Key Insights

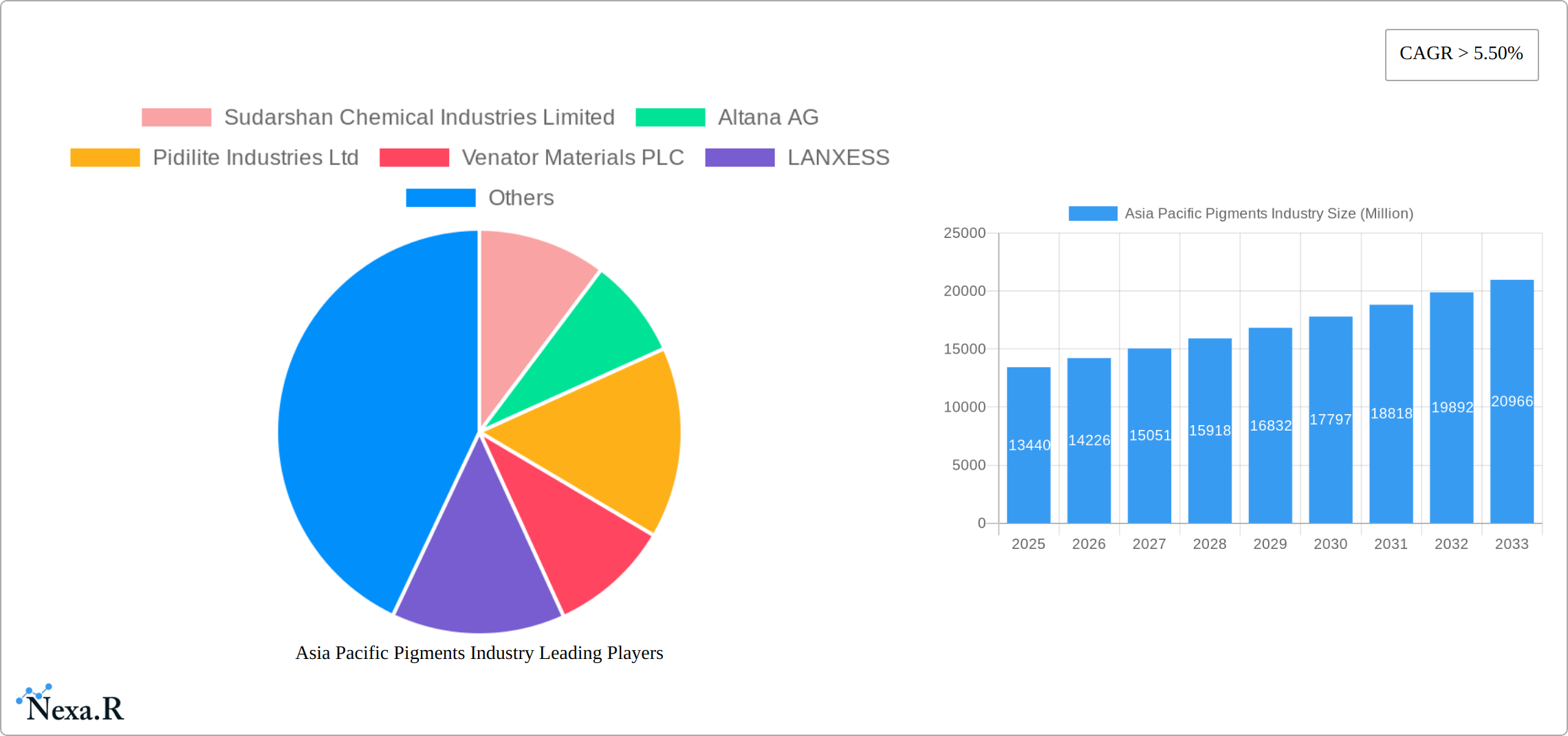

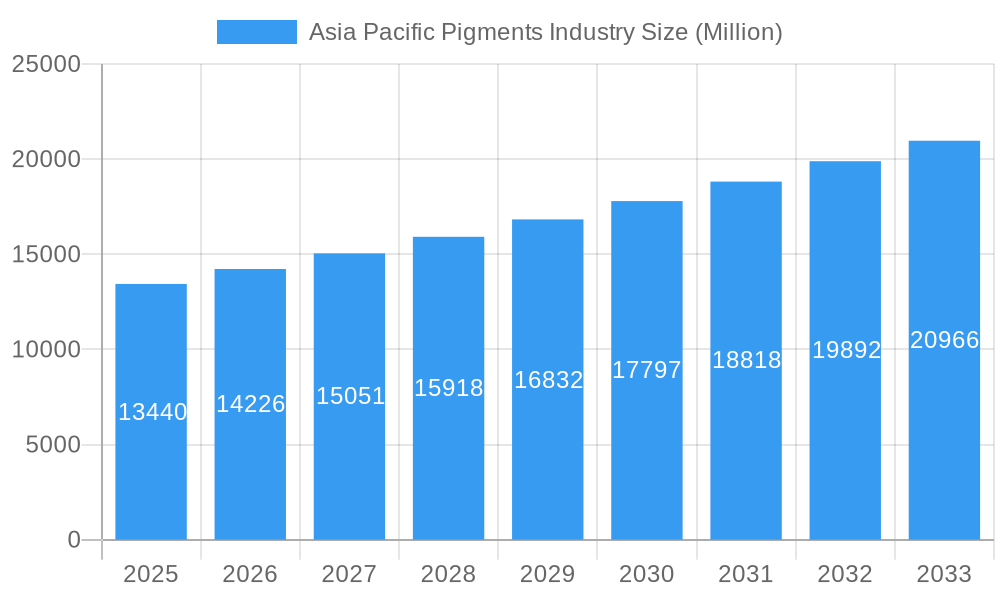

The Asia-Pacific pigments market, valued at $13.44 billion in 2025, is poised for robust growth, exhibiting a Compound Annual Growth Rate (CAGR) exceeding 5.50% from 2025 to 2033. This expansion is driven by several key factors. Firstly, the burgeoning construction and automotive industries in rapidly developing economies like China and India fuel significant demand for paints and coatings, the largest application segment for pigments. Secondly, the increasing popularity of vibrant and durable textiles, particularly in fashion and home furnishings, boosts the demand for high-quality organic and inorganic pigments. The rising adoption of advanced printing technologies further contributes to market growth, as pigments are crucial components in high-quality inks. Finally, the expanding plastics and packaging industries also contribute to the overall demand. However, the market faces challenges such as stringent environmental regulations concerning pigment production and disposal, potentially impacting production costs and hindering growth in certain segments. Furthermore, price volatility of raw materials, including minerals and chemicals, can affect profitability. Nevertheless, the ongoing innovation in pigment technology, focusing on environmentally friendly and high-performance products, coupled with the growth of emerging application sectors like cosmetics and electronics, are likely to offset these restraints and ensure sustained market growth throughout the forecast period.

Asia Pacific Pigments Industry Market Size (In Billion)

The market segmentation reveals a diverse landscape. Inorganic pigments, owing to their cost-effectiveness and wide applicability, hold a significant market share. However, the demand for specialty pigments, particularly organic pigments offering superior color properties and lightfastness, is experiencing rapid growth. Within applications, paints and coatings dominate the market, followed by textiles and printing inks. However, other application segments, such as plastics, leather, cosmetics, and electronics, are emerging as high-growth areas, fueled by increasing consumer demand for vibrant, durable, and aesthetically appealing products in diverse sectors. Key players such as Sudarshan Chemical Industries Limited, Altana AG, and BASF SE are investing heavily in research and development, focusing on sustainable and innovative pigment solutions to cater to the evolving market demands and maintain their competitive edge in this dynamic industry.

Asia Pacific Pigments Industry Company Market Share

Asia Pacific Pigments Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Asia Pacific pigments industry, covering market dynamics, growth trends, key players, and future outlook. With a detailed study period from 2019 to 2033, including a base year of 2025 and a forecast period from 2025 to 2033, this report is an essential resource for industry professionals, investors, and strategic decision-makers. The report utilizes a parent-child market approach, segmenting the market by product type and application, delivering granular insights for informed business strategies.

Asia Pacific Pigments Industry Market Dynamics & Structure

This section analyzes the competitive landscape, technological advancements, regulatory environment, and market trends shaping the Asia Pacific pigments industry. The market is characterized by a moderate level of concentration, with key players such as Sudarshan Chemical Industries Limited, Altana AG, Pidilite Industries Ltd, Venator Materials PLC, LANXESS, BASF SE, Wellton Chemical Co Ltd, The Chemours Company, Tronox Holdings PLC, and DIC CORPORATION holding significant market share. However, the presence of numerous smaller players contributes to a dynamic and competitive environment.

- Market Concentration: The top 10 players collectively hold approximately xx% of the market share (2024).

- Technological Innovation: Ongoing R&D efforts focus on developing sustainable and high-performance pigments, driving innovation in areas such as nanotechnology and bio-based pigments.

- Regulatory Framework: Stringent environmental regulations regarding VOC emissions and heavy metal content are shaping product development and manufacturing processes.

- Competitive Substitutes: Natural pigments and alternative colorants pose a competitive challenge, particularly in environmentally conscious applications.

- End-User Demographics: Growth is driven by increasing demand from the construction, automotive, and packaging industries, particularly in rapidly developing economies.

- M&A Trends: The industry has witnessed significant M&A activity in recent years, as evidenced by Cathay Industries' acquisition of Venator Materials PLC's iron oxide pigment business (November 2022) and Clariant's partial divestment of its pigments business (January 2022). These deals indicate a trend towards consolidation and expansion of global manufacturing footprints. The total value of M&A deals in the Asia Pacific pigments market from 2019 to 2024 was approximately xx Million.

Asia Pacific Pigments Industry Growth Trends & Insights

The Asia Pacific pigments market is experiencing dynamic expansion, fueled by sustained industrialization, rapid urbanization, and a growing consumer appetite for aesthetically superior products across diverse applications. The market size in 2024 was estimated at a significant figure, poised for continued robust growth with an anticipated Compound Annual Growth Rate (CAGR) of xx% during the period 2019-2024. Projections indicate the market will reach an impressive xx Million by 2033, propelled by the increasing adoption of pigments in sectors ranging from construction and automotive to packaging and textiles. Key to this growth are ongoing technological advancements, particularly in the development of high-performance specialty pigments and the rising demand for environmentally sustainable pigment alternatives. Evolving consumer preferences, with a pronounced emphasis on eco-friendly and sustainable product choices, are profoundly shaping the industry's direction. Our comprehensive report offers a detailed analysis of market penetration rates for various pigment types, providing critical insights into the adoption of different pigment technologies across a wide spectrum of applications.

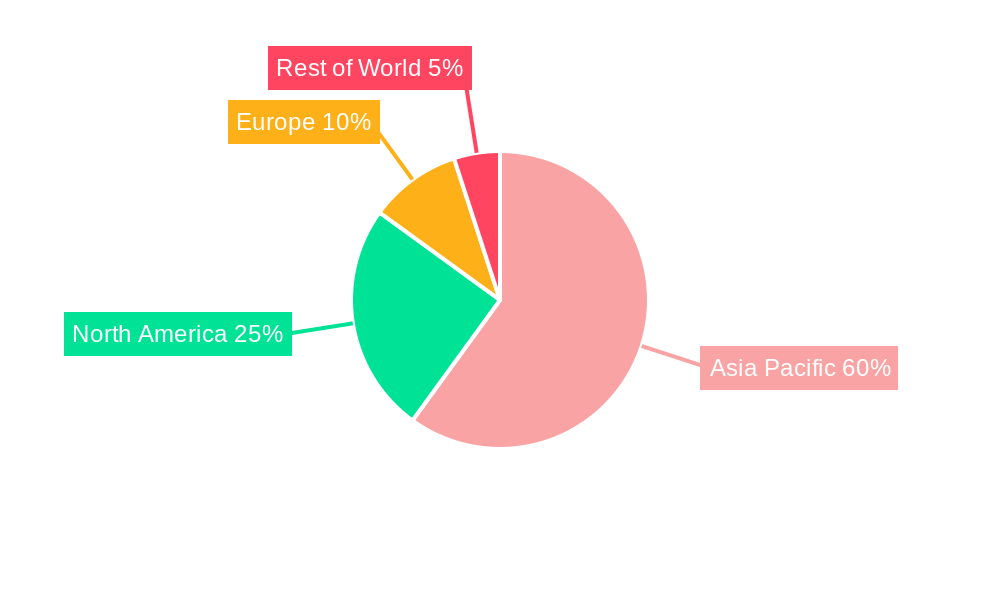

Dominant Regions, Countries, or Segments in Asia Pacific Pigments Industry

Within the expansive Asia Pacific landscape, China and India stand out as the dominant markets, collectively holding a substantial market share in 2024, with China accounting for approximately xx% and India for around xx%. This commanding position is underpinned by their robust economic growth trajectories, extensive infrastructure development initiatives, and formidable manufacturing capabilities. In terms of product segmentation, inorganic pigments continue to lead the market, representing approximately xx% of the total volume, closely followed by organic pigments at xx%. The paints and coatings segment remains the largest application area, demonstrating strong demand driven by the burgeoning construction and automotive industries across the region.

- Key Growth Enablers in China and India:

- Accelerated industrialization and ongoing urbanization driving demand for materials.

- Significant investments in large-scale infrastructure projects.

- Expansive growth and diversification of manufacturing sectors.

- Rising disposable incomes and increasing consumer spending power.

- Factors Contributing to Market Dominance:

- Vast and growing population bases.

- Supportive government policies and strategic industrial planning.

- Abundant availability of key raw material resources.

- Competitive cost structures in manufacturing operations.

Asia Pacific Pigments Industry Product Landscape

The Asia Pacific pigments market is characterized by a rich and diverse product portfolio. This includes a wide array of inorganic pigments such as iron oxides and titanium dioxide, alongside various organic pigments including azo and phthalocyanine types. Furthermore, the market features an increasing presence of specialty pigments, such as pearlescent and metallic pigments, catering to niche and high-value applications. Continuous innovation remains a cornerstone of the industry, with a strong focus on enhancing pigment performance, improving color vibrancy and durability, and developing advanced sustainable alternatives. Key advancements include the development of high-performance pigments that offer superior lightfastness, enhanced weatherability, and exceptional color strength, as well as the promising emergence of bio-based pigments that provide environmentally responsible solutions.

Key Drivers, Barriers & Challenges in Asia Pacific Pigments Industry

Key Drivers: The Asia Pacific pigments industry is propelled by several significant factors. Rapid industrialization, coupled with ongoing urbanization, is creating substantial demand across a multitude of end-use sectors, including construction, automotive, packaging, and textiles. Supportive government initiatives aimed at fostering infrastructure development and stimulating economic growth further contribute to the market's expansion. Moreover, continuous technological advancements in pigment synthesis and formulation are not only improving product performance but also unlocking new and innovative application possibilities, thereby driving market penetration.

Key Challenges: Despite the robust growth, the industry faces several challenges. Volatility in the prices of raw materials can impact profitability and supply chain stability. Increasingly stringent environmental regulations worldwide necessitate significant investment in compliance and sustainable practices. Intense competition, both from established domestic players and international manufacturers, places pressure on pricing and market share. Furthermore, the industry remains susceptible to supply chain disruptions and geopolitical uncertainties, which can affect the availability and cost of critical raw materials, posing an ongoing hurdle for sustained growth.

Emerging Opportunities in Asia Pacific Pigments Industry

Emerging opportunities lie in the development of sustainable and eco-friendly pigments, catering to the growing environmental consciousness among consumers. The expanding applications of pigments in high-growth sectors, such as electronics and cosmetics, present significant potential. Furthermore, tapping into untapped markets in Southeast Asia and other developing regions offers considerable growth prospects.

Growth Accelerators in the Asia Pacific Pigments Industry

Technological innovations, including the development of nanotechnology-based pigments and bio-based alternatives, will play a key role in accelerating market growth. Strategic partnerships and collaborations between pigment manufacturers and end-users will foster innovation and market penetration. Expansion into new geographic markets and the development of customized pigment solutions for specific applications will further propel market growth.

Key Players Shaping the Asia Pacific Pigments Industry Market

Notable Milestones in Asia Pacific Pigments Industry Sector

- November 2022: Cathay Industries acquired Venator Materials PLC's iron oxide pigment business, expanding its global manufacturing presence.

- January 2022: Clariant sold its pigments business to a consortium, retaining a 20% stake.

In-Depth Asia Pacific Pigments Industry Market Outlook

The Asia Pacific pigments market is poised for continued growth, driven by strong demand from key end-use sectors and ongoing technological advancements. Strategic investments in R&D, sustainable practices, and expansion into new markets will be crucial for success in this dynamic and competitive landscape. The focus on eco-friendly and high-performance pigments will be a key differentiator for companies seeking to capture significant market share in the years to come.

Asia Pacific Pigments Industry Segmentation

-

1. Product Type

-

1.1. Inorganic

- 1.1.1. Titanium Dioxide

- 1.1.2. Zinc Oxide

- 1.1.3. Other In

- 1.2. Organic

- 1.3. Specialty Pigments

- 1.4. Other Pr

-

1.1. Inorganic

-

2. Application

- 2.1. Paints and Coatings

- 2.2. Textiles

- 2.3. Printing Inks

- 2.4. Plastics

- 2.5. Leather

- 2.6. Other Ap

-

3. Geography

- 3.1. China

- 3.2. India

- 3.3. Japan

- 3.4. South Korea

- 3.5. Australia & New Zealand

- 3.6. Rest of Asia-Pacific

Asia Pacific Pigments Industry Segmentation By Geography

- 1. China

- 2. India

- 3. Japan

- 4. South Korea

- 5. Australia

- 6. Rest of Asia Pacific

Asia Pacific Pigments Industry Regional Market Share

Geographic Coverage of Asia Pacific Pigments Industry

Asia Pacific Pigments Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of > 5.50% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Inorganic

- 5.1.1.1. Titanium Dioxide

- 5.1.1.2. Zinc Oxide

- 5.1.1.3. Other In

- 5.1.2. Organic

- 5.1.3. Specialty Pigments

- 5.1.4. Other Pr

- 5.1.1. Inorganic

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Paints and Coatings

- 5.2.2. Textiles

- 5.2.3. Printing Inks

- 5.2.4. Plastics

- 5.2.5. Leather

- 5.2.6. Other Ap

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. China

- 5.3.2. India

- 5.3.3. Japan

- 5.3.4. South Korea

- 5.3.5. Australia & New Zealand

- 5.3.6. Rest of Asia-Pacific

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. China

- 5.4.2. India

- 5.4.3. Japan

- 5.4.4. South Korea

- 5.4.5. Australia

- 5.4.6. Rest of Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Asia Pacific Pigments Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Inorganic

- 6.1.1.1. Titanium Dioxide

- 6.1.1.2. Zinc Oxide

- 6.1.1.3. Other In

- 6.1.2. Organic

- 6.1.3. Specialty Pigments

- 6.1.4. Other Pr

- 6.1.1. Inorganic

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Paints and Coatings

- 6.2.2. Textiles

- 6.2.3. Printing Inks

- 6.2.4. Plastics

- 6.2.5. Leather

- 6.2.6. Other Ap

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. China

- 6.3.2. India

- 6.3.3. Japan

- 6.3.4. South Korea

- 6.3.5. Australia & New Zealand

- 6.3.6. Rest of Asia-Pacific

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. China Asia Pacific Pigments Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Inorganic

- 7.1.1.1. Titanium Dioxide

- 7.1.1.2. Zinc Oxide

- 7.1.1.3. Other In

- 7.1.2. Organic

- 7.1.3. Specialty Pigments

- 7.1.4. Other Pr

- 7.1.1. Inorganic

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Paints and Coatings

- 7.2.2. Textiles

- 7.2.3. Printing Inks

- 7.2.4. Plastics

- 7.2.5. Leather

- 7.2.6. Other Ap

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. China

- 7.3.2. India

- 7.3.3. Japan

- 7.3.4. South Korea

- 7.3.5. Australia & New Zealand

- 7.3.6. Rest of Asia-Pacific

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. India Asia Pacific Pigments Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Inorganic

- 8.1.1.1. Titanium Dioxide

- 8.1.1.2. Zinc Oxide

- 8.1.1.3. Other In

- 8.1.2. Organic

- 8.1.3. Specialty Pigments

- 8.1.4. Other Pr

- 8.1.1. Inorganic

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Paints and Coatings

- 8.2.2. Textiles

- 8.2.3. Printing Inks

- 8.2.4. Plastics

- 8.2.5. Leather

- 8.2.6. Other Ap

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. China

- 8.3.2. India

- 8.3.3. Japan

- 8.3.4. South Korea

- 8.3.5. Australia & New Zealand

- 8.3.6. Rest of Asia-Pacific

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Japan Asia Pacific Pigments Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Inorganic

- 9.1.1.1. Titanium Dioxide

- 9.1.1.2. Zinc Oxide

- 9.1.1.3. Other In

- 9.1.2. Organic

- 9.1.3. Specialty Pigments

- 9.1.4. Other Pr

- 9.1.1. Inorganic

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Paints and Coatings

- 9.2.2. Textiles

- 9.2.3. Printing Inks

- 9.2.4. Plastics

- 9.2.5. Leather

- 9.2.6. Other Ap

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. China

- 9.3.2. India

- 9.3.3. Japan

- 9.3.4. South Korea

- 9.3.5. Australia & New Zealand

- 9.3.6. Rest of Asia-Pacific

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. South Korea Asia Pacific Pigments Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Inorganic

- 10.1.1.1. Titanium Dioxide

- 10.1.1.2. Zinc Oxide

- 10.1.1.3. Other In

- 10.1.2. Organic

- 10.1.3. Specialty Pigments

- 10.1.4. Other Pr

- 10.1.1. Inorganic

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Paints and Coatings

- 10.2.2. Textiles

- 10.2.3. Printing Inks

- 10.2.4. Plastics

- 10.2.5. Leather

- 10.2.6. Other Ap

- 10.3. Market Analysis, Insights and Forecast - by Geography

- 10.3.1. China

- 10.3.2. India

- 10.3.3. Japan

- 10.3.4. South Korea

- 10.3.5. Australia & New Zealand

- 10.3.6. Rest of Asia-Pacific

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Australia Asia Pacific Pigments Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Inorganic

- 11.1.1.1. Titanium Dioxide

- 11.1.1.2. Zinc Oxide

- 11.1.1.3. Other In

- 11.1.2. Organic

- 11.1.3. Specialty Pigments

- 11.1.4. Other Pr

- 11.1.1. Inorganic

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Paints and Coatings

- 11.2.2. Textiles

- 11.2.3. Printing Inks

- 11.2.4. Plastics

- 11.2.5. Leather

- 11.2.6. Other Ap

- 11.3. Market Analysis, Insights and Forecast - by Geography

- 11.3.1. China

- 11.3.2. India

- 11.3.3. Japan

- 11.3.4. South Korea

- 11.3.5. Australia & New Zealand

- 11.3.6. Rest of Asia-Pacific

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Rest of Asia Pacific Asia Pacific Pigments Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Product Type

- 12.1.1. Inorganic

- 12.1.1.1. Titanium Dioxide

- 12.1.1.2. Zinc Oxide

- 12.1.1.3. Other In

- 12.1.2. Organic

- 12.1.3. Specialty Pigments

- 12.1.4. Other Pr

- 12.1.1. Inorganic

- 12.2. Market Analysis, Insights and Forecast - by Application

- 12.2.1. Paints and Coatings

- 12.2.2. Textiles

- 12.2.3. Printing Inks

- 12.2.4. Plastics

- 12.2.5. Leather

- 12.2.6. Other Ap

- 12.3. Market Analysis, Insights and Forecast - by Geography

- 12.3.1. China

- 12.3.2. India

- 12.3.3. Japan

- 12.3.4. South Korea

- 12.3.5. Australia & New Zealand

- 12.3.6. Rest of Asia-Pacific

- 12.1. Market Analysis, Insights and Forecast - by Product Type

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Sudarshan Chemical Industries Limited

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Altana AG

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Pidilite Industries Ltd

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Venator Materials PLC

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 LANXESS

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 BASF SE

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Wellton Chemical Co Ltd*List Not Exhaustive

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 The Chemours Company

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Tronox Holdings PLC

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 DIC CORPORATION

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.1 Sudarshan Chemical Industries Limited

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Asia Pacific Pigments Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Asia Pacific Pigments Industry Share (%) by Company 2025

List of Tables

- Table 1: Asia Pacific Pigments Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 2: Asia Pacific Pigments Industry Volume Kiloton Forecast, by Product Type 2020 & 2033

- Table 3: Asia Pacific Pigments Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 4: Asia Pacific Pigments Industry Volume Kiloton Forecast, by Application 2020 & 2033

- Table 5: Asia Pacific Pigments Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 6: Asia Pacific Pigments Industry Volume Kiloton Forecast, by Geography 2020 & 2033

- Table 7: Asia Pacific Pigments Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Asia Pacific Pigments Industry Volume Kiloton Forecast, by Region 2020 & 2033

- Table 9: Asia Pacific Pigments Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 10: Asia Pacific Pigments Industry Volume Kiloton Forecast, by Product Type 2020 & 2033

- Table 11: Asia Pacific Pigments Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 12: Asia Pacific Pigments Industry Volume Kiloton Forecast, by Application 2020 & 2033

- Table 13: Asia Pacific Pigments Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 14: Asia Pacific Pigments Industry Volume Kiloton Forecast, by Geography 2020 & 2033

- Table 15: Asia Pacific Pigments Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Asia Pacific Pigments Industry Volume Kiloton Forecast, by Country 2020 & 2033

- Table 17: Asia Pacific Pigments Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 18: Asia Pacific Pigments Industry Volume Kiloton Forecast, by Product Type 2020 & 2033

- Table 19: Asia Pacific Pigments Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 20: Asia Pacific Pigments Industry Volume Kiloton Forecast, by Application 2020 & 2033

- Table 21: Asia Pacific Pigments Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 22: Asia Pacific Pigments Industry Volume Kiloton Forecast, by Geography 2020 & 2033

- Table 23: Asia Pacific Pigments Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 24: Asia Pacific Pigments Industry Volume Kiloton Forecast, by Country 2020 & 2033

- Table 25: Asia Pacific Pigments Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 26: Asia Pacific Pigments Industry Volume Kiloton Forecast, by Product Type 2020 & 2033

- Table 27: Asia Pacific Pigments Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 28: Asia Pacific Pigments Industry Volume Kiloton Forecast, by Application 2020 & 2033

- Table 29: Asia Pacific Pigments Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 30: Asia Pacific Pigments Industry Volume Kiloton Forecast, by Geography 2020 & 2033

- Table 31: Asia Pacific Pigments Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 32: Asia Pacific Pigments Industry Volume Kiloton Forecast, by Country 2020 & 2033

- Table 33: Asia Pacific Pigments Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 34: Asia Pacific Pigments Industry Volume Kiloton Forecast, by Product Type 2020 & 2033

- Table 35: Asia Pacific Pigments Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 36: Asia Pacific Pigments Industry Volume Kiloton Forecast, by Application 2020 & 2033

- Table 37: Asia Pacific Pigments Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 38: Asia Pacific Pigments Industry Volume Kiloton Forecast, by Geography 2020 & 2033

- Table 39: Asia Pacific Pigments Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 40: Asia Pacific Pigments Industry Volume Kiloton Forecast, by Country 2020 & 2033

- Table 41: Asia Pacific Pigments Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 42: Asia Pacific Pigments Industry Volume Kiloton Forecast, by Product Type 2020 & 2033

- Table 43: Asia Pacific Pigments Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 44: Asia Pacific Pigments Industry Volume Kiloton Forecast, by Application 2020 & 2033

- Table 45: Asia Pacific Pigments Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 46: Asia Pacific Pigments Industry Volume Kiloton Forecast, by Geography 2020 & 2033

- Table 47: Asia Pacific Pigments Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 48: Asia Pacific Pigments Industry Volume Kiloton Forecast, by Country 2020 & 2033

- Table 49: Asia Pacific Pigments Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 50: Asia Pacific Pigments Industry Volume Kiloton Forecast, by Product Type 2020 & 2033

- Table 51: Asia Pacific Pigments Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 52: Asia Pacific Pigments Industry Volume Kiloton Forecast, by Application 2020 & 2033

- Table 53: Asia Pacific Pigments Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 54: Asia Pacific Pigments Industry Volume Kiloton Forecast, by Geography 2020 & 2033

- Table 55: Asia Pacific Pigments Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 56: Asia Pacific Pigments Industry Volume Kiloton Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia Pacific Pigments Industry?

The projected CAGR is approximately > 5.50%.

2. Which companies are prominent players in the Asia Pacific Pigments Industry?

Key companies in the market include Sudarshan Chemical Industries Limited, Altana AG, Pidilite Industries Ltd, Venator Materials PLC, LANXESS, BASF SE, Wellton Chemical Co Ltd*List Not Exhaustive, The Chemours Company, Tronox Holdings PLC, DIC CORPORATION.

3. What are the main segments of the Asia Pacific Pigments Industry?

The market segments include Product Type, Application, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 13.44 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand From the Paints and Coatings Industry; Rising Demand from the Textile Industry; The Increasing Demand for Pigments from Plastics Applications.

6. What are the notable trends driving market growth?

Increasing Demand from the Paints and Coatings Industry.

7. Are there any restraints impacting market growth?

Stringent Government Regulations on the usage of Pigments; High Cost Associated with the Organic Pigments.

8. Can you provide examples of recent developments in the market?

November 2022: Cathay Industries declared the successful acquisition of Venator Materials PLC's iron oxide pigment business. This strategic move is expected to facilitate the expansion of Cathay Industries' global manufacturing presence.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Kiloton.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia Pacific Pigments Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia Pacific Pigments Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia Pacific Pigments Industry?

To stay informed about further developments, trends, and reports in the Asia Pacific Pigments Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence