Key Insights

The global Feed Encapsulation market is poised for significant expansion, projected to reach approximately $1.2 billion by 2025, with a robust Compound Annual Growth Rate (CAGR) of around 8.5% anticipated through 2033. This substantial growth is primarily fueled by the escalating demand for enhanced animal nutrition, improved feed efficiency, and reduced environmental impact within the livestock and aquaculture industries. Key drivers include the increasing global protein consumption, necessitating more productive and sustainable animal farming practices. The growing awareness among farmers regarding the benefits of encapsulated feed additives – such as enhanced bioavailability, controlled release, and protection of sensitive ingredients from degradation – is further propelling market adoption. Technological advancements in encapsulation techniques, leading to more cost-effective and versatile solutions, also play a crucial role in market expansion.

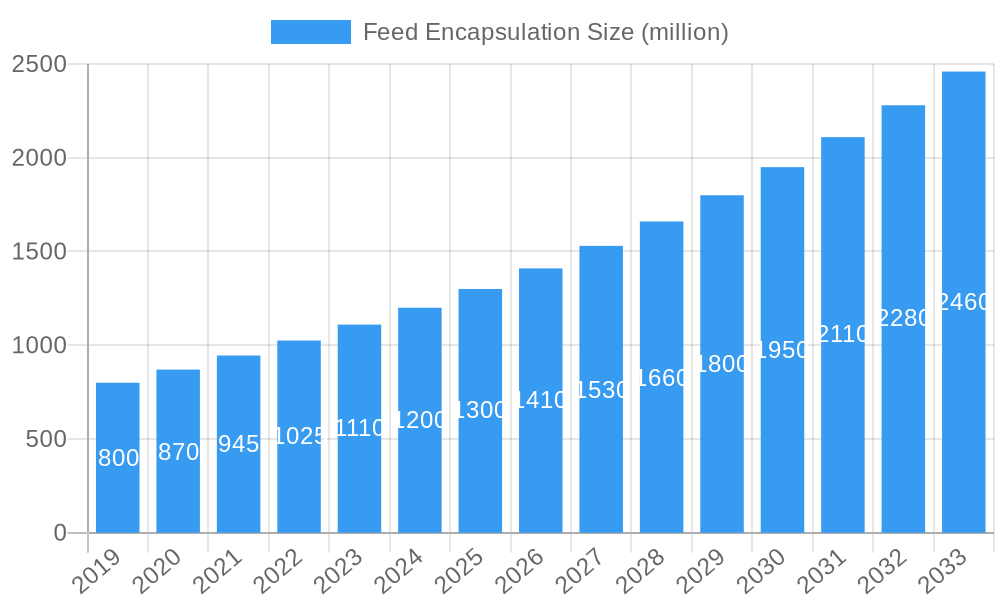

Feed Encapsulation Market Size (In Million)

The market is segmented across various applications, with Poultry and Swine currently dominating due to their high volume and the critical need for optimized feed formulations. Aquaculture is emerging as a rapidly growing segment, driven by the expanding global aquaculture production and the demand for specialized nutrient delivery systems. The "Others" category, encompassing ruminants and other animal types, is also expected to witness steady growth. In terms of types, Lipid-Based Coatings and Polymers are leading segments, offering effective protection and controlled release properties for a wide range of feed additives. However, Protein-Based Coatings and Carbohydrates are gaining traction due to their natural origin and biodegradability, aligning with the growing consumer preference for sustainable and "clean label" animal products. Restraints such as the initial investment costs for encapsulation technology and the need for specialized handling may pose challenges, but the overwhelming benefits and supportive regulatory landscape are expected to drive sustained market growth and innovation.

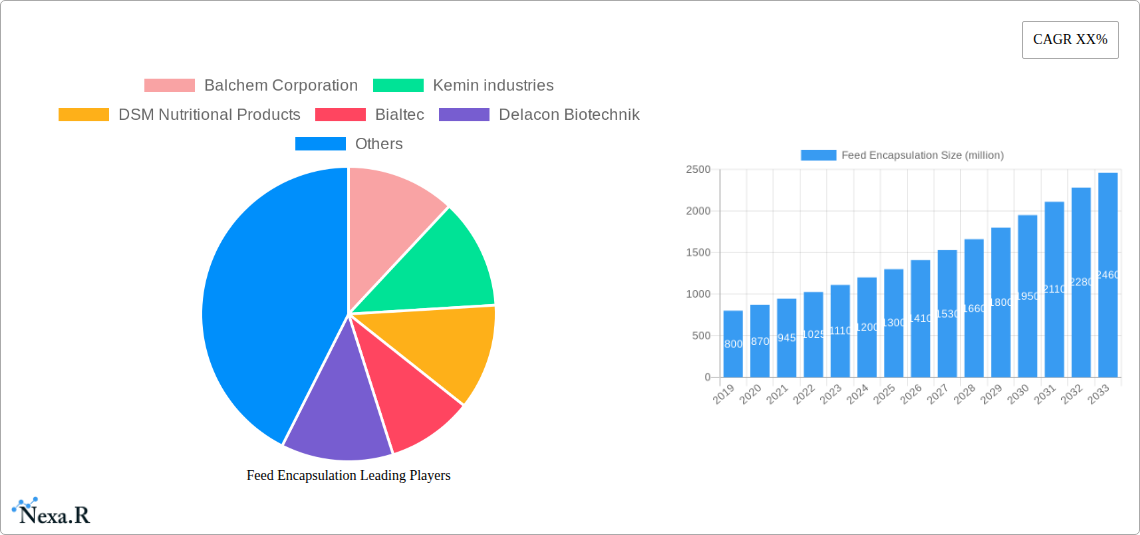

Feed Encapsulation Company Market Share

Feed Encapsulation Market Report: Comprehensive Analysis & Future Outlook (2019-2033)

This in-depth report provides a definitive analysis of the global feed encapsulation market, forecasting significant growth and revealing key strategic insights for industry stakeholders. Leveraging cutting-edge research and proprietary data, this report is your essential guide to understanding market dynamics, identifying growth opportunities, and navigating the competitive landscape of feed encapsulation solutions.

Feed Encapsulation Market Dynamics & Structure

The global feed encapsulation market, valued at approximately USD 5,600 million in 2025, exhibits a moderately concentrated structure driven by a few key global players and a growing number of specialized innovators. Technological innovation is a primary driver, with continuous advancements in encapsulation techniques aiming to enhance nutrient bioavailability, stability, and targeted delivery in animal feed. Regulatory frameworks, particularly concerning animal health, feed safety, and environmental impact, play a crucial role in shaping product development and market access. The market is influenced by the availability of competitive product substitutes, such as direct feed additives, but encapsulation offers distinct advantages in protecting sensitive ingredients. End-user demographics are increasingly focused on sustainable and efficient animal agriculture, demanding solutions that improve animal performance and reduce waste. Mergers and acquisitions (M&A) trends are evident as larger companies seek to expand their portfolios and gain access to proprietary technologies, with an estimated 15-20 M&A deals occurring annually during the historical period.

- Market Concentration: Dominated by key players like Balchem Corporation, Kemin Industries, and DSM Nutritional Products, with a growing presence of niche technology providers.

- Technological Innovation: Focus on improving encapsulation efficiency, release profiles, and cost-effectiveness for diverse feed ingredients.

- Regulatory Frameworks: Stringent regulations for animal feed safety and efficacy drive the adoption of advanced encapsulation technologies.

- Competitive Product Substitutes: While direct additives exist, encapsulation offers superior protection and targeted delivery for sensitive nutrients.

- End-User Demographics: Increasing demand from the poultry, swine, and aquaculture sectors for improved animal health and performance.

- M&A Trends: Strategic acquisitions aimed at consolidating market share and acquiring innovative technologies.

Feed Encapsulation Growth Trends & Insights

The feed encapsulation market is poised for robust expansion, projected to reach an estimated USD 10,200 million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 6.5% from the base year 2025. This growth is underpinned by evolving consumer preferences for sustainably sourced animal protein, which translates to a heightened demand for animal feed solutions that optimize nutrition and minimize environmental impact. The adoption rate of feed encapsulation technologies is steadily increasing across various animal segments, particularly in poultry and swine production, where the efficiency gains and improved animal health outcomes are most pronounced. Technological disruptions, such as the development of novel encapsulation materials like advanced polymers and natural compounds, are further accelerating market penetration. These innovations enable the protection of sensitive ingredients like vitamins, probiotics, and enzymes, ensuring their efficacy throughout the animal's digestive tract. Consumer behavior shifts towards traceable and ethically produced animal products indirectly fuel the demand for feed additives that enhance animal welfare and reduce the need for antibiotic growth promoters. The market penetration of feed encapsulation in advanced economies is already significant, but emerging economies present substantial untapped potential due to their rapidly growing livestock sectors and increasing investment in modern farming practices. The market size evolution is characterized by a consistent upward trajectory, driven by the inherent value proposition of feed encapsulation in improving feed efficiency, animal health, and reducing nutrient losses.

Dominant Regions, Countries, or Segments in Feed Encapsulation

The Poultry application segment currently dominates the global feed encapsulation market, projected to account for approximately 35% of the market share in 2025, with an estimated market value of USD 1,960 million. This dominance is driven by the sheer scale of the global poultry industry, its high feed conversion ratio requirements, and the critical need for efficient delivery of essential nutrients like vitamins, amino acids, and probiotics. North America, particularly the United States, is a leading country in feed encapsulation adoption due to its technologically advanced agricultural infrastructure, strong research and development capabilities in animal nutrition, and supportive regulatory environment for feed additives. Europe, with its focus on animal welfare and sustainable farming practices, also represents a significant market.

Dominant Application Segment: Poultry

- Key Drivers: High feed intake, demand for improved feed conversion ratios, critical need for protected vitamins, amino acids, and probiotics.

- Market Share (2025 Est.): ~35%

- Market Value (2025 Est.): ~USD 1,960 million

- Growth Potential: Continued strong demand driven by global meat consumption trends and advancements in feed formulation.

Dominant Type: Lipid-Based Coatings

- Key Drivers: Excellent barrier properties for moisture and oxygen, cost-effectiveness, and wide applicability for various feed ingredients.

- Market Share (2025 Est.): ~30%

- Market Value (2025 Est.): ~USD 1,680 million

- Growth Potential: Ongoing innovation in lipid encapsulation for enhanced release control and nutrient stability.

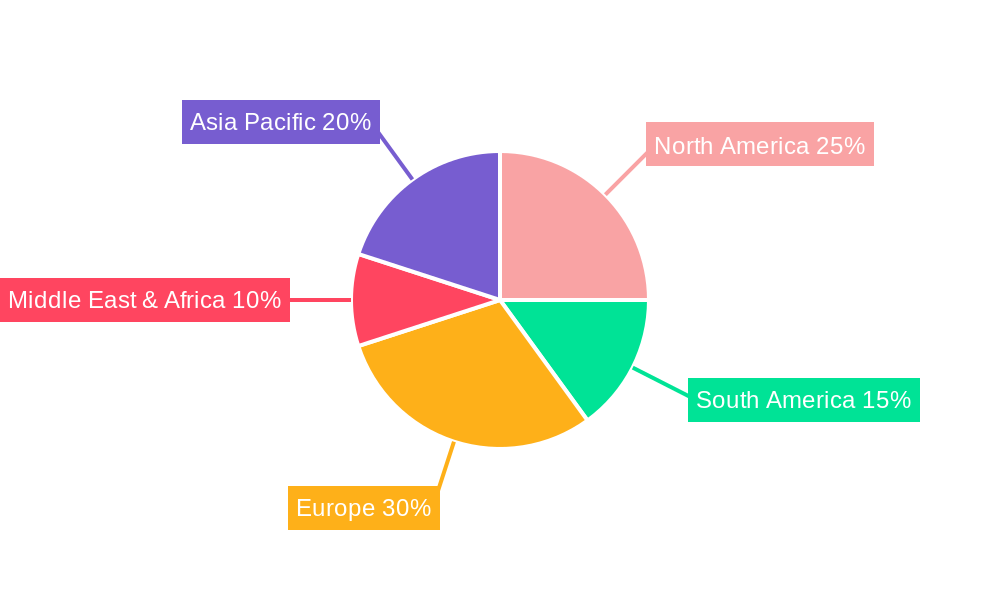

Leading Region: North America

- Key Drivers: Technologically advanced agriculture, robust R&D in animal nutrition, supportive regulatory landscape, high adoption rates of innovative feed solutions.

- Market Share (2025 Est.): ~30%

- Market Value (2025 Est.): ~USD 1,680 million

- Growth Potential: Continued leadership fueled by innovation and demand for premium animal feed ingredients.

Key Country: United States

- Dominance Factors: Large-scale animal production, early adoption of advanced feed technologies, significant investment in feed research.

- Market Value (2025 Est.): ~USD 1,120 million (within North America)

Feed Encapsulation Product Landscape

The feed encapsulation product landscape is characterized by a dynamic evolution of innovative solutions designed to protect sensitive feed ingredients and enhance their efficacy. Lipid-based coatings remain a cornerstone, offering excellent barrier properties against oxidation and moisture, crucial for vitamins and fatty acids. Polymers are increasingly utilized for sophisticated controlled-release mechanisms, ensuring nutrients are delivered at specific points in the animal's digestive tract. Protein and carbohydrate-based coatings are gaining traction due to their natural origins and improved digestibility, aligning with the growing demand for sustainable feed solutions. Natural materials, including plant extracts and essential oils, are being encapsulated to leverage their antimicrobial and performance-enhancing properties. Unique selling propositions often revolve around improved bioavailability, reduced ingredient degradation, enhanced palatability, and the ability to create multi-functional feed additives. Technological advancements are focusing on microencapsulation and nanoencapsulation techniques for more precise ingredient delivery and higher efficacy.

Key Drivers, Barriers & Challenges in Feed Encapsulation

The feed encapsulation market is propelled by several key drivers. Technological advancements in encapsulation materials and processes are enhancing efficiency and cost-effectiveness. The growing global demand for animal protein necessitates improved feed efficiency and animal health, which encapsulation directly addresses. Increasing consumer awareness regarding animal welfare and sustainable farming practices favors solutions that reduce antibiotic use and minimize environmental impact. Furthermore, the desire for enhanced nutrient bioavailability and stability in feed ingredients is a significant market propellant.

Conversely, barriers and challenges exist. The relatively high initial cost of certain advanced encapsulation technologies can be a hurdle for some producers, especially in price-sensitive markets. Regulatory complexities and the need for extensive testing and approval for new encapsulation methods can slow down market entry. Supply chain disruptions for specialized raw materials, particularly natural ingredients, can impact production and availability. Competitive pressures from alternative feed additive delivery methods and the inertia of established farming practices also present challenges.

Emerging Opportunities in Feed Encapsulation

Emerging opportunities in the feed encapsulation market are abundant, driven by evolving industry needs and technological frontiers. The development of novel encapsulation materials from sustainable and biodegradable sources presents a significant avenue for growth, appealing to environmentally conscious stakeholders. Untapped markets in developing regions, with their rapidly expanding livestock sectors, offer substantial potential for the adoption of advanced feed encapsulation solutions. Innovative applications, such as encapsulating precision fermentation products or novel feed enzymes, are poised to unlock new performance benefits for animal agriculture. Furthermore, the growing interest in plant-based feed ingredients and their inherent challenges with stability and palatability creates a strong demand for effective encapsulation technologies.

Growth Accelerators in the Feed Encapsulation Industry

Several catalysts are accelerating the long-term growth of the feed encapsulation industry. Breakthroughs in microfluidics and advanced polymer science are enabling the creation of highly precise and stable encapsulated products. Strategic partnerships between feed additive manufacturers, ingredient suppliers, and technology providers are fostering innovation and accelerating market penetration. Market expansion strategies targeting emerging economies, coupled with localized product development, are crucial for capturing growth. The increasing integration of digital technologies, such as AI-driven formulation and real-time monitoring of nutrient delivery, will further enhance the value proposition of encapsulated feed ingredients.

Key Players Shaping the Feed Encapsulation Market

- Balchem Corporation

- Kemin Industries

- DSM Nutritional Products

- Bialtec

- Delacon Biotechnik

- Adisseo

- Evonik Industries

- Novus International

- Phytobiotics

Notable Milestones in Feed Encapsulation Sector

- 2019: Launch of novel microencapsulation technology for heat-sensitive vitamins, enhancing stability in feed manufacturing (e.g., by Evonik Industries).

- 2020: Acquisition of a leading probiotic encapsulation specialist by a major animal nutrition company, signaling consolidation and focus on gut health solutions (e.g., by DSM Nutritional Products).

- 2021: Introduction of plant-derived protein-based encapsulation for improved palatability and nutrient release in swine feed (e.g., by Kemin Industries).

- 2022: Development of advanced polymer coatings for controlled release of amino acids, optimizing growth performance in poultry.

- 2023: Significant investment in R&D for encapsulated natural antioxidants to improve meat quality and shelf-life in aquaculture.

- 2024: Increased adoption of chitosan-based encapsulation for its antimicrobial properties in aquaculture feed, contributing to disease prevention.

In-Depth Feed Encapsulation Market Outlook

The future outlook for the feed encapsulation market is exceptionally positive, driven by a confluence of technological innovation, evolving industry demands, and supportive global trends. Growth accelerators, including advancements in materials science for novel encapsulation techniques and strategic collaborations across the value chain, will continue to fuel expansion. The market is expected to witness a sustained increase in demand for solutions that enhance animal health, optimize nutrient utilization, and contribute to sustainable animal agriculture. Emphasis on environmentally friendly and natural encapsulation methods will intensify, creating opportunities for bio-based materials. Strategic market expansion, particularly in rapidly developing economies with growing livestock populations, represents a significant opportunity for market leaders. Overall, the feed encapsulation market is positioned for robust and sustained growth, offering considerable potential for stakeholders who can adapt to these evolving dynamics.

Feed Encapsulation Segmentation

-

1. Application

- 1.1. Poultry

- 1.2. Swine

- 1.3. Aquaculture

- 1.4. Ruminants

- 1.5. Others

-

2. Types

- 2.1. Lipid-Based Coatings

- 2.2. Polymers

- 2.3. Protein-Based Coatings

- 2.4. Carbohydrates

- 2.5. Natural Materials

Feed Encapsulation Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Feed Encapsulation Regional Market Share

Geographic Coverage of Feed Encapsulation

Feed Encapsulation REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Feed Encapsulation Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Poultry

- 5.1.2. Swine

- 5.1.3. Aquaculture

- 5.1.4. Ruminants

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Lipid-Based Coatings

- 5.2.2. Polymers

- 5.2.3. Protein-Based Coatings

- 5.2.4. Carbohydrates

- 5.2.5. Natural Materials

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Feed Encapsulation Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Poultry

- 6.1.2. Swine

- 6.1.3. Aquaculture

- 6.1.4. Ruminants

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Lipid-Based Coatings

- 6.2.2. Polymers

- 6.2.3. Protein-Based Coatings

- 6.2.4. Carbohydrates

- 6.2.5. Natural Materials

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Feed Encapsulation Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Poultry

- 7.1.2. Swine

- 7.1.3. Aquaculture

- 7.1.4. Ruminants

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Lipid-Based Coatings

- 7.2.2. Polymers

- 7.2.3. Protein-Based Coatings

- 7.2.4. Carbohydrates

- 7.2.5. Natural Materials

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Feed Encapsulation Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Poultry

- 8.1.2. Swine

- 8.1.3. Aquaculture

- 8.1.4. Ruminants

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Lipid-Based Coatings

- 8.2.2. Polymers

- 8.2.3. Protein-Based Coatings

- 8.2.4. Carbohydrates

- 8.2.5. Natural Materials

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Feed Encapsulation Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Poultry

- 9.1.2. Swine

- 9.1.3. Aquaculture

- 9.1.4. Ruminants

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Lipid-Based Coatings

- 9.2.2. Polymers

- 9.2.3. Protein-Based Coatings

- 9.2.4. Carbohydrates

- 9.2.5. Natural Materials

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Feed Encapsulation Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Poultry

- 10.1.2. Swine

- 10.1.3. Aquaculture

- 10.1.4. Ruminants

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Lipid-Based Coatings

- 10.2.2. Polymers

- 10.2.3. Protein-Based Coatings

- 10.2.4. Carbohydrates

- 10.2.5. Natural Materials

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Balchem Corporation

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Kemin industries

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 DSM Nutritional Products

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Bialtec

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Delacon Biotechnik

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Adisseo

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Evonik Industries

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Novus International

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Phytobiotics

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.1 Balchem Corporation

List of Figures

- Figure 1: Global Feed Encapsulation Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Feed Encapsulation Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Feed Encapsulation Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Feed Encapsulation Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Feed Encapsulation Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Feed Encapsulation Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Feed Encapsulation Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Feed Encapsulation Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Feed Encapsulation Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Feed Encapsulation Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Feed Encapsulation Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Feed Encapsulation Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Feed Encapsulation Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Feed Encapsulation Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Feed Encapsulation Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Feed Encapsulation Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Feed Encapsulation Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Feed Encapsulation Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Feed Encapsulation Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Feed Encapsulation Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Feed Encapsulation Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Feed Encapsulation Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Feed Encapsulation Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Feed Encapsulation Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Feed Encapsulation Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Feed Encapsulation Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Feed Encapsulation Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Feed Encapsulation Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Feed Encapsulation Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Feed Encapsulation Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Feed Encapsulation Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Feed Encapsulation Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Feed Encapsulation Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Feed Encapsulation Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Feed Encapsulation Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Feed Encapsulation Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Feed Encapsulation Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Feed Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Feed Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Feed Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Feed Encapsulation Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Feed Encapsulation Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Feed Encapsulation Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Feed Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Feed Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Feed Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Feed Encapsulation Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Feed Encapsulation Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Feed Encapsulation Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Feed Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Feed Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Feed Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Feed Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Feed Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Feed Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Feed Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Feed Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Feed Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Feed Encapsulation Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Feed Encapsulation Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Feed Encapsulation Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Feed Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Feed Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Feed Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Feed Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Feed Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Feed Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Feed Encapsulation Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Feed Encapsulation Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Feed Encapsulation Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Feed Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Feed Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Feed Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Feed Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Feed Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Feed Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Feed Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Feed Encapsulation?

The projected CAGR is approximately 7%.

2. Which companies are prominent players in the Feed Encapsulation?

Key companies in the market include Balchem Corporation, Kemin industries, DSM Nutritional Products, Bialtec, Delacon Biotechnik, Adisseo, Evonik Industries, Novus International, Phytobiotics.

3. What are the main segments of the Feed Encapsulation?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Feed Encapsulation," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Feed Encapsulation report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Feed Encapsulation?

To stay informed about further developments, trends, and reports in the Feed Encapsulation, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence