues to outpace supply, creating a bottleneck for both IP vendors and their customers.

- Global Supply Chain Disruptions: Geopolitical factors and unforeseen events can disrupt the semiconductor supply chain, impacting the production and availability of chips that utilize licensed IP, indirectly affecting the IP market.

- Intense Competition and Pricing Pressures: The market is highly competitive, with established players and emerging entrants vying for market share. This can lead to pricing pressures and the need for continuous innovation to differentiate offerings. The global semiconductor IP market faces a projected challenge of $1.5$ billion in lost revenue potential due to integration complexities and verification delays in 2025, highlighting the need for streamlined solutions.

Emerging Opportunities in Semiconductor Silicon Intellectual Property Industry

Emerging opportunities within the Semiconductor Silicon Intellectual Property (IP) industry are abundant, driven by transformative technological shifts. The burgeoning field of AI at the Edge presents a significant opportunity for specialized AI accelerator IPs and efficient neural processing units (NPUs) that can operate with low power consumption. The rapid advancements in next-generation wireless technologies, such as 6G and beyond, will drive demand for novel communication interface IPs. Furthermore, the increasing focus on sustainable computing and energy efficiency opens doors for low-power processor IPs and power management solutions. The expansion of the metaverse and immersive technologies will necessitate high-performance graphics and compute IPs. The increasing complexity and security demands of automotive semiconductors, particularly for autonomous driving, represent a substantial and growing market for specialized safety-critical and high-performance IP.

Growth Accelerators in the Semiconductor Silicon Intellectual Property Industry Industry

Several key catalysts are accelerating growth in the Semiconductor Silicon Intellectual Property (IP) industry. Technological breakthroughs in areas like advanced node manufacturing, heterogeneous integration (chiplets), and novel semiconductor materials are creating fertile ground for new IP development and adoption. Strategic partnerships and collaborations between IP vendors, foundries, AI chip designers, and end-user application developers are crucial for co-optimizing IP for specific market needs and fostering ecosystem growth. For example, partnerships between IP providers and AI framework developers ensure seamless integration and performance optimization. Furthermore, market expansion strategies targeting rapidly growing sectors like automotive, industrial IoT, and healthcare are driving demand and creating new revenue streams. The increasing adoption of design reuse methodologies and the need to shorten product development cycles globally further solidify IP as a fundamental growth accelerator.

Key Players Shaping the Semiconductor Silicon Intellectual Property Industry Market

- Rambus Incorporated

- Achronix Semiconductor Corporation

- CEVA Inc

- LTIMindtree Limited

- Imagination Technologies Ltd

- Fujitsu Ltd

- Andes Technology Corporation

- Faraday Technology Corporation

- MIPS Tech LLC

- Digital Media Professionals

- Synopsys Inc

- Cadence Design Systems Inc

- eMemory Technology Inc

- MediaTek Inc

- VeriSilicon Holdings Co Ltd

- ARM Ltd (SoftBank )

Notable Milestones in Semiconductor Silicon Intellectual Property Industry Sector

- May 2023: CEVA Inc. announced the acquisition of the RealSpace 3D Spatial Audio business, technology, and patents from VisiSonics Corporation. This strategic move expands CEVA's application software portfolio for embedded systems, particularly strengthening its position in the wearables market where spatial audio is becoming a key differentiator.

- March 2023: Synopsys launched its groundbreaking Synopsys.ai suite, a comprehensive set of AI-powered electronic design automation (EDA) tools. This suite spans the entire chip design process, promising significant reductions in development time, costs, and improved chip yields for advanced process nodes (5nm, 3nm, 2nm-class, and beyond).

In-Depth Semiconductor Silicon Intellectual Property Industry Market Outlook

The Semiconductor Silicon Intellectual Property (IP) Industry is set for a period of sustained and dynamic growth, propelled by the relentless pace of technological innovation and the increasing complexity of semiconductor designs. Key growth accelerators include the pervasive demand for AI-centric processing, the evolution of high-speed connectivity standards, and the insatiable appetite for sophisticated functionalities across consumer electronics, automotive, and industrial sectors. Strategic partnerships between IP providers and leading semiconductor manufacturers are optimizing IP for cutting-edge applications, fostering ecosystem development. The ongoing trend of chipletization and heterogeneous integration further amplifies the need for modular and reusable IP. Future market potential is immense, particularly in areas like edge AI, advanced driver-assistance systems (ADAS), and next-generation communication technologies, underscoring the indispensable role of IP in shaping the future of electronics.

Semiconductor Silicon Intellectual Property Industry Segmentation

-

1. Revenue Type

- 1.1. License

- 1.2. Royalty

- 1.3. Services

-

2. IP Type

- 2.1. Processor IP

- 2.2. Wired and Wireless Interface IP

- 2.3. Other IP Types

-

3. End-user Vertical

- 3.1. Consumer Electronics

- 3.2. Computers and Peripherals

- 3.3. Automobile

- 3.4. Industrial

- 3.5. Other End-user Verticals

Semiconductor Silicon Intellectual Property Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. United Kingdom

- 2.2. Germany

- 2.3. France

-

3. Asia

- 3.1. China

- 3.2. Taiwan

- 3.3. Japan

- 3.4. South Korea

- 3.5. India

- 3.6. Australia and New Zealand

- 4. Latin America

- 5. Middle East and Africa

Semiconductor Silicon Intellectual Property Industry Regional Market Share

Geographic Coverage of Semiconductor Silicon Intellectual Property Industry

Semiconductor Silicon Intellectual Property Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 13.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Revenue Type

- 5.1.1. License

- 5.1.2. Royalty

- 5.1.3. Services

- 5.2. Market Analysis, Insights and Forecast - by IP Type

- 5.2.1. Processor IP

- 5.2.2. Wired and Wireless Interface IP

- 5.2.3. Other IP Types

- 5.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 5.3.1. Consumer Electronics

- 5.3.2. Computers and Peripherals

- 5.3.3. Automobile

- 5.3.4. Industrial

- 5.3.5. Other End-user Verticals

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia

- 5.4.4. Latin America

- 5.4.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Revenue Type

- 6. Global Semiconductor Silicon Intellectual Property Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Revenue Type

- 6.1.1. License

- 6.1.2. Royalty

- 6.1.3. Services

- 6.2. Market Analysis, Insights and Forecast - by IP Type

- 6.2.1. Processor IP

- 6.2.2. Wired and Wireless Interface IP

- 6.2.3. Other IP Types

- 6.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 6.3.1. Consumer Electronics

- 6.3.2. Computers and Peripherals

- 6.3.3. Automobile

- 6.3.4. Industrial

- 6.3.5. Other End-user Verticals

- 6.1. Market Analysis, Insights and Forecast - by Revenue Type

- 7. North America Semiconductor Silicon Intellectual Property Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Revenue Type

- 7.1.1. License

- 7.1.2. Royalty

- 7.1.3. Services

- 7.2. Market Analysis, Insights and Forecast - by IP Type

- 7.2.1. Processor IP

- 7.2.2. Wired and Wireless Interface IP

- 7.2.3. Other IP Types

- 7.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 7.3.1. Consumer Electronics

- 7.3.2. Computers and Peripherals

- 7.3.3. Automobile

- 7.3.4. Industrial

- 7.3.5. Other End-user Verticals

- 7.1. Market Analysis, Insights and Forecast - by Revenue Type

- 8. Europe Semiconductor Silicon Intellectual Property Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Revenue Type

- 8.1.1. License

- 8.1.2. Royalty

- 8.1.3. Services

- 8.2. Market Analysis, Insights and Forecast - by IP Type

- 8.2.1. Processor IP

- 8.2.2. Wired and Wireless Interface IP

- 8.2.3. Other IP Types

- 8.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 8.3.1. Consumer Electronics

- 8.3.2. Computers and Peripherals

- 8.3.3. Automobile

- 8.3.4. Industrial

- 8.3.5. Other End-user Verticals

- 8.1. Market Analysis, Insights and Forecast - by Revenue Type

- 9. Asia Semiconductor Silicon Intellectual Property Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Revenue Type

- 9.1.1. License

- 9.1.2. Royalty

- 9.1.3. Services

- 9.2. Market Analysis, Insights and Forecast - by IP Type

- 9.2.1. Processor IP

- 9.2.2. Wired and Wireless Interface IP

- 9.2.3. Other IP Types

- 9.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 9.3.1. Consumer Electronics

- 9.3.2. Computers and Peripherals

- 9.3.3. Automobile

- 9.3.4. Industrial

- 9.3.5. Other End-user Verticals

- 9.1. Market Analysis, Insights and Forecast - by Revenue Type

- 10. Latin America Semiconductor Silicon Intellectual Property Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Revenue Type

- 10.1.1. License

- 10.1.2. Royalty

- 10.1.3. Services

- 10.2. Market Analysis, Insights and Forecast - by IP Type

- 10.2.1. Processor IP

- 10.2.2. Wired and Wireless Interface IP

- 10.2.3. Other IP Types

- 10.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 10.3.1. Consumer Electronics

- 10.3.2. Computers and Peripherals

- 10.3.3. Automobile

- 10.3.4. Industrial

- 10.3.5. Other End-user Verticals

- 10.1. Market Analysis, Insights and Forecast - by Revenue Type

- 11. Middle East and Africa Semiconductor Silicon Intellectual Property Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Revenue Type

- 11.1.1. License

- 11.1.2. Royalty

- 11.1.3. Services

- 11.2. Market Analysis, Insights and Forecast - by IP Type

- 11.2.1. Processor IP

- 11.2.2. Wired and Wireless Interface IP

- 11.2.3. Other IP Types

- 11.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 11.3.1. Consumer Electronics

- 11.3.2. Computers and Peripherals

- 11.3.3. Automobile

- 11.3.4. Industrial

- 11.3.5. Other End-user Verticals

- 11.1. Market Analysis, Insights and Forecast - by Revenue Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Rambus Incorporated

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Achronix Semiconductor Corporation

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 CEVA Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 LTIMindtree Limited

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Imagination Technologies Ltd

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Fujitsu Ltd

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Andes Technology Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Faraday Technology Corporation

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 MIPS Tech LLC

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Digital Media Professionals

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Synopsys Inc

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Cadence Design Systems Inc

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 eMemory Technology Inc

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 MediaTek Inc

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 VeriSilicon Holdings Co Ltd

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 ARM Ltd (SoftBank )

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.1 Rambus Incorporated

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Semiconductor Silicon Intellectual Property Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Semiconductor Silicon Intellectual Property Industry Revenue (billion), by Revenue Type 2025 & 2033

- Figure 3: North America Semiconductor Silicon Intellectual Property Industry Revenue Share (%), by Revenue Type 2025 & 2033

- Figure 4: North America Semiconductor Silicon Intellectual Property Industry Revenue (billion), by IP Type 2025 & 2033

- Figure 5: North America Semiconductor Silicon Intellectual Property Industry Revenue Share (%), by IP Type 2025 & 2033

- Figure 6: North America Semiconductor Silicon Intellectual Property Industry Revenue (billion), by End-user Vertical 2025 & 2033

- Figure 7: North America Semiconductor Silicon Intellectual Property Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 8: North America Semiconductor Silicon Intellectual Property Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: North America Semiconductor Silicon Intellectual Property Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Semiconductor Silicon Intellectual Property Industry Revenue (billion), by Revenue Type 2025 & 2033

- Figure 11: Europe Semiconductor Silicon Intellectual Property Industry Revenue Share (%), by Revenue Type 2025 & 2033

- Figure 12: Europe Semiconductor Silicon Intellectual Property Industry Revenue (billion), by IP Type 2025 & 2033

- Figure 13: Europe Semiconductor Silicon Intellectual Property Industry Revenue Share (%), by IP Type 2025 & 2033

- Figure 14: Europe Semiconductor Silicon Intellectual Property Industry Revenue (billion), by End-user Vertical 2025 & 2033

- Figure 15: Europe Semiconductor Silicon Intellectual Property Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 16: Europe Semiconductor Silicon Intellectual Property Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: Europe Semiconductor Silicon Intellectual Property Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Semiconductor Silicon Intellectual Property Industry Revenue (billion), by Revenue Type 2025 & 2033

- Figure 19: Asia Semiconductor Silicon Intellectual Property Industry Revenue Share (%), by Revenue Type 2025 & 2033

- Figure 20: Asia Semiconductor Silicon Intellectual Property Industry Revenue (billion), by IP Type 2025 & 2033

- Figure 21: Asia Semiconductor Silicon Intellectual Property Industry Revenue Share (%), by IP Type 2025 & 2033

- Figure 22: Asia Semiconductor Silicon Intellectual Property Industry Revenue (billion), by End-user Vertical 2025 & 2033

- Figure 23: Asia Semiconductor Silicon Intellectual Property Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 24: Asia Semiconductor Silicon Intellectual Property Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Asia Semiconductor Silicon Intellectual Property Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Latin America Semiconductor Silicon Intellectual Property Industry Revenue (billion), by Revenue Type 2025 & 2033

- Figure 27: Latin America Semiconductor Silicon Intellectual Property Industry Revenue Share (%), by Revenue Type 2025 & 2033

- Figure 28: Latin America Semiconductor Silicon Intellectual Property Industry Revenue (billion), by IP Type 2025 & 2033

- Figure 29: Latin America Semiconductor Silicon Intellectual Property Industry Revenue Share (%), by IP Type 2025 & 2033

- Figure 30: Latin America Semiconductor Silicon Intellectual Property Industry Revenue (billion), by End-user Vertical 2025 & 2033

- Figure 31: Latin America Semiconductor Silicon Intellectual Property Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 32: Latin America Semiconductor Silicon Intellectual Property Industry Revenue (billion), by Country 2025 & 2033

- Figure 33: Latin America Semiconductor Silicon Intellectual Property Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Middle East and Africa Semiconductor Silicon Intellectual Property Industry Revenue (billion), by Revenue Type 2025 & 2033

- Figure 35: Middle East and Africa Semiconductor Silicon Intellectual Property Industry Revenue Share (%), by Revenue Type 2025 & 2033

- Figure 36: Middle East and Africa Semiconductor Silicon Intellectual Property Industry Revenue (billion), by IP Type 2025 & 2033

- Figure 37: Middle East and Africa Semiconductor Silicon Intellectual Property Industry Revenue Share (%), by IP Type 2025 & 2033

- Figure 38: Middle East and Africa Semiconductor Silicon Intellectual Property Industry Revenue (billion), by End-user Vertical 2025 & 2033

- Figure 39: Middle East and Africa Semiconductor Silicon Intellectual Property Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 40: Middle East and Africa Semiconductor Silicon Intellectual Property Industry Revenue (billion), by Country 2025 & 2033

- Figure 41: Middle East and Africa Semiconductor Silicon Intellectual Property Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Semiconductor Silicon Intellectual Property Industry Revenue billion Forecast, by Revenue Type 2020 & 2033

- Table 2: Global Semiconductor Silicon Intellectual Property Industry Revenue billion Forecast, by IP Type 2020 & 2033

- Table 3: Global Semiconductor Silicon Intellectual Property Industry Revenue billion Forecast, by End-user Vertical 2020 & 2033

- Table 4: Global Semiconductor Silicon Intellectual Property Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Global Semiconductor Silicon Intellectual Property Industry Revenue billion Forecast, by Revenue Type 2020 & 2033

- Table 6: Global Semiconductor Silicon Intellectual Property Industry Revenue billion Forecast, by IP Type 2020 & 2033

- Table 7: Global Semiconductor Silicon Intellectual Property Industry Revenue billion Forecast, by End-user Vertical 2020 & 2033

- Table 8: Global Semiconductor Silicon Intellectual Property Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: United States Semiconductor Silicon Intellectual Property Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Canada Semiconductor Silicon Intellectual Property Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Global Semiconductor Silicon Intellectual Property Industry Revenue billion Forecast, by Revenue Type 2020 & 2033

- Table 12: Global Semiconductor Silicon Intellectual Property Industry Revenue billion Forecast, by IP Type 2020 & 2033

- Table 13: Global Semiconductor Silicon Intellectual Property Industry Revenue billion Forecast, by End-user Vertical 2020 & 2033

- Table 14: Global Semiconductor Silicon Intellectual Property Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 15: United Kingdom Semiconductor Silicon Intellectual Property Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Germany Semiconductor Silicon Intellectual Property Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: France Semiconductor Silicon Intellectual Property Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Global Semiconductor Silicon Intellectual Property Industry Revenue billion Forecast, by Revenue Type 2020 & 2033

- Table 19: Global Semiconductor Silicon Intellectual Property Industry Revenue billion Forecast, by IP Type 2020 & 2033

- Table 20: Global Semiconductor Silicon Intellectual Property Industry Revenue billion Forecast, by End-user Vertical 2020 & 2033

- Table 21: Global Semiconductor Silicon Intellectual Property Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 22: China Semiconductor Silicon Intellectual Property Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Taiwan Semiconductor Silicon Intellectual Property Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Japan Semiconductor Silicon Intellectual Property Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: South Korea Semiconductor Silicon Intellectual Property Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: India Semiconductor Silicon Intellectual Property Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Australia and New Zealand Semiconductor Silicon Intellectual Property Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Semiconductor Silicon Intellectual Property Industry Revenue billion Forecast, by Revenue Type 2020 & 2033

- Table 29: Global Semiconductor Silicon Intellectual Property Industry Revenue billion Forecast, by IP Type 2020 & 2033

- Table 30: Global Semiconductor Silicon Intellectual Property Industry Revenue billion Forecast, by End-user Vertical 2020 & 2033

- Table 31: Global Semiconductor Silicon Intellectual Property Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 32: Global Semiconductor Silicon Intellectual Property Industry Revenue billion Forecast, by Revenue Type 2020 & 2033

- Table 33: Global Semiconductor Silicon Intellectual Property Industry Revenue billion Forecast, by IP Type 2020 & 2033

- Table 34: Global Semiconductor Silicon Intellectual Property Industry Revenue billion Forecast, by End-user Vertical 2020 & 2033

- Table 35: Global Semiconductor Silicon Intellectual Property Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Semiconductor Silicon Intellectual Property Industry?

The projected CAGR is approximately 13.9%.

2. Which companies are prominent players in the Semiconductor Silicon Intellectual Property Industry?

Key companies in the market include Rambus Incorporated, Achronix Semiconductor Corporation, CEVA Inc, LTIMindtree Limited, Imagination Technologies Ltd, Fujitsu Ltd, Andes Technology Corporation, Faraday Technology Corporation, MIPS Tech LLC, Digital Media Professionals, Synopsys Inc, Cadence Design Systems Inc, eMemory Technology Inc, MediaTek Inc, VeriSilicon Holdings Co Ltd, ARM Ltd (SoftBank ).

3. What are the main segments of the Semiconductor Silicon Intellectual Property Industry?

The market segments include Revenue Type, IP Type, End-user Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 7.9 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand for Connected Devices; Growing Demand for Modern SoC Designs.

6. What are the notable trends driving market growth?

Consumer Electronics to be the Largest End-user Vertical.

7. Are there any restraints impacting market growth?

IP Business Model and Economies of Scale.

8. Can you provide examples of recent developments in the market?

May 2023: CEVA Inc. announced the acquisition of the RealSpace 3D Spatial Audio business, technology, and patents from VisiSonicsCorporation. Based in Maryland, close to CEVA's sensor fusion R&D development center, the VisiSonicsspatial audio R&D team and software expand the Company's application software portfolio for embedded systems, bolstering CEVA's strong market position in wearables, where spatial audio is fast becoming a must-have component.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Semiconductor Silicon Intellectual Property Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Semiconductor Silicon Intellectual Property Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Semiconductor Silicon Intellectual Property Industry?

To stay informed about further developments, trends, and reports in the Semiconductor Silicon Intellectual Property Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence