Key Insights

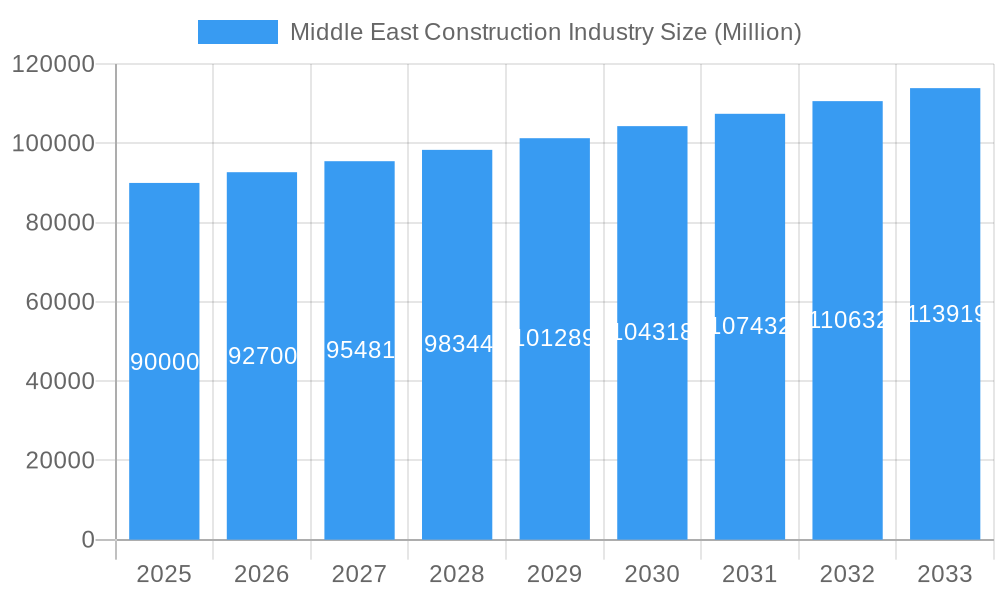

The Middle East construction industry, currently exhibiting a Compound Annual Growth Rate (CAGR) exceeding 3%, presents a robust market projected to reach significant value over the forecast period (2025-2033). Driven by large-scale infrastructure projects, burgeoning urbanization in key nations like Saudi Arabia and the UAE, and increasing government investments in housing and commercial developments, the sector shows strong potential. The segment breakdown reveals a diverse material landscape, with bitumen, rubber, metal, and polymer all playing significant roles. End-user demand is spread across residential, commercial, and industrial sectors, indicating a healthy and balanced market. While specific market size figures for 2025 are unavailable, extrapolating from the provided CAGR and considering typical industry growth patterns, a reasonable estimate for the 2025 market value could be in the range of $80 billion to $100 billion, given the scale of projects underway in the region. This range reflects the variability inherent in market forecasting. Challenges, however, exist, including fluctuating commodity prices, regional political instability in certain areas, and potential labor shortages which could restrain overall growth. Nevertheless, the long-term outlook remains positive, particularly with ongoing investments in mega-projects and diversification strategies across various sectors.

Middle East Construction Industry Market Size (In Billion)

The competitive landscape is populated by both international and regional players, indicating opportunities for both established companies and new entrants. Companies like Gautruss Pty Ltd, Corrugated Sheet Ltd, and Al Shafar Steel Engineering represent the breadth of materials and specialization within the industry. The analysis across different countries within the Middle East and Africa further reveals variations in market dynamics, with Saudi Arabia and the UAE expected to dominate owing to their considerable economic strength and ambitious infrastructure development plans. Ongoing monitoring of these factors—growth drivers, restraints, and competitive activities—is crucial for informed decision-making within this dynamic market. The continued focus on sustainable construction practices and technological advancements will also play a significant role in shaping the industry’s trajectory. The growth is expected to be fueled by the ongoing expansion of infrastructure, increased demand for housing, and government initiatives promoting economic diversification.

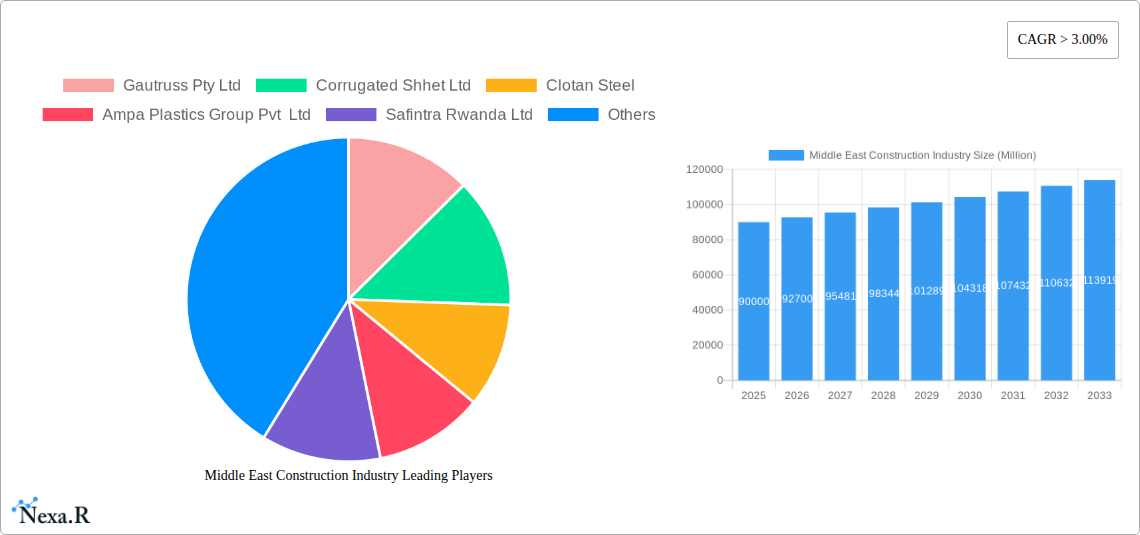

Middle East Construction Industry Company Market Share

Middle East Construction Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Middle East construction industry, encompassing market dynamics, growth trends, regional dominance, product landscape, challenges, opportunities, and key players. The report covers the period 2019-2033, with a base year of 2025 and a forecast period of 2025-2033. The study analyzes parent markets (construction materials) and child markets (residential, commercial, industrial construction) across key Middle Eastern and African countries. Market values are presented in millions of units.

Middle East Construction Industry Market Dynamics & Structure

The Middle East construction industry is characterized by a moderately concentrated market with significant players like Al Shafar Steel Engineering and Palram Industries Ltd. holding considerable market share (xx%). Technological innovation, particularly in sustainable building materials and construction techniques, is a key driver, although regulatory frameworks and bureaucratic hurdles (xx% delay reported in permitting processes) pose challenges. Competition from substitute materials, like sustainable alternatives to traditional concrete, is growing. The industry experiences fluctuating end-user demographics, influenced by population growth and urbanization. M&A activity remains robust, with an estimated xx M&A deals closed in the historical period (2019-2024), representing xx% increase compared to previous periods.

- Market Concentration: Moderately concentrated, with top 5 players holding xx% market share (2025).

- Technological Innovation: Focus on sustainable materials (e.g., recycled polymers, green concrete) and construction methods.

- Regulatory Frameworks: Bureaucratic processes and inconsistent regulations across countries.

- Competitive Product Substitutes: Growing competition from sustainable and cost-effective materials.

- End-User Demographics: Fluctuating demand driven by population growth and urbanization patterns.

- M&A Trends: Significant M&A activity, driven by consolidation and expansion strategies.

Middle East Construction Industry Growth Trends & Insights

The Middle East construction market witnessed significant growth during the historical period (2019-2024), expanding at a CAGR of xx%. This growth is attributed to large-scale infrastructure projects, increasing urbanization, and rising disposable incomes. The adoption rate of advanced technologies like BIM (Building Information Modeling) and prefabrication is gradually increasing, although at a slower pace than in more developed regions (xx% penetration rate in 2025). Consumer behavior shifts towards sustainable and energy-efficient buildings are impacting material choices. The forecast period (2025-2033) projects continued growth, albeit at a slightly moderated pace, driven by sustained government investment in infrastructure and ongoing mega-projects. The market size is projected to reach xx million in 2033.

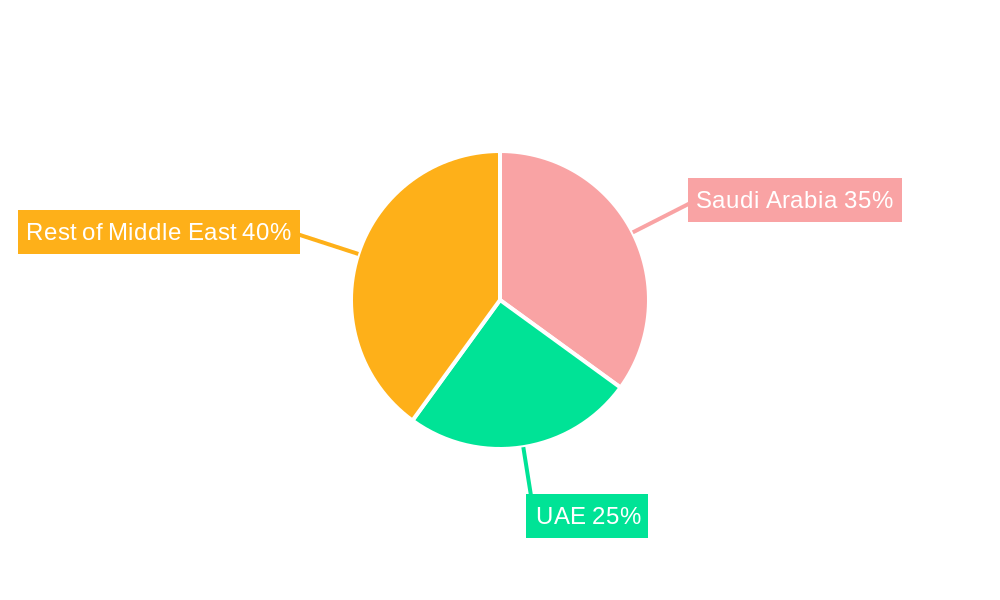

Dominant Regions, Countries, or Segments in Middle East Construction Industry

Saudi Arabia and the UAE remain the dominant markets, accounting for xx% of the total market size in 2025, driven by large-scale infrastructure developments (e.g., NEOM in Saudi Arabia) and substantial investments in real estate. Within segments, metal and polymer materials dominate due to their wide applicability in both residential and commercial construction, while the residential segment holds the largest market share (xx%).

- Key Drivers:

- Government Spending: Substantial investments in infrastructure and real estate development.

- Economic Growth: Positive economic outlook in leading countries driving construction activity.

- Urbanization: Rapid urbanization increasing demand for housing and commercial spaces.

- Dominance Factors:

- Market Size: Saudi Arabia and UAE are significantly larger markets compared to other countries.

- Government Initiatives: Supportive policies and regulations accelerating construction growth.

- Infrastructure Projects: Large-scale projects fueling demand for construction materials and services.

Middle East Construction Industry Product Landscape

The industry showcases a diverse product landscape encompassing various construction materials, ranging from traditional bitumen and rubber to advanced polymers and high-strength metals. Innovation focuses on sustainable, lightweight, and high-performance materials that reduce construction time and environmental impact. Products are increasingly tailored to specific project requirements, demonstrating improved performance metrics in terms of strength, durability, and energy efficiency.

Key Drivers, Barriers & Challenges in Middle East Construction Industry

Key Drivers: Government investments in infrastructure projects, increasing urbanization, growing tourism sector, and rising disposable incomes fuel market growth. Technological advancements in construction materials and techniques also boost efficiency and sustainability.

Challenges: Supply chain disruptions, especially during global events, cause significant price volatility and project delays. Regulatory complexities and bureaucratic hurdles increase project timelines and costs. Intense competition among contractors and material suppliers exerts downward pressure on profit margins.

Emerging Opportunities in Middle East Construction Industry

Untapped markets exist in the development of affordable housing, particularly for growing populations in rapidly urbanizing areas. Innovative construction technologies like 3D printing and modular construction offer opportunities for faster, cheaper, and more efficient construction. The growing demand for sustainable and green buildings creates significant opportunities for eco-friendly construction materials and methods.

Growth Accelerators in the Middle East Construction Industry

Technological advancements, particularly in BIM and prefabrication, enhance productivity and reduce construction time. Strategic partnerships between government agencies, contractors, and material suppliers drive collaboration and efficiency. Expansion into new markets within the Middle East and Africa unlocks untapped potential for growth.

Key Players Shaping the Middle East Construction Industry Market

- Gautruss Pty Ltd

- Corrugated Shhet Ltd

- Clotan Steel

- Ampa Plastics Group Pvt Ltd

- Safintra Rwanda Ltd

- Algoa Steel & Roofing

- Kirby International

- Al Shafar Steel Engineering

- Palram Industries Ltd

- Youngman

Notable Milestones in Middle East Construction Industry Sector

- 2021: Launch of NEOM mega-project in Saudi Arabia.

- 2022: Increased adoption of BIM technology in UAE construction projects.

- 2023: Several significant M&A deals in the construction materials sector.

In-Depth Middle East Construction Industry Market Outlook

The Middle East construction industry is poised for continued growth, driven by robust government investment, urbanization, and technological advancements. Strategic investments in sustainable infrastructure and the adoption of innovative construction methods will create significant opportunities for market expansion and enhanced profitability. The market's future potential hinges on addressing supply chain vulnerabilities and regulatory challenges.

Middle East Construction Industry Segmentation

-

1. Material

- 1.1. Bitumen

- 1.2. Rubber

- 1.3. Metal

- 1.4. Polymer

-

2. End User

- 2.1. Residential

- 2.2. Commercial

- 2.3. Industrial

Middle East Construction Industry Segmentation By Geography

-

1. Middle East

- 1.1. Saudi Arabia

- 1.2. United Arab Emirates

- 1.3. Israel

- 1.4. Qatar

- 1.5. Kuwait

- 1.6. Oman

- 1.7. Bahrain

- 1.8. Jordan

- 1.9. Lebanon

Middle East Construction Industry Regional Market Share

Geographic Coverage of Middle East Construction Industry

Middle East Construction Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.89% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material

- 5.1.1. Bitumen

- 5.1.2. Rubber

- 5.1.3. Metal

- 5.1.4. Polymer

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Residential

- 5.2.2. Commercial

- 5.2.3. Industrial

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Middle East

- 5.1. Market Analysis, Insights and Forecast - by Material

- 6. Middle East Construction Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material

- 6.1.1. Bitumen

- 6.1.2. Rubber

- 6.1.3. Metal

- 6.1.4. Polymer

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Residential

- 6.2.2. Commercial

- 6.2.3. Industrial

- 6.1. Market Analysis, Insights and Forecast - by Material

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Gautruss Pty Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Corrugated Shhet Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Clotan Steel

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Ampa Plastics Group Pvt Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Safintra Rwanda Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Algoa Steel & Roofing

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Kirby International**List Not Exhaustive

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Al Shafar Steel Engineering

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Palram Industries Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Youngman

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Gautruss Pty Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Middle East Construction Industry Revenue Breakdown (undefined, %) by Product 2025 & 2033

- Figure 2: Middle East Construction Industry Share (%) by Company 2025

List of Tables

- Table 1: Middle East Construction Industry Revenue undefined Forecast, by Material 2020 & 2033

- Table 2: Middle East Construction Industry Revenue undefined Forecast, by End User 2020 & 2033

- Table 3: Middle East Construction Industry Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Middle East Construction Industry Revenue undefined Forecast, by Material 2020 & 2033

- Table 5: Middle East Construction Industry Revenue undefined Forecast, by End User 2020 & 2033

- Table 6: Middle East Construction Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: Saudi Arabia Middle East Construction Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: United Arab Emirates Middle East Construction Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Israel Middle East Construction Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Qatar Middle East Construction Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 11: Kuwait Middle East Construction Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 12: Oman Middle East Construction Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 13: Bahrain Middle East Construction Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Jordan Middle East Construction Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Lebanon Middle East Construction Industry Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Middle East Construction Industry?

The projected CAGR is approximately 5.89%.

2. Which companies are prominent players in the Middle East Construction Industry?

Key companies in the market include Gautruss Pty Ltd, Corrugated Shhet Ltd, Clotan Steel, Ampa Plastics Group Pvt Ltd, Safintra Rwanda Ltd, Algoa Steel & Roofing, Kirby International**List Not Exhaustive, Al Shafar Steel Engineering, Palram Industries Ltd, Youngman.

3. What are the main segments of the Middle East Construction Industry?

The market segments include Material, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

4.; Rapid Urabanization4.; Increasing government investments.

6. What are the notable trends driving market growth?

Construction Activities Playing a Significant Role in the Construction Sheets Market.

7. Are there any restraints impacting market growth?

4.; Increasing cost of raw materials affecting the construction industry4.; Slowdown in economic growth affecting the market.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Middle East Construction Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Middle East Construction Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Middle East Construction Industry?

To stay informed about further developments, trends, and reports in the Middle East Construction Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence