Key Insights

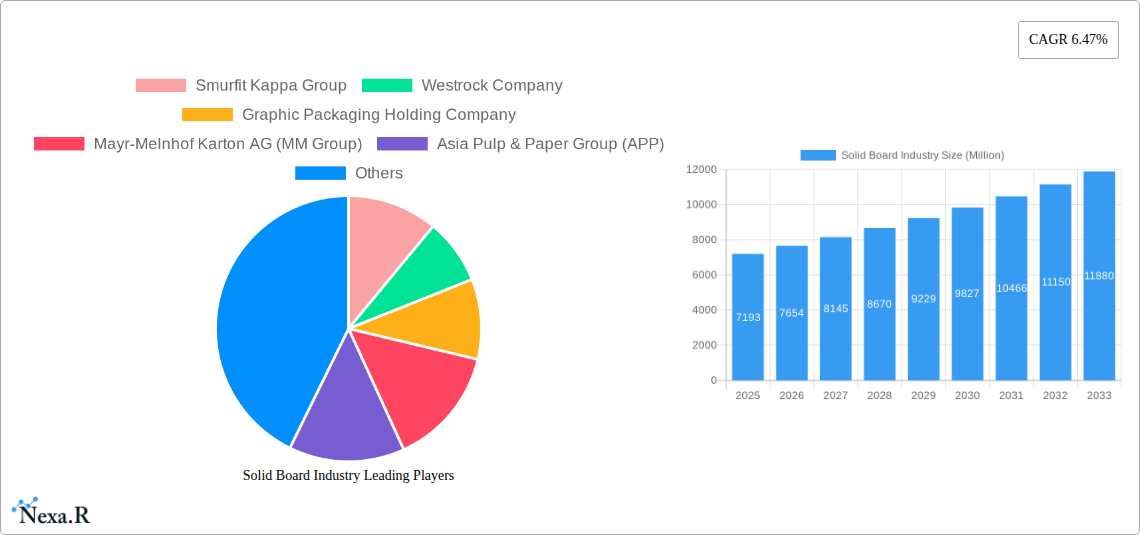

The global Solid Board market is poised for significant expansion, projected to reach a substantial valuation by 2033. With a robust Compound Annual Growth Rate (CAGR) of 6.47% from a 2025 base year, the market is driven by a confluence of factors including increasing consumer demand for sustainable packaging solutions, the burgeoning e-commerce sector, and the growing preference for visually appealing and durable packaging across various industries. The "Product Grade" segment showcases a diverse landscape, with Folding Boxboard and Liquid Packaging Board leading in adoption due to their versatility and widespread application in the food and beverage sectors. The "End-User" segment highlights the indispensable role of solid board in packaging for Food, Beverages, and Pharmaceuticals, directly correlating with essential consumer needs and stringent regulatory requirements for product integrity. Emerging economies, particularly in Asia, are expected to contribute significantly to this growth trajectory, fueled by rising disposable incomes and evolving retail environments.

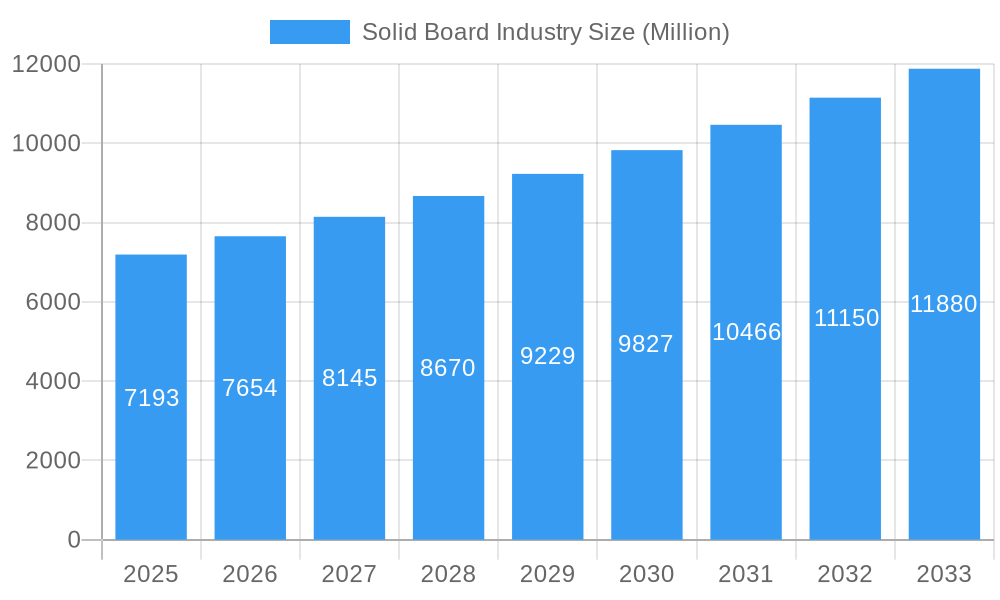

Solid Board Industry Market Size (In Billion)

Further analysis reveals that key trends such as the development of high-performance barrier coatings, the integration of smart packaging technologies for enhanced traceability, and the continuous innovation in sustainable raw materials are shaping the competitive landscape. These trends are addressing growing environmental concerns and consumer preferences for eco-friendly options. However, the market also faces challenges, including fluctuations in raw material prices, particularly pulp and paper, and intense competition from alternative packaging materials. Additionally, the capital-intensive nature of advanced manufacturing technologies and evolving waste management regulations in different regions present restraining factors that necessitate strategic investments and adaptive business models. Companies like Smurfit Kappa Group, Westrock Company, and Graphic Packaging Holding Company are at the forefront, actively pursuing strategies like mergers, acquisitions, and product innovation to capitalize on these market dynamics and maintain a competitive edge in the evolving solid board industry.

Solid Board Industry Company Market Share

Solid Board Industry Market Dynamics & Structure

The global solid board industry is characterized by a moderately concentrated market, with a few key players holding significant market share. Technological innovation is a primary driver, focusing on enhanced barrier properties, sustainability, and specialized functionalities for diverse end-user applications. Regulatory frameworks, particularly those concerning packaging sustainability, recyclability, and food contact safety, are increasingly influencing product development and market entry. Competitive product substitutes, such as flexible packaging and plastic alternatives, present an ongoing challenge, necessitating continuous innovation in solid board to maintain its competitive edge. End-user demographics are shifting towards a greater demand for eco-friendly and high-performance packaging solutions across all sectors, with significant growth observed in the food & beverage and pharmaceutical segments. Mergers and acquisitions (M&A) are prevalent, as larger companies seek to consolidate market presence, acquire new technologies, and expand their geographical reach.

- Market Concentration: Dominated by integrated paper and packaging manufacturers.

- Technological Innovation: Focus on lightweighting, improved printability, enhanced moisture and grease resistance, and bio-based coatings.

- Regulatory Influence: Growing emphasis on Extended Producer Responsibility (EPR) schemes and plastic reduction targets.

- Competitive Substitutes: Plastics, films, and emerging compostable materials.

- End-User Demographics: Increasing demand for premium, sustainable, and functional packaging.

- M&A Trends: Strategic acquisitions to bolster product portfolios and expand production capacity.

Solid Board Industry Growth Trends & Insights

The solid board industry is poised for robust growth, projected to witness a Compound Annual Growth Rate (CAGR) of approximately 6.5% during the forecast period of 2025–2033. This expansion is largely fueled by the burgeoning demand for sustainable and recyclable packaging solutions across the globe. The market size is estimated to reach USD 95,500 million in 2025, driven by evolving consumer preferences and stringent environmental regulations that favor paper-based alternatives over plastics. Adoption rates for high-quality coated solid board grades are escalating, particularly in the food and beverage sectors, where consumers increasingly prioritize visually appealing and safe packaging. Technological disruptions are centered on the development of advanced barrier coatings, enabling solid board to effectively replace plastic in applications like liquid packaging and food service. Consumer behavior shifts, including a heightened awareness of environmental impact and a willingness to support brands with sustainable packaging initiatives, are significantly influencing purchasing decisions and, consequently, the demand for solid board. The increasing focus on e-commerce is also a significant driver, as solid board offers excellent protection and durability for shipped goods. Furthermore, the pharmaceutical and healthcare sectors are witnessing a surge in demand for sterile, tamper-evident, and aesthetically pleasing solid board packaging, further contributing to market expansion.

Dominant Regions, Countries, or Segments in Solid Board Industry

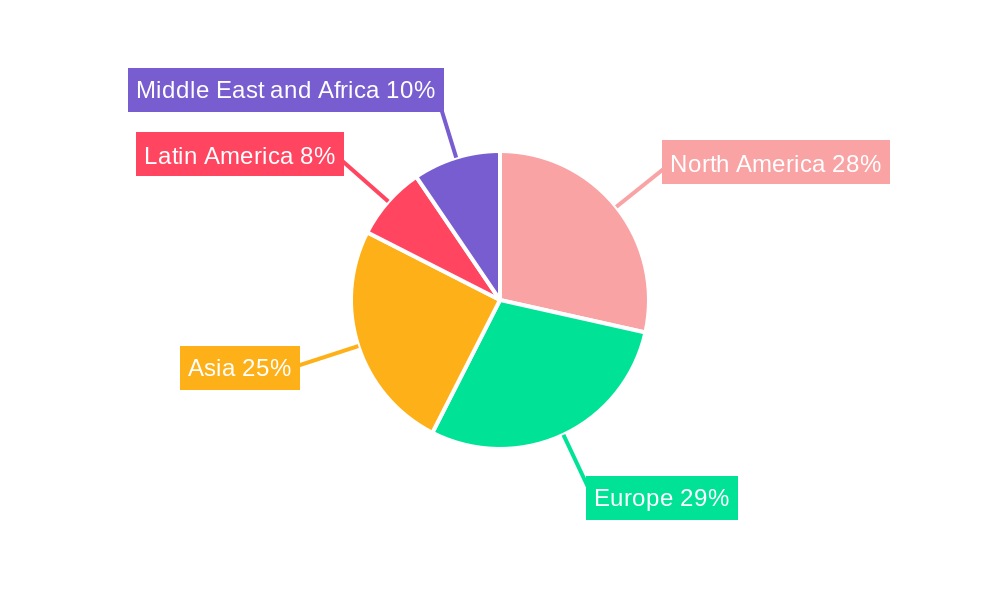

North America and Europe currently dominate the solid board industry, driven by established economies, high consumer spending, and stringent environmental regulations promoting sustainable packaging. The Food & Beverage end-user segment is the leading market driver, accounting for an estimated 35% of the total solid board consumption in 2025. This dominance is attributed to the continuous demand for packaging for a wide array of food products, including frozen foods, confectionery, dairy, and ready-to-eat meals. The increasing consumer preference for convenience and the growing popularity of ready-to-drink beverages further bolster the demand for liquid packaging board and folding boxboard within this segment.

Leading End-User Segment: Food & Beverage

- Market Share (2025 Estimate): ~35%

- Key Drivers:

- Growing demand for processed and packaged foods.

- Shift towards sustainable and recyclable packaging.

- Increasing popularity of ready-to-drink beverages and single-serve portions.

- Stringent food safety and hygiene regulations.

- Growth Potential: High, driven by global population growth and evolving dietary habits.

Leading Product Grade: Folding Boxboard (FBB)

- Market Share (2025 Estimate): ~30%

- Key Drivers:

- Versatility in applications across various end-user industries.

- Excellent printability for branding and marketing.

- Cost-effectiveness compared to other premium packaging materials.

- Growing demand in cosmetics, pharmaceuticals, and tobacco.

- Growth Potential: Significant, especially with advancements in coatings for enhanced barrier properties.

The Pharmaceutical and Healthcare segment is also a substantial contributor, driven by the need for safe, tamper-evident, and regulatory-compliant packaging. The Cosmetics and Toiletries sector contributes significantly due to the aesthetic appeal and premium look that solid board provides, enhancing brand perception. Regions with robust manufacturing bases and export-oriented economies, such as Asia-Pacific, are exhibiting rapid growth, fueled by increasing disposable incomes and a growing middle class.

Solid Board Industry Product Landscape

The solid board industry offers a diverse product landscape designed to meet specific end-user requirements. Key product grades include Solid Bleached Board (SBB), known for its excellent printability and brightness, ideal for high-graphic applications in food and cosmetics. Solid Unbleached Board (SUB) provides superior strength and barrier properties for industrial packaging and heavy-duty applications. Folding Boxboard (FBB) is a versatile grade used extensively for folding cartons in food, pharmaceuticals, and consumer goods. White-lined Chipboard (WLC) offers a cost-effective solution for various packaging needs. Liquid Packaging Board (LPB) is engineered with specialized coatings for beverage cartons, ensuring product integrity and shelf-life. Food Service Board is designed for direct food contact, offering grease and heat resistance. Innovations are focused on enhancing these grades with sustainable barrier coatings, improved recyclability, and a reduced environmental footprint.

Key Drivers, Barriers & Challenges in Solid Board Industry

Key Drivers: The solid board industry is propelled by several key drivers. The escalating global demand for sustainable and eco-friendly packaging is paramount, directly benefiting paper-based solutions as consumers and regulators shift away from single-use plastics. Technological advancements in papermaking and converting technologies are enabling the production of higher-performance solid boards with enhanced barrier properties, printability, and structural integrity. The growth of e-commerce necessitates robust and protective packaging, a role solid board fulfills effectively. Furthermore, evolving consumer preferences for premium and aesthetically pleasing packaging are driving demand for high-quality coated solid boards.

Barriers & Challenges: Despite its growth potential, the solid board industry faces significant barriers and challenges. Fluctuations in raw material prices, particularly wood pulp, can impact production costs and profitability. Intense competition from alternative packaging materials, including flexible plastics and advanced composite materials, poses a constant threat. Supply chain disruptions, exacerbated by geopolitical events and logistical complexities, can affect the availability and timely delivery of raw materials and finished products. Stringent and evolving regulatory landscapes, while a driver for sustainability, can also create compliance burdens and require significant investment in process adaptation. Moreover, the energy-intensive nature of paper production presents challenges in meeting increasingly ambitious carbon reduction targets.

Emerging Opportunities in Solid Board Industry

Emerging opportunities in the solid board industry lie in the development of innovative bio-based and compostable coatings that further enhance sustainability credentials and expand applications into niche markets. The growth of the personalized and premium consumer goods sector presents an opportunity for high-quality, visually appealing solid board packaging that enhances brand perception. Untapped markets in developing economies, with their rapidly growing middle classes and increasing demand for packaged goods, offer significant expansion potential. Furthermore, advancements in digital printing technologies can enable on-demand, customized solid board packaging solutions for smaller businesses and specialized product lines.

Growth Accelerators in the Solid Board Industry Industry

Several catalysts are accelerating the growth of the solid board industry. Technological breakthroughs in fiber technology and barrier coating applications are enabling solid board to compete effectively in demanding applications previously dominated by plastics. Strategic partnerships between paper manufacturers, brand owners, and packaging converters are fostering collaborative innovation and accelerating the adoption of new solid board solutions. Market expansion strategies, including the development of localized production facilities in high-growth regions and investments in advanced recycling infrastructure, are crucial for sustaining momentum. The increasing corporate commitment to sustainability goals, driven by stakeholder pressure and regulatory mandates, is a significant growth accelerator, prioritizing paper-based packaging solutions.

Key Players Shaping the Solid Board Industry Market

Smurfit Kappa Group Westrock Company Graphic Packaging Holding Company Mayr-Melnhof Karton AG (MM Group) Asia Pulp & Paper Group (APP) Pankaboard OYJ International Paper Company Stora Enso OYJ Metsa Board Nine Dragons Paper Holdings Limited

Notable Milestones in Solid Board Industry Sector

- June 2023: Stora Enso opened a new corrugated board manufacturing facility in De Lier, the Netherlands. This expansion, part of the De Jong Packaging Group acquisition, significantly enhances their Western Europe business unit's capacity with a focus on sustainable operations.

- June 2023: Metsa Group, in collaboration with Mets Spring and Fiskars Group, launched Mouto 3D, a fiber-based packaging solution. The boxboard outer packaging enhances visual appeal and quality, housing Fiskars' ReNew scissors made from recycled materials.

In-Depth Solid Board Industry Market Outlook

The future outlook for the solid board industry is exceptionally promising, driven by a confluence of factors. Continued advancements in material science and sustainable manufacturing practices will further solidify solid board's position as a preferred packaging material. The ongoing shift in consumer and regulatory preferences towards environmentally responsible options will serve as a primary growth accelerator, diminishing the market share of less sustainable alternatives. Strategic investments in expanding production capacities in emerging markets and optimizing supply chains will be critical for capturing burgeoning demand. The industry's adaptability to develop tailored solutions for evolving end-user needs, particularly in sectors like e-commerce and premium consumer goods, will ensure its sustained relevance and market dominance in the coming years.

Solid Board Industry Segmentation

-

1. Product Grade

- 1.1. Solid Bleached Board

- 1.2. Solid Unbleached Board

- 1.3. Folding Boxboard

- 1.4. White-lined Chipboard

- 1.5. Liquid Packaging Board

- 1.6. Food Service Board

-

2. End-User

- 2.1. Beverage

- 2.2. Food

- 2.3. Pharmaceutical and Healthcare

- 2.4. Cosmetics and Toiletries

- 2.5. Tobacco

Solid Board Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. United Kingdom

- 2.2. Germany

- 2.3. France

- 2.4. Italy

- 2.5. Spain

-

3. Asia

- 3.1. China

- 3.2. India

- 3.3. Japan

- 3.4. Australia and New Zealand

-

4. Latin America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Mexico

-

5. Middle East and Africa

- 5.1. United Arab Emirates

- 5.2. Saudi Arabia

- 5.3. South Africa

- 5.4. Egypt

Solid Board Industry Regional Market Share

Geographic Coverage of Solid Board Industry

Solid Board Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.47% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Grade

- 5.1.1. Solid Bleached Board

- 5.1.2. Solid Unbleached Board

- 5.1.3. Folding Boxboard

- 5.1.4. White-lined Chipboard

- 5.1.5. Liquid Packaging Board

- 5.1.6. Food Service Board

- 5.2. Market Analysis, Insights and Forecast - by End-User

- 5.2.1. Beverage

- 5.2.2. Food

- 5.2.3. Pharmaceutical and Healthcare

- 5.2.4. Cosmetics and Toiletries

- 5.2.5. Tobacco

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Product Grade

- 6. Global Solid Board Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Grade

- 6.1.1. Solid Bleached Board

- 6.1.2. Solid Unbleached Board

- 6.1.3. Folding Boxboard

- 6.1.4. White-lined Chipboard

- 6.1.5. Liquid Packaging Board

- 6.1.6. Food Service Board

- 6.2. Market Analysis, Insights and Forecast - by End-User

- 6.2.1. Beverage

- 6.2.2. Food

- 6.2.3. Pharmaceutical and Healthcare

- 6.2.4. Cosmetics and Toiletries

- 6.2.5. Tobacco

- 6.1. Market Analysis, Insights and Forecast - by Product Grade

- 7. North America Solid Board Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Grade

- 7.1.1. Solid Bleached Board

- 7.1.2. Solid Unbleached Board

- 7.1.3. Folding Boxboard

- 7.1.4. White-lined Chipboard

- 7.1.5. Liquid Packaging Board

- 7.1.6. Food Service Board

- 7.2. Market Analysis, Insights and Forecast - by End-User

- 7.2.1. Beverage

- 7.2.2. Food

- 7.2.3. Pharmaceutical and Healthcare

- 7.2.4. Cosmetics and Toiletries

- 7.2.5. Tobacco

- 7.1. Market Analysis, Insights and Forecast - by Product Grade

- 8. Europe Solid Board Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Grade

- 8.1.1. Solid Bleached Board

- 8.1.2. Solid Unbleached Board

- 8.1.3. Folding Boxboard

- 8.1.4. White-lined Chipboard

- 8.1.5. Liquid Packaging Board

- 8.1.6. Food Service Board

- 8.2. Market Analysis, Insights and Forecast - by End-User

- 8.2.1. Beverage

- 8.2.2. Food

- 8.2.3. Pharmaceutical and Healthcare

- 8.2.4. Cosmetics and Toiletries

- 8.2.5. Tobacco

- 8.1. Market Analysis, Insights and Forecast - by Product Grade

- 9. Asia Solid Board Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Grade

- 9.1.1. Solid Bleached Board

- 9.1.2. Solid Unbleached Board

- 9.1.3. Folding Boxboard

- 9.1.4. White-lined Chipboard

- 9.1.5. Liquid Packaging Board

- 9.1.6. Food Service Board

- 9.2. Market Analysis, Insights and Forecast - by End-User

- 9.2.1. Beverage

- 9.2.2. Food

- 9.2.3. Pharmaceutical and Healthcare

- 9.2.4. Cosmetics and Toiletries

- 9.2.5. Tobacco

- 9.1. Market Analysis, Insights and Forecast - by Product Grade

- 10. Latin America Solid Board Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Grade

- 10.1.1. Solid Bleached Board

- 10.1.2. Solid Unbleached Board

- 10.1.3. Folding Boxboard

- 10.1.4. White-lined Chipboard

- 10.1.5. Liquid Packaging Board

- 10.1.6. Food Service Board

- 10.2. Market Analysis, Insights and Forecast - by End-User

- 10.2.1. Beverage

- 10.2.2. Food

- 10.2.3. Pharmaceutical and Healthcare

- 10.2.4. Cosmetics and Toiletries

- 10.2.5. Tobacco

- 10.1. Market Analysis, Insights and Forecast - by Product Grade

- 11. Middle East and Africa Solid Board Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Grade

- 11.1.1. Solid Bleached Board

- 11.1.2. Solid Unbleached Board

- 11.1.3. Folding Boxboard

- 11.1.4. White-lined Chipboard

- 11.1.5. Liquid Packaging Board

- 11.1.6. Food Service Board

- 11.2. Market Analysis, Insights and Forecast - by End-User

- 11.2.1. Beverage

- 11.2.2. Food

- 11.2.3. Pharmaceutical and Healthcare

- 11.2.4. Cosmetics and Toiletries

- 11.2.5. Tobacco

- 11.1. Market Analysis, Insights and Forecast - by Product Grade

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Smurfit Kappa Group

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Westrock Company

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Graphic Packaging Holding Company

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Mayr-Melnhof Karton AG (MM Group)

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Asia Pulp & Paper Group (APP)

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Pankaboard OYJ*List Not Exhaustive

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 International Paper Company

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Stora Enso OYJ

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Metsa Board

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Nine Dragons Paper Holdings Limited

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Smurfit Kappa Group

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Solid Board Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Solid Board Industry Revenue (Million), by Product Grade 2025 & 2033

- Figure 3: North America Solid Board Industry Revenue Share (%), by Product Grade 2025 & 2033

- Figure 4: North America Solid Board Industry Revenue (Million), by End-User 2025 & 2033

- Figure 5: North America Solid Board Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 6: North America Solid Board Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Solid Board Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Solid Board Industry Revenue (Million), by Product Grade 2025 & 2033

- Figure 9: Europe Solid Board Industry Revenue Share (%), by Product Grade 2025 & 2033

- Figure 10: Europe Solid Board Industry Revenue (Million), by End-User 2025 & 2033

- Figure 11: Europe Solid Board Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 12: Europe Solid Board Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Solid Board Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Solid Board Industry Revenue (Million), by Product Grade 2025 & 2033

- Figure 15: Asia Solid Board Industry Revenue Share (%), by Product Grade 2025 & 2033

- Figure 16: Asia Solid Board Industry Revenue (Million), by End-User 2025 & 2033

- Figure 17: Asia Solid Board Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 18: Asia Solid Board Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Solid Board Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America Solid Board Industry Revenue (Million), by Product Grade 2025 & 2033

- Figure 21: Latin America Solid Board Industry Revenue Share (%), by Product Grade 2025 & 2033

- Figure 22: Latin America Solid Board Industry Revenue (Million), by End-User 2025 & 2033

- Figure 23: Latin America Solid Board Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 24: Latin America Solid Board Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Latin America Solid Board Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Solid Board Industry Revenue (Million), by Product Grade 2025 & 2033

- Figure 27: Middle East and Africa Solid Board Industry Revenue Share (%), by Product Grade 2025 & 2033

- Figure 28: Middle East and Africa Solid Board Industry Revenue (Million), by End-User 2025 & 2033

- Figure 29: Middle East and Africa Solid Board Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 30: Middle East and Africa Solid Board Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Middle East and Africa Solid Board Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Solid Board Industry Revenue Million Forecast, by Product Grade 2020 & 2033

- Table 2: Global Solid Board Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 3: Global Solid Board Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Solid Board Industry Revenue Million Forecast, by Product Grade 2020 & 2033

- Table 5: Global Solid Board Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 6: Global Solid Board Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Global Solid Board Industry Revenue Million Forecast, by Product Grade 2020 & 2033

- Table 10: Global Solid Board Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 11: Global Solid Board Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: United Kingdom Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Germany Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: France Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Italy Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Spain Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Global Solid Board Industry Revenue Million Forecast, by Product Grade 2020 & 2033

- Table 18: Global Solid Board Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 19: Global Solid Board Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 20: China Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: India Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Japan Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Australia and New Zealand Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Global Solid Board Industry Revenue Million Forecast, by Product Grade 2020 & 2033

- Table 25: Global Solid Board Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 26: Global Solid Board Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 27: Brazil Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Argentina Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: Mexico Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Global Solid Board Industry Revenue Million Forecast, by Product Grade 2020 & 2033

- Table 31: Global Solid Board Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 32: Global Solid Board Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 33: United Arab Emirates Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Saudi Arabia Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Egypt Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Solid Board Industry?

The projected CAGR is approximately 6.47%.

2. Which companies are prominent players in the Solid Board Industry?

Key companies in the market include Smurfit Kappa Group, Westrock Company, Graphic Packaging Holding Company, Mayr-Melnhof Karton AG (MM Group), Asia Pulp & Paper Group (APP), Pankaboard OYJ*List Not Exhaustive, International Paper Company, Stora Enso OYJ, Metsa Board, Nine Dragons Paper Holdings Limited.

3. What are the main segments of the Solid Board Industry?

The market segments include Product Grade, End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD 71.93 Million as of 2022.

5. What are some drivers contributing to market growth?

Strong Demand from the E-commerce Sector; Growing Demand for Lightweight Materials and Scope for Printing Innovations Propelling Growth in the Personal Care Segment.

6. What are the notable trends driving market growth?

The Beverage Segment is Expected to Record the Fastest Growth.

7. Are there any restraints impacting market growth?

Increasing Operational Costs.

8. Can you provide examples of recent developments in the market?

June 2023: Stora Enso opened a new corrugated board manufacturing facility in De Lier, the Netherlands. The site was part of the De Jong Packaging Group acquisition, later known as the Western Europe business unit within the Packaging Solutions Division. This massive expansion was designed with a strong focus on sustainable operations.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Solid Board Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Solid Board Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Solid Board Industry?

To stay informed about further developments, trends, and reports in the Solid Board Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence