Key Insights

The Adherence Packaging market is experiencing robust growth, projected to reach a substantial market size driven by an increasing emphasis on medication adherence and patient outcomes. With an estimated market size of approximately $6,500 million in 2025, the industry is poised for continued expansion, anticipating a Compound Annual Growth Rate (CAGR) of around 7.5% through 2033. This surge is primarily fueled by the growing prevalence of chronic diseases, an aging global population, and the subsequent rise in the number of individuals requiring consistent medication regimens. The convenience and enhanced safety offered by adherence packaging solutions, such as blister packs and pill organizers, directly address the challenges faced by patients in managing complex medication schedules, thereby reducing prescription abandonment and improving treatment efficacy. Furthermore, the increasing adoption of these packaging solutions by retail pharmacies, hospitals, and long-term care facilities underscores their value in streamlining pharmacy operations and improving patient care delivery.

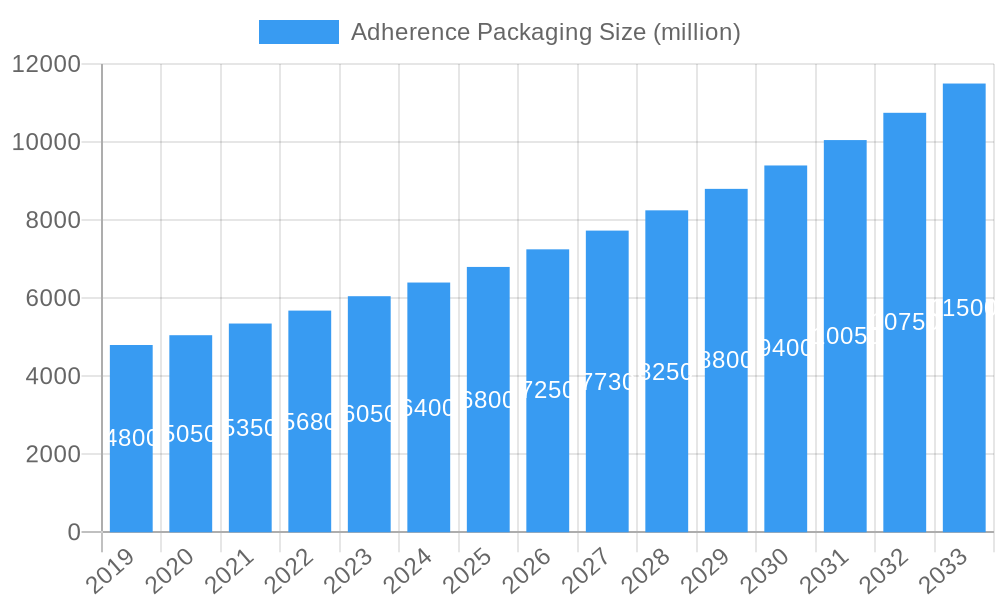

Adherence Packaging Market Size (In Billion)

Key market trends indicate a significant shift towards more sophisticated and automated adherence packaging systems. Technological advancements are leading to the development of smart adherence packaging with integrated tracking and reminder features, further boosting patient compliance. The rise of personalized medicine also necessitates tailored adherence packaging that can accommodate diverse drug combinations and dosages. While the market demonstrates strong upward momentum, certain restraints, such as the initial investment cost for advanced automated systems and the need for standardized regulatory frameworks across different regions, could pose challenges. However, the long-term outlook remains exceptionally positive, with continued innovation and increasing awareness of the critical role of medication adherence in overall healthcare success expected to drive sustained market expansion. The market's segmentation by application and type highlights the diverse needs being addressed, from simple plastic films for unit-dose packaging to more complex multi-material solutions for specialized requirements.

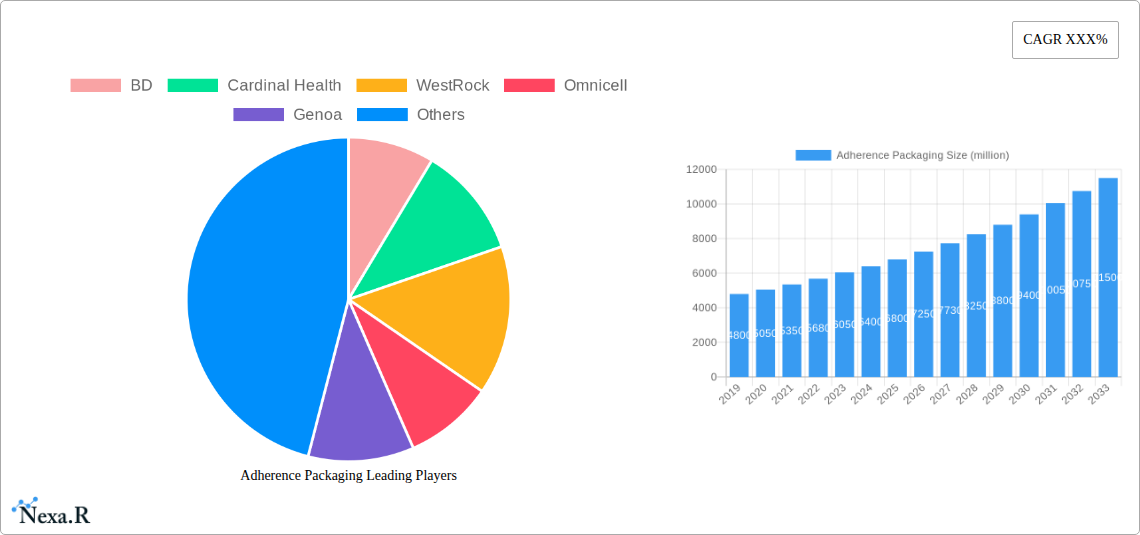

Adherence Packaging Company Market Share

Comprehensive Adherence Packaging Market Report: Dynamics, Growth, and Future Outlook (2019-2033)

This in-depth report provides a comprehensive analysis of the global Adherence Packaging market, offering critical insights for industry stakeholders. Covering the period from 2019 to 2033, with a base year of 2025 and a forecast period extending to 2033, this study meticulously examines market dynamics, growth trends, regional dominance, product innovation, key drivers, barriers, opportunities, and the competitive landscape. The report is structured to deliver actionable intelligence, enabling informed strategic decision-making within the pharmaceutical packaging sector. Our analysis incorporates high-traffic keywords relevant to adherence packaging, prescription packaging, medication adherence solutions, pharmaceutical seals, pill organizers, blister packs, and compliance packaging, ensuring maximum search engine visibility. We further segment the market by parent and child markets, providing granular insights into specialized niches. All quantitative data is presented in million units for clarity and ease of comparison.

Adherence Packaging Market Dynamics & Structure

The Adherence Packaging market exhibits a moderately concentrated structure, with key players like WestRock, Amcor, BD, and Cardinal Health holding significant shares. Technological innovation is a primary driver, fueled by the demand for enhanced patient safety and medication compliance. Advancements in smart packaging, such as those offering dose reminders and temperature monitoring, are reshaping product development. Regulatory frameworks, including FDA guidelines on child-resistant packaging and tamper-evident features, significantly influence product design and material selection. Competitive product substitutes include traditional prescription bottles, generic pill organizers, and alternative dispensing systems. End-user demographics, particularly the aging global population and the increasing prevalence of chronic diseases, are driving consistent demand for adherence solutions. Mergers and acquisitions (M&A) are a notable trend, with companies aiming to expand their product portfolios and geographic reach. For instance, the acquisition of smaller compliance packaging specialists by larger manufacturers aims to consolidate market share and leverage economies of scale.

- Market Concentration: Moderately concentrated with leading players controlling substantial market share.

- Technological Innovation Drivers: Demand for improved patient safety, medication adherence, smart packaging solutions, and data integration.

- Regulatory Frameworks: Strict adherence to FDA, EMA, and other regional regulations for safety, child resistance, and tamper-evidence.

- Competitive Product Substitutes: Traditional prescription bottles, non-specialized pill organizers, manual dose management.

- End-User Demographics: Aging population, individuals with chronic conditions, caregivers, and healthcare providers.

- M&A Trends: Strategic acquisitions to broaden product offerings, enhance technological capabilities, and gain market penetration. For example, acquisitions of specialized blister pack manufacturers by diversified packaging giants have been observed.

Adherence Packaging Growth Trends & Insights

The Adherence Packaging market is poised for robust growth, projected to witness a Compound Annual Growth Rate (CAGR) of approximately 6.8% from 2025 to 2033. This expansion is primarily driven by the escalating global burden of chronic diseases and the subsequent rise in prescription medication usage. The increasing awareness among healthcare professionals and patients regarding the detrimental impact of poor medication adherence on treatment outcomes and healthcare costs is a significant catalyst. The market size, estimated at around $7,500 million units in the base year 2025, is expected to surge as adoption rates for advanced adherence packaging solutions climb. Technological disruptions, including the integration of RFID tags for inventory management and tracking, and the development of personalized dosage systems, are further fueling market penetration. Consumer behavior shifts are also playing a crucial role, with a growing preference for convenient, easy-to-use, and visually appealing packaging that aids in medication management. The push for sustainable packaging materials, such as recyclable plastics and biodegradable paperboard, is also influencing product innovation and consumer choice. Furthermore, the increasing demand for pediatric adherence packaging, designed with child-resistant features and engaging visuals, highlights a growing niche within the market. The transition from paper-based instructions to digital integration within packaging, offering interactive patient support, is another key trend. The evolving healthcare landscape, with a greater emphasis on home-based care and remote patient monitoring, is creating new avenues for specialized adherence packaging solutions that facilitate self-management of medications. The report projects that by 2033, the market size will reach approximately $12,800 million units, reflecting consistent and strong expansion.

Dominant Regions, Countries, or Segments in Adherence Packaging

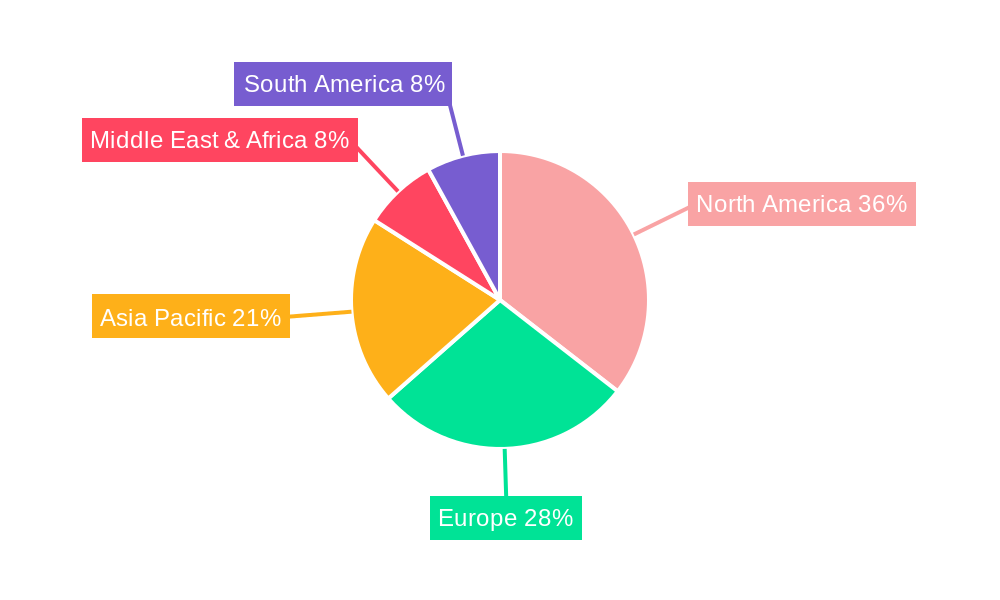

The Retail Pharmacies segment, within the Application category, is currently the dominant force in the Adherence Packaging market, accounting for an estimated 45% of the global market share in 2025. This dominance is attributed to the sheer volume of prescriptions dispensed through retail channels and the increasing emphasis by pharmacists on educating patients about medication adherence. The growing number of independent pharmacies and large retail pharmacy chains are actively implementing innovative adherence packaging solutions to differentiate their services and improve patient outcomes. The United States, specifically, stands out as a leading country due to its large patient population, advanced healthcare infrastructure, and proactive approach to managing chronic diseases. Government initiatives promoting medication adherence and reimbursement policies that favor adherence packaging further bolster its market position.

- Dominant Segment (Application): Retail Pharmacies, driven by high prescription volumes and pharmacist-led adherence programs. Estimated market share of 45% in 2025.

- Key Country: United States, characterized by a large patient base, strong healthcare system, and supportive government policies.

- Drivers in Retail Pharmacies:

- Increased patient demand for convenient medication management.

- Pharmacist recommendations and value-added services.

- Growing prevalence of chronic conditions requiring long-term medication regimens.

- Technological advancements in blister packaging and pill organizers.

- Manufacturer-led promotional programs for adherence packaging.

Within the Type segment, Plastic Film is projected to hold the largest market share, estimated at around 40% in 2025. The versatility, durability, and cost-effectiveness of plastic films, such as PVC, PET, and HDPE, make them ideal for various adherence packaging formats, including blister packs, cold-form foils, and sachets. The ongoing research and development in biodegradable and recyclable plastics are also contributing to the sustained demand for this material.

- Dominant Segment (Type): Plastic Film, offering versatility, durability, and cost-effectiveness. Estimated market share of 40% in 2025.

- Drivers in Plastic Film:

- Wide range of applications in blister packs, cold-form foils, and sachets.

- Advancements in barrier properties and material sustainability.

- Cost-effectiveness compared to other materials.

- Innovation in child-resistant and tamper-evident plastic closures.

- Integration with other materials for enhanced functionality.

Adherence Packaging Product Landscape

The Adherence Packaging product landscape is characterized by continuous innovation aimed at improving patient compliance and safety. Key product categories include multi-dose blister packs, dose-dispensing systems, pill organizers with reminder functions, and unit-dose packaging. Innovations such as integrated QR codes for accessing medication information, child-resistant designs, and tamper-evident seals are becoming standard features. Advanced materials, including high-barrier plastics and sustainable paperboard options, are being utilized to enhance product performance and environmental footprint. The focus is on creating intuitive, user-friendly solutions that simplify medication regimens for patients, particularly those with complex dosing schedules or cognitive impairments.

Key Drivers, Barriers & Challenges in Adherence Packaging

Key Drivers:

The Adherence Packaging market is propelled by the escalating global prevalence of chronic diseases, leading to increased prescription volumes. Growing awareness among healthcare providers and patients about the critical role of medication adherence in improving treatment efficacy and reducing healthcare costs is a major impetus. Technological advancements in smart packaging solutions, offering features like dose reminders and data tracking, are further accelerating adoption. The aging global population, with its higher incidence of multiple prescriptions, also significantly contributes to market growth.

Key Barriers & Challenges:

Despite the promising outlook, the Adherence Packaging market faces several challenges. High manufacturing costs associated with specialized adherence packaging solutions can be a deterrent, especially for smaller pharmaceutical companies or those serving price-sensitive markets. Stringent regulatory requirements for packaging materials and child-resistant features can also lead to longer product development cycles and increased compliance costs. Intense competition from traditional prescription packaging and the availability of generic dispensing systems present a competitive pressure. Supply chain disruptions, as experienced during global events, can impact the availability and cost of raw materials, affecting production.

Emerging Opportunities in Adherence Packaging

Emerging opportunities in the Adherence Packaging sector lie in the development of personalized adherence solutions tailored to individual patient needs and medication regimens. The integration of digital technologies, such as IoT-enabled packaging for remote patient monitoring and adherence tracking, presents a significant growth area. Untapped markets in developing economies, where access to advanced healthcare and medication management tools is limited, offer substantial potential for expansion. The growing demand for sustainable and eco-friendly packaging materials is creating opportunities for manufacturers to innovate in biodegradable and recyclable adherence packaging solutions.

Growth Accelerators in the Adherence Packaging Industry

Several catalysts are accelerating growth in the Adherence Packaging industry. Technological breakthroughs, particularly in smart packaging and serialization, are enhancing traceability and patient engagement. Strategic partnerships between pharmaceutical companies, packaging manufacturers, and technology providers are fostering innovation and market penetration. The increasing focus on value-based healthcare models, which prioritize patient outcomes, is driving the demand for solutions that demonstrably improve medication adherence. Furthermore, market expansion strategies, including geographical diversification and product portfolio extension into specialized therapeutic areas, are contributing to sustained growth.

Key Players Shaping the Adherence Packaging Market

- BD

- Cardinal Health

- WestRock

- Omnicell

- Genoa

- Parata

- Amcor

- Medicine-On-Time

- CHUDY

- Drug Package

- Global Factories

- Pearson Medical

- Accu-Chart Plus Healthcare Systems

- Arxium

- Manrex Limited

- McKesson Corporation

- TCGRx

Notable Milestones in Adherence Packaging Sector

- 2019: Introduction of advanced smart blister packs with integrated sensors for temperature and humidity monitoring.

- 2020: Increased demand for child-resistant and tamper-evident packaging solutions driven by evolving safety regulations.

- 2021: Significant investments in sustainable packaging materials, including biodegradable plastics and recycled paperboard.

- 2022: Launch of IoT-enabled adherence packaging solutions for remote patient monitoring by major tech and healthcare providers.

- 2023: Consolidation within the market through strategic mergers and acquisitions, aiming to enhance product portfolios and market reach.

- 2024: Increased adoption of serialization and track-and-trace technologies within adherence packaging to combat counterfeiting and improve supply chain integrity.

In-Depth Adherence Packaging Market Outlook

The future outlook for the Adherence Packaging market is exceptionally promising, driven by a confluence of factors. Growth accelerators such as continuous technological innovation in smart packaging, personalized medicine integration, and sustainable material development will fuel market expansion. Strategic partnerships and a greater emphasis on patient-centric healthcare models will foster wider adoption of these crucial solutions. The market is poised for significant growth, offering substantial opportunities for stakeholders to innovate, invest, and contribute to improved global health outcomes through enhanced medication adherence.

Adherence Packaging Segmentation

-

1. Application

- 1.1. Retail Pharmacies

- 1.2. Hospitals

- 1.3. Long-Term Center

- 1.4. Others

-

2. Type

- 2.1. Plastic Film

- 2.2. Paper & Paperboard

- 2.3. Aluminum

- 2.4. Others

Adherence Packaging Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Adherence Packaging Regional Market Share

Geographic Coverage of Adherence Packaging

Adherence Packaging REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.43% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Adherence Packaging Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Retail Pharmacies

- 5.1.2. Hospitals

- 5.1.3. Long-Term Center

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Plastic Film

- 5.2.2. Paper & Paperboard

- 5.2.3. Aluminum

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Adherence Packaging Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Retail Pharmacies

- 6.1.2. Hospitals

- 6.1.3. Long-Term Center

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Plastic Film

- 6.2.2. Paper & Paperboard

- 6.2.3. Aluminum

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Adherence Packaging Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Retail Pharmacies

- 7.1.2. Hospitals

- 7.1.3. Long-Term Center

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Plastic Film

- 7.2.2. Paper & Paperboard

- 7.2.3. Aluminum

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Adherence Packaging Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Retail Pharmacies

- 8.1.2. Hospitals

- 8.1.3. Long-Term Center

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Plastic Film

- 8.2.2. Paper & Paperboard

- 8.2.3. Aluminum

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Adherence Packaging Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Retail Pharmacies

- 9.1.2. Hospitals

- 9.1.3. Long-Term Center

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Plastic Film

- 9.2.2. Paper & Paperboard

- 9.2.3. Aluminum

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Adherence Packaging Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Retail Pharmacies

- 10.1.2. Hospitals

- 10.1.3. Long-Term Center

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Plastic Film

- 10.2.2. Paper & Paperboard

- 10.2.3. Aluminum

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 BD

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Cardinal Health

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 WestRock

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Omnicell

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Genoa

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Parata

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Amcor

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Medicine-On-Time

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 CHUDY

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Drug Package

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Global Factories

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Pearson Medical

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Accu-Chart Plus Healthcare Systems

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Arxium

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Manrex Limited

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Mckesson Corporation

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 TCGRx

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.1 BD

List of Figures

- Figure 1: Global Adherence Packaging Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Adherence Packaging Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Adherence Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Adherence Packaging Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Adherence Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Adherence Packaging Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Adherence Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Adherence Packaging Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Adherence Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Adherence Packaging Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Adherence Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Adherence Packaging Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Adherence Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Adherence Packaging Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Adherence Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Adherence Packaging Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Adherence Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Adherence Packaging Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Adherence Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Adherence Packaging Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Adherence Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Adherence Packaging Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Adherence Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Adherence Packaging Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Adherence Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Adherence Packaging Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Adherence Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Adherence Packaging Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Adherence Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Adherence Packaging Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Adherence Packaging Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Adherence Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Adherence Packaging Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Adherence Packaging Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Adherence Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Adherence Packaging Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Adherence Packaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Adherence Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Adherence Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Adherence Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Adherence Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Adherence Packaging Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Adherence Packaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Adherence Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Adherence Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Adherence Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Adherence Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Adherence Packaging Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Adherence Packaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Adherence Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Adherence Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Adherence Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Adherence Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Adherence Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Adherence Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Adherence Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Adherence Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Adherence Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Adherence Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Adherence Packaging Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Adherence Packaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Adherence Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Adherence Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Adherence Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Adherence Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Adherence Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Adherence Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Adherence Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Adherence Packaging Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Adherence Packaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Adherence Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Adherence Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Adherence Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Adherence Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Adherence Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Adherence Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Adherence Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Adherence Packaging?

The projected CAGR is approximately 6.43%.

2. Which companies are prominent players in the Adherence Packaging?

Key companies in the market include BD, Cardinal Health, WestRock, Omnicell, Genoa, Parata, Amcor, Medicine-On-Time, CHUDY, Drug Package, Global Factories, Pearson Medical, Accu-Chart Plus Healthcare Systems, Arxium, Manrex Limited, Mckesson Corporation, TCGRx.

3. What are the main segments of the Adherence Packaging?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Adherence Packaging," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Adherence Packaging report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Adherence Packaging?

To stay informed about further developments, trends, and reports in the Adherence Packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence