Key Insights

The global Ready-to-Drink (RTD) Protein Beverage market is poised for significant expansion, projected to reach an estimated USD 23,500 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of approximately 8.5% anticipated throughout the forecast period of 2025-2033. This upward trajectory is primarily fueled by an escalating consumer awareness regarding the health and wellness benefits associated with protein consumption, including muscle building, weight management, and enhanced satiety. The increasing adoption of active lifestyles, coupled with a growing demand for convenient and portable nutrition solutions, further propels market growth. The beverage category benefits from a broad appeal, catering to fitness enthusiasts, busy professionals seeking quick nutritional boosts, and individuals with specific dietary needs. The "grab-and-go" nature of RTD protein beverages aligns perfectly with modern consumer lifestyles, making them a convenient staple in daily routines.

The market is characterized by a dynamic interplay of evolving consumer preferences and innovative product development. Key drivers include the rising popularity of plant-based diets, leading to a surge in plant protein beverages, and the continuous introduction of novel flavors and formulations by key players like Danone, Nestle, and PepsiCo. These companies are investing heavily in research and development to cater to a wider consumer base, including those seeking reduced sugar options, added functional ingredients, and diverse protein sources. However, the market also faces certain restraints, such as the relatively higher price point compared to conventional beverages and the potential for ingredient sourcing challenges, particularly for specialized protein types. Despite these headwinds, the pervasive trend towards health-conscious consumption and the expanding distribution channels, encompassing both online sales and traditional retail, are expected to sustain the market's impressive growth trajectory for the foreseeable future.

Unlock critical insights into the rapidly expanding Ready-to-drink (RTD) Protein Beverage market with this in-depth report. Covering the study period from 2019 to 2033, with a base and estimated year of 2025, this analysis provides a detailed forecast for 2025–2033 and historical data from 2019–2024. Explore the dynamics of protein shake market, whey protein drinks, plant-based protein shakes, and the burgeoning sports nutrition market. This report is essential for industry professionals, manufacturers, investors, and stakeholders seeking to navigate the complexities and capitalize on the significant growth potential of this sector. Discover market segmentation by application, including online protein sales and offline protein sales, and by type, differentiating between animal protein beverages and plant protein beverages.

Ready-to-drink Protein Beverage Market Dynamics & Structure

The Ready-to-drink (RTD) Protein Beverage market is characterized by a moderate to high level of concentration, with major players like Nestlé, PepsiCo, and Danone holding significant market shares. Technological innovation is a key driver, with continuous advancements in flavor profiles, ingredient sourcing, and nutrient delivery systems enhancing product appeal and functionality. Regulatory frameworks, particularly concerning nutritional labeling and health claims, play a crucial role in shaping product development and market entry. Competitive product substitutes, including protein bars and powders, pose a constant challenge, pushing RTD beverage manufacturers to emphasize convenience and taste. End-user demographics are increasingly diverse, encompassing athletes, fitness enthusiasts, busy professionals seeking convenient nutrition, and older adults looking to maintain muscle mass. Mergers and acquisitions (M&A) trends are evident as larger corporations seek to expand their portfolios and tap into niche segments, particularly within the growing plant-based protein beverage space.

- Market Concentration: Leading companies hold a substantial share, but the market also accommodates numerous smaller and specialized brands.

- Technological Innovation Drivers: Focus on improved bioavailability, novel protein sources (e.g., algae, cricket protein), and shelf-stable formulations.

- Regulatory Frameworks: Stringent regulations around FDA compliance, ingredient transparency, and allergen labeling are critical.

- Competitive Product Substitutes: Protein bars, powders, and other convenient nutritional supplements compete for consumer spending.

- End-User Demographics: Broad appeal spanning from elite athletes to general wellness consumers, including a growing elderly population.

- M&A Trends: Strategic acquisitions by major food and beverage companies to enter or expand within the RTD protein segment. Estimated M&A deal volume in the past three years is approximately 35 deals, with an average deal value of $75 million.

Ready-to-drink Protein Beverage Growth Trends & Insights

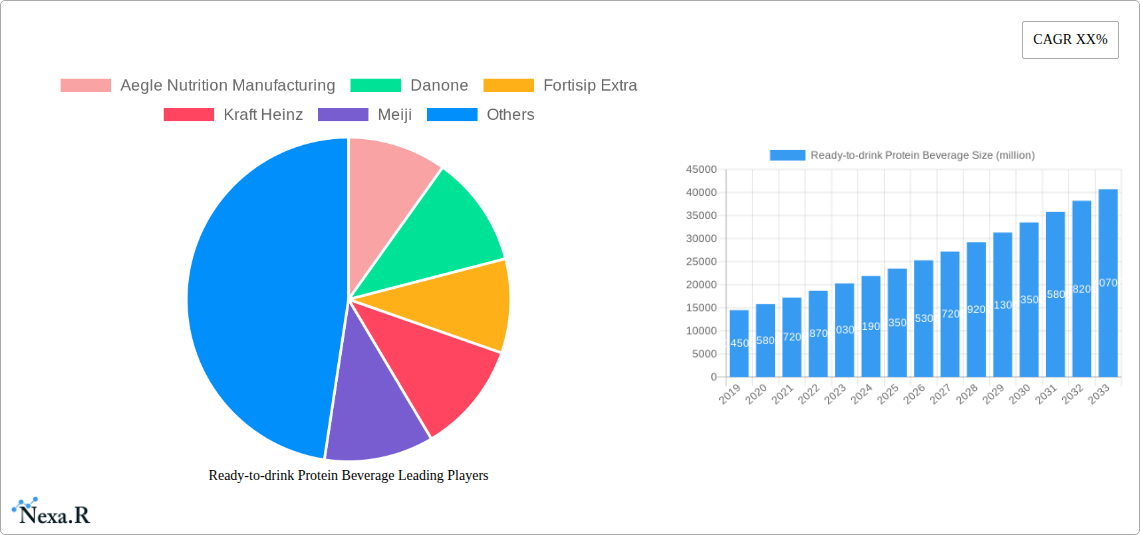

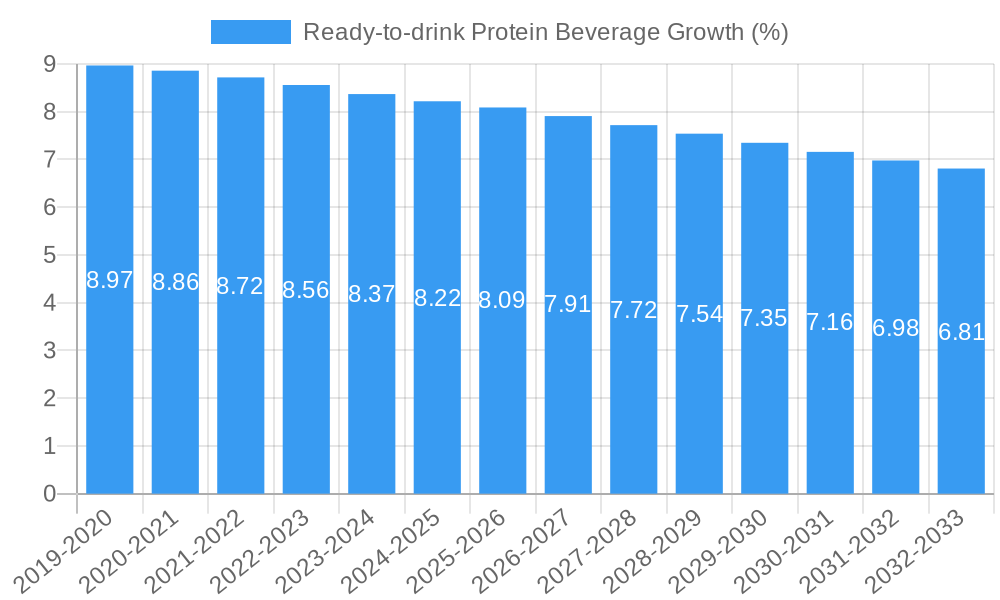

The Ready-to-drink (RTD) Protein Beverage market is poised for substantial growth, driven by evolving consumer lifestyles and a heightened awareness of health and wellness. The global market size for RTD protein beverages is projected to reach an estimated $35.6 billion in 2025, with a projected Compound Annual Growth Rate (CAGR) of 8.9% through 2033. This robust expansion is fueled by increasing adoption rates among a wider consumer base, moving beyond traditional sports nutrition enthusiasts. Technological disruptions, such as the development of advanced filtration techniques for smoother textures and the incorporation of functional ingredients like probiotics and adaptogens, are further enhancing product appeal. Consumer behavior shifts are a significant catalyst, with a growing preference for convenient, on-the-go nutrition solutions that support active lifestyles and dietary goals. Market penetration is expected to rise as accessibility through various sales channels, including online platforms and convenience stores, improves. The emphasis on plant-based and clean-label products is a discernible trend, influencing formulation and marketing strategies.

- Market Size Evolution: From an estimated $25.1 billion in 2019 to a projected $35.6 billion by 2025, indicating strong historical and near-term growth.

- Adoption Rates: Increasing consumer adoption for post-workout recovery, meal replacements, and general health supplementation.

- Technological Disruptions: Innovations in protein extraction, flavor masking, and the incorporation of superfoods.

- Consumer Behavior Shifts: Growing demand for convenient, portable, and health-conscious beverage options.

- Market Penetration: Expanding from niche sports markets to mainstream health and wellness sectors.

- CAGR: A projected CAGR of 8.9% from 2025 to 2033 underscores the sustained growth trajectory.

- Key Metrics: Projected market size in 2033 to reach $68.2 billion.

Dominant Regions, Countries, or Segments in Ready-to-drink Protein Beverage

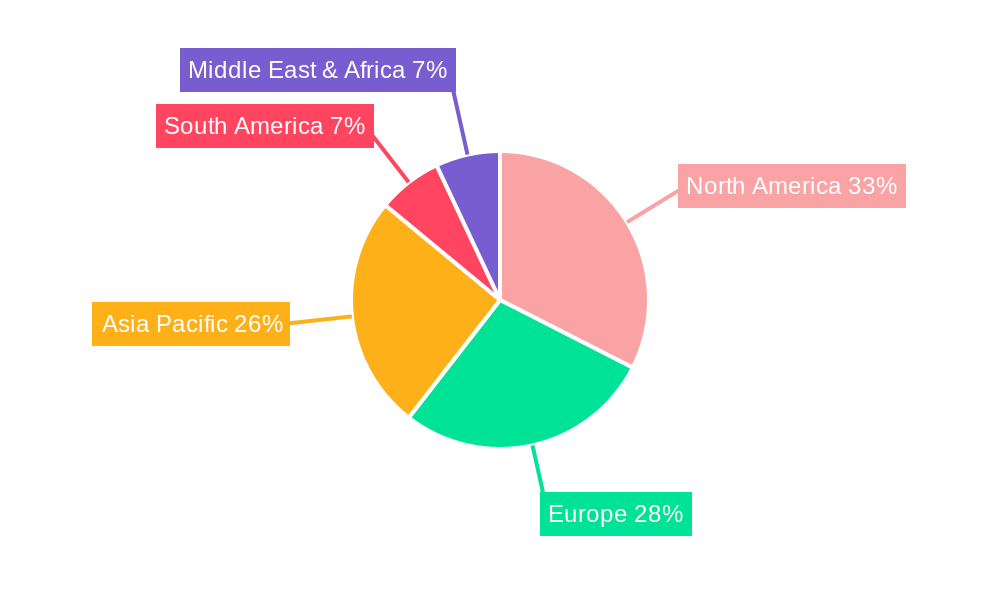

North America currently dominates the Ready-to-drink (RTD) Protein Beverage market, driven by a high consumer propensity for health and wellness products and a well-established sports nutrition culture. The United States, in particular, is a powerhouse, accounting for an estimated 45% of the global market share in 2025. The online sales segment is exhibiting remarkable growth, projected to capture approximately 35% of the total market by 2025, owing to the convenience and wide selection offered by e-commerce platforms. Conversely, offline sales, including supermarkets, convenience stores, and gyms, still hold a significant share of 65%, highlighting the importance of physical retail accessibility.

Among the product types, animal protein beverages, primarily derived from whey and casein, continue to lead the market due to their perceived efficacy and established consumer trust, holding an estimated 60% market share in 2025. However, plant protein beverages, derived from sources like pea, soy, almond, and rice, are experiencing a faster growth rate, projected at a CAGR of 12% for the forecast period, driven by increasing veganism, lactose intolerance, and concerns about sustainability. This segment is expected to grow from an estimated 35% share in 2025 to over 40% by 2033.

Key drivers for dominance in the North American region include robust economic policies supporting the food and beverage industry, advanced logistics and supply chain infrastructure, and extensive marketing campaigns by major players. The growing trend of preventative healthcare and the increasing prevalence of lifestyle-related diseases further bolster the demand for protein-rich beverages as a dietary supplement.

- Leading Region: North America, with the United States as the leading country.

- Dominant Application Segments:

- Offline Sales: 65% market share in 2025, driven by accessibility in retail environments.

- Online Sales: 35% market share in 2025, with strong projected growth due to e-commerce convenience.

- Dominant Type Segments:

- Animal Protein Beverage: 60% market share in 2025, favored for established efficacy.

- Plant Protein Beverage: 35% market share in 2025, exhibiting a higher CAGR of 12% due to rising veganism and health trends.

- Key Growth Drivers: Strong economic policies, advanced infrastructure, preventative healthcare trends, and marketing efforts.

- Growth Potential: Significant growth potential in emerging markets, particularly Asia-Pacific and Europe, with increasing disposable incomes and health consciousness.

Ready-to-drink Protein Beverage Product Landscape

The Ready-to-drink (RTD) protein beverage product landscape is characterized by continuous innovation focused on enhancing nutritional profiles, taste, and convenience. Manufacturers are leveraging advanced ingredient technologies, such as microencapsulation for improved protein solubility and reduced grittiness, and novel protein sources like hydrolysates for faster absorption. Product applications span across post-workout recovery, meal replacement, weight management, and general daily protein supplementation. Unique selling propositions often revolve around clean labels, low sugar content, the inclusion of functional ingredients like vitamins, minerals, and fiber, and a wide array of appealing flavors. Technological advancements in aseptic processing and packaging extend shelf life without compromising nutritional value, making these beverages increasingly accessible and convenient for on-the-go consumption. Estimated market penetration of enhanced functional RTD protein beverages has grown by 20% in the last two years.

Key Drivers, Barriers & Challenges in Ready-to-drink Protein Beverage

The Ready-to-drink (RTD) Protein Beverage market is propelled by several key drivers. Growing consumer awareness regarding the health benefits of protein, including muscle building, satiety, and metabolic support, is a primary catalyst. The increasing demand for convenient, on-the-go nutrition solutions for busy lifestyles and the rising popularity of fitness and sports activities further fuel market expansion. Technological advancements in formulation and flavor profiles are enhancing product appeal and catering to diverse consumer preferences.

- Key Drivers:

- Increased health and wellness consciousness.

- Demand for convenient nutritional solutions.

- Growth in the sports nutrition and fitness industries.

- Product innovation in flavors and formulations.

However, the market faces significant barriers and challenges. The relatively high price point of RTD protein beverages compared to other food options can be a deterrent for price-sensitive consumers. Intense competition from established beverage brands and substitute products like protein powders and bars requires continuous innovation and aggressive marketing. Stringent regulations regarding health claims and ingredient sourcing can also pose hurdles. Supply chain complexities, especially for specialized ingredients, and potential allergen concerns associated with certain protein sources can impact production and market accessibility.

- Barriers & Challenges:

- High product pricing.

- Intense market competition.

- Regulatory compliance and health claim substantiation.

- Supply chain disruptions and ingredient sourcing challenges.

- Potential allergen concerns. Estimated impact of supply chain issues on product availability is around 15% for certain niche ingredients.

Emerging Opportunities in Ready-to-drink Protein Beverage

Emerging opportunities in the Ready-to-drink (RTD) Protein Beverage sector lie in tapping into untapped consumer segments and developing innovative product offerings. The growing demand for plant-based protein beverages presents a significant avenue for expansion, with a focus on sustainable sourcing and novel protein bases like fava bean and pumpkin seed. Opportunities also exist in developing specialized RTD protein drinks targeting specific demographics, such as aging populations seeking to combat sarcopenia, or functional beverages incorporating added benefits like immune support or cognitive enhancement. The expansion of online sales channels and direct-to-consumer (DTC) models offers a direct engagement route with consumers. Furthermore, the integration of personalized nutrition solutions and the exploration of ethical and sustainable sourcing practices represent key growth avenues.

- Untapped Markets: Aging population, specific dietary needs (e.g., keto-friendly), and functional beverage integrations.

- Innovative Applications: Meal replacements, targeted nutritional support, and recovery beverages with added functional ingredients.

- Evolving Consumer Preferences: Demand for sustainable packaging, transparent sourcing, and clean label products.

Growth Accelerators in the Ready-to-drink Protein Beverage Industry

Several catalysts are accelerating the growth of the Ready-to-drink (RTD) Protein Beverage industry. Technological breakthroughs in protein processing, such as enzymatic hydrolysis and ultra-filtration, are leading to improved protein quality, digestibility, and texture, making products more palatable and effective. Strategic partnerships between beverage manufacturers and ingredient suppliers are fostering innovation and ensuring a consistent supply of high-quality protein sources. Furthermore, aggressive market expansion strategies by major players, including targeted marketing campaigns and increased distribution into mainstream retail channels, are significantly boosting accessibility and consumer adoption. The growing influencer marketing landscape within the health and fitness community also plays a crucial role in driving demand and creating brand awareness.

Key Players Shaping the Ready-to-drink Protein Beverage Market

- Aegle Nutrition Manufacturing

- Danone

- Fortisip Extra

- Kraft Heinz

- Meiji

- MusclePharm

- MyDrink

- Nestle

- PepsiCo

- Tyson Food

- Yili

- YouBar

Notable Milestones in Ready-to-drink Protein Beverage Sector

- 2019: Nestlé launches its plant-based protein beverage line, catering to the growing vegan and flexitarian consumer base.

- 2020: MusclePharm expands its RTD protein offerings with new formulations focused on enhanced recovery and performance.

- 2021: PepsiCo acquires Rockstar Energy, signaling its interest in diversifying its beverage portfolio with performance-oriented drinks.

- 2022: Danone's Silk brand introduces a new line of plant-based protein drinks with added probiotics.

- 2023: Kraft Heinz invests in a new functional beverage brand, highlighting its commitment to the health and wellness sector.

- 2024: Yili Group reports significant growth in its dairy-based protein beverage segment, driven by domestic demand in China.

- 2024 (Q3): Meiji launches a new RTD protein drink in Japan targeting a broader demographic beyond athletes.

In-Depth Ready-to-drink Protein Beverage Market Outlook

The future outlook for the Ready-to-drink (RTD) Protein Beverage market is exceptionally promising, driven by persistent global trends towards health consciousness and convenience. Growth accelerators, including ongoing advancements in protein science, the expanding variety of protein sources, and innovative product formulations, will continue to shape market offerings. Strategic partnerships and increased investment in research and development will foster product differentiation and market penetration. The increasing adoption of online sales channels and direct-to-consumer models will further enhance accessibility and customer engagement, paving the way for sustained and robust market growth. The anticipated market size in 2033 is projected to be $68.2 billion, indicating substantial future potential.

Ready-to-drink Protein Beverage Segmentation

-

1. Application

- 1.1. Online Sales

- 1.2. Offline Sales

-

2. Types

- 2.1. Animal Protein Beverage

- 2.2. Plant Protein Beverage

Ready-to-drink Protein Beverage Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Ready-to-drink Protein Beverage REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Ready-to-drink Protein Beverage Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Online Sales

- 5.1.2. Offline Sales

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Animal Protein Beverage

- 5.2.2. Plant Protein Beverage

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Ready-to-drink Protein Beverage Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Online Sales

- 6.1.2. Offline Sales

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Animal Protein Beverage

- 6.2.2. Plant Protein Beverage

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Ready-to-drink Protein Beverage Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Online Sales

- 7.1.2. Offline Sales

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Animal Protein Beverage

- 7.2.2. Plant Protein Beverage

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Ready-to-drink Protein Beverage Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Online Sales

- 8.1.2. Offline Sales

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Animal Protein Beverage

- 8.2.2. Plant Protein Beverage

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Ready-to-drink Protein Beverage Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Online Sales

- 9.1.2. Offline Sales

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Animal Protein Beverage

- 9.2.2. Plant Protein Beverage

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Ready-to-drink Protein Beverage Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Online Sales

- 10.1.2. Offline Sales

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Animal Protein Beverage

- 10.2.2. Plant Protein Beverage

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Aegle Nutrition Manufacturing

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Danone

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Fortisip Extra

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Kraft Heinz

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Meiji

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 MusclePharm

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 MyDrink

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Nestle

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 PepsiCo

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Tyson Food

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Yili

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 YouBar

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 Aegle Nutrition Manufacturing

List of Figures

- Figure 1: Global Ready-to-drink Protein Beverage Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Ready-to-drink Protein Beverage Revenue (million), by Application 2024 & 2032

- Figure 3: North America Ready-to-drink Protein Beverage Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Ready-to-drink Protein Beverage Revenue (million), by Types 2024 & 2032

- Figure 5: North America Ready-to-drink Protein Beverage Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Ready-to-drink Protein Beverage Revenue (million), by Country 2024 & 2032

- Figure 7: North America Ready-to-drink Protein Beverage Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Ready-to-drink Protein Beverage Revenue (million), by Application 2024 & 2032

- Figure 9: South America Ready-to-drink Protein Beverage Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Ready-to-drink Protein Beverage Revenue (million), by Types 2024 & 2032

- Figure 11: South America Ready-to-drink Protein Beverage Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Ready-to-drink Protein Beverage Revenue (million), by Country 2024 & 2032

- Figure 13: South America Ready-to-drink Protein Beverage Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Ready-to-drink Protein Beverage Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Ready-to-drink Protein Beverage Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Ready-to-drink Protein Beverage Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Ready-to-drink Protein Beverage Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Ready-to-drink Protein Beverage Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Ready-to-drink Protein Beverage Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Ready-to-drink Protein Beverage Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Ready-to-drink Protein Beverage Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Ready-to-drink Protein Beverage Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Ready-to-drink Protein Beverage Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Ready-to-drink Protein Beverage Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Ready-to-drink Protein Beverage Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Ready-to-drink Protein Beverage Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Ready-to-drink Protein Beverage Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Ready-to-drink Protein Beverage Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Ready-to-drink Protein Beverage Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Ready-to-drink Protein Beverage Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Ready-to-drink Protein Beverage Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Ready-to-drink Protein Beverage Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Ready-to-drink Protein Beverage Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Ready-to-drink Protein Beverage Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Ready-to-drink Protein Beverage Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Ready-to-drink Protein Beverage Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Ready-to-drink Protein Beverage Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Ready-to-drink Protein Beverage Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Ready-to-drink Protein Beverage Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Ready-to-drink Protein Beverage Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Ready-to-drink Protein Beverage Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Ready-to-drink Protein Beverage Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Ready-to-drink Protein Beverage Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Ready-to-drink Protein Beverage Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Ready-to-drink Protein Beverage Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Ready-to-drink Protein Beverage Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Ready-to-drink Protein Beverage Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Ready-to-drink Protein Beverage Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Ready-to-drink Protein Beverage Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Ready-to-drink Protein Beverage Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Ready-to-drink Protein Beverage Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Ready-to-drink Protein Beverage Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Ready-to-drink Protein Beverage Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Ready-to-drink Protein Beverage Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Ready-to-drink Protein Beverage Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Ready-to-drink Protein Beverage Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Ready-to-drink Protein Beverage Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Ready-to-drink Protein Beverage Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Ready-to-drink Protein Beverage Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Ready-to-drink Protein Beverage Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Ready-to-drink Protein Beverage Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Ready-to-drink Protein Beverage Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Ready-to-drink Protein Beverage Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Ready-to-drink Protein Beverage Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Ready-to-drink Protein Beverage Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Ready-to-drink Protein Beverage Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Ready-to-drink Protein Beverage Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Ready-to-drink Protein Beverage Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Ready-to-drink Protein Beverage Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Ready-to-drink Protein Beverage Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Ready-to-drink Protein Beverage Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Ready-to-drink Protein Beverage Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Ready-to-drink Protein Beverage Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Ready-to-drink Protein Beverage Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Ready-to-drink Protein Beverage Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Ready-to-drink Protein Beverage Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Ready-to-drink Protein Beverage Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Ready-to-drink Protein Beverage Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Ready-to-drink Protein Beverage?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Ready-to-drink Protein Beverage?

Key companies in the market include Aegle Nutrition Manufacturing, Danone, Fortisip Extra, Kraft Heinz, Meiji, MusclePharm, MyDrink, Nestle, PepsiCo, Tyson Food, Yili, YouBar.

3. What are the main segments of the Ready-to-drink Protein Beverage?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Ready-to-drink Protein Beverage," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Ready-to-drink Protein Beverage report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Ready-to-drink Protein Beverage?

To stay informed about further developments, trends, and reports in the Ready-to-drink Protein Beverage, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence