Key Insights

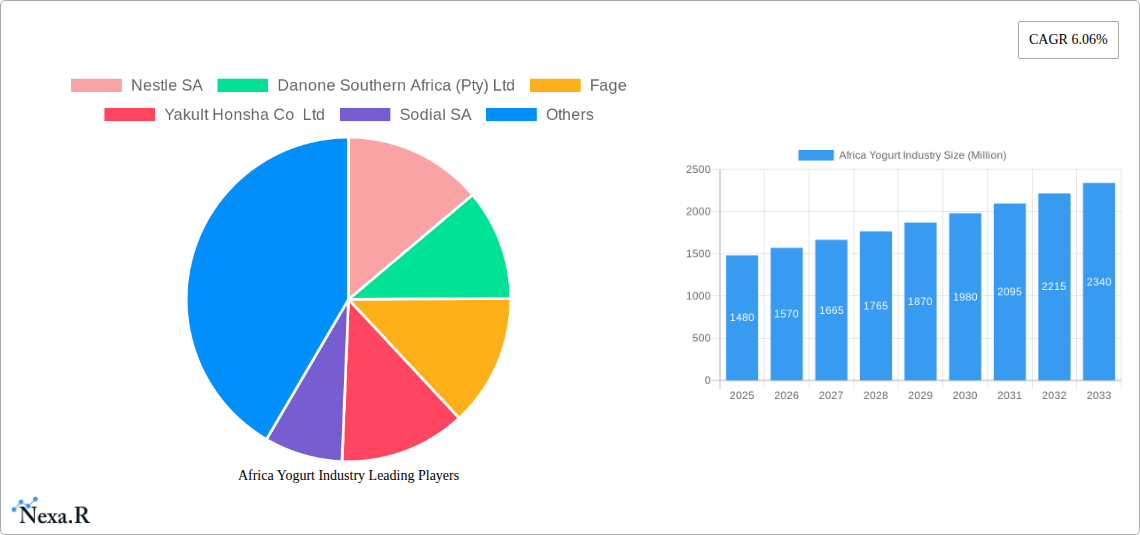

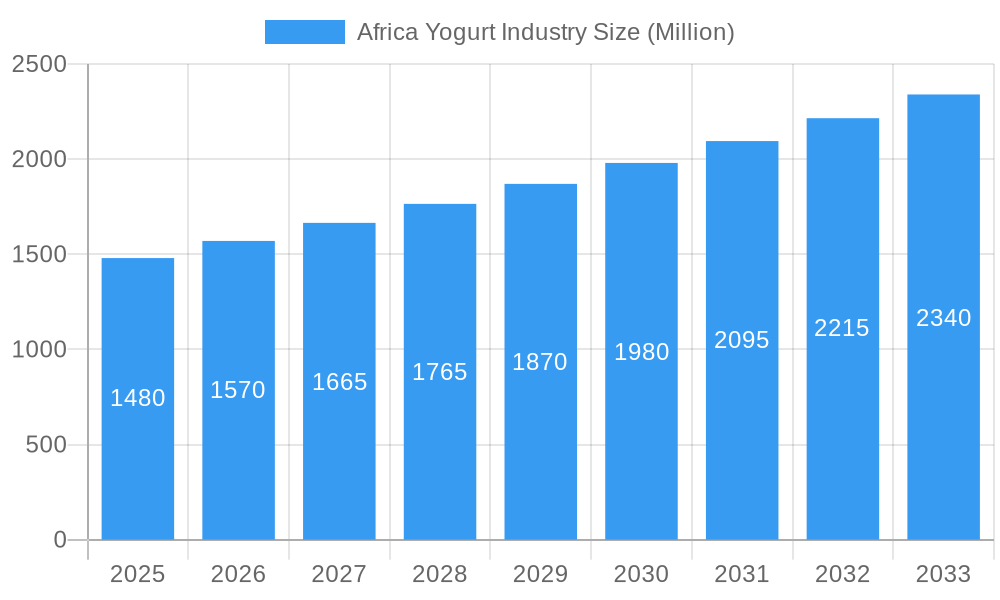

The African yogurt market is poised for substantial growth, projected to reach a valuation of USD 1.48 billion, driven by a compelling Compound Annual Growth Rate (CAGR) of 6.06% from 2025 to 2033. This robust expansion is primarily fueled by a confluence of evolving consumer preferences and a burgeoning middle class across the continent. Increasing health consciousness and a growing demand for convenient, nutritious food options are propelling the adoption of yogurt, particularly among urban populations. The market is segmented into dairy-based and non-dairy-based yogurts, with dairy-based yogurts currently holding a dominant share due to established production infrastructure and consumer familiarity. However, the non-dairy segment is exhibiting rapid growth, catering to a rising vegan and lactose-intolerant consumer base. Flavored yogurts are significantly outpacing plain varieties, reflecting a consumer desire for diverse taste profiles and product innovation. This trend is further amplified by the growing accessibility of yogurt through an expanding distribution network that includes supermarkets, hypermarkets, convenience stores, and increasingly, online platforms.

Africa Yogurt Industry Market Size (In Billion)

Further propelling the market's ascent are key drivers such as the increasing disposable income across many African nations, leading to higher spending on premium and health-focused food products. Key trends include a significant rise in the demand for fortified yogurts with added vitamins and probiotics, a growing interest in Greek yogurt variants known for their thicker texture and higher protein content, and a surge in private label offerings from major retailers, enhancing affordability and choice. Despite this optimistic outlook, certain restraints, such as logistical challenges in cold chain management for perishable products and price sensitivity in some lower-income regions, warrant strategic attention. Nevertheless, the overall trajectory indicates a dynamic and expanding African yogurt industry, with significant opportunities for both established players and new entrants to capitalize on evolving consumer demands and regional economic development.

Africa Yogurt Industry Company Market Share

Africa Yogurt Industry Market Analysis Report: Growth, Trends, and Future Outlook (2019-2033)

This comprehensive report provides an in-depth analysis of the Africa Yogurt Industry, covering market dynamics, growth trends, regional dominance, product landscape, key drivers, barriers, opportunities, and the strategies of major players. With a study period spanning from 2019 to 2033, and a base year of 2025, this report offers critical insights for industry professionals seeking to understand the evolving African yogurt market. The report leverages high-traffic keywords such as "Africa yogurt market," "dairy-based yogurt Africa," "non-dairy yogurt Africa," "yogurt consumption Africa," and "African food industry trends" to maximize search engine visibility and attract relevant stakeholders.

Africa Yogurt Industry Market Dynamics & Structure

The Africa Yogurt Industry is characterized by a moderately concentrated market, with major multinational corporations and established regional players vying for market share. Technological innovation is a significant driver, particularly in product development for health-conscious consumers and the exploration of sustainable production methods. Regulatory frameworks, while evolving, are becoming more conducive to market growth, with a focus on food safety and quality standards. Competitive product substitutes, including other dairy and plant-based alternatives, present a dynamic landscape, necessitating continuous product differentiation. End-user demographics are shifting towards younger, urbanized populations with increasing disposable incomes and a growing awareness of health and wellness. Mergers and acquisitions (M&A) trends are on the rise as larger companies seek to expand their footprint and diversify their product portfolios. For instance, in the historical period (2019-2024), we observed approximately 5-7 significant M&A deals focused on consolidating market share and acquiring innovative smaller brands. Barriers to innovation include the high cost of advanced processing technology and a lack of skilled labor in certain regions.

- Market Concentration: Moderately concentrated with a mix of global and local players.

- Technological Innovation: Driven by health benefits, plant-based alternatives, and sustainable practices.

- Regulatory Frameworks: Evolving to support food safety and industry growth.

- Competitive Substitutes: Non-dairy alternatives, other fermented dairy products.

- End-User Demographics: Young, urban, health-conscious consumers with growing disposable income.

- M&A Trends: Increasing, focused on market consolidation and portfolio expansion.

- Innovation Barriers: High technology costs, skilled labor shortages.

Africa Yogurt Industry Growth Trends & Insights

The Africa Yogurt Industry is poised for substantial growth over the forecast period (2025–2033), fueled by a confluence of favorable demographic, economic, and societal factors. The market size evolution is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 8.5% from 2025 to 2033, reaching an estimated value of over $5,500 million units by the end of the forecast period. Adoption rates for yogurt, particularly in emerging markets within the continent, are steadily increasing as consumers become more health-aware and seek convenient, nutritious food options. Technological disruptions, such as advancements in fermentation processes and the development of shelf-stable yogurt products, are enhancing product accessibility and appeal. Consumer behavior shifts are a pivotal element, with a noticeable trend towards preference for flavored yogurts, Greek-style yogurts, and low-sugar or sugar-free options. The growing acceptance of non-dairy alternatives, driven by lactose intolerance and vegan lifestyles, is also a significant contributor to market expansion. Market penetration is expected to rise from an estimated 35% in 2025 to over 50% by 2033, especially in urban centers. The influence of social media and digital marketing campaigns is further accelerating consumer awareness and demand for innovative yogurt products.

Dominant Regions, Countries, or Segments in Africa Yogurt Industry

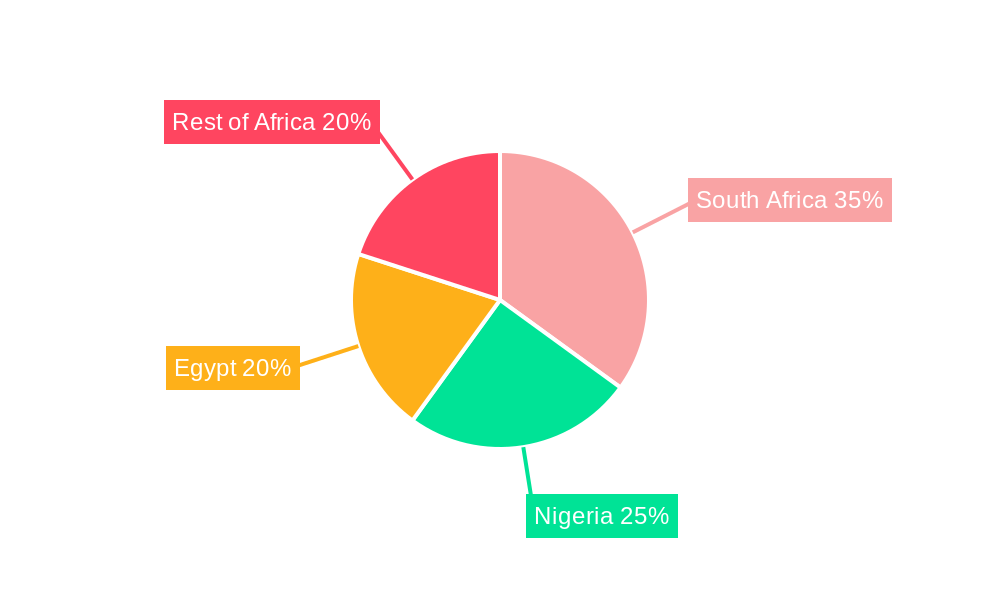

The African yogurt market exhibits distinct patterns of dominance across its various segments and geographies. Within the Category of yogurts, Dairy-based Yogurt remains the dominant segment, accounting for an estimated 80% of the market share due to established cultural preferences and wider availability. However, Non-dairy-based Yogurt is experiencing a rapid growth trajectory, projected to capture an increasing share, especially in urban and health-conscious markets. In terms of Type, Flavored Yogurt consistently leads, driven by consumer demand for variety and taste appeal, holding approximately 70% of the market share. Plain yogurt caters to a more niche but growing segment focused on health and versatility. The Distribution Channel landscape is primarily dominated by Supermarkets/Hypermarkets, which represent over 50% of yogurt sales, followed by Convenience Stores and a burgeoning Online Stores segment, which is expected to grow significantly. Geographically, South Africa has historically been the largest market, driven by its developed retail infrastructure and higher disposable incomes, currently holding around 35% of the total African yogurt market. Nigeria and Egypt are rapidly emerging as key growth engines, with Nigeria projected to witness a CAGR of over 10% during the forecast period, driven by its large population and increasing urbanization. The Rest of Africa, encompassing markets like Kenya, Ghana, and Morocco, presents significant untapped potential, characterized by growing middle classes and a rising demand for convenient and nutritious food products. Factors such as favorable government policies supporting the dairy sector, investment in cold chain infrastructure, and increasing consumer awareness of the health benefits of yogurt are key drivers in these dominant regions and countries.

- Dominant Category: Dairy-based Yogurt (approx. 80% market share)

- Fastest Growing Category: Non-dairy-based Yogurt

- Dominant Type: Flavored Yogurt (approx. 70% market share)

- Dominant Distribution Channel: Supermarkets/Hypermarkets (over 50% market share)

- Emerging Distribution Channel: Online Stores

- Leading Geography (Historical): South Africa (approx. 35% market share)

- Key Growth Regions: Nigeria, Egypt

- Untapped Potential: Rest of Africa (Kenya, Ghana, Morocco)

- Growth Drivers: Favorable policies, infrastructure development, health awareness.

Africa Yogurt Industry Product Landscape

The African yogurt market is witnessing a surge in product innovation driven by evolving consumer preferences for health, convenience, and indulgence. Product development is increasingly focused on offering enhanced nutritional profiles, such as high-protein yogurts and yogurts fortified with vitamins and probiotics. The introduction of plant-based yogurt alternatives, made from ingredients like coconut, almond, and soy, is a significant trend catering to a growing segment of health-conscious and lactose-intolerant consumers. Unique selling propositions often revolve around natural ingredients, reduced sugar content, and exotic flavor combinations reflecting local tastes. Technological advancements in UHT processing and aseptic packaging are enabling longer shelf life and wider distribution across the continent, making nutritious yogurt more accessible even in remote areas. The performance metrics are increasingly evaluated on consumer acceptance, nutritional value, and sustainability of production.

Key Drivers, Barriers & Challenges in Africa Yogurt Industry

The Africa Yogurt Industry is propelled by several key drivers, including a growing health and wellness consciousness among consumers, an increasing disposable income in urban areas, and the expanding young population. Technological advancements in production and distribution are also crucial, enabling wider reach and product diversification. Government initiatives promoting dairy production and food security further bolster the sector.

Key barriers and challenges include the underdeveloped cold chain infrastructure in many regions, which impacts product availability and spoilage. Fluctuations in raw material prices, particularly milk, can affect profitability. Regulatory hurdles and varying food safety standards across different African nations can also pose complexities for manufacturers. Intense competition from both local and international brands, coupled with limited consumer awareness in some rural areas, also presents ongoing challenges. The estimated impact of these challenges on market growth could be a reduction of 1-2% in projected CAGR if not adequately addressed.

- Key Drivers: Health consciousness, rising disposable income, young population, technological advancements, government support.

- Barriers & Challenges: Underdeveloped cold chain, raw material price volatility, regulatory complexities, intense competition, limited rural consumer awareness.

Emerging Opportunities in Africa Yogurt Industry

Emerging opportunities in the Africa Yogurt Industry lie in catering to the growing demand for plant-based and functional yogurts. The untapped potential in smaller African economies and rural populations presents a significant avenue for market expansion. Innovations in product formats, such as single-serving, portable yogurts and yogurt-based beverages, align with on-the-go consumption trends. Furthermore, there is a growing opportunity for developing yogurts with specific health benefits, such as those aiding digestion or boosting immunity, capitalizing on the increasing consumer focus on preventative healthcare.

Growth Accelerators in the Africa Yogurt Industry Industry

Long-term growth in the Africa Yogurt Industry will be significantly accelerated by strategic partnerships between local distributors and international manufacturers, facilitating market penetration and knowledge transfer. Technological breakthroughs in optimizing production efficiency and reducing environmental impact will enhance competitiveness and sustainability. Market expansion strategies focused on product localization, catering to diverse regional tastes and dietary needs, will be crucial. Furthermore, investments in consumer education campaigns highlighting the health benefits of yogurt will drive increased adoption rates across the continent.

Key Players Shaping the Africa Yogurt Industry Market

- Nestle SA

- Danone Southern Africa (Pty) Ltd

- Fage

- Yakult Honsha Co Ltd

- Sodial SA

- Parmalat Canada

- Kraft foods group Inc

- Viju Industries Nigeria Limited

- General Mills

- Chobani Inc

Notable Milestones in Africa Yogurt Industry Sector

- April 2021: General Mills announced the launch of yogurt that will pack more protein per cup than any other on the market. The new yogurt, called Ratio: Protein, follows the company's introduction of Ratio: Keto, which targets consumers tracking their three macronutrients: fat, protein, and carbohydrate. It's the latest in a series of yogurt launches at General Mills, targeting consumers with very specific dietary or taste preferences.

- June 2021: General Mills and Mars Inc.'s new mashup were Yoplait Skittles, a limited-edition yogurt launched in June that is designed to taste like Skittles candies. Available in 6-oz cups containing 160 calories each, the yogurt comes in three varieties: Original Skittles, Wild Berry Skittles, and Skittles Smoothies.

- 2021: Chobani LLC launched new flavors of zero sugar yogurt. According to the company, these new flavors are Mixed Berry and Strawberry, respectively. The strategy behind the new launch and product innovation is to offer consumers a sugar-free product so that the company can target diabetic patients, and also this specific strategy will enable the company to expand the business and enlarge the company's product portfolio.

In-Depth Africa Yogurt Industry Market Outlook

The Africa Yogurt Industry is set for robust expansion, driven by a confluence of factors that will shape its future trajectory. The increasing consumer demand for healthy and convenient food options, coupled with a growing understanding of the nutritional benefits of yogurt, forms the bedrock of this optimistic outlook. Furthermore, the penetration of modern retail formats and the rapid growth of e-commerce platforms will significantly enhance product accessibility across diverse geographies. Strategic investments in cold chain infrastructure and localized product development will be pivotal in unlocking the full potential of this dynamic market, promising substantial returns for stakeholders.

Africa Yogurt Industry Segmentation

-

1. Category

- 1.1. Dairy-based Yogurt

- 1.2. Non-dairy-based Yogurt

-

2. Type

- 2.1. Plain Yogurt

- 2.2. Flavored Yogurt

-

3. Distribution Channel

- 3.1. Supermarkets/Hypermarkets

- 3.2. Convenience Stores

- 3.3. Specialty Stores

- 3.4. Online Stores

- 3.5. Other Distribution Channels

-

4. Geography

- 4.1. South Africa

- 4.2. Nigeria

- 4.3. Egypt

- 4.4. Rest of Africa

Africa Yogurt Industry Segmentation By Geography

- 1. South Africa

- 2. Nigeria

- 3. Egypt

- 4. Rest of Africa

Africa Yogurt Industry Regional Market Share

Geographic Coverage of Africa Yogurt Industry

Africa Yogurt Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.06% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 Introduction of new flavors

- 3.2.2 formulations

- 3.2.3 and types of yogurt

- 3.2.4 including low-fat

- 3.2.5 Greek yogurt

- 3.2.6 and yogurt with added probiotics

- 3.2.7 caters to diverse consumer preferences.

- 3.3. Market Restrains

- 3.3.1 Inadequate infrastructure and logistical issues in some regions can hinder the efficient distribution of yogurt products

- 3.3.2 particularly in rural areas.

- 3.4. Market Trends

- 3.4.1 Growing demand for functional and fortified yogurt products with added health benefits

- 3.4.2 such as probiotics and reduced sugar content.

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Africa Yogurt Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Category

- 5.1.1. Dairy-based Yogurt

- 5.1.2. Non-dairy-based Yogurt

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Plain Yogurt

- 5.2.2. Flavored Yogurt

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Supermarkets/Hypermarkets

- 5.3.2. Convenience Stores

- 5.3.3. Specialty Stores

- 5.3.4. Online Stores

- 5.3.5. Other Distribution Channels

- 5.4. Market Analysis, Insights and Forecast - by Geography

- 5.4.1. South Africa

- 5.4.2. Nigeria

- 5.4.3. Egypt

- 5.4.4. Rest of Africa

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. South Africa

- 5.5.2. Nigeria

- 5.5.3. Egypt

- 5.5.4. Rest of Africa

- 5.1. Market Analysis, Insights and Forecast - by Category

- 6. South Africa Africa Yogurt Industry Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Category

- 6.1.1. Dairy-based Yogurt

- 6.1.2. Non-dairy-based Yogurt

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Plain Yogurt

- 6.2.2. Flavored Yogurt

- 6.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.3.1. Supermarkets/Hypermarkets

- 6.3.2. Convenience Stores

- 6.3.3. Specialty Stores

- 6.3.4. Online Stores

- 6.3.5. Other Distribution Channels

- 6.4. Market Analysis, Insights and Forecast - by Geography

- 6.4.1. South Africa

- 6.4.2. Nigeria

- 6.4.3. Egypt

- 6.4.4. Rest of Africa

- 6.1. Market Analysis, Insights and Forecast - by Category

- 7. Nigeria Africa Yogurt Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Category

- 7.1.1. Dairy-based Yogurt

- 7.1.2. Non-dairy-based Yogurt

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Plain Yogurt

- 7.2.2. Flavored Yogurt

- 7.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.3.1. Supermarkets/Hypermarkets

- 7.3.2. Convenience Stores

- 7.3.3. Specialty Stores

- 7.3.4. Online Stores

- 7.3.5. Other Distribution Channels

- 7.4. Market Analysis, Insights and Forecast - by Geography

- 7.4.1. South Africa

- 7.4.2. Nigeria

- 7.4.3. Egypt

- 7.4.4. Rest of Africa

- 7.1. Market Analysis, Insights and Forecast - by Category

- 8. Egypt Africa Yogurt Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Category

- 8.1.1. Dairy-based Yogurt

- 8.1.2. Non-dairy-based Yogurt

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Plain Yogurt

- 8.2.2. Flavored Yogurt

- 8.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.3.1. Supermarkets/Hypermarkets

- 8.3.2. Convenience Stores

- 8.3.3. Specialty Stores

- 8.3.4. Online Stores

- 8.3.5. Other Distribution Channels

- 8.4. Market Analysis, Insights and Forecast - by Geography

- 8.4.1. South Africa

- 8.4.2. Nigeria

- 8.4.3. Egypt

- 8.4.4. Rest of Africa

- 8.1. Market Analysis, Insights and Forecast - by Category

- 9. Rest of Africa Africa Yogurt Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Category

- 9.1.1. Dairy-based Yogurt

- 9.1.2. Non-dairy-based Yogurt

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Plain Yogurt

- 9.2.2. Flavored Yogurt

- 9.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.3.1. Supermarkets/Hypermarkets

- 9.3.2. Convenience Stores

- 9.3.3. Specialty Stores

- 9.3.4. Online Stores

- 9.3.5. Other Distribution Channels

- 9.4. Market Analysis, Insights and Forecast - by Geography

- 9.4.1. South Africa

- 9.4.2. Nigeria

- 9.4.3. Egypt

- 9.4.4. Rest of Africa

- 9.1. Market Analysis, Insights and Forecast - by Category

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2025

- 10.2. Company Profiles

- 10.2.1 Nestle SA

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 Danone Southern Africa (Pty) Ltd

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Fage

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Yakult Honsha Co Ltd

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Sodial SA

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 Parmalat Canada

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 Kraft foods group Inc

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 Viju Industries Nigeria Limited

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 General Mills

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 Chobani Inc

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.1 Nestle SA

List of Figures

- Figure 1: Africa Yogurt Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Africa Yogurt Industry Share (%) by Company 2025

List of Tables

- Table 1: Africa Yogurt Industry Revenue Million Forecast, by Category 2020 & 2033

- Table 2: Africa Yogurt Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 3: Africa Yogurt Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 4: Africa Yogurt Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 5: Africa Yogurt Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Africa Yogurt Industry Revenue Million Forecast, by Category 2020 & 2033

- Table 7: Africa Yogurt Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 8: Africa Yogurt Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 9: Africa Yogurt Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 10: Africa Yogurt Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 11: Africa Yogurt Industry Revenue Million Forecast, by Category 2020 & 2033

- Table 12: Africa Yogurt Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 13: Africa Yogurt Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 14: Africa Yogurt Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 15: Africa Yogurt Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Africa Yogurt Industry Revenue Million Forecast, by Category 2020 & 2033

- Table 17: Africa Yogurt Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 18: Africa Yogurt Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 19: Africa Yogurt Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 20: Africa Yogurt Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: Africa Yogurt Industry Revenue Million Forecast, by Category 2020 & 2033

- Table 22: Africa Yogurt Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 23: Africa Yogurt Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 24: Africa Yogurt Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 25: Africa Yogurt Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Africa Yogurt Industry?

The projected CAGR is approximately 6.06%.

2. Which companies are prominent players in the Africa Yogurt Industry?

Key companies in the market include Nestle SA, Danone Southern Africa (Pty) Ltd, Fage, Yakult Honsha Co Ltd, Sodial SA, Parmalat Canada, Kraft foods group Inc, Viju Industries Nigeria Limited, General Mills, Chobani Inc.

3. What are the main segments of the Africa Yogurt Industry?

The market segments include Category, Type, Distribution Channel, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.48 Million as of 2022.

5. What are some drivers contributing to market growth?

Introduction of new flavors. formulations. and types of yogurt. including low-fat. Greek yogurt. and yogurt with added probiotics. caters to diverse consumer preferences..

6. What are the notable trends driving market growth?

Growing demand for functional and fortified yogurt products with added health benefits. such as probiotics and reduced sugar content..

7. Are there any restraints impacting market growth?

Inadequate infrastructure and logistical issues in some regions can hinder the efficient distribution of yogurt products. particularly in rural areas..

8. Can you provide examples of recent developments in the market?

In 2021, Chobani LLC launched new flavors of zero sugar yogurt. According to the company, these new flavors are Mixed Berry and Strawberry, respectively. The strategy behind the new launch and product innovation is to offer consumers a sugar-free product so that the company can target diabetic patients, and also this specific strategy will enable the company to expand the business and enlarge the company's product portfolio.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Africa Yogurt Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Africa Yogurt Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Africa Yogurt Industry?

To stay informed about further developments, trends, and reports in the Africa Yogurt Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence