Key Insights

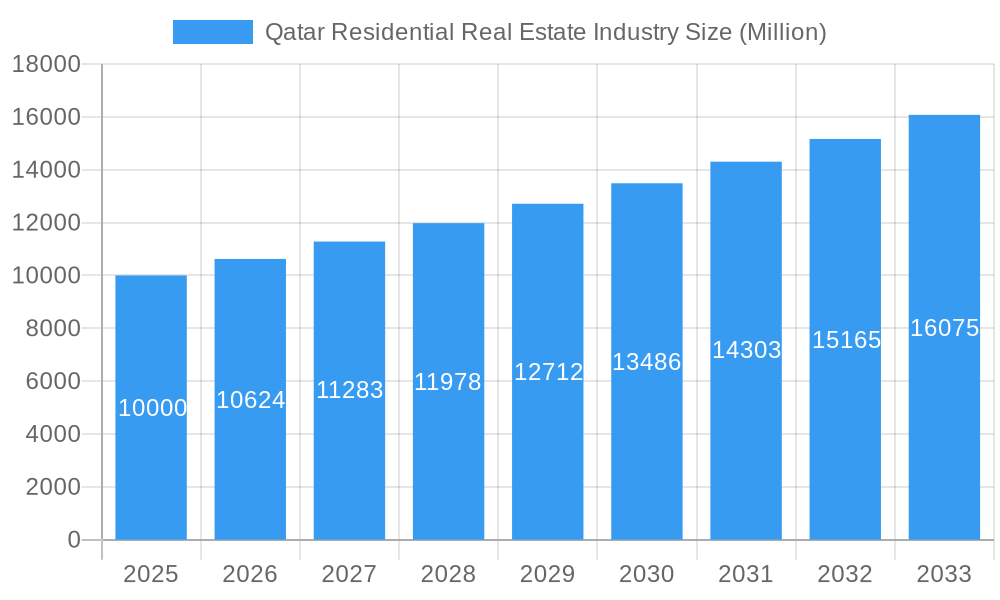

The Qatar residential real estate market is poised for significant expansion, projected to reach $7831.75 million by 2033, with a compound annual growth rate (CAGR) of 7.46% from the base year 2024. This robust growth trajectory is propelled by Qatar's dynamic economic landscape, characterized by substantial infrastructure investments, particularly following major international events, and ongoing economic diversification initiatives. These factors are attracting considerable foreign investment and stimulating domestic housing demand. Furthermore, a growing population, augmented by a substantial expatriate workforce, is driving the need for diverse housing options, from apartments and condominiums to villas and landed properties. Demand is most concentrated in key urban centers such as Doha, Al Wakrah, and Al Rayyan, owing to their well-established infrastructure and proximity to major employment hubs. However, the market may encounter challenges such as the volatility of global energy prices, which can influence investor confidence and governmental expenditure, and land availability constraints, especially in prime locations. Despite these hurdles, the long-term outlook remains optimistic, supported by government efforts to enhance housing affordability and the continuous development of integrated master-planned communities. The competitive environment is characterized by the presence of established developers like Barwa Real Estate and Qatari Diar, alongside agile emerging players, signifying a vibrant and evolving market.

Qatar Residential Real Estate Industry Market Size (In Billion)

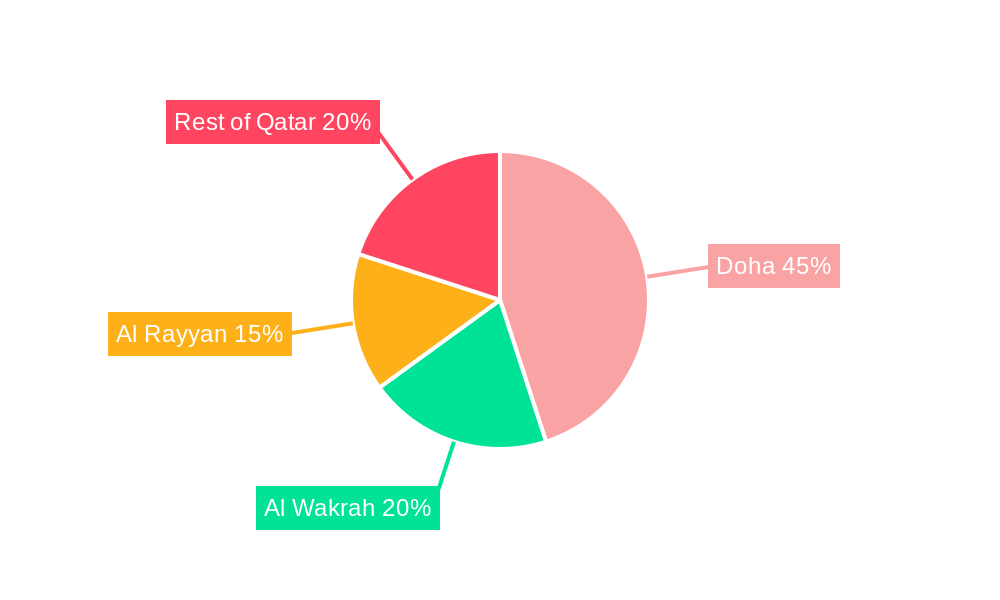

Market segmentation, based on property type (apartments/condominiums, villas/landed houses) and key geographical regions (Doha, Al Wakrah, Al Rayyan, and the remainder of Qatar), provides a detailed perspective on market dynamics. Apartments and condominiums typically serve a wider demographic and lifestyle spectrum, while villas and landed houses appeal to the premium segment, attracting high-net-worth individuals and families. The geographical distribution of demand mirrors the concentration of economic activity and infrastructural development in major metropolitan areas. Analyzing these segments facilitates the formulation of targeted investment strategies and a deeper comprehension of the specific requirements within various market niches. Future market expansion will likely be shaped by government housing policies, demographic shifts, and ongoing infrastructure development across Qatar.

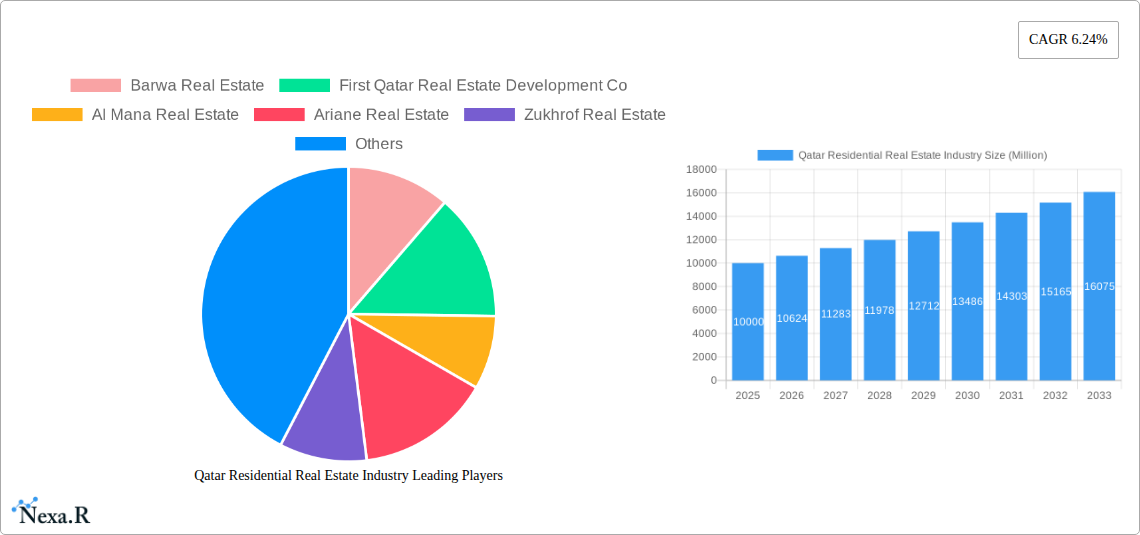

Qatar Residential Real Estate Industry Company Market Share

Qatar Residential Real Estate Industry: 2019-2033 Market Report

This comprehensive report provides an in-depth analysis of the Qatar residential real estate market, covering the period 2019-2033. With a focus on key segments – Apartments & Condominiums and Villas & Landed Houses – across major cities like Doha, Al Wakrah, Al Rayyan, and the Rest of Qatar, this study offers invaluable insights for investors, developers, and industry professionals. The report leverages extensive data analysis to provide a detailed forecast, identifying growth drivers, challenges, and emerging opportunities within this dynamic market. The base year for this report is 2025, with estimations for 2025 and forecasts spanning 2025-2033. The historical period analyzed is 2019-2024.

Keywords: Qatar Real Estate, Residential Real Estate Qatar, Doha Real Estate, Al Wakrah Real Estate, Al Rayyan Real Estate, Apartments Qatar, Villas Qatar, Condominiums Qatar, Real Estate Market Qatar, Qatar Property Market, Real Estate Investment Qatar, Barwa Real Estate, First Qatar, Al Mana Real Estate, Qatari Diar

Qatar Residential Real Estate Industry Market Dynamics & Structure

The Qatari residential real estate market, valued at xx million in 2024, exhibits a moderately concentrated structure with several prominent players. Market leadership is contested amongst established developers like Barwa Real Estate and Qatari Diar Real Estate Company, alongside emerging players such as Mazaya Real Estate Development and Ezdan Holding Group. Technological innovation, while present, faces barriers including high initial investment costs and regulatory complexities. The regulatory framework, while generally supportive of development, is subject to periodic revisions influencing project timelines and investment decisions. Competition is primarily driven by product differentiation, location, and pricing strategies. Substitutes are limited, mostly encompassing rental markets.

- Market Concentration: Moderately concentrated, with top 5 players holding approximately xx% market share (2024).

- Technological Innovation: Smart home technology adoption is gradually increasing, but faces high implementation costs.

- Regulatory Framework: Supportive but subject to changes impacting project approvals and timelines.

- Competitive Substitutes: Limited, primarily rental properties.

- End-User Demographics: Growing expatriate population and a rising middle class are key drivers of demand.

- M&A Trends: A moderate number of M&A deals were observed between 2019-2024, averaging xx deals per year. (Value of deals: xx Million).

Qatar Residential Real Estate Industry Growth Trends & Insights

The Qatari residential real estate market experienced a period of moderate growth between 2019 and 2024, driven by factors including infrastructure development, government initiatives, and population growth. The market is projected to experience a compound annual growth rate (CAGR) of xx% during the forecast period (2025-2033), reaching an estimated value of xx million by 2033. This growth trajectory is underpinned by ongoing infrastructure projects linked to the FIFA World Cup 2022 legacy and sustained government investment in housing initiatives. Consumer behavior reflects a preference for high-quality, sustainable developments, with increasing demand for smart home features and convenient locations. Technological disruptions, such as the use of PropTech solutions, are starting to reshape the market, enhancing efficiency and transparency in transactions and property management.

Dominant Regions, Countries, or Segments in Qatar Residential Real Estate Industry

Doha, the capital city, remains the dominant region, capturing approximately xx% of the total market share in 2024. Its strong economic activity, high concentration of employment opportunities, and established infrastructure contribute to high demand. The Apartments and Condominiums segment currently represents a larger portion of the market compared to Villas and Landed Houses, driven by a greater affordability and preference for urban living.

Key Drivers for Doha:

- Strong economic activity and high employment rates.

- Well-developed infrastructure and amenities.

- High concentration of expatriates and a growing middle class.

Key Drivers for Apartments & Condominiums:

- Affordability compared to villas.

- Preference for urban living and proximity to amenities.

- Growing demand from young professionals and families.

Qatar Residential Real Estate Industry Product Landscape

The product landscape is characterized by a wide range of residential properties, catering to diverse needs and preferences. Innovations focus on sustainable building practices, smart home technologies, and enhanced amenities to provide added value and improve residents’ quality of life. Developments increasingly incorporate green building standards, energy-efficient designs, and smart home features, attracting environmentally conscious buyers. Unique selling propositions include prime locations, luxury finishes, and state-of-the-art amenities.

Key Drivers, Barriers & Challenges in Qatar Residential Real Estate Industry

Key Drivers:

- Government initiatives promoting real estate development.

- Increasing population and urbanization.

- Infrastructure development and improvements.

- Foreign investment and tourism growth.

Challenges:

- High construction costs and material prices.

- Regulatory complexities and bureaucratic hurdles.

- Dependence on expatriate workforce affecting labor costs.

- Competition from existing and new developers. This pressure impacts profit margins and pushes developers to innovate.

Emerging Opportunities in Qatar Residential Real Estate Industry

Emerging opportunities include the expansion of affordable housing options to cater to a growing segment of the population, the increasing demand for sustainable and green buildings, and the development of smart city initiatives that incorporate advanced technologies and infrastructure. The growth of PropTech platforms offers potential for streamlining transactions and improving transparency. The development of integrated communities offering comprehensive amenities will also drive future growth.

Growth Accelerators in the Qatar Residential Real Estate Industry

Long-term growth is further propelled by sustained government investment in infrastructure and housing, ongoing economic diversification efforts, and the potential for increased tourism. Strategic partnerships between local and international developers will facilitate knowledge transfer and attract further investment. Technological advancements, such as the application of Building Information Modelling (BIM) and sustainable construction techniques, will enhance efficiency and improve the overall quality of projects.

Key Players Shaping the Qatar Residential Real Estate Industry Market

- Barwa Real Estate

- First Qatar Real Estate Development Co

- Al Mana Real Estate

- Ariane Real Estate

- Zukhrof Real Estate

- Mazaya Real Estate Development

- United Development Company

- Les Roses Real Estate

- Qatari Diar Real Estate Company

- Mirage International Property Consultants

- Ezdan Holding Group

- Al Asmakh Real Estate

Notable Milestones in Qatar Residential Real Estate Industry Sector

- 2022 (Nov): Completion of several major residential projects in connection with the FIFA World Cup.

- 2021 (Dec): Launch of a new government initiative to support affordable housing development.

- 2020 (Mar): Implementation of new building codes focused on sustainability.

- 2019 (June): Significant increase in foreign investment in the real estate sector.

In-Depth Qatar Residential Real Estate Industry Market Outlook

The Qatar residential real estate market presents significant long-term growth potential, driven by continued government support, infrastructure development, and a growing population. Strategic opportunities exist in sustainable development, affordable housing, and technological integration. The market’s future success will depend on adapting to evolving consumer preferences, embracing technological innovations, and navigating regulatory changes effectively. The market's long-term growth outlook is positive, with significant opportunities for investors and developers who can effectively leverage these trends.

Qatar Residential Real Estate Industry Segmentation

-

1. Type

- 1.1. Apartments & Condominiums

- 1.2. Villas & Landed Houses

Qatar Residential Real Estate Industry Segmentation By Geography

- 1. Qatar

Qatar Residential Real Estate Industry Regional Market Share

Geographic Coverage of Qatar Residential Real Estate Industry

Qatar Residential Real Estate Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.46% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Apartments & Condominiums

- 5.1.2. Villas & Landed Houses

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Qatar

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Qatar Residential Real Estate Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Apartments & Condominiums

- 6.1.2. Villas & Landed Houses

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Barwa Real Estate

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 First Qatar Real Estate Development Co

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Al Mana Real Estate

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Ariane Real Estate

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Zukhrof Real Estate

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Mazaya Real Estate Development

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 United Development Company

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Les Roses Real Estate

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Qatari Diar Real Estate Company

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Mirage International Property Consultants**List Not Exhaustive

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Ezdan Holding Group

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Al Asmakh Real Estate

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 Barwa Real Estate

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Qatar Residential Real Estate Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Qatar Residential Real Estate Industry Share (%) by Company 2025

List of Tables

- Table 1: Qatar Residential Real Estate Industry Revenue million Forecast, by Type 2020 & 2033

- Table 2: Qatar Residential Real Estate Industry Revenue million Forecast, by Region 2020 & 2033

- Table 3: Qatar Residential Real Estate Industry Revenue million Forecast, by Type 2020 & 2033

- Table 4: Qatar Residential Real Estate Industry Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Qatar Residential Real Estate Industry?

The projected CAGR is approximately 7.46%.

2. Which companies are prominent players in the Qatar Residential Real Estate Industry?

Key companies in the market include Barwa Real Estate, First Qatar Real Estate Development Co, Al Mana Real Estate, Ariane Real Estate, Zukhrof Real Estate, Mazaya Real Estate Development, United Development Company, Les Roses Real Estate, Qatari Diar Real Estate Company, Mirage International Property Consultants**List Not Exhaustive, Ezdan Holding Group, Al Asmakh Real Estate.

3. What are the main segments of the Qatar Residential Real Estate Industry?

The market segments include Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 7831.75 million as of 2022.

5. What are some drivers contributing to market growth?

4.; Rapid Urabanization4.; Increasing government investments.

6. What are the notable trends driving market growth?

Qatar’s Housing Market is Gradually Improving.

7. Are there any restraints impacting market growth?

4.; Increasing cost of raw materials affecting the construction industry4.; Slowdown in economic growth affecting the market.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Qatar Residential Real Estate Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Qatar Residential Real Estate Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Qatar Residential Real Estate Industry?

To stay informed about further developments, trends, and reports in the Qatar Residential Real Estate Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence