Key Insights

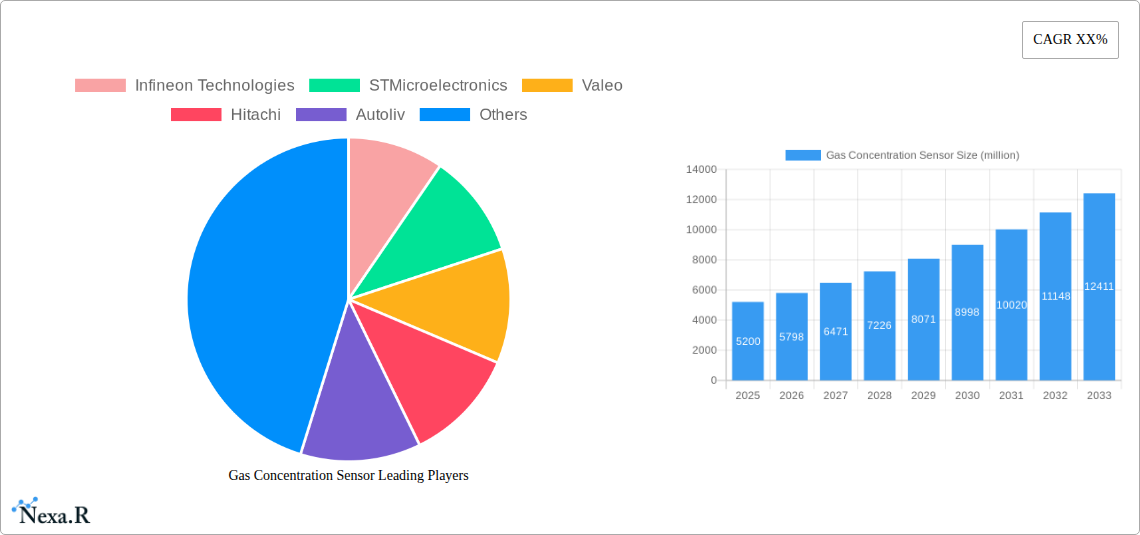

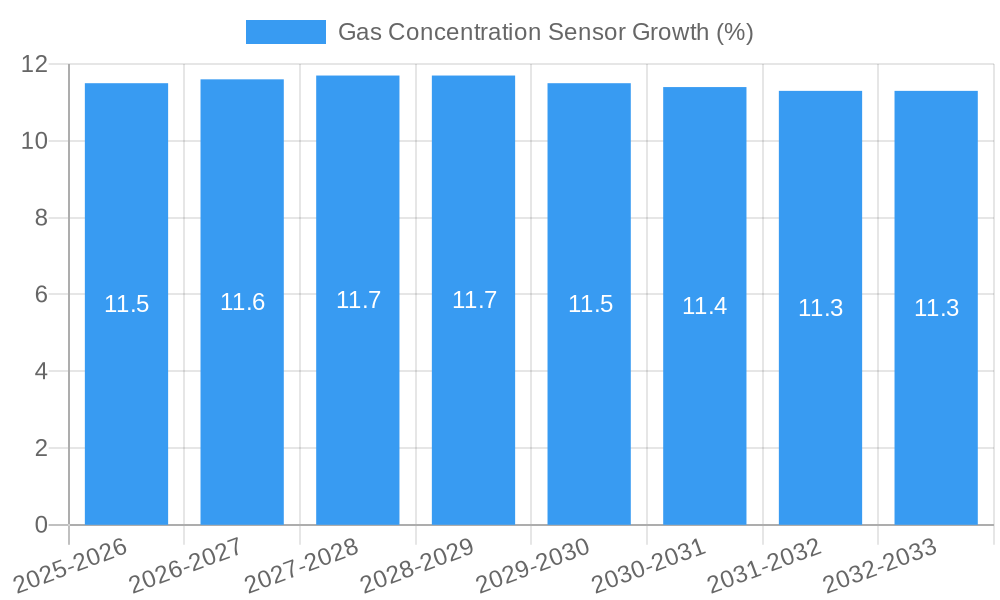

The global Gas Concentration Sensor market is poised for significant expansion, projected to reach an estimated USD 5,200 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of 11.5% throughout the forecast period of 2025-2033. This dynamic growth is primarily fueled by the escalating demand for enhanced automotive safety and emissions control systems. As regulatory bodies worldwide tighten emission standards, the need for sophisticated gas concentration sensors to monitor and manage exhaust gases in both passenger and commercial vehicles intensifies. The increasing adoption of advanced driver-assistance systems (ADAS) and autonomous driving technologies further amplifies this requirement, as these systems rely on accurate real-time data from sensors to ensure optimal performance and safety. The proliferation of connected car technologies also contributes to market growth, enabling remote monitoring and diagnostics of vehicle emissions and performance.

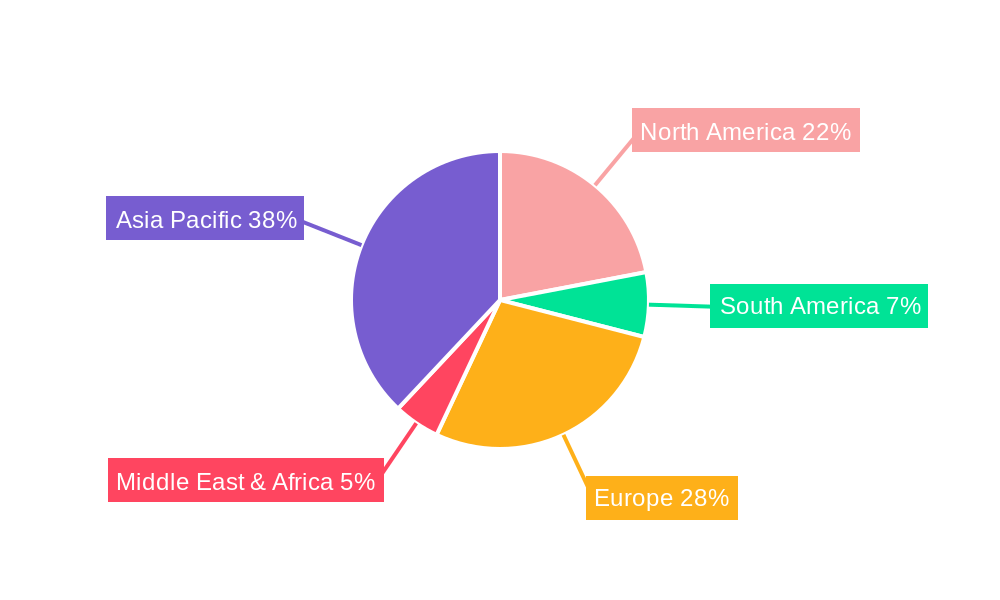

Several key trends are shaping the Gas Concentration Sensor market. The shift towards Zirconia sensors, renowned for their accuracy and durability, is a prominent development, alongside the continued relevance of Titanium Dioxide oxygen sensors in specific applications. Geographically, the Asia Pacific region, particularly China and India, is expected to emerge as a dominant force, driven by rapid industrialization, a burgeoning automotive sector, and supportive government initiatives. Europe and North America, with their established automotive industries and stringent environmental regulations, will remain crucial markets. While the market is experiencing substantial growth, certain restraints, such as the high cost of advanced sensor technology and the complexities associated with integration into existing vehicle architectures, could pose challenges. Nevertheless, ongoing research and development in sensor technology, coupled with strategic collaborations among leading players like Robert Bosch, Continental, and DENSO, are expected to mitigate these restraints and propel the market forward.

Comprehensive Report on the Global Gas Concentration Sensor Market: Dynamics, Trends, and Future Outlook (2019-2033)

This in-depth market research report offers a strategic analysis of the global Gas Concentration Sensor market, encompassing a detailed examination of its dynamics, growth trajectory, competitive landscape, and future opportunities. Covering a study period from 2019 to 2033, with a base year of 2025, this report leverages robust data and expert insights to provide actionable intelligence for industry stakeholders. The report targets professionals in automotive manufacturing, sensor technology, environmental monitoring, and industrial automation, delivering a holistic understanding of this critical market segment.

Gas Concentration Sensor Market Dynamics & Structure

The global Gas Concentration Sensor market exhibits a moderate concentration, with leading players like Robert Bosch, Continental, DENSO, and Infineon Technologies holding significant market shares. Technological innovation is a primary driver, fueled by increasingly stringent emission regulations worldwide and the growing demand for advanced driver-assistance systems (ADAS) and autonomous driving technologies. The regulatory framework, particularly in regions like Europe and North America, mandates stricter emission standards, pushing for the development and adoption of sophisticated gas sensing solutions for both passenger and commercial vehicles.

- Market Concentration: Moderate, with key players investing heavily in R&D.

- Technological Innovation Drivers: Emission regulations, ADAS integration, predictive maintenance.

- Regulatory Frameworks: Euro 7, EPA standards, CAFE standards influencing sensor development.

- Competitive Product Substitutes: Limited for direct emission control, but advancements in alternative sensing technologies pose a long-term threat.

- End-User Demographics: Automotive OEMs, Tier-1 suppliers, industrial automation providers.

- M&A Trends: Strategic acquisitions focused on sensor technology enhancement and market expansion, with an estimated xx M&A deals in the historical period.

Gas Concentration Sensor Growth Trends & Insights

The global Gas Concentration Sensor market is projected to witness substantial growth, driven by escalating demand across diverse applications, particularly within the automotive sector. The market size, estimated to be around \$2,500 million in the base year 2025, is expected to expand at a Compound Annual Growth Rate (CAGR) of approximately 6.8% during the forecast period of 2025–2033. This growth is underpinned by the continuous evolution of internal combustion engines, the burgeoning adoption of hybrid and electric vehicles requiring advanced battery management and thermal control, and the increasing implementation of industrial safety and process control systems. The shift towards cleaner energy sources and more efficient industrial operations further fuels the need for precise and reliable gas monitoring.

The historical period (2019–2024) saw a steady uptake in gas concentration sensors, largely propelled by emission control mandates and the increasing complexity of vehicle powertrains. As automotive manufacturers strive to meet evolving environmental standards, the integration of advanced sensors, including Zirconia and Titanium Dioxide Oxygen Sensors, has become paramount. These sensors are crucial for optimizing fuel combustion, thereby reducing harmful emissions like NOx, CO, and unburned hydrocarbons. Beyond automotive applications, the industrial sector's demand for gas concentration sensors for process optimization, worker safety, and environmental compliance contributes significantly to market expansion. Predictive maintenance in industrial settings, enabled by continuous gas monitoring, is also a growing trend, reducing downtime and operational costs.

Technological disruptions, such as the miniaturization of sensors, enhanced sensitivity, and improved durability, are making gas concentration sensors more accessible and applicable in a wider range of scenarios. The development of smart sensors with integrated processing capabilities allows for real-time data analysis and communication, paving the way for more intelligent control systems. Consumer behavior shifts towards environmentally conscious choices and the demand for safer living and working environments are indirectly influencing the market. Governments worldwide are also playing a crucial role through stricter regulations and incentives for adopting cleaner technologies. The market penetration of advanced gas concentration sensors is expected to deepen as awareness of their benefits in terms of safety, efficiency, and environmental protection grows. Furthermore, the increasing complexity of manufacturing processes and the need for precise environmental monitoring in various industries, from petrochemicals to food and beverage, are creating sustained demand for these sensors.

Dominant Regions, Countries, or Segments in Gas Concentration Sensor

The Passenger Vehicle segment is unequivocally the dominant force driving the growth of the global Gas Concentration Sensor market. This dominance stems from several intertwined factors, including the sheer volume of passenger vehicles produced globally, the stringent regulatory environment governing automotive emissions, and the continuous integration of advanced sensing technologies for enhanced performance and safety. In the base year 2025, the passenger vehicle segment is estimated to account for a market share of approximately 65-70% of the total Gas Concentration Sensor market.

The Asia Pacific region, particularly China, is emerging as a powerhouse for both production and consumption of gas concentration sensors in the passenger vehicle segment. China's vast automotive manufacturing base, coupled with the government's strong push for cleaner vehicles through emission standards like China VI and incentives for new energy vehicles (NEVs), creates a fertile ground for sensor adoption. Furthermore, countries like Japan and South Korea, with their established automotive industries and focus on technological innovation, also contribute significantly to regional dominance.

Europe, with its long-standing commitment to environmental protection and strict emission regulations like Euro 7, continues to be a crucial market. Manufacturers in this region are at the forefront of developing and implementing advanced Zirconia and Titanium Dioxide Oxygen Sensors to meet these challenging standards. North America, driven by evolving EPA standards and the increasing adoption of ADAS, also represents a substantial market for gas concentration sensors in passenger vehicles.

Key drivers fueling the dominance of the passenger vehicle segment include:

- Stringent Emission Regulations: Mandates for reducing CO2, NOx, and particulate matter emissions necessitate the widespread use of advanced oxygen sensors for precise engine control.

- ADAS and Autonomous Driving: The proliferation of ADAS features, such as adaptive cruise control and automatic emergency braking, often relies on integrated sensing systems that can include gas concentration monitoring for exhaust gas recirculation (EGR) control and other engine management functions.

- Fuel Efficiency Initiatives: Optimizing fuel combustion through precise air-fuel ratio control directly translates to improved fuel efficiency, a key consumer demand and regulatory objective.

- Technological Advancements in Sensors: Innovations in Zirconia and Titanium Dioxide Oxygen Sensors, leading to improved accuracy, faster response times, and enhanced durability, make them indispensable for modern passenger vehicles.

- Growing Automotive Production: The overall increase in global passenger vehicle production, especially in emerging economies, directly translates to higher demand for all automotive components, including gas concentration sensors.

The market share of passenger vehicles in the base year 2025 is projected to be around \$1,750 million. The growth potential within this segment remains robust, driven by the ongoing transition towards electrified powertrains, which still require sophisticated thermal management and battery health monitoring systems that can benefit from gas sensing technologies.

Gas Concentration Sensor Product Landscape

The Gas Concentration Sensor product landscape is characterized by continuous innovation aimed at enhancing accuracy, responsiveness, and durability. Key product types include Zirconia Sensors, widely used for oxygen sensing in exhaust systems due to their robustness and high-temperature resistance, and Titanium Dioxide Oxygen Sensors, often employed in specific applications requiring different operating characteristics. Manufacturers are focusing on miniaturization, improved signal processing capabilities, and integration with other electronic control units (ECUs). Applications span from precise stoichiometric control for fuel efficiency and emission reduction in passenger and commercial vehicles to safety monitoring in industrial environments and process optimization in various manufacturing sectors. Unique selling propositions lie in advanced diagnostics, extended lifespan, and compatibility with complex vehicle architectures.

Key Drivers, Barriers & Challenges in Gas Concentration Sensor

Key Drivers:

- Stringent Emission Regulations: Global mandates for reduced vehicular emissions are the primary catalyst.

- Automotive Electrification & Hybridization: Need for advanced thermal management and battery monitoring.

- Industrial Automation & Safety: Growing demand for process control and hazardous gas detection.

- Advancements in Sensor Technology: Miniaturization, increased accuracy, and faster response times.

- ADAS Integration: Demand for comprehensive sensing suites in modern vehicles.

Key Barriers & Challenges:

- High R&D Costs: Development of cutting-edge sensor technology requires substantial investment.

- Supply Chain Volatility: Raw material availability and geopolitical factors can impact production.

- Cost Sensitivity in Certain Segments: Price pressure, particularly in lower-tier automotive markets.

- Standardization Issues: Lack of universal standards can hinder interoperability.

- Emerging Alternative Technologies: Research into non-traditional sensing methods.

Emerging Opportunities in Gas Concentration Sensor

Emerging opportunities in the Gas Concentration Sensor market are abundant, particularly in the development of smart, connected sensors capable of real-time data analytics and predictive diagnostics. The increasing focus on indoor air quality monitoring presents a significant untapped market for domestic and commercial applications. Furthermore, the expansion of industrial IoT (IIoT) is creating demand for robust and reliable gas sensors in smart factories for process optimization and predictive maintenance. The growing interest in hydrogen energy storage and utilization also opens avenues for specialized hydrogen gas sensors. The development of highly sensitive and selective sensors for niche applications, such as food spoilage detection or medical diagnostics, represents another promising area for growth.

Growth Accelerators in the Gas Concentration Sensor Industry

Several catalysts are accelerating the long-term growth of the Gas Concentration Sensor industry. Technological breakthroughs in materials science are leading to the development of more efficient and cost-effective sensor components. Strategic partnerships between sensor manufacturers and automotive OEMs are crucial for co-developing integrated solutions that meet evolving vehicle requirements. Market expansion into developing economies, driven by increasing automotive production and industrialization, will provide significant growth impetus. Furthermore, the ongoing research into novel sensing principles and the refinement of existing technologies to achieve higher sensitivity and selectivity will continue to fuel innovation and demand.

Key Players Shaping the Gas Concentration Sensor Market

- Infineon Technologies

- STMicroelectronics

- Valeo

- Hitachi

- Autoliv

- Mobis

- ZF

- NXP Semiconductors

- Robert Bosch

- Continental

- DENSO

- Analog Devices

- Sensata Technologies

- Delphi

Notable Milestones in Gas Concentration Sensor Sector

- 2019: Launch of advanced Zirconia sensors with extended lifespan and faster response times by Continental.

- 2020: Bosch introduces a new generation of multi-gas sensors for enhanced air quality monitoring.

- 2021: STMicroelectronics announces a new family of compact and low-power gas sensors for consumer electronics.

- 2022: Valeo expands its sensor portfolio to include advanced NOx sensors for heavy-duty vehicles.

- 2023: Infineon Technologies and NXP Semiconductors forge strategic partnerships to develop next-generation automotive sensing solutions.

- 2024 (Projected): Anticipated advancements in solid-state gas sensing technologies with improved selectivity and reduced power consumption.

In-Depth Gas Concentration Sensor Market Outlook

The future outlook for the Gas Concentration Sensor market is exceptionally promising, driven by sustained regulatory pressures and rapid technological advancements. The ongoing electrification of the automotive sector, while transforming powertrains, continues to require sophisticated sensing for thermal management and battery safety, creating new avenues for sensor integration. Industrial automation, IIoT, and the burgeoning smart city initiatives will further amplify the demand for reliable and intelligent gas sensing solutions. Strategic investments in research and development, coupled with collaborative efforts between industry players, will be pivotal in unlocking new applications and enhancing sensor performance, ensuring robust market growth throughout the forecast period.

Gas Concentration Sensor Segmentation

-

1. Application

- 1.1. Passenger Vehicle

- 1.2. Commercial Vehicle

-

2. Types

- 2.1. Zirconia Sensor

- 2.2. Titanium Dioxide Oxygen Sensor

Gas Concentration Sensor Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Gas Concentration Sensor REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Gas Concentration Sensor Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Vehicle

- 5.1.2. Commercial Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Zirconia Sensor

- 5.2.2. Titanium Dioxide Oxygen Sensor

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Gas Concentration Sensor Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Vehicle

- 6.1.2. Commercial Vehicle

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Zirconia Sensor

- 6.2.2. Titanium Dioxide Oxygen Sensor

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Gas Concentration Sensor Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Vehicle

- 7.1.2. Commercial Vehicle

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Zirconia Sensor

- 7.2.2. Titanium Dioxide Oxygen Sensor

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Gas Concentration Sensor Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Vehicle

- 8.1.2. Commercial Vehicle

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Zirconia Sensor

- 8.2.2. Titanium Dioxide Oxygen Sensor

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Gas Concentration Sensor Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Vehicle

- 9.1.2. Commercial Vehicle

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Zirconia Sensor

- 9.2.2. Titanium Dioxide Oxygen Sensor

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Gas Concentration Sensor Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Vehicle

- 10.1.2. Commercial Vehicle

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Zirconia Sensor

- 10.2.2. Titanium Dioxide Oxygen Sensor

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Infineon Technologies

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 STMicroelectronics

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Valeo

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Hitachi

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Autoliv

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Mobis

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 ZF

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 NXP Semiconductors

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Robert Bosch

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Continental

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 DENSO

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Analog Devices

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Sensata Technologies

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Delphi

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.1 Infineon Technologies

List of Figures

- Figure 1: Global Gas Concentration Sensor Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Gas Concentration Sensor Revenue (million), by Application 2024 & 2032

- Figure 3: North America Gas Concentration Sensor Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Gas Concentration Sensor Revenue (million), by Types 2024 & 2032

- Figure 5: North America Gas Concentration Sensor Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Gas Concentration Sensor Revenue (million), by Country 2024 & 2032

- Figure 7: North America Gas Concentration Sensor Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Gas Concentration Sensor Revenue (million), by Application 2024 & 2032

- Figure 9: South America Gas Concentration Sensor Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Gas Concentration Sensor Revenue (million), by Types 2024 & 2032

- Figure 11: South America Gas Concentration Sensor Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Gas Concentration Sensor Revenue (million), by Country 2024 & 2032

- Figure 13: South America Gas Concentration Sensor Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Gas Concentration Sensor Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Gas Concentration Sensor Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Gas Concentration Sensor Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Gas Concentration Sensor Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Gas Concentration Sensor Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Gas Concentration Sensor Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Gas Concentration Sensor Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Gas Concentration Sensor Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Gas Concentration Sensor Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Gas Concentration Sensor Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Gas Concentration Sensor Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Gas Concentration Sensor Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Gas Concentration Sensor Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Gas Concentration Sensor Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Gas Concentration Sensor Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Gas Concentration Sensor Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Gas Concentration Sensor Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Gas Concentration Sensor Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Gas Concentration Sensor Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Gas Concentration Sensor Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Gas Concentration Sensor Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Gas Concentration Sensor Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Gas Concentration Sensor Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Gas Concentration Sensor Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Gas Concentration Sensor Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Gas Concentration Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Gas Concentration Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Gas Concentration Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Gas Concentration Sensor Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Gas Concentration Sensor Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Gas Concentration Sensor Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Gas Concentration Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Gas Concentration Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Gas Concentration Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Gas Concentration Sensor Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Gas Concentration Sensor Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Gas Concentration Sensor Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Gas Concentration Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Gas Concentration Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Gas Concentration Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Gas Concentration Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Gas Concentration Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Gas Concentration Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Gas Concentration Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Gas Concentration Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Gas Concentration Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Gas Concentration Sensor Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Gas Concentration Sensor Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Gas Concentration Sensor Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Gas Concentration Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Gas Concentration Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Gas Concentration Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Gas Concentration Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Gas Concentration Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Gas Concentration Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Gas Concentration Sensor Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Gas Concentration Sensor Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Gas Concentration Sensor Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Gas Concentration Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Gas Concentration Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Gas Concentration Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Gas Concentration Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Gas Concentration Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Gas Concentration Sensor Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Gas Concentration Sensor Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Gas Concentration Sensor?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Gas Concentration Sensor?

Key companies in the market include Infineon Technologies, STMicroelectronics, Valeo, Hitachi, Autoliv, Mobis, ZF, NXP Semiconductors, Robert Bosch, Continental, DENSO, Analog Devices, Sensata Technologies, Delphi.

3. What are the main segments of the Gas Concentration Sensor?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Gas Concentration Sensor," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Gas Concentration Sensor report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Gas Concentration Sensor?

To stay informed about further developments, trends, and reports in the Gas Concentration Sensor, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence