Key Insights

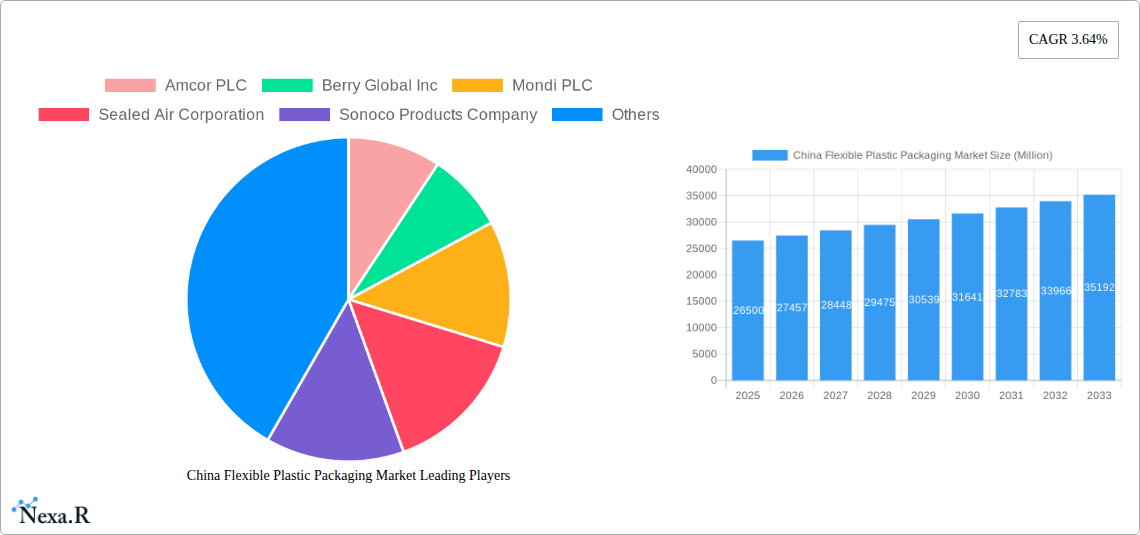

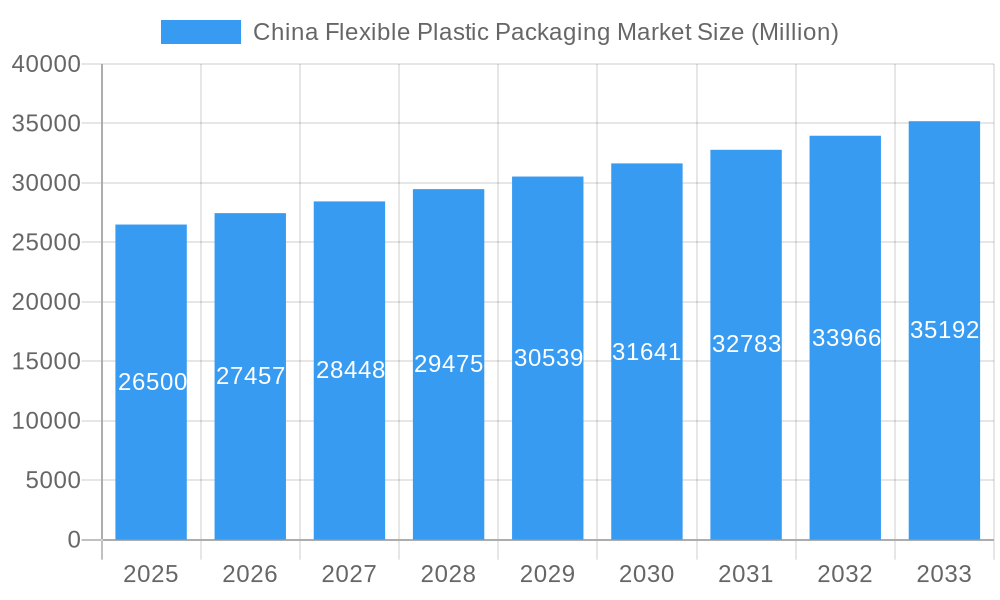

The China Flexible Plastic Packaging market is poised for substantial growth, projected to reach a market size of approximately USD 26,500 million by 2025, with an estimated Compound Annual Growth Rate (CAGR) of 3.64% through 2033. This expansion is primarily fueled by the burgeoning food and beverage industry, which demands innovative and sustainable packaging solutions to preserve product freshness and extend shelf life. The increasing consumer preference for convenience and ready-to-eat meals, coupled with the rapid growth of e-commerce, further propels the demand for flexible packaging formats like pouches and bags. Furthermore, the medical and pharmaceutical sectors are witnessing a significant uptake of flexible packaging due to its sterile properties and tamper-evident features. The personal care and household care segments also contribute to market growth, driven by evolving consumer lifestyles and an increasing awareness of product hygiene and preservation.

China Flexible Plastic Packaging Market Market Size (In Billion)

Despite the robust growth, certain restraints such as fluctuating raw material prices, particularly for Polyethene (PE) and Bi-oriented Polypropylene (BOPP), and the growing environmental concerns regarding plastic waste management, present challenges. However, the industry is actively addressing these concerns through the development of biodegradable and recyclable packaging materials, aligning with government initiatives and consumer demand for eco-friendly options. The market is characterized by a competitive landscape with key players like Amcor PLC, Berry Global Inc., and Mondi PLC investing in advanced manufacturing technologies and sustainable innovations. The dominant presence of domestic manufacturers in China, such as Cangzhou Hualiang Packaging Decoration Co Ltd and Qingdao Kingchuan Packaging, underscores the localized strengths and opportunities within the market. The ongoing shift towards premiumization and value-added packaging is expected to drive further innovation and market expansion in the coming years.

China Flexible Plastic Packaging Market Company Market Share

This in-depth report delivers a definitive analysis of the China flexible plastic packaging market, a critical sector driven by soaring consumer demand, rapid industrialization, and evolving sustainability mandates. Explore the intricate dynamics, growth trajectories, and competitive landscape of this high-growth market, encompassing key parent and child market segments. With extensive data spanning the historical period (2019-2024), base year (2025), and forecast period (2025-2033), this report provides actionable intelligence for stakeholders seeking to capitalize on emerging opportunities. Discover detailed breakdowns of material types (Polyethene (PE), Bi-oriented Polypropylene (BOPP), Cast Polypropylene (CPP), Polyvinyl Chloride (PVC), Ethylene Vinyl Alcohol (EVOH), Other Materials), product types (Pouches, Bags, Films and Wraps, Other Product Types like Blister Packs, Liners), and end-user industries (Food (Candy & Confectionery, Frozen Foods, Fresh Produce, Dairy Products, Dry Foods, Meat, Poultry, And Seafood, Pet Food, Other Food), Beverage, Medical and Pharmaceutical, Personal Care and Household Care, Other End-User Industries).

China Flexible Plastic Packaging Market Market Dynamics & Structure

The China flexible plastic packaging market exhibits a moderately concentrated structure, with a blend of large multinational corporations and a robust contingent of domestic players vying for market share. Technological innovation is a significant driver, with continuous advancements in material science, barrier properties, and printing technologies enhancing product functionality and appeal. Key innovation drivers include the pursuit of lightweighting, improved shelf-life extension, and the development of sustainable packaging solutions. Regulatory frameworks, particularly those pertaining to environmental protection and waste management, are increasingly influencing market dynamics, pushing manufacturers towards recyclable and biodegradable materials. Competitive product substitutes, such as rigid packaging and alternative materials, pose a constant challenge, necessitating ongoing innovation and cost optimization. End-user demographics are shifting, with a growing middle class and a rising demand for convenience, premiumization, and health-conscious products directly impacting packaging requirements. Mergers and acquisitions (M&A) are an active component of market strategy, with companies seeking to expand their product portfolios, geographic reach, and technological capabilities. For instance, recent M&A activity in the broader packaging sector suggests a trend towards consolidation to achieve economies of scale and enhance competitive positioning. Barriers to innovation include high R&D costs, complex supply chain integrations for new materials, and consumer acceptance of novel packaging formats. The overall market is characterized by a dynamic interplay between innovation, regulation, and evolving consumer preferences, shaping its future trajectory.

China Flexible Plastic Packaging Market Growth Trends & Insights

The China flexible plastic packaging market is poised for robust growth, projected to expand significantly from its 2025 market size of approximately $xx billion to $xx billion by 2033, exhibiting a compound annual growth rate (CAGR) of approximately xx% during the forecast period (2025-2033). This expansion is fueled by a confluence of macroeconomic factors and evolving consumer behaviors. The increasing disposable income and the burgeoning middle class in China are driving higher consumption of packaged goods across all end-user industries, particularly in food, beverages, and personal care. The convenience offered by flexible packaging, including its lightweight nature, ease of handling, and re-sealability, resonates strongly with modern lifestyles. Technological advancements are playing a pivotal role, with the development of advanced barrier films, high-resolution printing capabilities, and innovative designs enhancing product appeal and extending shelf life. This is particularly evident in the food and beverage sectors, where maintaining product freshness and integrity is paramount. Furthermore, the growing awareness and demand for sustainable packaging solutions are creating new avenues for growth. The industry is witnessing a surge in the adoption of recyclable and bio-based flexible packaging, driven by both consumer preference and increasing government regulations aimed at reducing plastic waste. This shift is compelling manufacturers to invest in research and development for eco-friendly alternatives. Consumer behavior is also adapting, with a greater emphasis on health and wellness influencing packaging choices, leading to increased demand for packaging that preserves nutritional value and extends freshness. The e-commerce boom in China has also significantly boosted the demand for flexible packaging, as it offers cost-effectiveness and protection during transit for a wide range of products. The market penetration of flexible packaging in China continues to deepen across various applications, supplanting traditional packaging formats due to its inherent advantages in cost, performance, and design flexibility. The adoption rates for innovative and sustainable flexible packaging solutions are expected to accelerate as manufacturers and consumers alike prioritize environmental responsibility and product quality.

Dominant Regions, Countries, or Segments in China Flexible Plastic Packaging Market

Within the China flexible plastic packaging market, the Food End-User Industry stands as the most dominant segment, projected to command a substantial market share exceeding xx% by 2033. This segment’s dominance is underpinned by several interconnected factors, including China's massive population, rapidly evolving dietary habits, and the growing demand for convenience foods and premium packaged products. Specifically within the food sector, the sub-segments of Dairy Products, Meat, Poultry, And Seafood, and Candy & Confectionery are experiencing particularly robust growth. The increasing adoption of processed and pre-packaged foods, driven by busy urban lifestyles and improved cold chain logistics, directly translates to higher demand for specialized flexible packaging that ensures product safety, extends shelf life, and maintains visual appeal. The Food segment's dominance is further amplified by its direct correlation with advancements in flexible packaging materials. For instance, the widespread use of Polyethene (PE), particularly high-density PE (HDPE) and linear low-density PE (LLDPE), as a primary material in food packaging, underscores its importance. Bi-oriented Polypropylene (BOPP) also plays a crucial role due to its excellent clarity, barrier properties, and printability, making it ideal for snack food packaging and confectioneries. The Pouches product type, encompassing stand-up pouches, retort pouches, and zipper pouches, is also a significant contributor to the Food segment's growth, offering convenience and extended shelf life for various food items.

Key drivers for the dominance of the Food segment include:

- Economic Policies: Government initiatives supporting food processing and safety standards indirectly boost demand for high-quality flexible packaging.

- Infrastructure Development: Enhanced cold chain logistics and distribution networks facilitate the wider availability of packaged food products, increasing reliance on flexible packaging.

- Consumer Preferences: A growing middle class with higher disposable incomes is opting for convenient, hygienically packaged food items. The demand for premium and aesthetically pleasing packaging further fuels this trend.

- Technological Advancements in Materials: Innovations in PE, BOPP, and other materials offering improved barrier properties against oxygen, moisture, and light are crucial for preserving food quality and extending shelf life, directly benefiting this segment.

- Market Share: The Food segment consistently holds the largest market share, estimated to be over xx% of the total China flexible plastic packaging market in 2025.

- Growth Potential: Continued urbanization and the rise of e-commerce for groceries will ensure sustained high growth rates for flexible packaging in the food sector.

While the Food segment leads, the Beverage and Personal Care and Household Care segments are also significant growth areas, driven by similar trends in consumption and convenience. However, the sheer volume and daily necessity of food products position the Food industry as the undisputed leader in the China flexible plastic packaging market.

China Flexible Plastic Packaging Market Product Landscape

The China flexible plastic packaging market is characterized by a diverse and innovative product landscape designed to meet the evolving needs of consumers and industries. Pouches, particularly stand-up pouches with re-sealable closures and retort pouches for extended shelf life, are highly sought after, especially in the food and beverage sectors. Films and Wraps remain fundamental, with advancements in multi-layer films offering enhanced barrier properties, printability, and functionality for a wide array of applications, from snack packaging to industrial wrapping. Bags, including gusseted bags and flat-bottom bags, continue to be prevalent for bulk packaging of dry goods and pet food. Unique selling propositions in this market revolve around sustainability, with a growing emphasis on mono-material packaging for improved recyclability and the development of compostable and biodegradable alternatives. Technological advancements are focused on improving oxygen and moisture barrier properties, critical for extending product shelf life and reducing food waste. High-definition printing capabilities allow for vibrant branding and sophisticated graphics, enhancing product shelf appeal. Performance metrics such as tensile strength, puncture resistance, and seal integrity are continuously being optimized to ensure product protection during transit and handling.

Key Drivers, Barriers & Challenges in China Flexible Plastic Packaging Market

Key Drivers:

The China flexible plastic packaging market is propelled by several key drivers. Foremost among these is the ever-increasing consumer demand for packaged goods driven by a rising middle class and urbanization, particularly in the food and beverage sectors. The inherent advantages of flexible packaging, such as lightweighting, cost-effectiveness, and convenience, make it a preferred choice for both manufacturers and consumers. Technological advancements in material science, leading to enhanced barrier properties, improved printability, and innovative design features, are also significant catalysts. Furthermore, the growing global and domestic emphasis on sustainable packaging solutions, including recyclable, compostable, and bio-based materials, presents a substantial growth opportunity as regulations tighten and consumer awareness rises.

Barriers & Challenges:

Despite robust growth, the market faces significant barriers and challenges. The increasing regulatory scrutiny and public pressure regarding plastic waste and environmental pollution present a major hurdle, necessitating substantial investment in R&D for sustainable alternatives and waste management infrastructure. Fluctuations in raw material prices, particularly for petrochemical-based plastics, can impact profit margins and supply chain stability. The complexities of recycling infrastructure and consumer participation in recycling programs in China can also hinder the adoption of truly circular packaging models. Moreover, intense competition from both domestic and international players drives down margins and demands continuous innovation and cost optimization. The supply chain integration for novel sustainable materials can also be challenging, requiring collaboration across the value chain. Quantifiable impacts include potential increases in production costs for sustainable materials and a need for significant capital investment in new manufacturing technologies.

Emerging Opportunities in China Flexible Plastic Packaging Market

Emerging opportunities in the China flexible plastic packaging market are multifaceted. The push towards circular economy principles is creating significant demand for mono-material flexible packaging solutions that are easily recyclable. This includes innovations in barrier films made from a single polymer type, such as mono-PE or mono-PP, which are gaining traction in food and personal care applications. Furthermore, the growing demand for convenience and on-the-go consumption fuels opportunities in smaller, single-serve pouches and sachets for snacks, beverages, and personal care items. The e-commerce sector's rapid expansion necessitates robust yet lightweight packaging solutions, presenting opportunities for specialized protective films and mailer bags. Investments in biodegradable and compostable flexible packaging are also poised to grow as environmental consciousness deepens and regulations evolve, particularly for short-shelf-life products and single-use applications. The medical and pharmaceutical sector also offers significant untapped potential for high-barrier, sterile flexible packaging solutions.

Growth Accelerators in the China Flexible Plastic Packaging Market Industry

Several key catalysts are accelerating long-term growth in the China flexible plastic packaging market. Technological breakthroughs in material science, leading to the development of advanced barrier properties, enhanced recyclability, and the creation of novel bio-based plastics, are fundamental. Strategic partnerships and collaborations between raw material suppliers, packaging manufacturers, and brand owners are crucial for driving innovation and scaling sustainable solutions. For example, collaborations focused on developing closed-loop recycling systems or enhancing the performance of compostable materials will accelerate adoption. Market expansion strategies, including penetration into emerging Tier 3 and Tier 4 cities with growing consumer bases and investments in localized production facilities, will further fuel growth. The increasing adoption of digital printing technologies allows for greater customization, shorter runs, and faster turnaround times, catering to the demand for personalized packaging and enabling quicker market entry for new products. Furthermore, government support for the development of a robust waste management and recycling infrastructure will be a critical accelerator for the widespread adoption of sustainable flexible packaging.

Key Players Shaping the China Flexible Plastic Packaging Market Market

- Amcor PLC

- Berry Global Inc

- Mondi PLC

- Sealed Air Corporation

- Sonoco Products Company

- Cangzhou Hualiang Packaging Decoration Co Ltd

- Qingdao Kingchuan Packaging

- Jieshou Tianhong New Material Co Ltd

- Wenzhou Co-pack Co Ltd

Notable Milestones in China Flexible Plastic Packaging Market Sector

- May 2024: Amcor, in partnership with AVON, launched the AmPrima™ Plus refill pouch for AVON Little Black Dress classic shower gels in China. This recycle-ready packaging signifies a significant step towards sustainability, resulting in an 83% reduction in carbon footprint and substantial reductions in water consumption and renewable energy usage during recycling.

- January 2024: Mars China introduced a Snickers bar with dark chocolate cereal utilizing mono-material flexible packaging. This innovative product features individual packaging made from a mono PP material, designed to promote recycling and cater to a low-sugar, low-glycemic index consumer preference.

In-Depth China Flexible Plastic Packaging Market Market Outlook

The China flexible plastic packaging market is set for sustained and significant growth, driven by a potent combination of evolving consumer lifestyles, supportive government policies, and relentless technological innovation. The burgeoning middle class's demand for convenience, premium products, and enhanced food safety will continue to be a primary growth accelerator. Strategic opportunities lie in further developing and scaling high-performance, sustainable packaging solutions, including mono-material recyclable options and advanced biodegradable alternatives. The expansion of e-commerce will continue to fuel demand for durable and lightweight flexible packaging. Collaboration across the value chain to improve recycling infrastructure and consumer education will be critical for realizing the full potential of a circular economy in plastic packaging. Future market growth will also be shaped by continuous innovation in barrier technologies and printing, offering brands enhanced product protection and consumer engagement. The China flexible plastic packaging market is not just a growing sector; it's a dynamic landscape poised for transformation towards greater sustainability and innovation.

China Flexible Plastic Packaging Market Segmentation

-

1. Material Type

- 1.1. Polyethene (PE)

- 1.2. Bi-oriented Polypropylene (BOPP)

- 1.3. Cast Polypropylene (CPP)

- 1.4. Polyvinyl Chloride (PVC)

- 1.5. Ethylene Vinyl Alcohol (EVOH)

- 1.6. Other Ma

-

2. Product Type

- 2.1. Pouches

- 2.2. Bags

- 2.3. Films and Wraps

- 2.4. Other Product Types (Blister Packs, Liners, etc)

-

3. End-User Industry

-

3.1. Food

- 3.1.1. Candy & Confectionery

- 3.1.2. Frozen Foods

- 3.1.3. Fresh Produce

- 3.1.4. Dairy Products

- 3.1.5. Dry Foods

- 3.1.6. Meat, Poultry, And Seafood

- 3.1.7. Pet Food

- 3.1.8. Other Fo

- 3.2. Beverage

- 3.3. Medical and Pharmaceutical

- 3.4. Personal Care and Household Care

- 3.5. Other En

-

3.1. Food

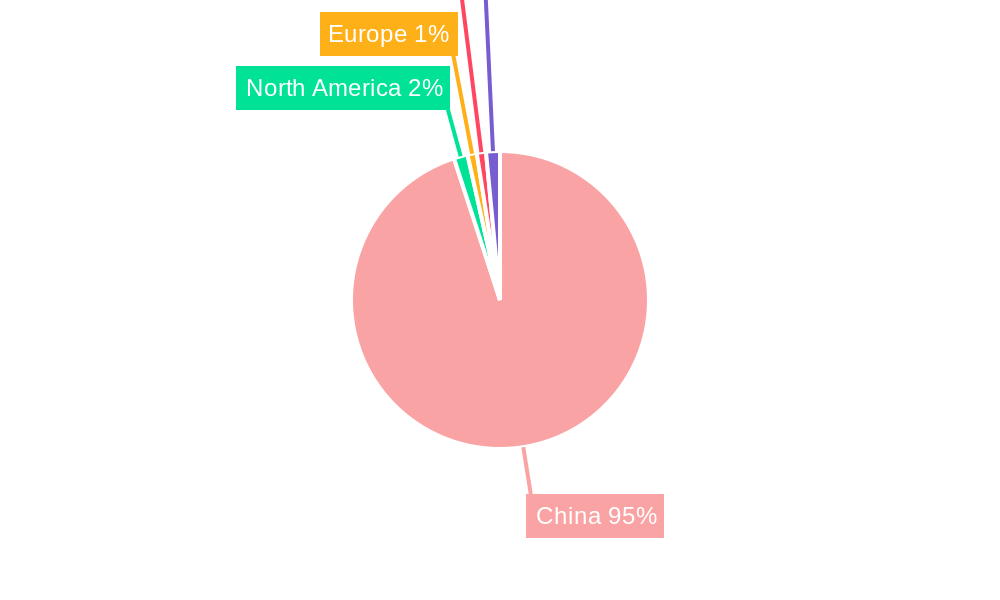

China Flexible Plastic Packaging Market Segmentation By Geography

- 1. China

China Flexible Plastic Packaging Market Regional Market Share

Geographic Coverage of China Flexible Plastic Packaging Market

China Flexible Plastic Packaging Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.64% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 5.1.1. Polyethene (PE)

- 5.1.2. Bi-oriented Polypropylene (BOPP)

- 5.1.3. Cast Polypropylene (CPP)

- 5.1.4. Polyvinyl Chloride (PVC)

- 5.1.5. Ethylene Vinyl Alcohol (EVOH)

- 5.1.6. Other Ma

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Pouches

- 5.2.2. Bags

- 5.2.3. Films and Wraps

- 5.2.4. Other Product Types (Blister Packs, Liners, etc)

- 5.3. Market Analysis, Insights and Forecast - by End-User Industry

- 5.3.1. Food

- 5.3.1.1. Candy & Confectionery

- 5.3.1.2. Frozen Foods

- 5.3.1.3. Fresh Produce

- 5.3.1.4. Dairy Products

- 5.3.1.5. Dry Foods

- 5.3.1.6. Meat, Poultry, And Seafood

- 5.3.1.7. Pet Food

- 5.3.1.8. Other Fo

- 5.3.2. Beverage

- 5.3.3. Medical and Pharmaceutical

- 5.3.4. Personal Care and Household Care

- 5.3.5. Other En

- 5.3.1. Food

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. China

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 6. China Flexible Plastic Packaging Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 6.1.1. Polyethene (PE)

- 6.1.2. Bi-oriented Polypropylene (BOPP)

- 6.1.3. Cast Polypropylene (CPP)

- 6.1.4. Polyvinyl Chloride (PVC)

- 6.1.5. Ethylene Vinyl Alcohol (EVOH)

- 6.1.6. Other Ma

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Pouches

- 6.2.2. Bags

- 6.2.3. Films and Wraps

- 6.2.4. Other Product Types (Blister Packs, Liners, etc)

- 6.3. Market Analysis, Insights and Forecast - by End-User Industry

- 6.3.1. Food

- 6.3.1.1. Candy & Confectionery

- 6.3.1.2. Frozen Foods

- 6.3.1.3. Fresh Produce

- 6.3.1.4. Dairy Products

- 6.3.1.5. Dry Foods

- 6.3.1.6. Meat, Poultry, And Seafood

- 6.3.1.7. Pet Food

- 6.3.1.8. Other Fo

- 6.3.2. Beverage

- 6.3.3. Medical and Pharmaceutical

- 6.3.4. Personal Care and Household Care

- 6.3.5. Other En

- 6.3.1. Food

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Amcor PLC

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Berry Global Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Mondi PLC

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Sealed Air Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Sonoco Products Company

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Cangzhou Hualiang Packaging Decoration Co Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Qingdao Kingchuan Packaging

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Jieshou Tianhong New Material Co Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Wenzhou Co-pack Co Ltd7 2 Heat Map Analysi

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Amcor PLC

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Flexible Plastic Packaging Market Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: China Flexible Plastic Packaging Market Share (%) by Company 2025

List of Tables

- Table 1: China Flexible Plastic Packaging Market Revenue million Forecast, by Material Type 2020 & 2033

- Table 2: China Flexible Plastic Packaging Market Revenue million Forecast, by Product Type 2020 & 2033

- Table 3: China Flexible Plastic Packaging Market Revenue million Forecast, by End-User Industry 2020 & 2033

- Table 4: China Flexible Plastic Packaging Market Revenue million Forecast, by Region 2020 & 2033

- Table 5: China Flexible Plastic Packaging Market Revenue million Forecast, by Material Type 2020 & 2033

- Table 6: China Flexible Plastic Packaging Market Revenue million Forecast, by Product Type 2020 & 2033

- Table 7: China Flexible Plastic Packaging Market Revenue million Forecast, by End-User Industry 2020 & 2033

- Table 8: China Flexible Plastic Packaging Market Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Flexible Plastic Packaging Market?

The projected CAGR is approximately 3.64%.

2. Which companies are prominent players in the China Flexible Plastic Packaging Market?

Key companies in the market include Amcor PLC, Berry Global Inc, Mondi PLC, Sealed Air Corporation, Sonoco Products Company, Cangzhou Hualiang Packaging Decoration Co Ltd, Qingdao Kingchuan Packaging, Jieshou Tianhong New Material Co Ltd, Wenzhou Co-pack Co Ltd7 2 Heat Map Analysi.

3. What are the main segments of the China Flexible Plastic Packaging Market?

The market segments include Material Type, Product Type, End-User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.51 million as of 2022.

5. What are some drivers contributing to market growth?

The E-commerce Sector is Expected to Propel the Market.

6. What are the notable trends driving market growth?

Retail E-commerce is Expected to Propel the Market's Growth.

7. Are there any restraints impacting market growth?

The E-commerce Sector is Expected to Propel the Market.

8. Can you provide examples of recent developments in the market?

May 8 2024 – Amcor developing and producing responsible packaging solutions, and AVON, a cosmetics, skin care and personal care pioneer with a 135-year history, today announced the launch of the AmPrima™ Plus refill pouch for the AVON Little Black Dress classic shower gels in China. The recycle-ready packaging will result in an 83% reduction in carbon footprint, and 88% and 79% reduction in water consumption and renewable energy respectively when it's recycled.*

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Flexible Plastic Packaging Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Flexible Plastic Packaging Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Flexible Plastic Packaging Market?

To stay informed about further developments, trends, and reports in the China Flexible Plastic Packaging Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence