Key Insights

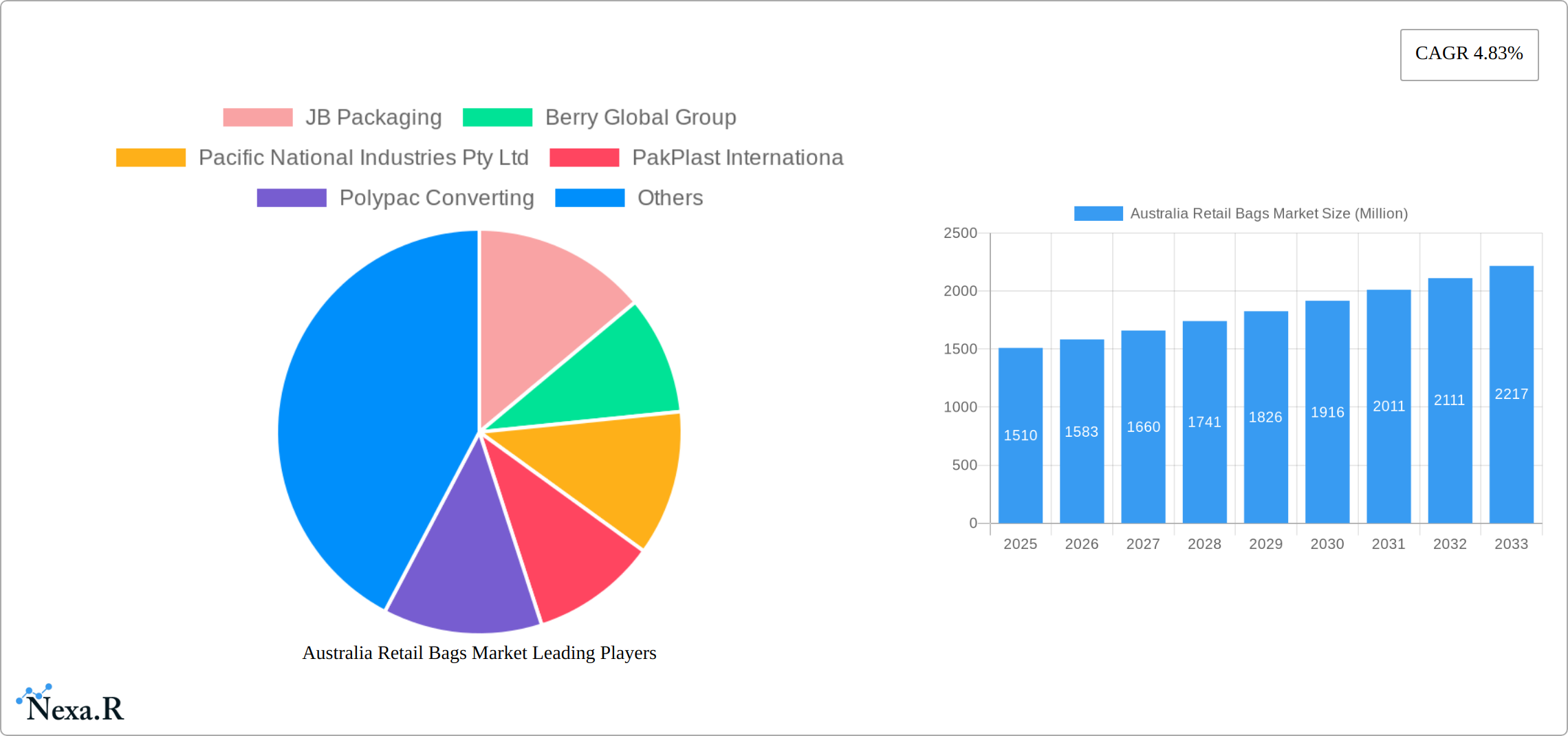

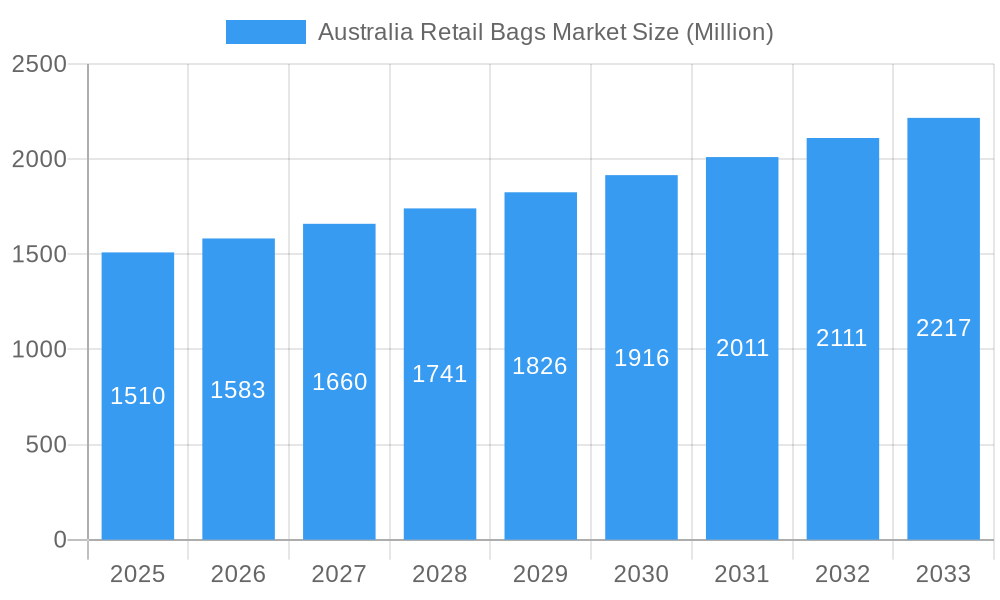

The Australian retail bags market, valued at $1.51 billion in 2025, is projected to experience steady growth, driven by a rising e-commerce sector and increasing consumer demand for convenient and sustainable packaging solutions. The market's Compound Annual Growth Rate (CAGR) of 4.83% from 2025 to 2033 indicates a consistent expansion, fueled by the increasing popularity of online shopping and the growing preference for eco-friendly alternatives like paper and natural fabric bags. Key segments within the market include paper and natural fabric bags, which are gaining traction due to growing environmental concerns, and plastic bags (HDPE, LDPE, PP, rPET, etc.), which continue to dominate due to their cost-effectiveness and versatility. The foodservice, grocery, and hospitality sectors are major end-users, contributing significantly to the overall market demand. Competition among established players like JB Packaging, Berry Global Group, and Pacific National Industries Pty Ltd, along with emerging players, fosters innovation and drives market expansion. However, fluctuating raw material prices and increasing environmental regulations present challenges to market growth. The continued focus on sustainability is likely to reshape the market landscape, with a higher emphasis on recycled and biodegradable materials in the coming years.

Australia Retail Bags Market Market Size (In Billion)

The forecast for the Australian retail bags market indicates a positive trajectory, with anticipated growth across various segments. The increasing adoption of sustainable packaging practices by businesses will create opportunities for manufacturers of eco-friendly retail bags. Furthermore, advancements in packaging technology, such as improved barrier properties and enhanced recyclability, are expected to influence the demand for specific bag types. Government initiatives promoting sustainability and waste reduction are likely to further accelerate the shift towards environmentally responsible packaging options. However, potential challenges include managing fluctuating raw material costs and ensuring compliance with evolving environmental regulations. Strategic partnerships, investment in research and development, and the adoption of innovative production processes will be crucial for businesses to maintain a competitive edge in this dynamic market.

Australia Retail Bags Market Company Market Share

Australia Retail Bags Market: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Australian retail bags market, offering invaluable insights for industry professionals, investors, and strategic decision-makers. The study covers the period from 2019 to 2033, with a focus on the base year 2025 and a forecast period spanning 2025-2033. The report segments the market by material (Paper and Natural Fabric, Plastic (HDPE, LDPE, PP, rPET, etc.)) and end-user industry (Foodservice, Grocery, Industrial, Hospitality, Other End-user Industries), providing a granular understanding of market dynamics and growth potential. The total market size is expected to reach xx Million units by 2033.

Australia Retail Bags Market Market Dynamics & Structure

The Australian retail bags market is characterized by a moderately concentrated landscape, with key players like JB Packaging, Berry Global Group, Pacific National Industries Pty Ltd, PakPlast International, Polypac Converting, Detmold Group, Gispac, United Paper, PrimePac, and Bag People Australia vying for market share. Technological innovation, particularly in sustainable and recyclable materials, is a major driver. Stringent environmental regulations are pushing the adoption of eco-friendly alternatives, while the increasing demand for convenient and aesthetically pleasing packaging influences product development. The market also witnesses significant M&A activity, with larger players acquiring smaller firms to expand their product portfolio and market reach. Competitive product substitutes, such as reusable bags and online delivery alternatives, pose a challenge.

- Market Concentration: Moderately concentrated, with the top 5 players holding approximately xx% market share in 2024.

- Technological Innovation: Strong focus on sustainable materials (rPET, recycled paper) and improved barrier properties.

- Regulatory Framework: Increasingly stringent regulations on single-use plastics are driving demand for eco-friendly alternatives.

- Competitive Substitutes: Reusable bags and online shopping present competitive pressures.

- End-User Demographics: Growing urban population and changing consumer preferences influence demand.

- M&A Trends: xx M&A deals recorded between 2019 and 2024, indicating consolidation within the sector.

Australia Retail Bags Market Growth Trends & Insights

The Australian retail bags market has witnessed consistent growth over the historical period (2019-2024), driven by factors such as rising consumer spending, increasing retail sales, and the expanding food service sector. The market size was xx Million units in 2024, exhibiting a CAGR of xx% during 2019-2024. Technological advancements, such as the introduction of innovative materials and improved manufacturing processes, have significantly enhanced the performance and functionality of retail bags. Shifting consumer preferences towards sustainable and eco-friendly options are impacting the demand for recyclable and biodegradable bags. Market penetration of sustainable bags is expected to increase from xx% in 2024 to xx% by 2033. The forecast period (2025-2033) is projected to witness continued growth, fueled by e-commerce expansion and the increasing focus on sustainability within the retail sector. The market is expected to reach xx Million units by 2033, with a projected CAGR of xx%.

Dominant Regions, Countries, or Segments in Australia Retail Bags Market

The Australian retail bags market is a dynamic landscape shaped by evolving consumer preferences and environmental concerns. The grocery sector remains the dominant end-user industry, accounting for a substantial portion of retail bag consumption, driven by the high volume of packaging needed in supermarkets and grocery stores. While plastic bags historically held the largest market share due to their cost-effectiveness and versatility, a significant shift is underway. The paper and natural fabric segments are experiencing robust growth, fueled by increasing consumer demand for eco-friendly alternatives and stricter regulations aimed at reducing plastic waste. This transition is particularly evident in major population centers. New South Wales and Victoria continue to be the leading states in terms of market size, reflecting their higher population densities and thriving retail sectors. However, growth is also being observed in other states as sustainability initiatives gain momentum across the country.

- Dominant End-User Industry: Grocery (Market share data for 2024 to be inserted here)

- Dominant Material Segment (by volume): Plastic (Market share data for 2024 to be inserted here); Dominant Material Segment (by growth): Paper & Natural Fabrics (Market share growth data for 2024 to be inserted here)

- Key Growth Drivers: The increasing consumer awareness of sustainability issues, coupled with stringent environmental regulations and ongoing technological advancements in eco-friendly materials, are the primary growth drivers. Furthermore, the rise of e-commerce is influencing the demand for specific types of retail bags suitable for online deliveries.

- Regional Dominance: New South Wales and Victoria maintain their leading positions due to higher population density and significant retail activity. However, growth is also observed in other states as sustainability practices are adopted more broadly.

Australia Retail Bags Market Product Landscape

The Australian retail bags market offers a diverse range of products designed to meet the varying needs of end-users. Innovation is heavily focused on enhancing sustainability, with biodegradable and compostable options rapidly gaining market share. Beyond sustainability, improvements in barrier properties to extend product shelf life and the availability of customized designs are also key features driving product differentiation. This differentiation extends to material composition, size, design aesthetics, and printing capabilities. Advancements in printing technology allow for high-quality branding and customized designs, enabling businesses to enhance brand visibility and consumer appeal. The market is responding to the demand for both functional and visually appealing packaging solutions.

Key Drivers, Barriers & Challenges in Australia Retail Bags Market

Key Drivers:

- Growing consumer demand for convenient, attractive, and sustainable packaging.

- Increasingly stringent focus on sustainability and the implementation of related environmental regulations.

- Technological advancements in sustainable materials and efficient manufacturing processes.

- The continued expansion of e-commerce and the growth of online retail, creating demand for specialized packaging solutions.

- Government incentives and support for sustainable packaging alternatives.

Key Challenges:

- Fluctuations in raw material prices, impacting production costs.

- The complexity and cost of complying with stringent regulatory requirements for sustainable materials and certifications.

- Competition from substitute products such as reusable bags and the increasing popularity of online deliveries, which reduce reliance on single-use bags.

- Supply chain disruptions, potentially affecting the availability and cost of raw materials and finished products.

- Educating consumers about the benefits and proper disposal of eco-friendly bag options.

Emerging Opportunities in Australia Retail Bags Market

- Growing demand for customizable and branded bags.

- Increased adoption of biodegradable and compostable materials.

- Expansion into niche markets such as luxury retail and e-commerce packaging.

- Development of innovative bag designs that enhance product preservation and shelf life.

Growth Accelerators in the Australia Retail Bags Market Industry

Long-term growth is propelled by increasing environmental awareness leading to a preference for sustainable bags, advancements in recyclable material technology, and strategic partnerships between bag manufacturers and retailers focusing on sustainable packaging solutions. Expansion into new market segments like e-commerce and premium retail will also fuel market growth.

Key Players Shaping the Australia Retail Bags Market Market

- JB Packaging

- Berry Global Group (Berry Global Group)

- Pacific National Industries Pty Ltd

- PakPlast International

- Polypac Converting

- Detmold Group

- Gispac

- United Paper

- PrimePac

- Bag People Australia

Notable Milestones in Australia Retail Bags Market Sector

- March 2024: Visy's launch of recyclable paper bags made in Australia signifies a significant step towards promoting sustainability and reducing reliance on single-use plastics.

- April 2024: W23 Global's launch of a USD125 million VC fund focused on innovative and sustainable grocery retail start-ups will indirectly stimulate demand for eco-friendly retail bags.

- Add other relevant milestones here with dates and brief descriptions.

In-Depth Australia Retail Bags Market Market Outlook

The Australian retail bags market is poised for substantial growth in the coming years. The increasing focus on sustainability will drive the demand for eco-friendly alternatives, while technological innovations will lead to the development of more efficient and cost-effective packaging solutions. Strategic partnerships and collaborations within the industry will play a crucial role in shaping the future of this dynamic market, creating significant opportunities for both established players and new entrants.

Australia Retail Bags Market Segmentation

-

1. Material

- 1.1. Paper and Natural Fabric

- 1.2. Plastic (HDPE, LDPE, PP, rPET, etc.)

-

2. End-user Industry

- 2.1. Foodservice

- 2.2. Grocery

- 2.3. Industrial

- 2.4. Hospitality

- 2.5. Other End-user Industries

Australia Retail Bags Market Segmentation By Geography

- 1. Australia

Australia Retail Bags Market Regional Market Share

Geographic Coverage of Australia Retail Bags Market

Australia Retail Bags Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.83% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material

- 5.1.1. Paper and Natural Fabric

- 5.1.2. Plastic (HDPE, LDPE, PP, rPET, etc.)

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Foodservice

- 5.2.2. Grocery

- 5.2.3. Industrial

- 5.2.4. Hospitality

- 5.2.5. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Australia

- 5.1. Market Analysis, Insights and Forecast - by Material

- 6. Australia Retail Bags Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material

- 6.1.1. Paper and Natural Fabric

- 6.1.2. Plastic (HDPE, LDPE, PP, rPET, etc.)

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Foodservice

- 6.2.2. Grocery

- 6.2.3. Industrial

- 6.2.4. Hospitality

- 6.2.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Material

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 JB Packaging

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Berry Global Group

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Pacific National Industries Pty Ltd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 PakPlast Internationa

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Polypac Converting

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Detmold Group

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Gispac

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 United Paper

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 PrimePac

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Bag People Australia

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 JB Packaging

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Australia Retail Bags Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Australia Retail Bags Market Share (%) by Company 2025

List of Tables

- Table 1: Australia Retail Bags Market Revenue Million Forecast, by Material 2020 & 2033

- Table 2: Australia Retail Bags Market Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 3: Australia Retail Bags Market Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Australia Retail Bags Market Revenue Million Forecast, by Material 2020 & 2033

- Table 5: Australia Retail Bags Market Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 6: Australia Retail Bags Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Australia Retail Bags Market?

The projected CAGR is approximately 4.83%.

2. Which companies are prominent players in the Australia Retail Bags Market?

Key companies in the market include JB Packaging, Berry Global Group, Pacific National Industries Pty Ltd, PakPlast Internationa, Polypac Converting, Detmold Group, Gispac, United Paper, PrimePac, Bag People Australia.

3. What are the main segments of the Australia Retail Bags Market?

The market segments include Material, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.51 Million as of 2022.

5. What are some drivers contributing to market growth?

The Growing Demand for Unit-sized Bags is Expected to Drive Growth; Legislative Changes will Propel the Growth of Paper-based Bags (State-wise Ban on Plastic Bags <35 microns).

6. What are the notable trends driving market growth?

Paper and Natural Fabric to Witness Significant Growth.

7. Are there any restraints impacting market growth?

Near and Medium-term Dependence on Material Prices and the Dynamic Nature of the End-user Demand Expected to Pose Challenges; Anticipated Barriers to Entry for New Entrants Posed by Incumbents who have Established Partnerships with Retailers in the Country.

8. Can you provide examples of recent developments in the market?

April 2024 - W23 Global unites five major players in the global grocery arena. Ahold Delhaize (operating in the US, Europe, and Indonesia), Tesco (based in the UK, ROI, and Europe), Woolworths Group (hailing from Australia and New Zealand), Empire Company Limited/Sobeys Inc. (representing Canada), and Shoprite Group (focused on Africa). This collaborative effort has birthed a new retail venture capital (VC) fund, aiming to invest USD125 million into the most innovative start-ups and scale-ups worldwide over the next five years. These investments are specifically targeted at revolutionizing the grocery retail landscape and tackling its sustainability challenges head-on.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Australia Retail Bags Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Australia Retail Bags Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Australia Retail Bags Market?

To stay informed about further developments, trends, and reports in the Australia Retail Bags Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence