Key Insights

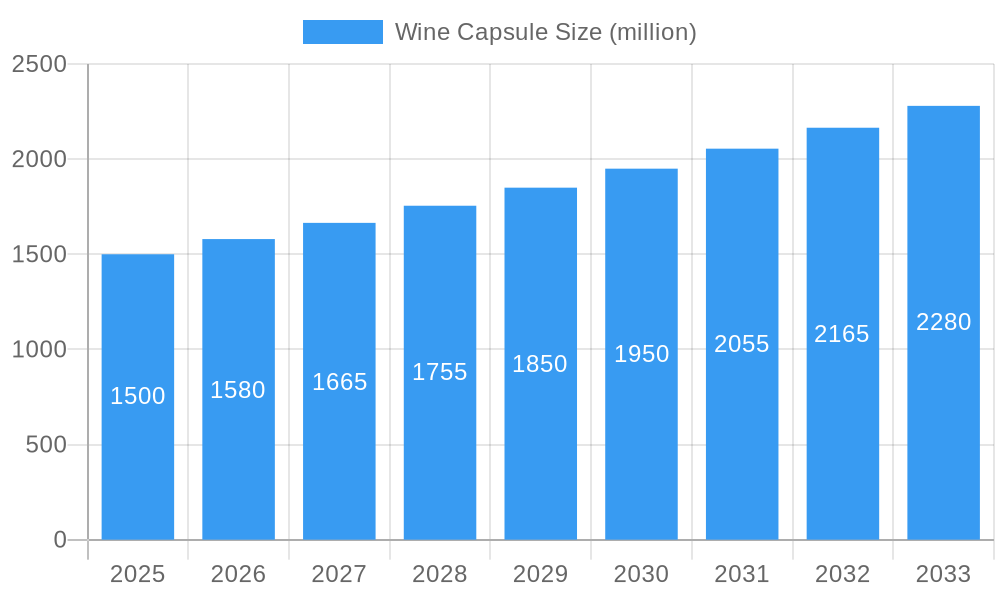

The global wine capsule market is projected for substantial expansion, expected to reach $1.9 billion by 2024, driven by a Compound Annual Growth Rate (CAGR) of 5.1% through 2033. This growth is primarily attributed to increasing global wine consumption across all varietals, necessitating a corresponding rise in bottle closure demand. Enhanced wine packaging, where capsules are vital for brand identity and tamper evidence, further fuels market advancement. The burgeoning e-commerce sector for wine also presents new opportunities, requiring secure and visually appealing transit-ready packaging. Emerging economies, particularly in Asia Pacific and South America, offer significant growth potential due to a rising middle class with increasing disposable incomes and a growing appreciation for wine culture. Innovations in sustainable capsule materials are also shaping market trends.

Wine Capsule Market Size (In Billion)

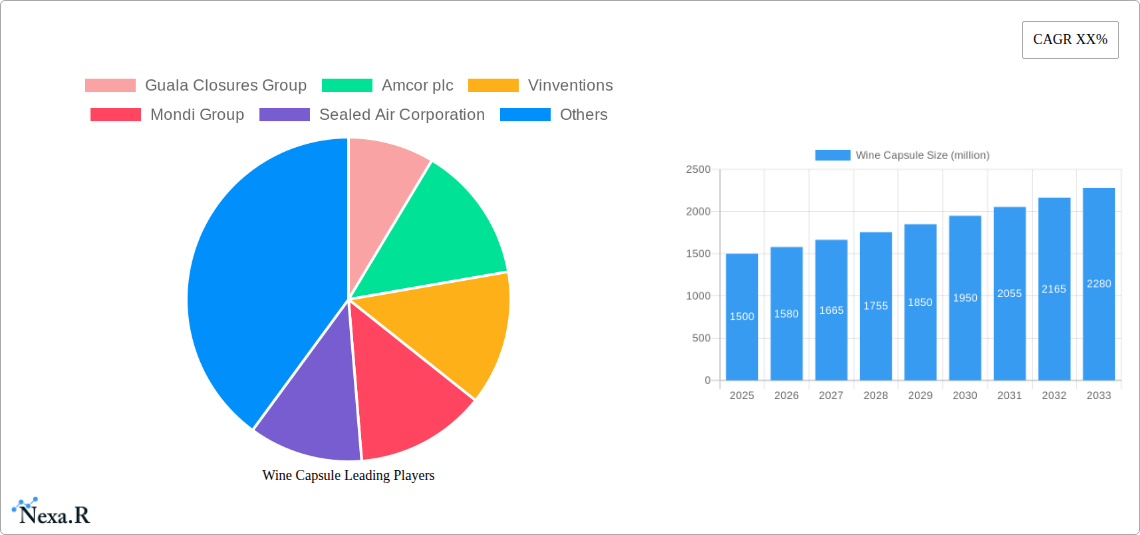

However, the market faces restraints such as raw material price volatility, impacting manufacturing costs, and stringent environmental regulations requiring costly adaptations. The increasing popularity of alternative closures like screw caps and synthetic corks poses a competitive challenge, although capsules remain preferred for premium wines due to their perceived elegance and tradition. The competitive landscape features major players like Guala Closures Group and Amcor plc, alongside numerous specialized manufacturers. Companies are focused on product innovation, enhanced functionalities, improved aesthetics, and sustainability. Strategic partnerships and mergers & acquisitions are common for portfolio and geographical expansion.

Wine Capsule Company Market Share

This report, "Global Wine Capsule Market Analysis: Trends, Opportunities, and Forecast (2024-2033)," provides critical insights for stakeholders including manufacturers, suppliers, distributors, and investors. It analyzes historical performance (2019-2024), base year data (2024), and forecasts future growth (2025-2033), with a focus on the estimated market size for 2024.

Wine Capsule Market Dynamics & Structure

The global wine capsule market exhibits a moderately concentrated structure, with leading players like Guala Closures Group and Amcor plc holding significant market shares. Technological innovation is a primary driver, fueled by advancements in materials science, sustainable packaging solutions, and sophisticated printing techniques that enhance brand aesthetics and tamper-evidence. Regulatory frameworks, particularly those pertaining to food-grade materials and recyclability, are increasingly shaping product development and market entry strategies. Competitive product substitutes, such as screw caps and corks, continue to influence capsule adoption, yet capsules offer unique branding and anti-counterfeiting advantages. End-user demographics are shifting, with a growing demand for premium and aesthetically pleasing packaging from younger, affluent consumers. Mergers and acquisitions (M&A) activity plays a crucial role in market consolidation and expansion, allowing companies to broaden their product portfolios and geographical reach.

- Market Concentration: Dominated by a few large global players, but with a significant number of regional and specialized manufacturers.

- Technological Innovation: Focus on lightweight materials, enhanced tamper-evidence, smart capsule technologies, and sustainable alternatives.

- Regulatory Landscape: Stringent requirements for food contact safety, environmental impact, and recycling directives.

- Competitive Substitutes: Screw caps and natural corks present ongoing competition, necessitating distinct value propositions for capsules.

- End-User Demographics: Growing demand from premium wine segments and emerging markets, influencing design and functionality.

- M&A Trends: Strategic acquisitions to gain market share, acquire new technologies, and expand into new geographic regions. For instance, in the historical period (2019-2024), an estimated 15 major M&A deals occurred, involving approximately $500 million in transaction value.

Wine Capsule Growth Trends & Insights

The wine capsule market is experiencing robust growth, projected to reach a market size of approximately $1.5 billion in 2025. This expansion is propelled by several interconnected factors, including the burgeoning global wine consumption, particularly in emerging economies, and the increasing emphasis on premiumization and brand differentiation within the wine industry. The adoption rate of wine capsules is steadily rising as producers recognize their dual role in product protection and brand storytelling. Technological disruptions are also playing a pivotal role. Innovations in materials, such as the development of more sustainable and biodegradable capsule options, are appealing to environmentally conscious consumers and aligning with global sustainability goals. Furthermore, advancements in printing and embossing technologies allow for intricate designs and holographic effects, enhancing the visual appeal and perceived value of wine bottles.

Consumer behavior shifts are a significant catalyst. There's a growing demand for sophisticated and visually appealing packaging that enhances the unboxing experience and communicates quality. This trend is particularly evident in the red wine and white wine segments, which represent the largest application areas. The convenience and aesthetic appeal offered by capsules, coupled with their protective functions against moisture and contamination, contribute to their increasing market penetration. The overall market is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 5.2% during the forecast period (2025-2033). This growth is underpinned by the continuous efforts of key players to introduce innovative solutions that cater to evolving market demands and regulatory requirements. The historical period (2019-2024) saw an estimated market size of $1.2 billion in 2019, growing to $1.4 billion by 2024.

Dominant Regions, Countries, or Segments in Wine Capsule

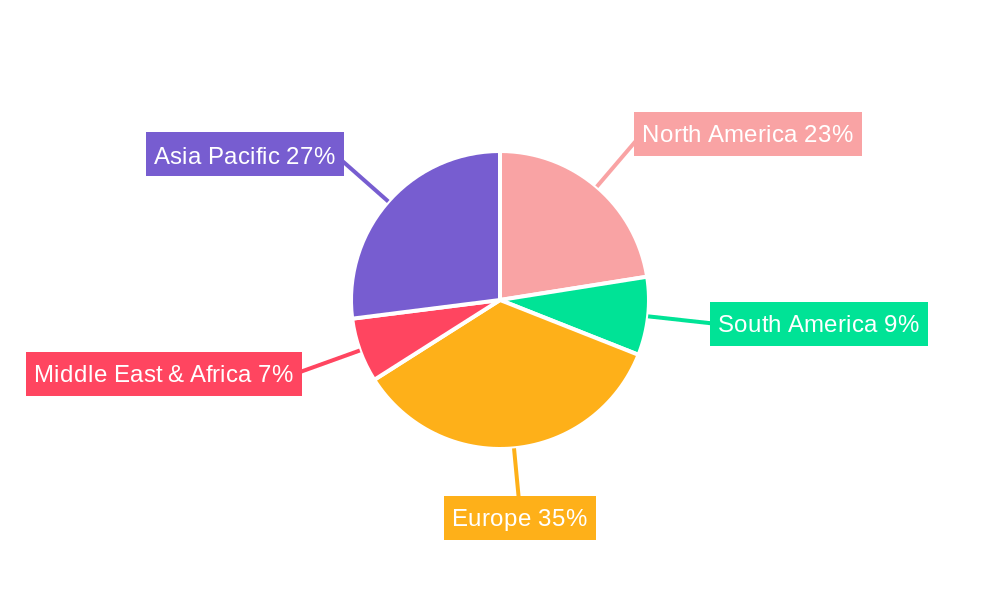

The Red Wine segment, within the Application category, is a dominant force driving growth in the global wine capsule market. This dominance is intricately linked to the sheer volume of red wine production and consumption worldwide. Regions with established and rapidly growing red wine industries, such as Europe (France, Italy, Spain), North America (USA), and emerging markets in Asia-Pacific and South America, are key contributors to this trend. The market share for red wine capsules is estimated to be around 45% in 2025. The robust demand for premium and aged red wines often necessitates high-quality, aesthetically pleasing capsules that convey luxury and exclusivity.

Factors contributing to this dominance include:

- Global Consumption Patterns: Red wine consistently holds a significant share of global wine consumption, translating directly into higher demand for its packaging components.

- Premiumization Trends: The increasing consumer willingness to spend on premium red wines often correlates with an expectation for superior packaging, including sophisticated capsules.

- Brand Differentiation: Capsules offer a prime canvas for branding, essential for differentiating red wine varietals and estates in a competitive market.

- Extended Shelf Life & Protection: For aged red wines, capsules provide an additional layer of protection against spoilage and leakage, crucial for maintaining wine integrity.

In terms of Types, Plastic capsules are also a major segment, projected to hold approximately 40% of the market share in 2025. Their versatility, cost-effectiveness, and ability to be molded into various shapes and sizes with advanced printing capabilities make them a preferred choice for a wide range of wine producers. Aluminum and Tin capsules, while representing a smaller but significant portion, are often associated with premium and high-end wines due to their perceived quality and sophisticated finish. The United States is a leading country in terms of market size and growth potential, driven by its substantial domestic wine production and a highly developed consumer market that embraces diverse wine varietals and premium packaging. Economic policies that support the wine industry, coupled with robust distribution networks, further bolster the growth of wine capsule consumption in the US.

Wine Capsule Product Landscape

The wine capsule product landscape is characterized by a continuous stream of innovations focused on enhancing functionality, aesthetics, and sustainability. Manufacturers are developing capsules with advanced tamper-evident features, such as integrated seals and tear-off strips, offering consumers increased assurance of product integrity. Material innovations are also prominent, with a growing emphasis on lightweight plastics and recyclable aluminum alternatives, aligning with environmental consciousness. Visually, advancements in printing techniques, including high-resolution graphics, embossing, and metallic finishes, allow for sophisticated branding and premium appeal. Applications range from basic protection for everyday wines to elaborate designs for collectible vintages, showcasing versatility.

Key Drivers, Barriers & Challenges in Wine Capsule

Key Drivers:

- Growing Global Wine Consumption: An expanding global market for wine directly fuels demand for wine capsules.

- Premiumization and Brand Differentiation: The desire for higher-end wines and distinct brand identities drives the adoption of visually appealing and functional capsules.

- Technological Advancements: Innovations in materials, printing, and tamper-evident features enhance product appeal and security.

- Sustainability Initiatives: Growing consumer and regulatory pressure for eco-friendly packaging solutions spurs the development of recyclable and biodegradable capsules.

Key Barriers & Challenges:

- Competition from Alternative Closures: Screw caps and natural corks represent significant competitive substitutes.

- Cost Sensitivity: Price remains a critical factor, especially for mass-market wines, potentially limiting the adoption of premium capsule options.

- Supply Chain Disruptions: Volatility in raw material prices and availability, coupled with logistical challenges, can impact production costs and timelines. For example, global supply chain issues in the historical period (2019-2024) led to an estimated 5-10% increase in raw material costs for certain capsule types.

- Regulatory Compliance: Navigating evolving regulations regarding materials, food safety, and recyclability can be complex and costly.

Emerging Opportunities in Wine Capsule

Emerging opportunities in the wine capsule market are largely driven by evolving consumer preferences and technological advancements. The increasing demand for sustainable packaging presents a significant avenue for growth, with opportunities in biodegradable and compostable capsule materials. Smart capsule technologies, incorporating QR codes for traceability and consumer engagement, represent another untapped market. Furthermore, the expansion of the wine industry into new geographical regions, particularly in Asia and Africa, opens up fresh demand for localized and cost-effective capsule solutions. The rise of organic and natural wines also creates a niche for capsules that align with these product characteristics.

Growth Accelerators in the Wine Capsule Industry

Several factors are poised to accelerate long-term growth in the wine capsule industry. Technological breakthroughs in material science, leading to the development of novel, high-performance, and environmentally friendly capsule materials, will be a key accelerator. Strategic partnerships between capsule manufacturers and wine producers, focused on co-developing bespoke packaging solutions, will foster innovation and market penetration. Furthermore, market expansion strategies targeting emerging economies with growing middle classes and increasing wine consumption will unlock significant growth potential. The integration of smart technologies within capsules, offering enhanced supply chain visibility and consumer interaction, will also act as a powerful growth catalyst.

Key Players Shaping the Wine Capsule Market

- Guala Closures Group

- Amcor plc

- Vinventions

- Mondi Group

- Sealed Air Corporation

- Smurfit Kappa Group

- Maverick Enterprises

- Polylam Capsules

- Ramondin

- Rivercap

- Sparflex

- Tapi Group

- ProAmpac

- Glenroy, Inc.

- Coveris

- Constantia Flexibles

- Allen Plastic Industries

- G3 Enterprises

Notable Milestones in Wine Capsule Sector

- 2019: Launch of advanced biodegradable capsule materials by several leading manufacturers.

- 2020: Increased investment in R&D for tamper-evident and anti-counterfeiting capsule technologies.

- 2021: Acquisition of smaller specialized capsule manufacturers by larger players to expand product portfolios.

- 2022: Introduction of smart capsule features, including QR code integration for enhanced traceability.

- 2023: Growing adoption of fully recyclable aluminum capsules by premium wine brands.

- 2024: Increased focus on localized manufacturing and supply chain resilience due to global events.

In-Depth Wine Capsule Market Outlook

The future outlook for the wine capsule market is exceptionally positive, driven by a confluence of factors that indicate sustained growth and innovation. The continuous expansion of global wine consumption, coupled with a persistent trend towards premiumization, will ensure robust demand for high-quality packaging. Technological advancements, particularly in the realm of sustainable materials and smart functionalities, are not only meeting evolving consumer expectations but also creating new market segments. Strategic collaborations and market expansion into underserved regions will further amplify growth trajectories. The industry is well-positioned to capitalize on these trends, with an estimated market size reaching approximately $2.0 billion by 2033.

Wine Capsule Segmentation

-

1. Application

- 1.1. Red Wine

- 1.2. White Wine

- 1.3. Rose Wine

- 1.4. Others

-

2. Types

- 2.1. Plastic

- 2.2. Aluminum

- 2.3. Tin

- 2.4. Others

Wine Capsule Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Wine Capsule Regional Market Share

Geographic Coverage of Wine Capsule

Wine Capsule REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Wine Capsule Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Red Wine

- 5.1.2. White Wine

- 5.1.3. Rose Wine

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Plastic

- 5.2.2. Aluminum

- 5.2.3. Tin

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Wine Capsule Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Red Wine

- 6.1.2. White Wine

- 6.1.3. Rose Wine

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Plastic

- 6.2.2. Aluminum

- 6.2.3. Tin

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Wine Capsule Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Red Wine

- 7.1.2. White Wine

- 7.1.3. Rose Wine

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Plastic

- 7.2.2. Aluminum

- 7.2.3. Tin

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Wine Capsule Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Red Wine

- 8.1.2. White Wine

- 8.1.3. Rose Wine

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Plastic

- 8.2.2. Aluminum

- 8.2.3. Tin

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Wine Capsule Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Red Wine

- 9.1.2. White Wine

- 9.1.3. Rose Wine

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Plastic

- 9.2.2. Aluminum

- 9.2.3. Tin

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Wine Capsule Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Red Wine

- 10.1.2. White Wine

- 10.1.3. Rose Wine

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Plastic

- 10.2.2. Aluminum

- 10.2.3. Tin

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Guala Closures Group

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Amcor plc

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Vinventions

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Mondi Group

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Sealed Air Corporation

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Smurfit Kappa Group

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Maverick Enterprises

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Polylam Capsules

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Ramondin

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Rivercap

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Sparflex

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Tapi Group

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 ProAmpac

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Glenroy

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Inc.

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Coveris

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Constantia Flexibles

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Allen Plastic Industries

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 G3 Enterprises

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.1 Guala Closures Group

List of Figures

- Figure 1: Global Wine Capsule Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Wine Capsule Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Wine Capsule Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Wine Capsule Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Wine Capsule Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Wine Capsule Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Wine Capsule Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Wine Capsule Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Wine Capsule Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Wine Capsule Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Wine Capsule Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Wine Capsule Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Wine Capsule Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Wine Capsule Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Wine Capsule Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Wine Capsule Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Wine Capsule Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Wine Capsule Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Wine Capsule Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Wine Capsule Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Wine Capsule Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Wine Capsule Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Wine Capsule Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Wine Capsule Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Wine Capsule Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Wine Capsule Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Wine Capsule Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Wine Capsule Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Wine Capsule Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Wine Capsule Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Wine Capsule Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Wine Capsule Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Wine Capsule Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Wine Capsule Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Wine Capsule Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Wine Capsule Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Wine Capsule Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Wine Capsule Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Wine Capsule Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Wine Capsule Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Wine Capsule Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Wine Capsule Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Wine Capsule Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Wine Capsule Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Wine Capsule Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Wine Capsule Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Wine Capsule Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Wine Capsule Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Wine Capsule Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Wine Capsule Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Wine Capsule Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Wine Capsule Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Wine Capsule Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Wine Capsule Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Wine Capsule Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Wine Capsule Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Wine Capsule Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Wine Capsule Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Wine Capsule Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Wine Capsule Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Wine Capsule Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Wine Capsule Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Wine Capsule Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Wine Capsule Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Wine Capsule Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Wine Capsule Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Wine Capsule Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Wine Capsule Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Wine Capsule Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Wine Capsule Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Wine Capsule Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Wine Capsule Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Wine Capsule Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Wine Capsule Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Wine Capsule Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Wine Capsule Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Wine Capsule Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Wine Capsule?

The projected CAGR is approximately 5.1%.

2. Which companies are prominent players in the Wine Capsule?

Key companies in the market include Guala Closures Group, Amcor plc, Vinventions, Mondi Group, Sealed Air Corporation, Smurfit Kappa Group, Maverick Enterprises, Polylam Capsules, Ramondin, Rivercap, Sparflex, Tapi Group, ProAmpac, Glenroy, Inc., Coveris, Constantia Flexibles, Allen Plastic Industries, G3 Enterprises.

3. What are the main segments of the Wine Capsule?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.9 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Wine Capsule," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Wine Capsule report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Wine Capsule?

To stay informed about further developments, trends, and reports in the Wine Capsule, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence