Key Insights

The Asia-Pacific small satellite market is poised for significant expansion, driven by escalating demand for Earth observation, communication, and navigation services. Key growth catalysts include rapid technological advancements, supportive government initiatives for space exploration, and a robust talent pool. The market is projected to reach $3.79 billion by 2025, with a Compound Annual Growth Rate (CAGR) of approximately 31%, indicating substantial growth from its base year of 2025. Leading economies such as China, Japan, India, and South Korea are spearheading investments in space infrastructure and small satellite technology. Market segmentation spans applications (communication, Earth observation, navigation), orbit classes (LEO, MEO, GEO), end-users (commercial, government, military), and propulsion technologies (electric, gas-based, liquid fuel). Low Earth Orbit (LEO) satellites are dominant for Earth observation and IoT, while electric propulsion enhances cost-effectiveness and mission longevity. Initial capital investment and regulatory hurdles may present challenges.

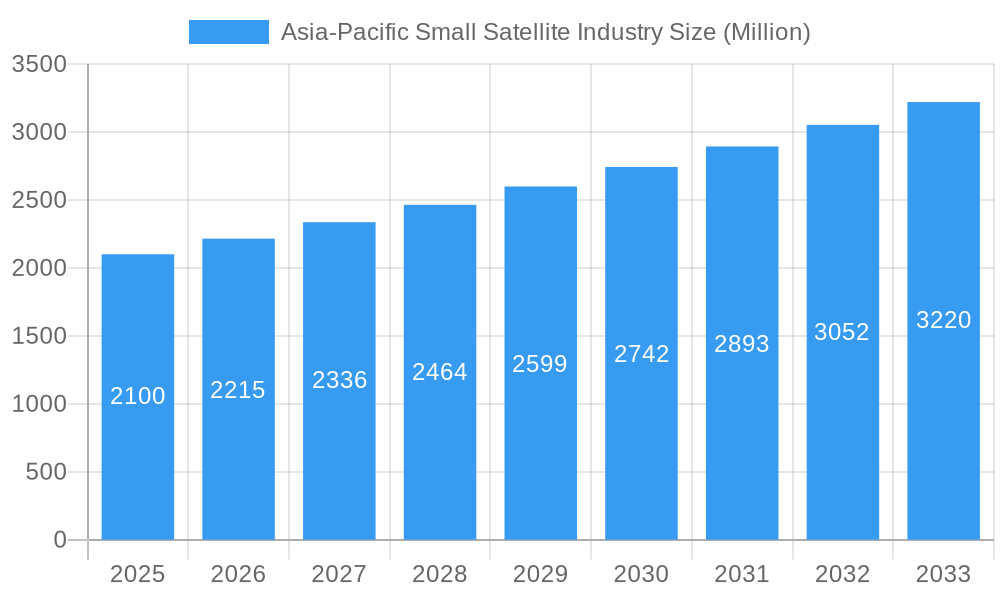

Asia-Pacific Small Satellite Industry Market Size (In Billion)

The Asia-Pacific small satellite market demonstrates a highly promising outlook through 2033. Ongoing technological innovations, especially in miniaturization and cost-effective launch solutions, will fuel further growth. Increased private sector engagement and public-private partnerships are anticipated to accelerate innovation. The expanding use of small satellites for environmental monitoring, disaster management, and precision agriculture will be pivotal drivers. While competition is intensifying, established players and government bodies will continue to shape the market. The region's strategic location and escalating investments in space technology position it to be a global leader in the small satellite industry.

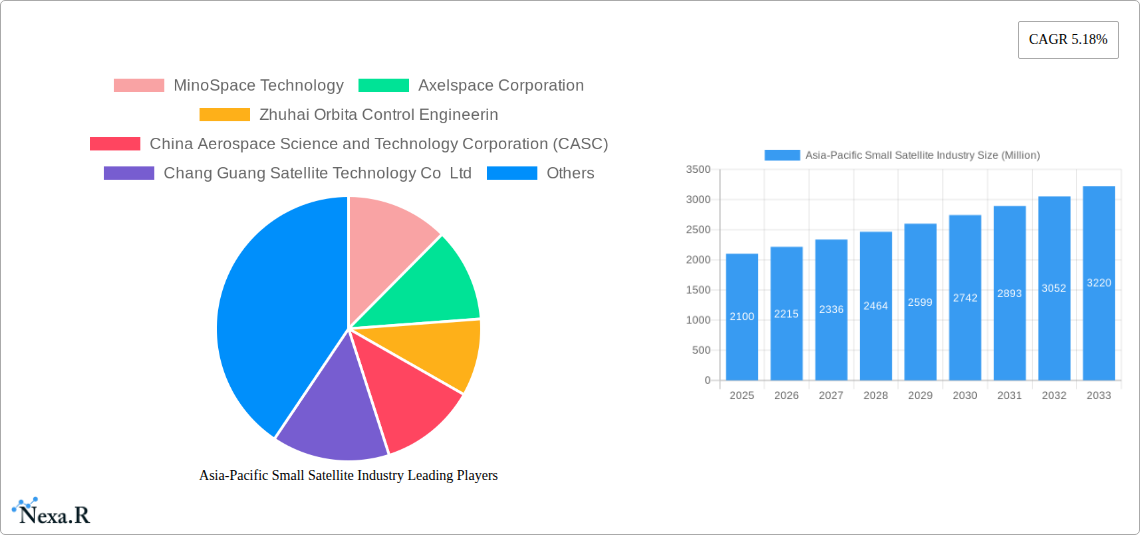

Asia-Pacific Small Satellite Industry Company Market Share

Asia-Pacific Small Satellite Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the burgeoning Asia-Pacific small satellite industry, covering the period from 2019 to 2033. It examines market dynamics, growth trends, key players, and future opportunities across various segments including communication, Earth observation, and navigation satellites. The report is a must-read for industry professionals, investors, and policymakers seeking to understand and capitalize on this rapidly expanding market.

Keywords: Asia-Pacific small satellite market, small satellite industry, satellite technology, LEO satellites, GEO satellites, MEO satellites, space technology, communication satellites, Earth observation satellites, navigation satellites, space observation, commercial satellites, military satellites, government satellites, MinoSpace Technology, Axelspace Corporation, Zhuhai Orbita Control Engineering, CASC, Chang Guang Satellite Technology, Spacety Aerospace, Guodian Gaoke, satellite launches, market size, market share, CAGR, market forecast, industry trends.

Asia-Pacific Small Satellite Industry Market Dynamics & Structure

The Asia-Pacific small satellite market is characterized by increasing market concentration among leading players like CASC and Guodian Gaoke, alongside the emergence of innovative companies such as MinoSpace Technology and Axelspace Corporation. Technological advancements, particularly in miniaturization and electric propulsion, are key drivers. Regulatory frameworks vary across the region, impacting market access and growth. Competition from larger satellite providers exists, but the cost-effectiveness and agility of small satellites provide a significant advantage. The market is witnessing a rise in M&A activity as larger companies seek to acquire smaller, innovative firms.

- Market Concentration: The top 5 players currently hold an estimated xx% market share, with CASC leading the pack.

- Technological Innovation: Miniaturization, CubeSats, and electric propulsion are driving cost reduction and increased deployment flexibility.

- Regulatory Landscape: Varied regulatory frameworks across countries present both opportunities and challenges for market entrants.

- Competitive Landscape: Larger satellite companies pose a competitive threat, but small satellites offer cost advantages and faster deployment times.

- M&A Activity: An estimated xx M&A deals occurred between 2019-2024, with a projected increase in the forecast period.

- End-User Demographics: Commercial applications are currently dominant, followed by government and military sectors.

Asia-Pacific Small Satellite Industry Growth Trends & Insights

The Asia-Pacific small satellite market exhibits strong growth, driven by increasing demand across various applications and technological advancements. The market size, valued at xx Million in 2025 (estimated), is projected to reach xx Million by 2033, exhibiting a CAGR of xx% during the forecast period (2025-2033). Adoption rates are significantly increasing, particularly in the commercial sector, driven by the decreasing cost of launching and operating small satellites. Technological disruptions such as the rise of CubeSats and advanced propulsion systems are fueling this growth. Consumer behavior shifts towards data-driven decision-making and the need for real-time information further accelerate market expansion. The historical period (2019-2024) saw significant growth, establishing a strong foundation for the projected future expansion.

Dominant Regions, Countries, or Segments in Asia-Pacific Small Satellite Industry

China is currently the dominant region in the Asia-Pacific small satellite market, driven by significant government investment in space exploration and the presence of major players such as CASC and Guodian Gaoke. The LEO segment holds the largest market share due to its cost-effectiveness and suitability for various applications. Within applications, Earth observation is a leading segment owing to its use in agriculture, urban planning, and disaster management. The commercial sector dominates the end-user market, reflecting the growing role of private companies in leveraging small satellite technology.

- Key Drivers:

- Government Initiatives: Significant investment in space research and development by nations like China.

- Technological Advancements: Cost reduction and improved performance of small satellites.

- Commercial Applications: Growing demand for data and services across various industries.

- Dominance Factors:

- Market Share: China’s significant market share reflects its strong government support and presence of major manufacturers.

- Growth Potential: The LEO segment and Earth Observation application boast significant growth potential.

Asia-Pacific Small Satellite Industry Product Landscape

The Asia-Pacific small satellite market showcases a diverse product landscape, featuring a range of satellite designs, payloads, and launch services. Innovations include miniaturized sensors, improved communication systems, and advanced propulsion technologies. These advancements enable enhanced data collection, faster data transmission, and longer operational lifetimes. Key selling propositions emphasize cost-effectiveness, adaptability to specific mission needs, and rapid deployment capabilities. Technological advancements in areas such as AI-powered image analysis and improved data processing capabilities further enhance the utility of these satellites.

Key Drivers, Barriers & Challenges in Asia-Pacific Small Satellite Industry

Key Drivers:

- Increasing demand for Earth observation data across diverse sectors.

- Government initiatives to promote domestic space industries.

- Technological advancements in miniaturization, propulsion, and data processing.

Key Challenges and Restraints:

- Supply chain disruptions impacting component availability and production costs.

- Regulatory hurdles and licensing processes for satellite launches and operations.

- Intense competition from established and emerging players. This results in pressure on pricing and margins. (Estimated impact: xx% reduction in average profit margins in 2024)

Emerging Opportunities in Asia-Pacific Small Satellite Industry

- New Applications: Expanding use cases in IoT, precision agriculture, and environmental monitoring.

- Untapped Markets: Reaching underserved regions through low-cost satellite communication services.

- Technological Advancements: Integration of AI and machine learning for enhanced data analysis.

Growth Accelerators in the Asia-Pacific Small Satellite Industry

Technological breakthroughs, particularly in areas like propulsion systems and data processing, are significantly accelerating market growth. Strategic partnerships between private companies and government agencies are fostering innovation and streamlining the development process. Market expansion strategies targeting new applications and underserved regions are opening up new avenues for growth.

Key Players Shaping the Asia-Pacific Small Satellite Industry Market

- MinoSpace Technology

- Axelspace Corporation

- Zhuhai Orbita Control Engineering

- China Aerospace Science and Technology Corporation (CASC)

- Chang Guang Satellite Technology Co Ltd

- Spacety Aerospace Co

- Guodian Gaoke

Notable Milestones in Asia-Pacific Small Satellite Industry Sector

- March 2022: CASC successfully launched the Tiankun-2 satellites into a low-Earth polar orbit using the Long March 6A rocket.

- March 2022: Guodian Gaoke's Tianqi 19 commercial data relay satellite was launched via the Long March 8 rocket.

- February 2022: Launch of 89 Jilin-1 optical imaging satellites (CASC), each weighing 30-45 kg.

In-Depth Asia-Pacific Small Satellite Industry Market Outlook

The Asia-Pacific small satellite market is poised for continued robust growth, driven by technological advancements, increasing demand, and supportive government policies. The focus on miniaturization, cost reduction, and enhanced capabilities will continue to attract new entrants and fuel innovation. Strategic partnerships and investments will be key factors in shaping the future of the industry. The market presents significant opportunities for companies to capitalize on the growing need for satellite-based data and services across various sectors.

Asia-Pacific Small Satellite Industry Segmentation

-

1. Application

- 1.1. Communication

- 1.2. Earth Observation

- 1.3. Navigation

- 1.4. Space Observation

- 1.5. Others

-

2. Orbit Class

- 2.1. GEO

- 2.2. LEO

- 2.3. MEO

-

3. End User

- 3.1. Commercial

- 3.2. Military & Government

- 3.3. Other

-

4. Propulsion Tech

- 4.1. Electric

- 4.2. Gas based

- 4.3. Liquid Fuel

Asia-Pacific Small Satellite Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. Japan

- 1.3. South Korea

- 1.4. India

- 1.5. Australia

- 1.6. New Zealand

- 1.7. Indonesia

- 1.8. Malaysia

- 1.9. Singapore

- 1.10. Thailand

- 1.11. Vietnam

- 1.12. Philippines

Asia-Pacific Small Satellite Industry Regional Market Share

Geographic Coverage of Asia-Pacific Small Satellite Industry

Asia-Pacific Small Satellite Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 31% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Communication

- 5.1.2. Earth Observation

- 5.1.3. Navigation

- 5.1.4. Space Observation

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Orbit Class

- 5.2.1. GEO

- 5.2.2. LEO

- 5.2.3. MEO

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Commercial

- 5.3.2. Military & Government

- 5.3.3. Other

- 5.4. Market Analysis, Insights and Forecast - by Propulsion Tech

- 5.4.1. Electric

- 5.4.2. Gas based

- 5.4.3. Liquid Fuel

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Asia-Pacific Small Satellite Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Communication

- 6.1.2. Earth Observation

- 6.1.3. Navigation

- 6.1.4. Space Observation

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Orbit Class

- 6.2.1. GEO

- 6.2.2. LEO

- 6.2.3. MEO

- 6.3. Market Analysis, Insights and Forecast - by End User

- 6.3.1. Commercial

- 6.3.2. Military & Government

- 6.3.3. Other

- 6.4. Market Analysis, Insights and Forecast - by Propulsion Tech

- 6.4.1. Electric

- 6.4.2. Gas based

- 6.4.3. Liquid Fuel

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 MinoSpace Technology

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Axelspace Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Zhuhai Orbita Control Engineerin

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 China Aerospace Science and Technology Corporation (CASC)

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Chang Guang Satellite Technology Co Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Spacety Aerospace Co

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Guodian Gaoke

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.1 MinoSpace Technology

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Asia-Pacific Small Satellite Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Asia-Pacific Small Satellite Industry Share (%) by Company 2025

List of Tables

- Table 1: Asia-Pacific Small Satellite Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Asia-Pacific Small Satellite Industry Revenue billion Forecast, by Orbit Class 2020 & 2033

- Table 3: Asia-Pacific Small Satellite Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 4: Asia-Pacific Small Satellite Industry Revenue billion Forecast, by Propulsion Tech 2020 & 2033

- Table 5: Asia-Pacific Small Satellite Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Asia-Pacific Small Satellite Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 7: Asia-Pacific Small Satellite Industry Revenue billion Forecast, by Orbit Class 2020 & 2033

- Table 8: Asia-Pacific Small Satellite Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 9: Asia-Pacific Small Satellite Industry Revenue billion Forecast, by Propulsion Tech 2020 & 2033

- Table 10: Asia-Pacific Small Satellite Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 11: China Asia-Pacific Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Japan Asia-Pacific Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: South Korea Asia-Pacific Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: India Asia-Pacific Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Australia Asia-Pacific Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: New Zealand Asia-Pacific Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Indonesia Asia-Pacific Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Malaysia Asia-Pacific Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Singapore Asia-Pacific Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Thailand Asia-Pacific Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Vietnam Asia-Pacific Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Philippines Asia-Pacific Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia-Pacific Small Satellite Industry?

The projected CAGR is approximately 31%.

2. Which companies are prominent players in the Asia-Pacific Small Satellite Industry?

Key companies in the market include MinoSpace Technology, Axelspace Corporation, Zhuhai Orbita Control Engineerin, China Aerospace Science and Technology Corporation (CASC), Chang Guang Satellite Technology Co Ltd, Spacety Aerospace Co, Guodian Gaoke.

3. What are the main segments of the Asia-Pacific Small Satellite Industry?

The market segments include Application, Orbit Class, End User, Propulsion Tech.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.79 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Satellites that are being launched into LEO is driving the market demand.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

March 2022: The China Aerospace Science and Technology Corporation successfully launched the Tiankun-2 satellites into a low-Earth polar orbit on the debut launch of the Long March 6A.March 2022: Guodian Gaoke's Tianqi 19 commercial data relay satellite was launched from the Long March 8 rocket.February 2022: A total of 89 Jilin-1 optical imaging satellites manufactured by CASC each weighing 30-45 kg were launched into orbit.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia-Pacific Small Satellite Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia-Pacific Small Satellite Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia-Pacific Small Satellite Industry?

To stay informed about further developments, trends, and reports in the Asia-Pacific Small Satellite Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence