Key Insights

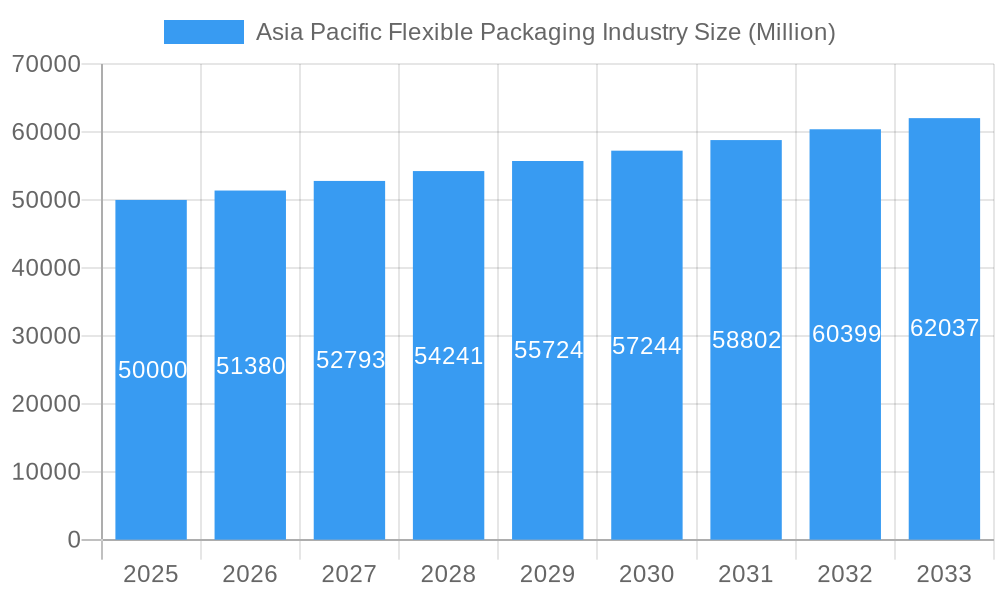

The Asia Pacific flexible packaging market, valued at approximately $XX million in 2025 (assuming a logical extrapolation from the provided data and considering the region's significant contribution to global flexible packaging), is projected to exhibit robust growth, driven by several key factors. The region's burgeoning food and beverage industry, coupled with a rising demand for convenient and shelf-stable products, significantly fuels market expansion. Furthermore, the increasing adoption of e-commerce and online grocery shopping necessitates efficient and protective packaging solutions, bolstering demand for flexible packaging options like pouches and bags. Growth is further propelled by advancements in flexible packaging materials, such as sustainable and recyclable options, catering to the growing environmental awareness among consumers and businesses. While factors like fluctuating raw material prices and stringent regulations may pose some challenges, the overall market outlook remains positive, with a projected Compound Annual Growth Rate (CAGR) of 2.76% from 2025 to 2033.

Asia Pacific Flexible Packaging Industry Market Size (In Billion)

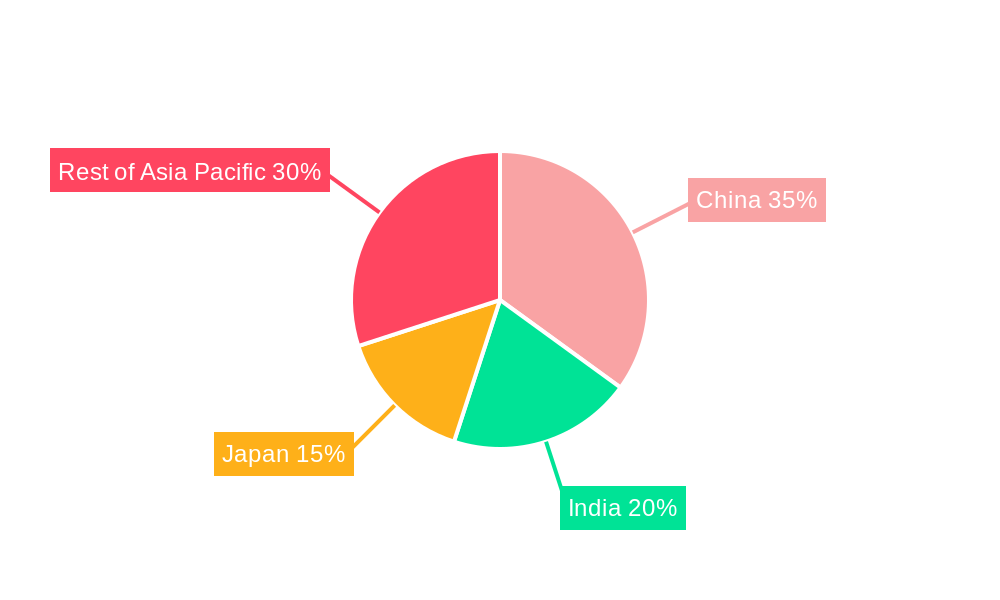

Within the Asia Pacific region, countries like China, India, and Japan are key drivers, representing a significant portion of the market share. China, in particular, benefits from its vast manufacturing base and extensive consumer population. India's expanding middle class and rising disposable incomes are also contributing to increased demand. Japan's focus on advanced packaging technologies and sophisticated consumer preferences further contribute to the regional growth. Segmentation within the market reveals a strong preference for plastic packaging due to its cost-effectiveness and versatility, though the demand for eco-friendly alternatives, such as paper and compostable materials, is steadily increasing. The food and beverage sector dominates the end-user vertical, followed by the pharmaceutical and medical, and household and personal care segments. This indicates a diverse range of applications driving market growth across various industry sectors in the Asia Pacific region.

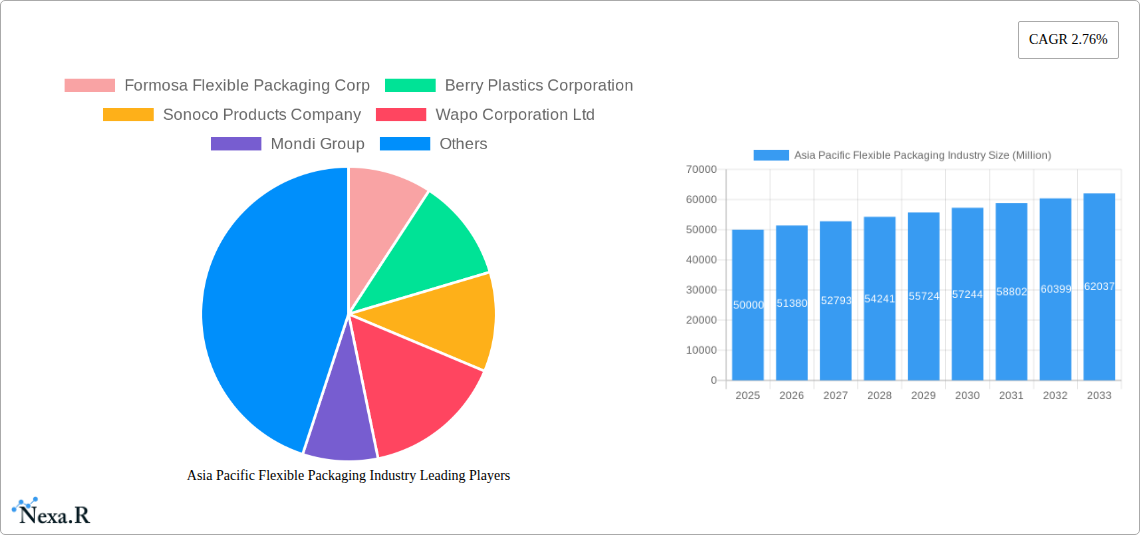

Asia Pacific Flexible Packaging Industry Company Market Share

Asia Pacific Flexible Packaging Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Asia Pacific flexible packaging industry, covering market dynamics, growth trends, key players, and future outlook. The study period spans from 2019 to 2033, with 2025 serving as the base and estimated year. The report delves into various segments including material type (plastic, paper, aluminum/composites), end-user verticals (food, beverages, pharmaceutical & medical, household & personal care, others), country-specific analyses (China, India, Japan, Australia, Rest of Asia Pacific), and packaging types (pouches, bags, wraps, others). Market values are presented in million units.

Asia Pacific Flexible Packaging Industry Market Dynamics & Structure

The Asia Pacific flexible packaging market is characterized by a dynamic and moderately concentrated landscape. A few dominant global and regional players command a significant portion of the market share, fostering a competitive environment that also includes a robust network of smaller, agile, and specialized local manufacturers. This interplay drives innovation and caters to diverse regional needs. Key market enablers include escalating consumer demand for sustainable, convenient, and high-performance packaging solutions. Simultaneously, a tightening regulatory framework across the region, particularly concerning material recyclability, the reduction of single-use plastics, and stringent food safety standards, is fundamentally influencing packaging material choices and manufacturing processes. The industry is witnessing continuous strategic mergers and acquisitions (M&A) activity, indicative of consolidation trends, the pursuit of synergistic growth, and the expansion of key players into new markets and capabilities. While flexible packaging offers distinct advantages, it faces ongoing competition from evolving rigid packaging alternatives, necessitating continuous differentiation and value proposition enhancement.

- Market Concentration: The top 5 players are estimated to hold approximately 45-55% of the market share in 2025.

- Technological Innovation: A pronounced focus on developing and adopting sustainable materials, including advanced bioplastics, certified recycled content, and innovative barrier technologies. Furthermore, significant advancements in high-speed digital printing and intelligent packaging solutions are gaining traction.

- Regulatory Landscape: Increasingly stringent regulations worldwide, with a significant regional push towards enhanced plastic waste management, extended producer responsibility (EPR) schemes, and harmonized food safety standards are shaping industry practices.

- M&A Activity: Approximately 30-40 significant M&A deals were recorded between 2019 and 2024. Projections suggest an increase to 45-55 deals between 2025 and 2033, driven by vertical integration and technology acquisition strategies.

- Competitive Substitutes: The ongoing innovation and adoption of advanced rigid packaging solutions (e.g., advanced plastics, composites, and glass) present a moderate but evolving threat, requiring flexible packaging to continuously demonstrate its superior value proposition in terms of performance and sustainability.

- Innovation Barriers: Substantial investment in research and development for novel sustainable materials, coupled with the inherent challenges in scaling up the production of these materials to meet mass-market demand and ensuring comparable performance characteristics to traditional plastics, remain significant hurdles.

Asia Pacific Flexible Packaging Industry Growth Trends & Insights

The Asia Pacific flexible packaging market has experienced robust and sustained growth between 2019 and 2024. This expansion was primarily fueled by a confluence of factors: rising disposable incomes and a burgeoning middle class leading to increased consumer spending, evolving consumer preferences towards convenience and visually appealing product presentation, and the escalating demand for protective and extended-shelf-life packaging across a diverse array of end-use sectors including food & beverage, pharmaceuticals, personal care, and industrial goods. The market is poised to maintain this impressive growth trajectory throughout the forecast period (2025-2033), with an anticipated Compound Annual Growth Rate (CAGR) of approximately 6.5% to 7.5%. Technological disruptions are acting as significant catalysts, with the widespread adoption of advanced digital printing enabling greater customization and faster turnaround times, alongside the emergence of sophisticated smart packaging solutions that offer enhanced traceability and consumer engagement. Crucially, a powerful consumer and regulatory-driven shift towards sustainability and eco-friendly packaging is profoundly influencing market growth. The market penetration of demonstrably sustainable packaging options, encompassing those with recycled content, improved recyclability, or compostability, is projected to reach a significant milestone of 30-40% by 2033.

Dominant Regions, Countries, or Segments in Asia Pacific Flexible Packaging Industry

China and India dominate the Asia Pacific flexible packaging market, driven by their large populations, expanding consumer base, and robust manufacturing sectors. Within material segments, plastics currently hold the largest market share, but paper and aluminum/composites are gaining traction due to the increasing emphasis on sustainability. The food and beverage sector represents the largest end-user vertical.

- Leading Countries: China and India account for approximately xx% of the total market value.

- Dominant Material: Plastic packaging accounts for approximately xx% of the market.

- Largest End-User Vertical: Food and beverage industry holds the highest demand.

- Key Growth Drivers: Increasing demand from e-commerce, rising consumer spending, and government support for manufacturing and infrastructure development.

Asia Pacific Flexible Packaging Industry Product Landscape

The Asia Pacific flexible packaging market showcases a diverse product landscape, including pouches, bags, wraps, and other specialized packaging formats. Product innovation focuses on enhancing barrier properties, improving shelf life, and incorporating sustainable materials. Stand-up pouches with resealable features are gaining popularity, while advancements in printing technologies allow for more visually appealing and informative packaging designs. Unique selling propositions include customized designs, improved product protection, and incorporation of sustainable materials, including bioplastics and recycled content.

Key Drivers, Barriers & Challenges in Asia Pacific Flexible Packaging Industry

Key Drivers:

- Rising disposable incomes and changing consumer lifestyles.

- Increasing demand from the food and beverage sector.

- Growth of the e-commerce industry.

- Technological advancements in packaging materials and printing techniques.

Challenges and Restraints:

- Fluctuations in raw material prices.

- Environmental concerns and regulations on plastic waste.

- Intense competition among industry players.

- Supply chain disruptions and logistics challenges.

Emerging Opportunities in Asia Pacific Flexible Packaging Industry

- Growing demand for sustainable and eco-friendly packaging solutions.

- Expansion into untapped markets within the region.

- Development of innovative packaging formats and technologies (e.g., active and intelligent packaging).

- Customization of packaging solutions to meet specific consumer needs.

Growth Accelerators in the Asia Pacific Flexible Packaging Industry

Technological advancements, strategic partnerships, and market expansion strategies are key catalysts for long-term growth in the Asia Pacific flexible packaging industry. Investments in sustainable materials and advanced manufacturing technologies will further drive market expansion. Collaborations between packaging manufacturers and brand owners will lead to innovative packaging solutions tailored to specific market needs. Expansion into high-growth markets within the region will also fuel substantial future growth.

Key Players Shaping the Asia Pacific Flexible Packaging Industry Market

- Formosa Flexible Packaging Corp

- Berry Global Group, Inc.

- Sonoco Products Company

- Wapo Corporation Ltd

- Mondi Group

- Rengo Co Ltd

- Ester Industries Ltd (Wilemina Finance Corporation)

- TCPL Packaging Ltd

- Sealed Air Corporation

- Chuan Peng Enterprise Co Ltd

- Amcor Ltd

Notable Milestones in Asia Pacific Flexible Packaging Industry Sector

- September 2022: Amcor's strategic USD 45 million investment in ePac Flexible Packaging significantly bolstered its capabilities in digital printing and short-run flexible packaging solutions. This move directly addresses the burgeoning demand for agile, customized, and on-demand packaging, particularly for small and medium-sized enterprises (SMEs) and emerging brands.

- August 2022: The inauguration of Amcor's state-of-the-art innovation center in Jiangyin, China, underscores a deep commitment to advancing sustainable material science and pioneering cutting-edge packaging innovations specifically tailored for the Asia Pacific market. This strategic expansion signals a strong focus on accelerated technological development and localized manufacturing excellence to better serve regional clients.

In-Depth Asia Pacific Flexible Packaging Industry Market Outlook

The Asia Pacific flexible packaging market is on an upward trajectory, presenting substantial and multifaceted growth potential for the foreseeable future. The continuous pursuit of innovation will be the primary engine driving future market dynamics. This includes significant advancements in the development and application of truly sustainable packaging materials, the widespread adoption of versatile digital printing technologies that enable personalization and efficiency, and the integration of intelligent packaging solutions offering enhanced functionality and data insights. Strategic collaborations, targeted mergers and acquisitions, and aggressive expansion into rapidly developing emerging markets within the region will be pivotal strategic imperatives for players aiming to secure market leadership and capitalize on the overall growth trajectory. The overarching commitment to sustainability, coupled with relentless technological advancements, will continue to propel this dynamic sector towards remarkable growth and innovation.

Asia Pacific Flexible Packaging Industry Segmentation

-

1. Type

- 1.1. Pouches

- 1.2. Bags

- 1.3. Wraps

- 1.4. Other Types

-

2. Material

- 2.1. Plastic

- 2.2. Paper

- 2.3. Aluminum/Composites

-

3. End-user Industry

- 3.1. Food

- 3.2. Beverages

- 3.3. Pharmaceutical and Medical

- 3.4. Household and Personal Care

- 3.5. Other End-user Industries

Asia Pacific Flexible Packaging Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. Japan

- 1.3. South Korea

- 1.4. India

- 1.5. Australia

- 1.6. New Zealand

- 1.7. Indonesia

- 1.8. Malaysia

- 1.9. Singapore

- 1.10. Thailand

- 1.11. Vietnam

- 1.12. Philippines

Asia Pacific Flexible Packaging Industry Regional Market Share

Geographic Coverage of Asia Pacific Flexible Packaging Industry

Asia Pacific Flexible Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Pouches

- 5.1.2. Bags

- 5.1.3. Wraps

- 5.1.4. Other Types

- 5.2. Market Analysis, Insights and Forecast - by Material

- 5.2.1. Plastic

- 5.2.2. Paper

- 5.2.3. Aluminum/Composites

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Food

- 5.3.2. Beverages

- 5.3.3. Pharmaceutical and Medical

- 5.3.4. Household and Personal Care

- 5.3.5. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Asia Pacific Flexible Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Pouches

- 6.1.2. Bags

- 6.1.3. Wraps

- 6.1.4. Other Types

- 6.2. Market Analysis, Insights and Forecast - by Material

- 6.2.1. Plastic

- 6.2.2. Paper

- 6.2.3. Aluminum/Composites

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Food

- 6.3.2. Beverages

- 6.3.3. Pharmaceutical and Medical

- 6.3.4. Household and Personal Care

- 6.3.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Formosa Flexible Packaging Corp

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Berry Plastics Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Sonoco Products Company

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Wapo Corporation Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Mondi Group

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Rengo Co Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Ester Industries Ltd (Wilemina Finance Corporation)*List Not Exhaustive

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 TCPL Packaging Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Sealed Air Corporation

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Chuan Peng Enterprise Co Ltd

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Amcor Ltd

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 Formosa Flexible Packaging Corp

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Asia Pacific Flexible Packaging Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Asia Pacific Flexible Packaging Industry Share (%) by Company 2025

List of Tables

- Table 1: Asia Pacific Flexible Packaging Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Asia Pacific Flexible Packaging Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 3: Asia Pacific Flexible Packaging Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 4: Asia Pacific Flexible Packaging Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Asia Pacific Flexible Packaging Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Asia Pacific Flexible Packaging Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 7: Asia Pacific Flexible Packaging Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 8: Asia Pacific Flexible Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: China Asia Pacific Flexible Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Japan Asia Pacific Flexible Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: South Korea Asia Pacific Flexible Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: India Asia Pacific Flexible Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Australia Asia Pacific Flexible Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: New Zealand Asia Pacific Flexible Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Indonesia Asia Pacific Flexible Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Malaysia Asia Pacific Flexible Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Singapore Asia Pacific Flexible Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Thailand Asia Pacific Flexible Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Vietnam Asia Pacific Flexible Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Philippines Asia Pacific Flexible Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia Pacific Flexible Packaging Industry?

The projected CAGR is approximately 4.2%.

2. Which companies are prominent players in the Asia Pacific Flexible Packaging Industry?

Key companies in the market include Formosa Flexible Packaging Corp, Berry Plastics Corporation, Sonoco Products Company, Wapo Corporation Ltd, Mondi Group, Rengo Co Ltd, Ester Industries Ltd (Wilemina Finance Corporation)*List Not Exhaustive, TCPL Packaging Ltd, Sealed Air Corporation, Chuan Peng Enterprise Co Ltd, Amcor Ltd.

3. What are the main segments of the Asia Pacific Flexible Packaging Industry?

The market segments include Type, Material, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 301.2 billion as of 2022.

5. What are some drivers contributing to market growth?

Increased Demand for Convenient Packaging; Demand for Longer Shelf Life and Innovative Packaging.

6. What are the notable trends driving market growth?

Food-Packaging Industry to Drive the Market Growth.

7. Are there any restraints impacting market growth?

Concerns about the Environment and Recycling of Packaging Material.

8. Can you provide examples of recent developments in the market?

September 2022: Amcor, a key player in responsible packaging solutions development and production, announced a new strategic investment in ePac Flexible Packaging ("ePac"), a pioneer in high-quality, brief run length digitally-based flexible packaging of up to USD 45 million. Amcor will own more minority shares of ePac Holdings LLC due to the investment.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia Pacific Flexible Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia Pacific Flexible Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia Pacific Flexible Packaging Industry?

To stay informed about further developments, trends, and reports in the Asia Pacific Flexible Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence