Key Insights

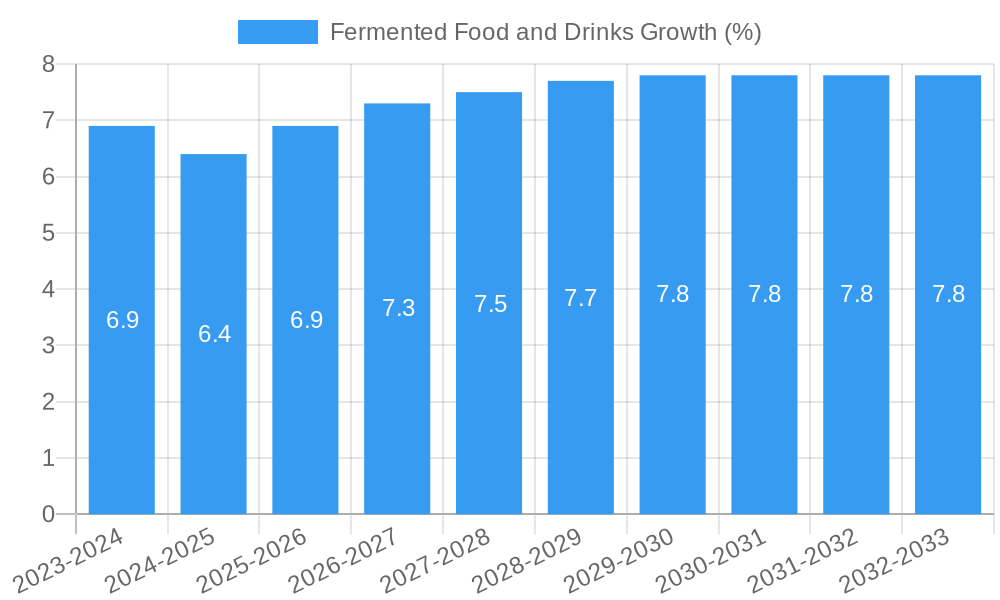

The global fermented food and drinks market is poised for robust expansion, projected to reach a significant market size of approximately $580 million by 2025, with an anticipated Compound Annual Growth Rate (CAGR) of around 7.5% through 2033. This growth is fueled by an escalating consumer demand for healthier and more natural food options, driven by a growing awareness of the positive impact of probiotics and gut health on overall well-being. Key market drivers include the rising popularity of functional foods and beverages, innovative product development in both alcoholic and non-alcoholic categories, and the increasing accessibility of fermented products through diverse retail channels, including online platforms and specialty stores. The market is experiencing a dynamic shift towards premium and artisanal offerings, alongside a surge in plant-based fermented alternatives, catering to evolving dietary preferences and ethical considerations.

The market's trajectory is further shaped by several compelling trends. The burgeoning interest in gut health and the microbiome has propelled fermented foods from niche products to mainstream staples. Consumers are actively seeking out ingredients known for their digestive benefits, such as probiotics and prebiotics, which are abundant in fermented items like yogurt, kefir, kimchi, and kombucha. Technological advancements in fermentation processes are enabling greater product consistency and shelf-life, further driving adoption. While significant growth opportunities exist, the market faces certain restraints. These include potential challenges related to maintaining consistent quality and taste profiles across mass production, the need for consumer education regarding the benefits and consumption of certain fermented products, and stringent regulatory frameworks in some regions concerning novel food ingredients and production standards. Despite these hurdles, the overarching consumer shift towards health-conscious choices and the continuous innovation by major players like General Mills, Heineken, and Danone ensure a dynamic and promising future for the fermented food and drinks sector.

Fermented Food and Drinks Market Analysis: Trends, Opportunities, and Key Players (2019-2033)

This comprehensive report delves into the dynamic global fermented food and drinks market, offering an in-depth analysis of its growth trajectory, key drivers, and emerging opportunities. Covering the period from 2019 to 2033, with a base year of 2025, this report provides actionable insights for industry professionals seeking to navigate this rapidly expanding sector. We examine the market's structure, technological innovations, consumer behavior shifts, and the competitive landscape, with a specific focus on parent and child market segments to uncover nuanced growth potentials.

Fermented Food and Drinks Market Dynamics & Structure

The global fermented food and drinks market is characterized by a moderate to high concentration, with key players like General Mills, Heineken, Kraft Heinz, Danone, Anheuser-Busch InBev, Carlsberg Group, and Constellation Brands holding significant market shares. Technological innovation is a primary driver, with advancements in fermentation processes, probiotic strain development, and shelf-life extension technologies significantly impacting product development and consumer appeal. Regulatory frameworks, while varying by region, are generally supportive of food safety and product labeling, fostering consumer trust. Competitive product substitutes, particularly in the non-alcoholic beverage and plant-based food categories, present a growing challenge, necessitating continuous innovation. End-user demographics show a rising demand from health-conscious millennials and Gen Z consumers actively seeking gut-friendly and natural food options. Mergers and acquisition (M&A) trends are also evident, as larger corporations seek to expand their portfolios and gain access to innovative startups and specialized product lines. For instance, the past few years have seen an estimated 15-20 M&A deals within the fermented foods sector, indicating consolidation and strategic growth. Barriers to innovation often include the complexity of maintaining consistent fermentation cultures, stringent quality control requirements, and the need for consumer education regarding the benefits of fermented products.

Fermented Food and Drinks Growth Trends & Insights

The global fermented food and drinks market is poised for robust growth, projected to reach an estimated value of $XXX billion by 2033. This expansion is fueled by a confluence of factors, including escalating consumer awareness of the health benefits associated with gut microbiome health, the increasing demand for natural and minimally processed foods, and the growing popularity of diverse fermented product categories. The market penetration of fermented foods and drinks, historically focused on traditional items like yogurt and sauerkraut, is rapidly diversifying to encompass a broader spectrum of products, including kombucha, kimchi, kefir, fermented plant-based alternatives, and a wide array of artisanal fermented beverages. The CAGR for the forecast period (2025-2033) is estimated at XX%, reflecting sustained expansion. Technological disruptions are playing a pivotal role, with advancements in rapid fermentation techniques, the isolation and application of specific probiotic strains for targeted health benefits, and improved packaging solutions that enhance shelf stability and product quality. Consumer behavior shifts are marked by a growing preference for functional foods and beverages that offer more than just nutritional value. Consumers are actively seeking products that can support digestive health, boost immunity, and contribute to overall well-being. This trend is particularly pronounced in the younger demographics, who are more open to exploring novel food and beverage experiences and are influenced by health and wellness trends prevalent on social media. The "probiotic revolution" has firmly established fermented foods and drinks as a mainstream category, moving beyond niche markets to become integral components of daily diets. The increasing availability of these products across various retail channels, from hypermarkets to online platforms, further amplifies their adoption rates. The historical period (2019-2024) witnessed a steady upward trend, setting a strong foundation for the accelerated growth expected in the coming years.

Dominant Regions, Countries, or Segments in Fermented Food and Drinks

The global fermented food and drinks market's dominance is intricately linked to a combination of established consumer habits, supportive economic policies, and robust distribution networks. Among the application segments, Hypermarkets and Supermarkets currently hold the largest market share, estimated at XX% in 2025, due to their extensive reach and ability to cater to a broad consumer base seeking convenience and variety. Specialty Food Stores follow, capturing consumers willing to pay a premium for artisanal and unique fermented products. Online Retailers are experiencing the fastest growth, projected to surge from XX% in 2025 to an estimated XX% by 2033, driven by convenience and the expanding product portfolios offered by e-commerce platforms.

In terms of product Types, Dairy Food and Drinks continue to be a dominant segment, accounting for approximately XX% of the market in 2025, owing to the widespread popularity of yogurt, cheese, and kefir. However, Alcoholic and Non-Alcoholic Drinks are rapidly gaining traction, with alcoholic fermented beverages like beer and wine, and non-alcoholic options such as kombucha and probiotic sodas, witnessing significant growth. The non-alcoholic segment, in particular, is projected to experience a CAGR of XX% during the forecast period. Bakery Foods, while a smaller segment, are seeing innovation with the incorporation of sourdough and other fermented elements.

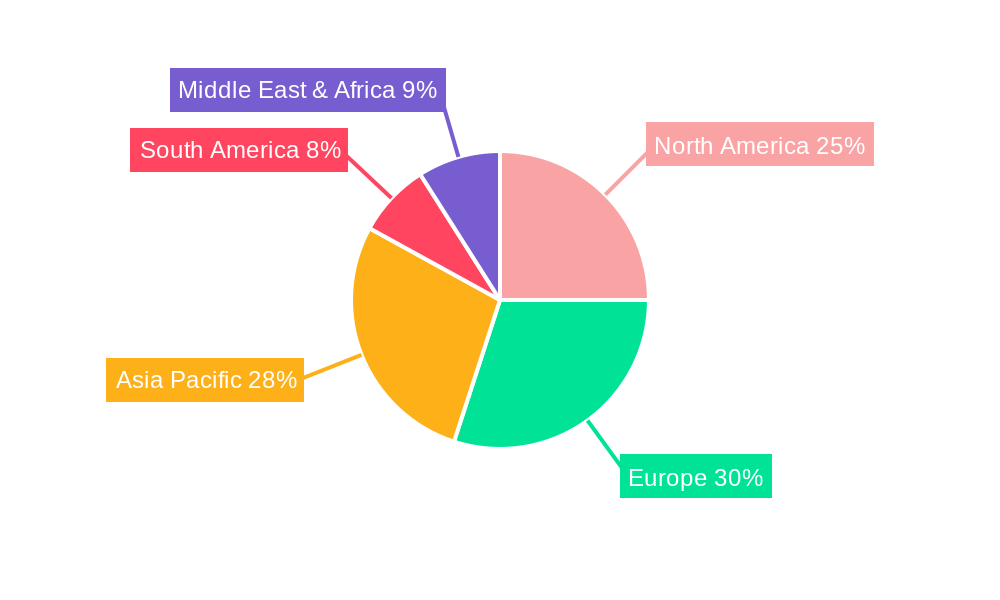

Geographically, North America and Europe are leading regions, collectively holding an estimated XX% of the global market share in 2025. These regions benefit from high consumer awareness regarding health and wellness, a well-developed food infrastructure, and significant investments in research and development of fermented products.

- Key Drivers in North America & Europe:

- High Disposable Income: Enables consumers to opt for premium and health-oriented fermented products.

- Strong Health and Wellness Trends: A cultural emphasis on gut health and natural foods.

- Advanced Retail Infrastructure: Well-established hypermarkets, supermarkets, and sophisticated online retail channels.

- Proactive Regulatory Environments: Favorable policies supporting food innovation and labeling.

Asia-Pacific is emerging as a significant growth engine, driven by its large population, increasing urbanization, and rising middle class with growing purchasing power and adoption of Western dietary trends. Countries like China and India are witnessing a surge in demand for fermented products, both traditional and Westernized.

Fermented Food and Drinks Product Landscape

The fermented food and drinks product landscape is characterized by a continuous stream of innovations driven by consumer demand for novel flavors, enhanced nutritional profiles, and functional benefits. Key product developments include the expansion of plant-based fermented alternatives, such as almond-based yogurts and coconut kefir, catering to vegan and lactose-intolerant consumers. Probiotic-rich beverages like kombucha and water kefir are evolving with exotic fruit infusions and functional add-ins like adaptogens. The application of advanced fermentation techniques is leading to improved texture, taste, and shelf-life for products like fermented vegetables and artisanal sourdough breads. Performance metrics are increasingly focused on probiotic counts, digestive enzyme activity, and the presence of beneficial metabolites. Unique selling propositions often revolve around artisanal production methods, specific strain identification for targeted health benefits, and sustainable sourcing of ingredients.

Key Drivers, Barriers & Challenges in Fermented Food and Drinks

Key Drivers: The fermented food and drinks market is propelled by several key drivers. The escalating consumer awareness of the profound health benefits associated with a healthy gut microbiome is a primary catalyst, fueling demand for probiotic-rich foods and beverages. The growing global trend towards natural, minimally processed, and functional foods further strengthens this market. Technological advancements in fermentation processes, including the development of specific probiotic strains for targeted health outcomes and improved production efficiency, are also significant growth accelerators. Economic factors, such as rising disposable incomes in emerging economies, are enabling wider access to these often premium products.

- Technological Advancements: Innovations in strain selection, rapid fermentation, and shelf-life extension.

- Health and Wellness Trend: Increased consumer focus on gut health, immunity, and natural ingredients.

- Dietary Preferences: Growing adoption of plant-based and allergen-free fermented options.

- Emerging Market Growth: Rising disposable incomes and changing dietary habits in developing nations.

Barriers & Challenges: Despite its growth, the market faces several challenges. Consistency in fermentation and quality control across diverse product lines remains a significant hurdle, impacting shelf-life and consumer trust. Supply chain complexities, particularly for sourcing specialized ingredients and maintaining cold chains for certain products, can pose logistical issues. Stringent and varied regulatory frameworks across different countries can complicate product approvals and market entry. Intense competition from established food and beverage giants as well as agile startups, coupled with the need for effective consumer education about the benefits and proper consumption of fermented products, also presents considerable challenges.

- Supply Chain Issues: Sourcing specialized cultures, maintaining cold chain logistics.

- Regulatory Hurdles: Navigating diverse international food safety and labeling regulations.

- Consumer Education: Explaining the benefits and usage of novel fermented products.

- Shelf-Life and Stability: Ensuring consistent quality and efficacy over time.

- Competitive Landscape: Intense rivalry from both established players and innovative newcomers.

Emerging Opportunities in Fermented Food and Drinks

Emerging opportunities in the fermented food and drinks industry are diverse and promising. There is significant potential in developing fermented products tailored for specific dietary needs, such as low-FODMAP fermented foods for individuals with digestive sensitivities. The burgeoning plant-based food market offers a fertile ground for innovation in dairy-free fermented alternatives like oat-based kefirs and cashew-based yogurts. Furthermore, exploring novel fermentation substrates and utilizing underutilized ingredients can lead to unique and sustainable product offerings. The functional beverage segment is ripe for expansion, with opportunities in fermented drinks fortified with vitamins, minerals, and other bioactive compounds for enhanced health benefits. The integration of fermented ingredients into snack bars, condiments, and meal kits also presents a substantial untapped market.

Growth Accelerators in the Fermented Food and Drinks Industry

The fermented food and drinks industry is experiencing sustained growth driven by several key accelerators. Technological breakthroughs in precision fermentation, allowing for the production of specific beneficial compounds and flavors, are revolutionizing product development. Strategic partnerships between ingredient suppliers, manufacturers, and research institutions are fostering innovation and accelerating the commercialization of new fermented products. Market expansion strategies, particularly targeting underserved regions and demographics, are opening up new avenues for growth. The increasing demand for sustainable and ethically produced food options aligns perfectly with traditional fermentation processes, further boosting the industry's appeal. Continuous investment in R&D for novel strains and applications is critical for maintaining competitive advantage and driving long-term market expansion.

Key Players Shaping the Fermented Food and Drinks Market

- General Mills

- Heineken

- Kraft Heinz

- Danone

- Anheuser-Busch InBev

- Carlsberg Group

- Constellation Brands

Notable Milestones in Fermented Food and Drinks Sector

- 2019: Increased consumer interest in gut health and probiotics drives growth in kombucha and kefir markets.

- 2020: Launch of new plant-based fermented dairy alternatives by major dairy companies.

- 2021: Significant investment in startups developing novel fermentation technologies.

- 2022: Growing popularity of kimchi and other fermented vegetables in Western markets.

- 2023: Advancements in personalized nutrition incorporating fermented foods for specific health benefits.

- 2024: Expansion of fermented beverage categories beyond traditional alcohol and kombucha.

In-Depth Fermented Food and Drinks Market Outlook

The outlook for the fermented food and drinks market remains exceptionally strong, driven by an enduring consumer shift towards health and wellness. Future growth accelerators will be deeply rooted in continued technological innovation, particularly in precision fermentation and the development of targeted probiotic strains. Strategic partnerships will be crucial for unlocking new product categories and expanding global reach. Market expansion into emerging economies, coupled with an increasing demand for sustainable and natural food options, will provide significant growth impetus. The industry is well-positioned to capitalize on evolving consumer preferences for functional foods, personalized nutrition, and plant-based alternatives, ensuring a trajectory of sustained and dynamic expansion in the coming years.

Fermented Food and Drinks Segmentation

-

1. Application

- 1.1. Hypermarkets and Supermarkets

- 1.2. Specialty Food Stores

- 1.3. Independent Retailers

- 1.4. Online Retailers

-

2. Types

- 2.1. Alcoholic and Non-Alcoholic Drinks

- 2.2. Dairy Food and Drinks

- 2.3. Bakery Foods

- 2.4. Other

Fermented Food and Drinks Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Fermented Food and Drinks REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Fermented Food and Drinks Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hypermarkets and Supermarkets

- 5.1.2. Specialty Food Stores

- 5.1.3. Independent Retailers

- 5.1.4. Online Retailers

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Alcoholic and Non-Alcoholic Drinks

- 5.2.2. Dairy Food and Drinks

- 5.2.3. Bakery Foods

- 5.2.4. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Fermented Food and Drinks Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hypermarkets and Supermarkets

- 6.1.2. Specialty Food Stores

- 6.1.3. Independent Retailers

- 6.1.4. Online Retailers

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Alcoholic and Non-Alcoholic Drinks

- 6.2.2. Dairy Food and Drinks

- 6.2.3. Bakery Foods

- 6.2.4. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Fermented Food and Drinks Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hypermarkets and Supermarkets

- 7.1.2. Specialty Food Stores

- 7.1.3. Independent Retailers

- 7.1.4. Online Retailers

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Alcoholic and Non-Alcoholic Drinks

- 7.2.2. Dairy Food and Drinks

- 7.2.3. Bakery Foods

- 7.2.4. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Fermented Food and Drinks Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hypermarkets and Supermarkets

- 8.1.2. Specialty Food Stores

- 8.1.3. Independent Retailers

- 8.1.4. Online Retailers

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Alcoholic and Non-Alcoholic Drinks

- 8.2.2. Dairy Food and Drinks

- 8.2.3. Bakery Foods

- 8.2.4. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Fermented Food and Drinks Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hypermarkets and Supermarkets

- 9.1.2. Specialty Food Stores

- 9.1.3. Independent Retailers

- 9.1.4. Online Retailers

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Alcoholic and Non-Alcoholic Drinks

- 9.2.2. Dairy Food and Drinks

- 9.2.3. Bakery Foods

- 9.2.4. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Fermented Food and Drinks Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hypermarkets and Supermarkets

- 10.1.2. Specialty Food Stores

- 10.1.3. Independent Retailers

- 10.1.4. Online Retailers

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Alcoholic and Non-Alcoholic Drinks

- 10.2.2. Dairy Food and Drinks

- 10.2.3. Bakery Foods

- 10.2.4. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 General Mills

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Heineken

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Kraft Heinz

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Danone

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Anheuser-Busch InBev

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Carlsberg Group

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Constellation Brands

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.1 General Mills

List of Figures

- Figure 1: Global Fermented Food and Drinks Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Fermented Food and Drinks Revenue (million), by Application 2024 & 2032

- Figure 3: North America Fermented Food and Drinks Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Fermented Food and Drinks Revenue (million), by Types 2024 & 2032

- Figure 5: North America Fermented Food and Drinks Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Fermented Food and Drinks Revenue (million), by Country 2024 & 2032

- Figure 7: North America Fermented Food and Drinks Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Fermented Food and Drinks Revenue (million), by Application 2024 & 2032

- Figure 9: South America Fermented Food and Drinks Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Fermented Food and Drinks Revenue (million), by Types 2024 & 2032

- Figure 11: South America Fermented Food and Drinks Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Fermented Food and Drinks Revenue (million), by Country 2024 & 2032

- Figure 13: South America Fermented Food and Drinks Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Fermented Food and Drinks Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Fermented Food and Drinks Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Fermented Food and Drinks Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Fermented Food and Drinks Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Fermented Food and Drinks Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Fermented Food and Drinks Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Fermented Food and Drinks Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Fermented Food and Drinks Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Fermented Food and Drinks Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Fermented Food and Drinks Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Fermented Food and Drinks Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Fermented Food and Drinks Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Fermented Food and Drinks Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Fermented Food and Drinks Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Fermented Food and Drinks Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Fermented Food and Drinks Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Fermented Food and Drinks Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Fermented Food and Drinks Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Fermented Food and Drinks Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Fermented Food and Drinks Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Fermented Food and Drinks Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Fermented Food and Drinks Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Fermented Food and Drinks Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Fermented Food and Drinks Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Fermented Food and Drinks Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Fermented Food and Drinks Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Fermented Food and Drinks Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Fermented Food and Drinks Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Fermented Food and Drinks Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Fermented Food and Drinks Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Fermented Food and Drinks Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Fermented Food and Drinks Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Fermented Food and Drinks Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Fermented Food and Drinks Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Fermented Food and Drinks Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Fermented Food and Drinks Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Fermented Food and Drinks Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Fermented Food and Drinks Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Fermented Food and Drinks Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Fermented Food and Drinks Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Fermented Food and Drinks Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Fermented Food and Drinks Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Fermented Food and Drinks Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Fermented Food and Drinks Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Fermented Food and Drinks Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Fermented Food and Drinks Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Fermented Food and Drinks Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Fermented Food and Drinks Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Fermented Food and Drinks Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Fermented Food and Drinks Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Fermented Food and Drinks Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Fermented Food and Drinks Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Fermented Food and Drinks Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Fermented Food and Drinks Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Fermented Food and Drinks Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Fermented Food and Drinks Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Fermented Food and Drinks Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Fermented Food and Drinks Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Fermented Food and Drinks Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Fermented Food and Drinks Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Fermented Food and Drinks Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Fermented Food and Drinks Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Fermented Food and Drinks Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Fermented Food and Drinks Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Fermented Food and Drinks Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Fermented Food and Drinks?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Fermented Food and Drinks?

Key companies in the market include General Mills, Heineken, Kraft Heinz, Danone, Anheuser-Busch InBev, Carlsberg Group, Constellation Brands.

3. What are the main segments of the Fermented Food and Drinks?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5600.00, USD 8400.00, and USD 11200.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Fermented Food and Drinks," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Fermented Food and Drinks report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Fermented Food and Drinks?

To stay informed about further developments, trends, and reports in the Fermented Food and Drinks, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence