Key Insights

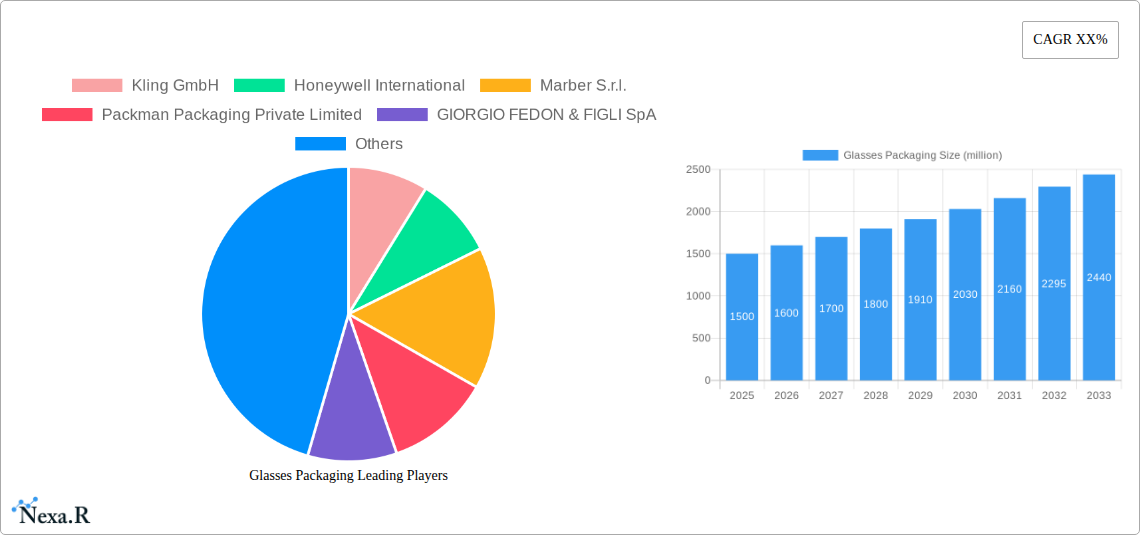

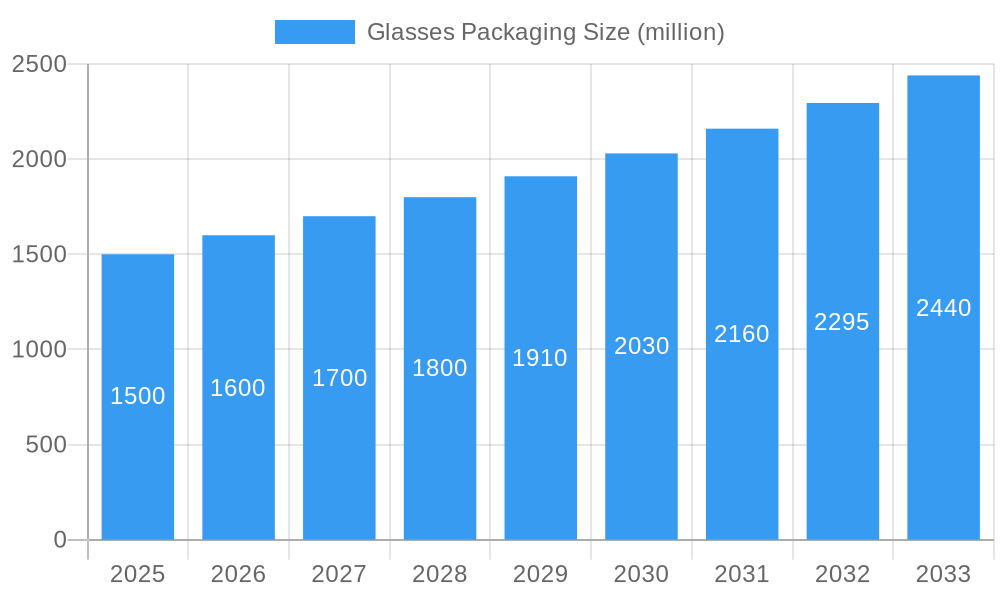

The global glasses packaging market is experiencing robust growth, projected to reach an estimated $1,500 million by 2025, with a Compound Annual Growth Rate (CAGR) of 6.5% anticipated over the forecast period of 2025-2033. This expansion is primarily fueled by the escalating demand for eyewear, driven by a growing global population, increasing awareness of eye health, and the rising prevalence of vision-related issues. Furthermore, the fashion industry's increasing emphasis on eyewear as a style accessory is also contributing significantly to market expansion. The shift towards e-commerce and online sales channels has opened up new avenues for accessibility and consumer reach, while traditional offline retail continues to hold a substantial share, catering to a diverse consumer base.

Glasses Packaging Market Size (In Billion)

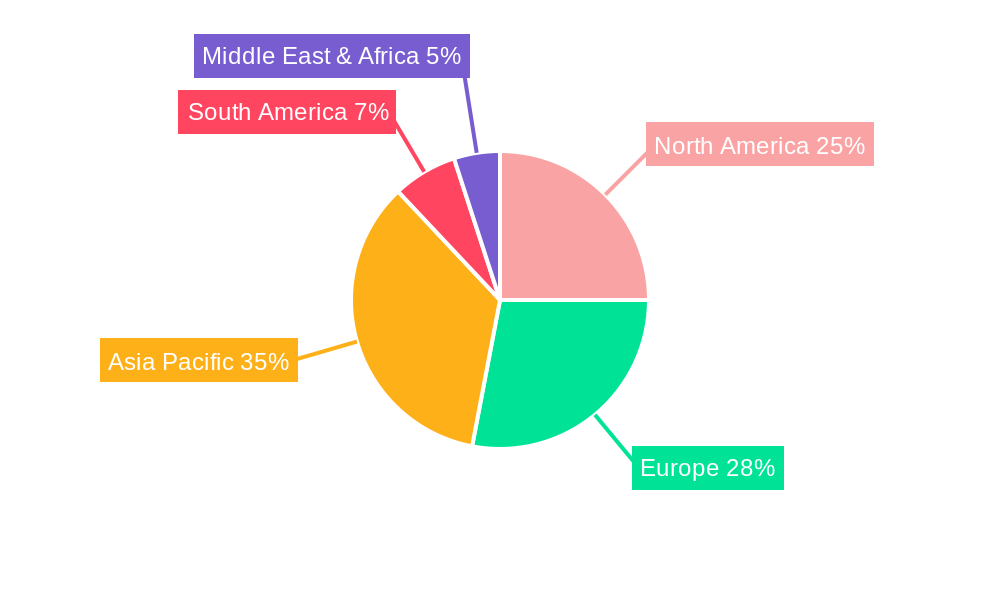

Key growth drivers for the glasses packaging market include technological advancements in packaging materials and designs, offering enhanced protection and aesthetic appeal. The increasing consumer preference for sustainable and eco-friendly packaging solutions is also shaping market trends, pushing manufacturers towards biodegradable and recyclable options. However, challenges such as fluctuating raw material costs and intense competition among key players like Kling GmbH, Honeywell International, and Packman Packaging Private Limited, are expected to restrain market growth to some extent. The market is segmented by application into Online Sales and Offline Sales, and by type into Paper Glasses Packaging, Plastic Glasses Packaging, Leather Glasses Packaging, and Others. Asia Pacific, led by China and India, is anticipated to be a dominant region due to its vast consumer base and burgeoning e-commerce landscape.

Glasses Packaging Company Market Share

Here's a comprehensive, SEO-optimized report description for Glasses Packaging, designed for immediate use and maximum industry appeal.

Glasses Packaging Market Dynamics & Structure

The global glasses packaging market is characterized by a moderate concentration, with key players like Kling GmbH, Honeywell International, Marber S.r.l., Packman Packaging Private Limited, GIORGIO FEDON & FIGLI SpA, Pyramex Safety Products, GATTO ASTUCCI SPA, Rongyu Packing, Umiya Plast, and lsunny holding significant influence. Technological innovation is primarily driven by advancements in sustainable materials and smart packaging solutions, aiming to enhance product protection, brand visibility, and consumer experience. Regulatory frameworks are evolving to mandate eco-friendly packaging options and stringent product safety standards, impacting material choices and manufacturing processes. Competitive product substitutes, such as direct-to-consumer (DTC) models bypassing traditional retail packaging, and the increasing use of generic packaging by online retailers, present ongoing challenges. End-user demographics are shifting, with a growing demand for premium, personalized, and eco-conscious packaging solutions from both online and offline sales channels. Mergers and acquisitions (M&A) are notable trends, with companies consolidating to gain market share, access new technologies, and expand their geographical reach. For instance, the historical period of 2019-2024 witnessed several strategic acquisitions aimed at bolstering product portfolios and distribution networks, reflecting an ongoing consolidation effort. Innovation barriers include the high cost of R&D for novel sustainable materials and the complexity of redesigning existing supply chains to accommodate new packaging formats. The market's structural dynamics are a blend of established corrugated and plastic packaging manufacturers alongside emerging specialists in luxury and eco-friendly solutions.

- Market Concentration: Moderate, with a mix of large multinational corporations and specialized regional players.

- Technological Drivers: Sustainable materials (recycled content, biodegradable options), smart packaging (RFID, QR codes), improved protective features.

- Regulatory Frameworks: Environmental regulations (REACH, packaging waste directives), product safety standards for optical goods.

- Competitive Substitutes: DTC business models, minimalist online packaging, reusable eyewear cases.

- End-User Demographics: Growing demand for sustainable, premium, and customizable packaging across all age groups.

- M&A Trends: Strategic acquisitions to enhance product offerings, expand global presence, and secure raw material supply.

Glasses Packaging Growth Trends & Insights

The global glasses packaging market is poised for robust growth, projected to evolve significantly from its 2019 base year to a projected 2025 estimated year and further into a comprehensive 2033 forecast. This evolution is fueled by a confluence of factors, including the burgeoning e-commerce landscape, rising consumer awareness regarding sustainable practices, and continuous innovation in material science and design. The market size is expected to witness a Compound Annual Growth Rate (CAGR) of approximately 5.5% during the forecast period of 2025–2033. This impressive trajectory is underpinned by an increasing adoption rate of specialized and aesthetically pleasing packaging solutions across both online and offline sales channels. For instance, the surge in online shopping for eyewear necessitates packaging that offers superior protection during transit while also serving as a compelling unboxing experience, thereby enhancing brand loyalty. The penetration of eco-friendly packaging materials, such as recycled paper and biodegradable plastics, is rapidly increasing as manufacturers respond to consumer demand and regulatory pressures. Technological disruptions, including advancements in digital printing for personalized packaging and the integration of smart features like anti-counterfeiting measures, are also playing a pivotal role in shaping market trends. Consumer behavior shifts are clearly evident, with a pronounced preference for brands that demonstrate environmental responsibility and offer a premium unboxing experience. This is particularly true for the Parent Market of general packaging solutions, where the demand for specialized eyewear containment is a significant sub-segment. Within the Child Market for glasses, the increasing prevalence of prescription eyewear, sunglasses, and specialized performance eyewear all contribute to a diversified demand for packaging. The historical period of 2019–2024 laid the groundwork for these trends, with steady growth in e-commerce and a nascent but growing interest in sustainable packaging. As we move into the base year of 2025 and beyond, these trends are expected to accelerate, driving significant market expansion and redefining industry standards. The overall market penetration for specialized glasses packaging is estimated to reach 75% by 2033, up from approximately 60% in 2024.

Dominant Regions, Countries, or Segments in Glasses Packaging

The Online Sales segment is emerging as a dominant force driving growth in the global glasses packaging market. This dominance is propelled by several interconnected factors, including the unparalleled convenience offered to consumers, the vast reach of e-commerce platforms, and the increasing sophistication of logistics and shipping networks. In 2025, Online Sales are projected to account for approximately 65% of the total glasses packaging market value, a significant increase from its share in the historical period of 2019–2024. Key drivers for this segment's supremacy include:

- Global E-commerce Expansion: The continuous growth of online retail, particularly in emerging economies, is creating a vast customer base for eyewear purchases that necessitates reliable and attractive packaging.

- Direct-to-Consumer (DTC) Models: Many eyewear brands are adopting DTC strategies, enabling them to bypass traditional retail channels and connect directly with consumers, thus increasing reliance on robust shipping packaging.

- Technological Advancements in Logistics: Innovations in supply chain management, faster delivery times, and improved tracking systems make online purchasing of glasses a seamless experience, encouraging higher sales volumes.

- Enhanced Unboxing Experience: Brands are increasingly leveraging packaging in the online sales channel to create a memorable unboxing experience, fostering brand loyalty and driving repeat purchases. This is a critical differentiator in a competitive online marketplace.

While Offline Sales will continue to be a significant channel, its growth rate is expected to be slower compared to online sales due to market saturation in some regions and the structural shifts towards digital commerce.

Among the Types of glasses packaging, Plastic Glasses Packaging currently holds a substantial market share, estimated at around 45% in 2025, owing to its durability, cost-effectiveness, and versatility in design. However, the market is witnessing a rapid rise in the adoption of Paper Glasses Packaging, driven by growing environmental concerns and regulatory pushes towards sustainability. Paper packaging is projected to see a CAGR of over 7% during the forecast period, significantly outpacing other types. This growth is fueled by:

- Consumer Demand for Sustainability: A growing segment of consumers actively seeks out products with eco-friendly packaging.

- Regulatory Support for Paper: Many governments are introducing policies that favor or mandate the use of recyclable and biodegradable materials like paper.

- Material Innovation: Advancements in paperboard technology are leading to stronger, more water-resistant, and visually appealing paper packaging solutions.

Leather Glasses Packaging caters to the premium segment, offering a luxurious feel and superior protection, contributing a niche but valuable market share. The "Others" category, which may include innovative composite materials or advanced protective foams, is expected to grow as R&D efforts yield new solutions.

Glasses Packaging Product Landscape

The glasses packaging product landscape is dynamically evolving, driven by a pursuit of enhanced protection, aesthetic appeal, and sustainability. Innovations in Paper Glasses Packaging are a key highlight, with advancements in recycled content, improved structural integrity for better impact resistance, and premium finishes such as matte coatings and embossing. Plastic Glasses Packaging continues to see innovations focused on using recycled plastics (rPET) and developing thinner, more lightweight designs without compromising protection, alongside advancements in tamper-evident seals. Leather Glasses Packaging is increasingly incorporating sustainable leather alternatives and sophisticated closure mechanisms, offering a blend of luxury and ethical sourcing. Performance metrics such as drop resistance, crush strength, and UV protection are continually being optimized. Unique selling propositions are emerging from integrated features like cleaning cloths, anti-fog solutions, and digital authentication tags for authenticity.

Key Drivers, Barriers & Challenges in Glasses Packaging

Key Drivers:

- Surging E-commerce Growth: The exponential rise in online eyewear sales necessitates secure and appealing packaging for shipping, directly boosting demand.

- Sustainability Imperative: Increasing consumer and regulatory pressure for eco-friendly packaging solutions, favoring recycled, biodegradable, and recyclable materials.

- Brand Differentiation: Packaging is a crucial touchpoint for brand experience, driving demand for innovative and aesthetically pleasing designs that enhance unboxing.

- Technological Advancements: Innovations in material science and printing technologies enable more protective, customizable, and cost-effective packaging solutions.

Barriers & Challenges:

- Supply Chain Volatility: Fluctuations in raw material prices (e.g., paper pulp, virgin plastics) and availability can impact production costs and lead times.

- Cost of Sustainable Materials: While demand is high, the initial cost of sourcing and implementing certain sustainable packaging materials can be prohibitive for some manufacturers.

- Regulatory Compliance Complexity: Navigating diverse and evolving packaging regulations across different regions can be challenging and costly.

- Competition from Reusable Packaging: The growing popularity of reusable eyewear cases, especially within the prescription eyewear segment, poses a potential challenge to single-use packaging.

- Logistical Constraints for Oversized/Fragile Items: Ensuring adequate protection for larger or exceptionally fragile eyewear, such as performance goggles or specialized medical devices, presents unique packaging design hurdles.

Emerging Opportunities in Glasses Packaging

Emerging opportunities in glasses packaging lie in the development of "smart" packaging solutions that offer enhanced functionality beyond mere containment. This includes integrating near-field communication (NFC) chips or QR codes for product authentication, providing detailed product information, or facilitating direct customer engagement. The burgeoning market for sustainable and biodegradable packaging materials presents a significant growth avenue, with potential for innovation in novel plant-based or compostable alternatives. Furthermore, the increasing demand for personalized and limited-edition eyewear creates opportunities for bespoke, high-end packaging that caters to specific consumer segments. Untapped markets in developing economies, where e-commerce adoption is rapidly increasing, also offer substantial growth potential for cost-effective yet protective packaging solutions.

Growth Accelerators in the Glasses Packaging Industry

Long-term growth in the glasses packaging industry will be significantly accelerated by continued technological breakthroughs in material science, particularly in the development of advanced biodegradable and compostable polymers and advanced paper composites. Strategic partnerships between packaging manufacturers, eyewear brands, and technology providers will foster the creation of integrated solutions, such as smart packaging with embedded tracking or authentication features. Market expansion strategies targeting emerging economies, where the middle class and disposable income are rising, will also act as a key accelerator. Furthermore, proactive adoption of circular economy principles, focusing on closed-loop recycling systems for packaging materials, will enhance brand reputation and drive consumer loyalty, creating a sustainable growth engine.

Key Players Shaping the Glasses Packaging Market

- Kling GmbH

- Honeywell International

- Marber S.r.l.

- Packman Packaging Private Limited

- GIORGIO FEDON & FIGLI SpA

- Pyramex Safety Products

- GATTO ASTUCCI SPA

- Rongyu Packing

- Umiya Plast

- lsunny

Notable Milestones in Glasses Packaging Sector

- 2020: Increased focus on sustainable materials in response to heightened environmental awareness and preliminary regulatory shifts.

- 2021: Significant growth in custom-designed packaging for direct-to-consumer eyewear brands, driven by e-commerce expansion.

- 2022: Introduction of advanced protective cushioning materials derived from recycled plastics.

- 2023: Rise in "unboxing experience" packaging, incorporating unique textures, colors, and interior designs.

- 2024: Further integration of QR codes on packaging for enhanced product information and authentication.

In-Depth Glasses Packaging Market Outlook

The future outlook for the glasses packaging market is exceptionally positive, characterized by sustained growth and transformative innovation. The primary growth accelerators will be the continuous expansion of online sales channels, the unyielding demand for sustainable packaging solutions, and the increasing sophistication of packaging design as a brand differentiator. Strategic investments in research and development for novel biodegradable materials and the implementation of smart packaging technologies will create significant competitive advantages. Furthermore, a growing emphasis on circular economy principles and the development of robust recycling infrastructures will not only drive market expansion but also foster long-term industry resilience and environmental responsibility, ensuring a robust and evolving market landscape through 2033.

Glasses Packaging Segmentation

-

1. Application

- 1.1. Online Sales

- 1.2. Offline Sales

-

2. Types

- 2.1. Paper Glasses Packaging

- 2.2. Plastic Glasses Packaging

- 2.3. Leather Glasses Packaging

- 2.4. Others

Glasses Packaging Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Glasses Packaging Regional Market Share

Geographic Coverage of Glasses Packaging

Glasses Packaging REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Glasses Packaging Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Online Sales

- 5.1.2. Offline Sales

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Paper Glasses Packaging

- 5.2.2. Plastic Glasses Packaging

- 5.2.3. Leather Glasses Packaging

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Glasses Packaging Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Online Sales

- 6.1.2. Offline Sales

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Paper Glasses Packaging

- 6.2.2. Plastic Glasses Packaging

- 6.2.3. Leather Glasses Packaging

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Glasses Packaging Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Online Sales

- 7.1.2. Offline Sales

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Paper Glasses Packaging

- 7.2.2. Plastic Glasses Packaging

- 7.2.3. Leather Glasses Packaging

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Glasses Packaging Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Online Sales

- 8.1.2. Offline Sales

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Paper Glasses Packaging

- 8.2.2. Plastic Glasses Packaging

- 8.2.3. Leather Glasses Packaging

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Glasses Packaging Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Online Sales

- 9.1.2. Offline Sales

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Paper Glasses Packaging

- 9.2.2. Plastic Glasses Packaging

- 9.2.3. Leather Glasses Packaging

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Glasses Packaging Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Online Sales

- 10.1.2. Offline Sales

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Paper Glasses Packaging

- 10.2.2. Plastic Glasses Packaging

- 10.2.3. Leather Glasses Packaging

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Kling GmbH

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Honeywell International

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Marber S.r.l.

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Packman Packaging Private Limited

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 GIORGIO FEDON & FIGLI SpA

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Pyramex Safety Products

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 GATTO ASTUCCI SPA

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Rongyu Packing

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Umiya Plast

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 lsunny

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Kling GmbH

List of Figures

- Figure 1: Global Glasses Packaging Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Glasses Packaging Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Glasses Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Glasses Packaging Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Glasses Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Glasses Packaging Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Glasses Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Glasses Packaging Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Glasses Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Glasses Packaging Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Glasses Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Glasses Packaging Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Glasses Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Glasses Packaging Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Glasses Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Glasses Packaging Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Glasses Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Glasses Packaging Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Glasses Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Glasses Packaging Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Glasses Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Glasses Packaging Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Glasses Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Glasses Packaging Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Glasses Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Glasses Packaging Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Glasses Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Glasses Packaging Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Glasses Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Glasses Packaging Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Glasses Packaging Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Glasses Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Glasses Packaging Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Glasses Packaging Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Glasses Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Glasses Packaging Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Glasses Packaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Glasses Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Glasses Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Glasses Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Glasses Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Glasses Packaging Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Glasses Packaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Glasses Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Glasses Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Glasses Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Glasses Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Glasses Packaging Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Glasses Packaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Glasses Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Glasses Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Glasses Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Glasses Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Glasses Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Glasses Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Glasses Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Glasses Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Glasses Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Glasses Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Glasses Packaging Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Glasses Packaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Glasses Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Glasses Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Glasses Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Glasses Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Glasses Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Glasses Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Glasses Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Glasses Packaging Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Glasses Packaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Glasses Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Glasses Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Glasses Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Glasses Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Glasses Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Glasses Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Glasses Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Glasses Packaging?

The projected CAGR is approximately 4%.

2. Which companies are prominent players in the Glasses Packaging?

Key companies in the market include Kling GmbH, Honeywell International, Marber S.r.l., Packman Packaging Private Limited, GIORGIO FEDON & FIGLI SpA, Pyramex Safety Products, GATTO ASTUCCI SPA, Rongyu Packing, Umiya Plast, lsunny.

3. What are the main segments of the Glasses Packaging?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5600.00, USD 8400.00, and USD 11200.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Glasses Packaging," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Glasses Packaging report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Glasses Packaging?

To stay informed about further developments, trends, and reports in the Glasses Packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence