Key Insights

The global Radioactive Shipping Containers market is projected for robust growth, reaching an estimated market size of approximately $1.2 billion by 2025, with a Compound Annual Growth Rate (CAGR) of around 6.5% anticipated to persist through 2033. This expansion is primarily fueled by the increasing demand for safe and compliant transportation of radioactive materials across various critical sectors. The manufacturing industry, a significant consumer, utilizes these containers for the movement of radiopharmaceuticals, radioisotopes for industrial imaging, and other radioactive sources. Similarly, the mining industry, particularly in uranium extraction, requires specialized containers for transporting radioactive ores and waste. The pharmaceutical industry's growing reliance on radiopharmaceuticals for diagnostic and therapeutic applications further propels market demand. Emerging economies are also contributing to this growth as they expand their nuclear power capacities and healthcare infrastructure.

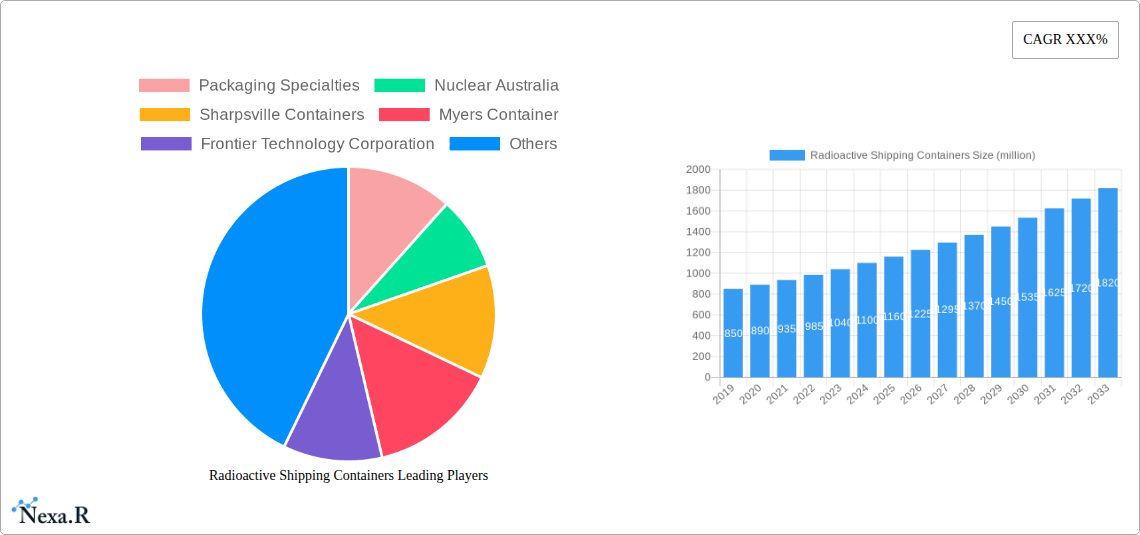

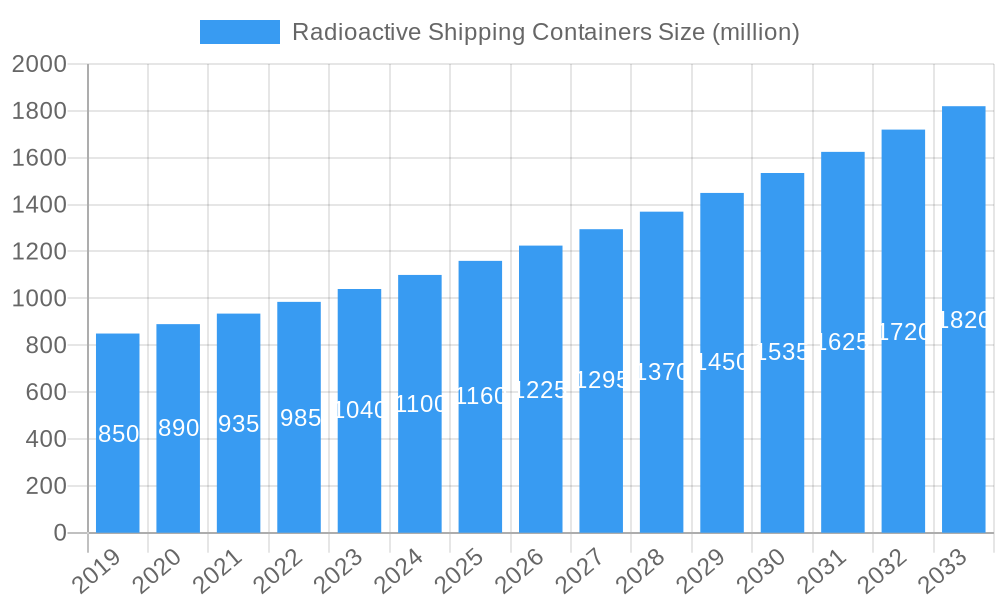

Radioactive Shipping Containers Market Size (In Million)

However, the market faces certain restraints that necessitate strategic approaches. Stringent regulatory frameworks and the high cost associated with compliance, manufacturing, and disposal of radioactive materials can pose challenges. Public perception and concerns regarding the safety of transporting radioactive substances, coupled with the risk of accidents, also influence market dynamics. Nonetheless, technological advancements in container design, focusing on enhanced shielding, durability, and containment, are actively addressing these concerns. Innovations in materials science and engineering are leading to lighter yet more robust containers, improving logistical efficiency and safety profiles. The market is segmented by application and type, with Type A packaging dominating the current landscape due to its widespread use in routine transport of low-level radioactive materials. The ongoing research and development efforts are expected to introduce more advanced Type B packaging solutions for higher-risk materials, further shaping the market's future trajectory.

Radioactive Shipping Containers Company Market Share

Radioactive Shipping Containers Market Research Report: Dynamics, Trends, and Future Outlook (2019-2033)

This comprehensive report provides an in-depth analysis of the global radioactive shipping containers market. Leveraging extensive historical data and expert forecasts, we delve into market dynamics, growth trends, regional dominance, product innovations, key challenges, emerging opportunities, and the competitive landscape. The study covers the period from 2019 to 2033, with a base year of 2025, offering actionable insights for industry stakeholders.

Radioactive Shipping Containers Market Dynamics & Structure

The radioactive shipping containers market exhibits moderate concentration, with a mix of established players and emerging innovators. Key drivers of technological innovation include advancements in shielding materials for enhanced safety, improved container designs for easier handling and increased capacity, and the development of smart features for real-time monitoring of contents. Regulatory frameworks, particularly stringent international standards from bodies like the IAEA, play a pivotal role in shaping product development and market entry. Competitive product substitutes, while limited for highly radioactive materials, can emerge in the form of alternative transportation methods or advancements in on-site material management. End-user demographics are largely defined by nuclear power generation, medical isotope production, research institutions, and mining operations, each with unique containment and transport needs. Mergers and acquisitions (M&A) trends, though not as frequent as in broader industrial sectors, are observed as companies seek to expand their product portfolios, gain technological expertise, or secure market share. For instance, a potential M&A deal volume of approximately $XX million over the forecast period could consolidate specialized capabilities. Barriers to innovation include the high cost of research and development, the lengthy and rigorous certification processes for new container designs, and the inherent risks associated with handling radioactive materials.

- Market Concentration: Moderate, with a few dominant players and a growing number of niche providers.

- Technological Innovation Drivers: Advanced shielding, ergonomic designs, real-time monitoring capabilities.

- Regulatory Frameworks: Strict international standards (IAEA) are paramount.

- Competitive Product Substitutes: Limited for high-level radioactive waste, but potential exists in alternative logistics.

- End-User Demographics: Nuclear power, medical isotopes, research, mining.

- M&A Trends: Strategic acquisitions to gain technology or market access.

- Innovation Barriers: High R&D costs, lengthy certification, safety risks.

Radioactive Shipping Containers Growth Trends & Insights

The radioactive shipping containers market is poised for steady growth, projected to reach approximately $XXX million by 2033. This expansion is fueled by the increasing global demand for nuclear energy as a low-carbon power source, the growing use of radioisotopes in medical diagnostics and treatments, and ongoing advancements in industrial applications. The compound annual growth rate (CAGR) for the forecast period (2025-2033) is estimated at XX%, indicating a robust upward trajectory. Adoption rates for advanced, compliant containers are steadily rising as regulatory scrutiny intensifies and safety standards evolve. Technological disruptions are primarily focused on enhancing the safety, efficiency, and traceability of radioactive material transport. Innovations in composite materials for lighter yet more robust containers, along with the integration of IoT devices for real-time tracking and environmental monitoring, are set to redefine industry standards. Consumer behavior shifts are observable, with end-users increasingly prioritizing suppliers offering comprehensive service packages, including regulatory compliance support, custom design solutions, and robust logistical networks. The market penetration of Type B packaging, designed for higher-risk radioactive materials, is expected to grow in parallel with the expansion of nuclear power and advanced medical applications. The historical period (2019-2024) has seen a steady increase in demand, driven by established nuclear infrastructure and a growing awareness of safe radioactive material handling.

- Market Size Evolution: Projected to reach $XXX million by 2033.

- CAGR: Estimated at XX% for 2025-2033.

- Adoption Rates: Increasing for advanced and compliant containers.

- Technological Disruptions: Focus on enhanced safety, efficiency, and traceability.

- Consumer Behavior Shifts: Preference for comprehensive service packages and regulatory compliance.

- Market Penetration: Growing demand for Type B packaging.

- Historical Growth (2019-2024): Steady increase driven by established infrastructure and safety awareness.

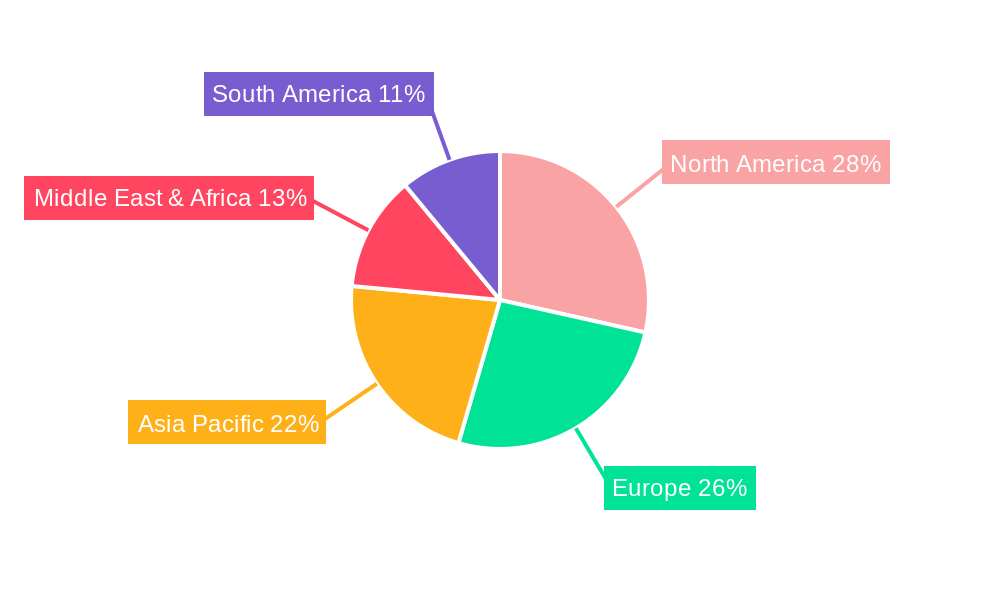

Dominant Regions, Countries, or Segments in Radioactive Shipping Containers

The Manufacturing Industry segment, specifically within the broader context of nuclear fuel cycle operations and specialized industrial radiography, is a dominant driver of growth for radioactive shipping containers. This segment's dominance is underpinned by the consistent need for secure and compliant transport of various radioactive sources and waste materials generated during manufacturing processes. Economically developed regions with established nuclear power infrastructure, such as North America and Europe, exhibit significant market share due to extensive operational facilities and a robust regulatory enforcement regime. For instance, the United States and France individually account for approximately XX% and YY% of the global market share respectively, driven by their large nuclear power fleets and advanced research sectors. Key drivers within these regions include government policies supporting nuclear energy, substantial investment in infrastructure upgrades for handling radioactive materials, and a highly developed network of specialized logistics providers. The Type B Packaging segment also holds considerable sway, as it caters to the transportation of higher-risk radioactive materials, including spent nuclear fuel and high-activity sources, which are crucial for both energy production and advanced medical treatments. Growth potential in these dominant segments is further amplified by the ongoing decommissioning of older nuclear facilities, which necessitates the safe and secure transport of radioactive waste. The Pharmaceutical Industry is also a significant, albeit secondary, contributor, with increasing demand for shielded containers for radioisotopes used in diagnostics and targeted therapies. The market share for the Manufacturing Industry application is estimated at XX% of the total market, with Type B Packaging representing YY% of the total container types.

- Dominant Application Segment: Manufacturing Industry (nuclear fuel cycle, industrial radiography).

- Dominant Packaging Type: Type B Packaging.

- Leading Regions: North America, Europe.

- Key Countries & Market Share: United States (XX%), France (YY%).

- Key Drivers (Regional): Supportive government policies for nuclear energy, infrastructure investment, advanced logistics networks.

- Growth Potential Drivers: Nuclear facility decommissioning, increasing use of radioisotopes in medicine.

- Market Share (Application): Manufacturing Industry (XX%).

- Market Share (Type): Type B Packaging (YY%).

Radioactive Shipping Containers Product Landscape

The radioactive shipping containers product landscape is characterized by a relentless focus on enhanced safety, compliance, and operational efficiency. Innovations include the development of multi-layered shielding solutions, often utilizing advanced composites and depleted uranium alloys, to meet increasingly stringent radiation attenuation requirements. Designs are evolving to incorporate features like impact-resistant outer shells, integrated temperature control systems for sensitive isotopes, and user-friendly handling mechanisms to minimize human exposure. Performance metrics are rigorously tested against international standards for drop, puncture, fire, and immersion resistance. Unique selling propositions often lie in custom-engineered solutions tailored to specific radioactive material types and transport routes, as well as the integration of advanced tracking and monitoring technologies. Technological advancements are also seen in materials science, leading to lighter, more durable containers that reduce transportation costs while maintaining superior protection.

Key Drivers, Barriers & Challenges in Radioactive Shipping Containers

Key Drivers:

- Increasing Global Nuclear Energy Demand: A fundamental driver as more reactors come online and require safe transport of fuel and waste.

- Growth in Medical Radioisotope Applications: Expanding use in diagnostics and therapies necessitates reliable containment solutions.

- Stringent Regulatory Compliance: Evolving international and national safety regulations mandate advanced container designs.

- Technological Advancements in Materials and Design: Innovations lead to safer, more efficient, and cost-effective solutions.

- Decommissioning of Nuclear Facilities: This process generates significant volumes of radioactive waste requiring specialized transport.

Key Barriers & Challenges:

- High Costs of Development and Certification: Rigorous testing and regulatory approval processes are expensive and time-consuming.

- Supply Chain Disruptions and Lead Times: Specialized materials and manufacturing processes can lead to extended production cycles.

- Complex Regulatory Landscape: Navigating differing international and national regulations can be challenging.

- Public Perception and Safety Concerns: Negative public sentiment surrounding nuclear materials can impact project approvals and operations.

- Skilled Workforce Shortage: A limited pool of experienced engineers and technicians specialized in radioactive containment.

- Competition from Alternative Technologies: While limited for high-level waste, advancements in on-site storage can indirectly impact transport demand. The impact of supply chain disruptions can lead to extended lead times of up to XX months for critical components.

Emerging Opportunities in Radioactive Shipping Containers

Emerging opportunities in the radioactive shipping containers sector are centered around the development of solutions for the burgeoning small modular reactor (SMR) market, requiring specialized transport of novel fuel forms. Furthermore, there is growing demand for enhanced security features, including tamper-evident seals and advanced tracking systems, to address evolving security threats. The increasing global focus on sustainable waste management practices also presents opportunities for innovative recycling and repurposing of spent fuel, which will involve specialized containment. Untapped markets in developing economies with nascent nuclear programs or expanding medical isotope production offer significant growth potential. The development of standardized, modular container designs for increased interoperability and reduced customization costs is another avenue for future growth.

Growth Accelerators in the Radioactive Shipping Containers Industry

The radioactive shipping containers industry is experiencing sustained growth acceleration driven by several key catalysts. The ongoing global energy transition, with many nations revisiting or expanding their nuclear power portfolios, is a primary growth accelerator. This is complemented by continuous advancements in medical imaging and targeted radionuclide therapies, which directly correlate with the demand for transporting these critical isotopes. Furthermore, significant investments in upgrading and expanding existing nuclear infrastructure worldwide, including the decommissioning of older plants, are creating a steady stream of demand for compliant and robust shipping solutions. The increasing stringency and harmonization of international safety regulations also act as a powerful accelerator, pushing manufacturers to innovate and adopt higher standards. Strategic partnerships between container manufacturers, logistics providers, and research institutions are fostering faster development cycles and market penetration.

Key Players Shaping the Radioactive Shipping Containers Market

- Packaging Specialties

- Nuclear Australia

- Sharpsville Containers

- Myers Container

- Frontier Technology Corporation

- Wagstaff Applied Technologies

- Comecer

- Nuclear Shields

- Gammadata

- Lemer Pax

- Hopewell Designs

- Nordion

- MarShield

- Thermo Fisher Scientific

- Mirion Technologies

- Berthold Technologies

- Transnuclear Inc. (AREVA)

- Ortec (AMETEK)

- Precision Custom Components (PCC)

Notable Milestones in Radioactive Shipping Containers Sector

- 2019: Launch of enhanced shielding materials for Type B containers by Nuclear Shields, improving radiation attenuation by approximately XX%.

- 2020: Gammadata secures a significant contract for spent fuel transportation casks for a European nuclear power plant decommissioning project.

- 2021: Thermo Fisher Scientific introduces advanced real-time tracking and monitoring systems for radioactive source transport, enhancing security.

- 2022: Mirion Technologies acquires a specialized container manufacturer, expanding its product portfolio for medical isotope transport.

- 2023: Wagstaff Applied Technologies patents a new lightweight composite material for Type A packaging, reducing transport weight by XX%.

- 2024: Transnuclear Inc. (AREVA) announces successful completion of rigorous testing for a new generation of cask designs to meet evolving regulatory demands.

In-Depth Radioactive Shipping Containers Market Outlook

The radioactive shipping containers market is projected for sustained and robust growth, driven by the enduring importance of nuclear energy, the rapid expansion of radioisotope applications in healthcare, and the ongoing global effort to safely manage radioactive waste. Key growth accelerators, including technological breakthroughs in materials science and an increasingly stringent regulatory environment, will continue to propel the industry forward. Strategic partnerships and market expansion into emerging economies with developing nuclear infrastructure represent significant future opportunities. The market is expected to witness further consolidation and specialization, with companies focusing on delivering integrated solutions that encompass not only container manufacturing but also logistics, regulatory support, and end-of-life services. The overall outlook is positive, indicating a strong and expanding market for these critical containment solutions.

Radioactive Shipping Containers Segmentation

-

1. Application

- 1.1. Manufacturing Industry

- 1.2. Mining Industry

- 1.3. Pharmaceutical Industry

- 1.4. Others

-

2. Type

- 2.1. Type A Packaging

- 2.2. Type B Packaging

Radioactive Shipping Containers Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Radioactive Shipping Containers Regional Market Share

Geographic Coverage of Radioactive Shipping Containers

Radioactive Shipping Containers REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Radioactive Shipping Containers Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Manufacturing Industry

- 5.1.2. Mining Industry

- 5.1.3. Pharmaceutical Industry

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Type A Packaging

- 5.2.2. Type B Packaging

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Radioactive Shipping Containers Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Manufacturing Industry

- 6.1.2. Mining Industry

- 6.1.3. Pharmaceutical Industry

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Type A Packaging

- 6.2.2. Type B Packaging

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Radioactive Shipping Containers Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Manufacturing Industry

- 7.1.2. Mining Industry

- 7.1.3. Pharmaceutical Industry

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Type A Packaging

- 7.2.2. Type B Packaging

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Radioactive Shipping Containers Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Manufacturing Industry

- 8.1.2. Mining Industry

- 8.1.3. Pharmaceutical Industry

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Type A Packaging

- 8.2.2. Type B Packaging

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Radioactive Shipping Containers Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Manufacturing Industry

- 9.1.2. Mining Industry

- 9.1.3. Pharmaceutical Industry

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Type A Packaging

- 9.2.2. Type B Packaging

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Radioactive Shipping Containers Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Manufacturing Industry

- 10.1.2. Mining Industry

- 10.1.3. Pharmaceutical Industry

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Type A Packaging

- 10.2.2. Type B Packaging

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Packaging Specialties

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Nuclear Australia

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Sharpsville Containers

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Myers Container

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Frontier Technology Corporation

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Wagstaff Applied Technologies

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Comecer

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Nuclear Shields

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Gammadata

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Lemer Pax

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Hopewell Designs

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Nordion

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 MarShield

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Thermo Fisher Scientific

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Mirion Technologies

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Berthold Technologies

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Transnuclear Inc. (AREVA)

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Ortec (AMETEK)

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Precision Custom Components (PCC)

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.1 Packaging Specialties

List of Figures

- Figure 1: Global Radioactive Shipping Containers Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Radioactive Shipping Containers Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Radioactive Shipping Containers Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Radioactive Shipping Containers Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Radioactive Shipping Containers Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Radioactive Shipping Containers Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Radioactive Shipping Containers Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Radioactive Shipping Containers Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Radioactive Shipping Containers Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Radioactive Shipping Containers Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Radioactive Shipping Containers Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Radioactive Shipping Containers Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Radioactive Shipping Containers Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Radioactive Shipping Containers Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Radioactive Shipping Containers Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Radioactive Shipping Containers Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Radioactive Shipping Containers Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Radioactive Shipping Containers Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Radioactive Shipping Containers Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Radioactive Shipping Containers Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Radioactive Shipping Containers Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Radioactive Shipping Containers Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Radioactive Shipping Containers Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Radioactive Shipping Containers Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Radioactive Shipping Containers Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Radioactive Shipping Containers Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Radioactive Shipping Containers Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Radioactive Shipping Containers Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Radioactive Shipping Containers Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Radioactive Shipping Containers Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Radioactive Shipping Containers Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Radioactive Shipping Containers Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Radioactive Shipping Containers Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Radioactive Shipping Containers Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Radioactive Shipping Containers Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Radioactive Shipping Containers Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Radioactive Shipping Containers Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Radioactive Shipping Containers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Radioactive Shipping Containers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Radioactive Shipping Containers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Radioactive Shipping Containers Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Radioactive Shipping Containers Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Radioactive Shipping Containers Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Radioactive Shipping Containers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Radioactive Shipping Containers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Radioactive Shipping Containers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Radioactive Shipping Containers Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Radioactive Shipping Containers Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Radioactive Shipping Containers Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Radioactive Shipping Containers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Radioactive Shipping Containers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Radioactive Shipping Containers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Radioactive Shipping Containers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Radioactive Shipping Containers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Radioactive Shipping Containers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Radioactive Shipping Containers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Radioactive Shipping Containers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Radioactive Shipping Containers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Radioactive Shipping Containers Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Radioactive Shipping Containers Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Radioactive Shipping Containers Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Radioactive Shipping Containers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Radioactive Shipping Containers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Radioactive Shipping Containers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Radioactive Shipping Containers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Radioactive Shipping Containers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Radioactive Shipping Containers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Radioactive Shipping Containers Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Radioactive Shipping Containers Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Radioactive Shipping Containers Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Radioactive Shipping Containers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Radioactive Shipping Containers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Radioactive Shipping Containers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Radioactive Shipping Containers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Radioactive Shipping Containers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Radioactive Shipping Containers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Radioactive Shipping Containers Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Radioactive Shipping Containers?

The projected CAGR is approximately 6%.

2. Which companies are prominent players in the Radioactive Shipping Containers?

Key companies in the market include Packaging Specialties, Nuclear Australia, Sharpsville Containers, Myers Container, Frontier Technology Corporation, Wagstaff Applied Technologies, Comecer, Nuclear Shields, Gammadata, Lemer Pax, Hopewell Designs, Nordion, MarShield, Thermo Fisher Scientific, Mirion Technologies, Berthold Technologies, Transnuclear Inc. (AREVA), Ortec (AMETEK), Precision Custom Components (PCC).

3. What are the main segments of the Radioactive Shipping Containers?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Radioactive Shipping Containers," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Radioactive Shipping Containers report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Radioactive Shipping Containers?

To stay informed about further developments, trends, and reports in the Radioactive Shipping Containers, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence