Key Insights

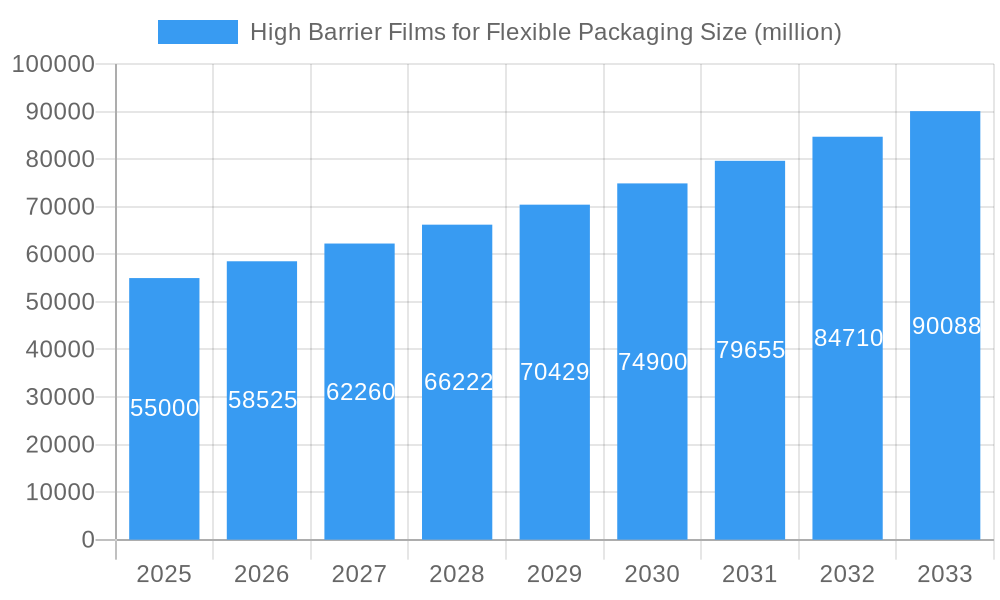

The global High Barrier Films for Flexible Packaging market is poised for robust expansion, projected to reach approximately USD 55,000 million by 2025, with a compelling Compound Annual Growth Rate (CAGR) of around 6.5% through 2033. This growth is primarily propelled by the escalating demand for extended shelf-life, enhanced product protection, and improved food safety across the Food & Beverage sector, which represents a significant application segment. The Pharmaceutical & Medical industry also contributes substantially, driven by the stringent packaging requirements for sensitive drugs and medical devices. Technological advancements in film manufacturing, leading to superior barrier properties against oxygen, moisture, and UV radiation, coupled with the growing consumer preference for lightweight and sustainable packaging solutions, further fuel market momentum.

High Barrier Films for Flexible Packaging Market Size (In Billion)

The market's trajectory is further influenced by evolving consumer lifestyles and the increasing adoption of convenience foods and ready-to-eat meals, necessitating advanced packaging to maintain freshness and quality. Key trends include the rising prominence of bio-based and recyclable high barrier films like PLA, responding to stringent environmental regulations and a growing eco-conscious consumer base. While the adoption of PET, CPP, and BOPP films continues, the innovation in materials like PVA and other advanced polymers is reshaping the competitive landscape. Restraints, such as the higher cost associated with certain high-barrier materials and the complexity of recycling multilayered structures, are being addressed through ongoing research and development efforts focused on cost-effectiveness and circular economy principles, indicating a dynamic and evolving market.

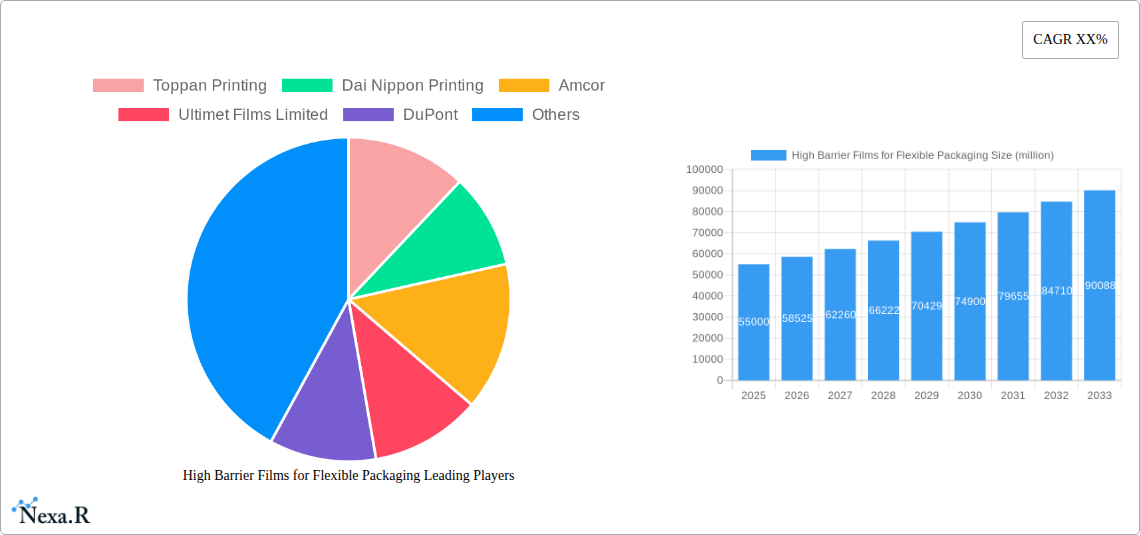

High Barrier Films for Flexible Packaging Company Market Share

Here's a comprehensive, SEO-optimized report description for "High Barrier Films for Flexible Packaging," designed for immediate use without modification.

High Barrier Films for Flexible Packaging Market Dynamics & Structure

The global high barrier films for flexible packaging market is characterized by a dynamic interplay of technological advancements, stringent regulatory landscapes, and evolving consumer demands. Market concentration varies across geographies, with leading players like Toppan Printing, Dai Nippon Printing, and Amcor holding significant shares, particularly in established regions. Technological innovation remains a primary driver, fueled by the continuous pursuit of enhanced shelf-life, product protection, and sustainability in packaging solutions. Key innovation drivers include the development of advanced material science, such as novel polymer formulations and co-extrusion techniques, enabling films with superior oxygen, moisture, and light barrier properties. Regulatory frameworks, particularly concerning food safety and environmental impact, also shape market dynamics, pushing manufacturers towards compliant and sustainable materials. Competitive product substitutes, including rigid packaging and alternative barrier technologies, pose a constant challenge, necessitating continuous product differentiation and performance improvements. End-user demographics are increasingly influenced by a growing awareness of health, wellness, and environmental concerns, driving demand for packaging that preserves product integrity and minimizes waste. Mergers and acquisitions (M&A) are a notable trend, with companies like Berry Plastics and Taghleef Industries actively consolidating their market positions and expanding their technological capabilities. The overarching trend is towards high-performance, eco-friendly barrier films catering to diverse end-use industries.

- Market Concentration: Moderately concentrated with a few key global players.

- Technological Innovation: Driven by material science advancements for enhanced barrier properties and sustainability.

- Regulatory Impact: Stringent food safety and environmental regulations are key influencers.

- Competitive Landscape: Faces competition from rigid packaging and other barrier solutions.

- End-User Demographics: Increasing demand for safety, shelf-life extension, and eco-consciousness.

- M&A Activity: Strategic consolidations and acquisitions to enhance market reach and technology portfolios.

High Barrier Films for Flexible Packaging Growth Trends & Insights

The high barrier films for flexible packaging market is poised for robust expansion, driven by an escalating demand for extended shelf-life, product preservation, and sustainable packaging alternatives across a multitude of industries. The market size is projected to witness a substantial Compound Annual Growth Rate (CAGR) of approximately 7.5% from 2025 to 2033, indicating a strong upward trajectory. This growth is underpinned by shifting consumer preferences towards convenience and health-conscious food options, which necessitate advanced packaging to maintain freshness and prevent spoilage. The Food & Beverage segment, accounting for over 60% of the market share, is a primary growth engine, with increasing adoption of high barrier films for products like snacks, dairy, processed meats, and beverages. Pharmaceutical and medical applications are also contributing significantly, driven by the critical need for sterile, safe, and precisely preserved medications and medical devices. The adoption rates of advanced barrier technologies are accelerating as manufacturers recognize their role in reducing food waste and extending product viability, a critical factor in both economic and environmental sustainability. Technological disruptions, such as the development of novel nano-composite barrier materials and advanced coating technologies, are further enhancing performance metrics like oxygen and moisture transmission rates, offering superior protection compared to traditional packaging. Consumer behavior is increasingly influenced by the perceived quality and safety of packaged goods, with a growing willingness to opt for products that demonstrate superior packaging integrity. The rise of e-commerce and the accompanying logistical demands also necessitate robust packaging solutions that can withstand transit, further bolstering the demand for high barrier films. The market penetration of these advanced films is expected to rise, particularly in emerging economies where urbanization and rising disposable incomes are leading to increased consumption of packaged goods. This comprehensive market analysis, powered by our proprietary XXX insights, provides a detailed roadmap of the evolving landscape and future opportunities.

Dominant Regions, Countries, or Segments in High Barrier Films for Flexible Packaging

The Food & Beverage application segment stands as the undisputed leader in the high barrier films for flexible packaging market, consistently driving growth and innovation. This dominance is intrinsically linked to the universal demand for safe, fresh, and long-lasting food products. The sheer volume of food and beverage items consumed globally, coupled with an increasing consumer preference for convenience and extended shelf-life, makes this segment the largest and most dynamic. Within this segment, processed foods, dairy products, snacks, and ready-to-eat meals are key beneficiaries of high barrier packaging. The PET (Polyethylene Terephthalate) type of high barrier film holds a significant market share within the broader film category due to its excellent clarity, mechanical strength, and good barrier properties, making it a preferred choice for many food and beverage applications.

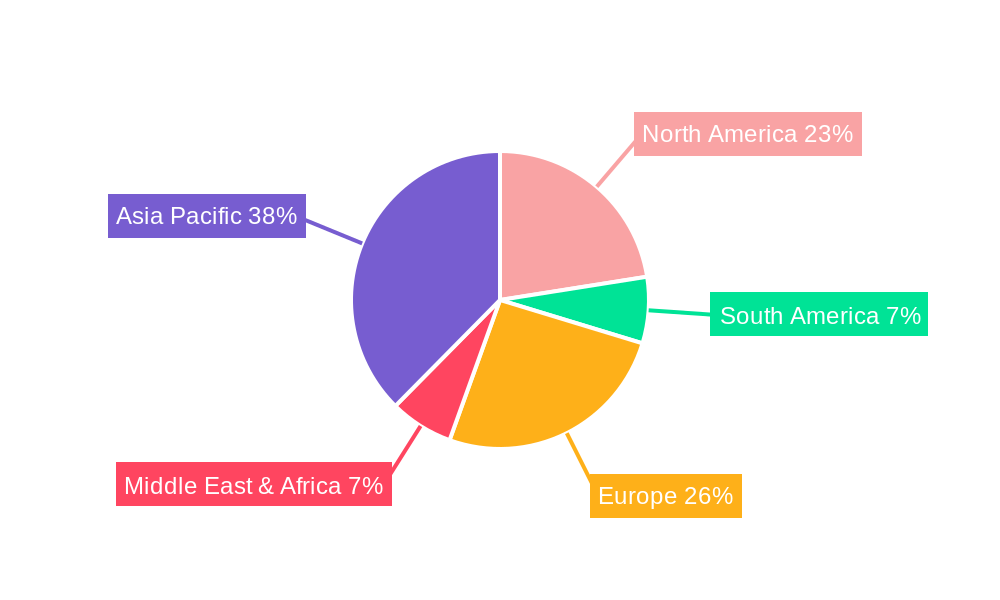

Geographically, Asia Pacific is emerging as a dominant region, fueled by rapid economic development, a burgeoning middle class, and a growing packaged food industry. Countries like China and India, with their massive populations and increasing urbanization, represent vast markets for high barrier packaging solutions. Government initiatives promoting food processing and manufacturing, along with advancements in packaging technology adoption, further solidify Asia Pacific's leading position.

- Application Dominance: Food & Beverage segment leads due to demand for shelf-life extension and product preservation.

- Key sub-segments include processed foods, dairy, snacks, and beverages.

- Market share estimated to be over 60% within the overall high barrier films market.

- Material Dominance: PET films are a leading choice due to their versatile properties.

- PET offers excellent clarity, strength, and good barrier performance for food applications.

- Regional Dominance: Asia Pacific leads market growth due to economic expansion and a booming packaged food industry.

- Key drivers include rising disposable incomes, urbanization, and government support for food processing.

- China and India are pivotal markets within the region.

- Country-Specific Drivers: Increasing consumer awareness about food safety and quality in emerging economies.

- Growth Potential: Continued expansion of the processed food market and adoption of modern packaging technologies.

High Barrier Films for Flexible Packaging Product Landscape

The high barrier films for flexible packaging market is defined by a continuous stream of product innovations aimed at enhancing performance, sustainability, and versatility. Manufacturers are developing films with superior oxygen, moisture, and aroma barrier properties, extending product shelf-life and reducing spoilage in applications ranging from gourmet foods to sensitive pharmaceuticals. Key innovations include multi-layer co-extruded films, advanced coatings, and the incorporation of novel materials like nano-composites and high-barrier polymers such as PVDC (Polyvinylidene Chloride) alternatives and advanced PE (Polyethylene) grades. The introduction of metallized films and AlOx (Aluminum Oxide) coatings offers exceptional barrier performance, while bio-based and recyclable barrier films are gaining traction, addressing growing environmental concerns. Unique selling propositions often lie in achieving a balance between high barrier performance, processability, and end-of-life recyclability.

Key Drivers, Barriers & Challenges in High Barrier Films for Flexible Packaging

The high barrier films for flexible packaging market is propelled by several key drivers. Technological advancements in material science, leading to films with superior barrier properties and enhanced shelf-life for packaged goods, are a primary catalyst. The increasing global demand for food security and reduced food waste necessitates effective preservation solutions. Furthermore, stringent regulations regarding product safety and hygiene in the food, beverage, and pharmaceutical sectors mandate the use of high-performance packaging. The growing consumer preference for convenient, ready-to-eat meals and the expansion of e-commerce logistics also contribute to the demand for robust and protective packaging.

However, the market faces significant barriers and challenges. The high cost associated with advanced barrier films, compared to conventional packaging materials, can hinder adoption, especially in price-sensitive markets. The complexity of manufacturing multi-layer barrier films and the need for specialized equipment can also be a restraint. Environmental concerns regarding the recyclability of multi-material barrier films, despite ongoing innovation, remain a challenge. Supply chain disruptions, raw material price volatility, and intense competition among manufacturers add further complexity. Regulatory hurdles related to food contact materials and the evolving landscape of sustainable packaging mandates can also pose challenges for market players.

Emerging Opportunities in High Barrier Films for Flexible Packaging

Emerging opportunities in the high barrier films for flexible packaging sector are multifaceted, driven by evolving consumer demands and technological advancements. The increasing consumer awareness and regulatory push towards sustainable packaging present a significant opportunity for the development and adoption of recyclable or compostable high barrier films. Innovations in bio-based polymers and mono-material solutions are key to unlocking this potential. Furthermore, the growing demand for personalized and functional packaging in the pharmaceutical and nutraceutical industries, requiring precise barrier properties for specific active ingredients, offers a niche growth avenue. The expansion of the ready-to-eat meal market and premium food segments in emerging economies also creates a robust demand for packaging that maintains freshness and visual appeal.

Growth Accelerators in the High Barrier Films for Flexible Packaging Industry

Several factors are accelerating long-term growth in the high barrier films for flexible packaging industry. Ongoing research and development into novel barrier materials and nanotechnology are continuously pushing the performance envelope, offering enhanced protection against oxygen, moisture, and UV light. Strategic partnerships between film manufacturers, brand owners, and converters are crucial for co-developing tailored solutions and driving market adoption. The increasing focus on reducing food waste globally is a powerful market accelerator, as high barrier films play a critical role in extending the shelf-life of perishable goods. Moreover, the development of advanced recycling technologies and the growing adoption of circular economy principles are creating opportunities for more sustainable barrier film solutions, which will further fuel market expansion.

Key Players Shaping the High Barrier Films for Flexible Packaging Market

- Toppan Printing

- Dai Nippon Printing

- Amcor

- Ultimet Films Limited

- DuPont

- Toray Advanced Film

- Mitsubishi PLASTICS

- Toyobo

- Schur Flexibles Group

- Sealed Air

- Mondi

- Wipak

- 3M

- QIKE

- Berry Plastics

- Taghleef Industries

- Fraunhofer POLO

- Sunrise

- JBF RAK

- Konica Minolta

- FUJIFILM

- Biofilm

Notable Milestones in High Barrier Films for Flexible Packaging Sector

- 2019: Launch of novel bio-based barrier films with enhanced recyclability.

- 2020: Significant investment in AlOx coating technology by major players to improve barrier performance.

- 2021: Introduction of advanced mono-material barrier solutions to meet growing sustainability demands.

- 2022: Increased M&A activity focused on acquiring companies with specialized barrier film technologies.

- 2023: Development of ultra-thin, high-performance barrier films for reduced material usage.

- 2024: Growing emphasis on antimicrobial barrier films for enhanced product safety.

In-Depth High Barrier Films for Flexible Packaging Market Outlook

The future of the high barrier films for flexible packaging market is exceptionally promising, with sustained growth anticipated to be driven by a confluence of technological innovation, increasing global demand for preserved goods, and a strong imperative for sustainable packaging solutions. Growth accelerators include the continuous evolution of advanced materials, such as nano-structured coatings and novel polymers, which will offer unprecedented levels of protection and functionality. Strategic collaborations between industry stakeholders will be pivotal in bringing these innovations to market and tailoring them to specific end-use applications. The ongoing global effort to combat food waste will further underscore the critical role of high barrier films in extending product shelf-life and ensuring food security. As the industry increasingly embraces circular economy principles, the development and widespread adoption of recyclable and bio-based high barrier films will represent a significant avenue for market expansion and differentiation.

High Barrier Films for Flexible Packaging Segmentation

-

1. Application

- 1.1. Food & Beverage

- 1.2. Pharmaceutical & Medical

- 1.3. Electron

- 1.4. Others

-

2. Types

- 2.1. PET

- 2.2. CPP

- 2.3. BOPP

- 2.4. PVA

- 2.5. PLA

- 2.6. Others

High Barrier Films for Flexible Packaging Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

High Barrier Films for Flexible Packaging Regional Market Share

Geographic Coverage of High Barrier Films for Flexible Packaging

High Barrier Films for Flexible Packaging REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global High Barrier Films for Flexible Packaging Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Food & Beverage

- 5.1.2. Pharmaceutical & Medical

- 5.1.3. Electron

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. PET

- 5.2.2. CPP

- 5.2.3. BOPP

- 5.2.4. PVA

- 5.2.5. PLA

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America High Barrier Films for Flexible Packaging Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Food & Beverage

- 6.1.2. Pharmaceutical & Medical

- 6.1.3. Electron

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. PET

- 6.2.2. CPP

- 6.2.3. BOPP

- 6.2.4. PVA

- 6.2.5. PLA

- 6.2.6. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America High Barrier Films for Flexible Packaging Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Food & Beverage

- 7.1.2. Pharmaceutical & Medical

- 7.1.3. Electron

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. PET

- 7.2.2. CPP

- 7.2.3. BOPP

- 7.2.4. PVA

- 7.2.5. PLA

- 7.2.6. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe High Barrier Films for Flexible Packaging Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Food & Beverage

- 8.1.2. Pharmaceutical & Medical

- 8.1.3. Electron

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. PET

- 8.2.2. CPP

- 8.2.3. BOPP

- 8.2.4. PVA

- 8.2.5. PLA

- 8.2.6. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa High Barrier Films for Flexible Packaging Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Food & Beverage

- 9.1.2. Pharmaceutical & Medical

- 9.1.3. Electron

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. PET

- 9.2.2. CPP

- 9.2.3. BOPP

- 9.2.4. PVA

- 9.2.5. PLA

- 9.2.6. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific High Barrier Films for Flexible Packaging Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Food & Beverage

- 10.1.2. Pharmaceutical & Medical

- 10.1.3. Electron

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. PET

- 10.2.2. CPP

- 10.2.3. BOPP

- 10.2.4. PVA

- 10.2.5. PLA

- 10.2.6. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Toppan Printing

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Dai Nippon Printing

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Amcor

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Ultimet Films Limited

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 DuPont

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Toray Advanced Film

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Mitsubishi PLASTICS

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Toyobo

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Schur Flexibles Group

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Sealed Air

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Mondi

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Wipak

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 3M

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 QIKE

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Berry Plastics

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Taghleef Industries

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Fraunhofer POLO

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Sunrise

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 JBF RAK

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Konica Minolta

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 FUJIFILM

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 Biofilm

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.1 Toppan Printing

List of Figures

- Figure 1: Global High Barrier Films for Flexible Packaging Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America High Barrier Films for Flexible Packaging Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America High Barrier Films for Flexible Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America High Barrier Films for Flexible Packaging Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America High Barrier Films for Flexible Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America High Barrier Films for Flexible Packaging Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America High Barrier Films for Flexible Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America High Barrier Films for Flexible Packaging Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America High Barrier Films for Flexible Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America High Barrier Films for Flexible Packaging Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America High Barrier Films for Flexible Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America High Barrier Films for Flexible Packaging Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America High Barrier Films for Flexible Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe High Barrier Films for Flexible Packaging Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe High Barrier Films for Flexible Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe High Barrier Films for Flexible Packaging Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe High Barrier Films for Flexible Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe High Barrier Films for Flexible Packaging Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe High Barrier Films for Flexible Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa High Barrier Films for Flexible Packaging Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa High Barrier Films for Flexible Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa High Barrier Films for Flexible Packaging Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa High Barrier Films for Flexible Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa High Barrier Films for Flexible Packaging Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa High Barrier Films for Flexible Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific High Barrier Films for Flexible Packaging Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific High Barrier Films for Flexible Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific High Barrier Films for Flexible Packaging Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific High Barrier Films for Flexible Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific High Barrier Films for Flexible Packaging Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific High Barrier Films for Flexible Packaging Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global High Barrier Films for Flexible Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global High Barrier Films for Flexible Packaging Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global High Barrier Films for Flexible Packaging Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global High Barrier Films for Flexible Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global High Barrier Films for Flexible Packaging Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global High Barrier Films for Flexible Packaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States High Barrier Films for Flexible Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada High Barrier Films for Flexible Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico High Barrier Films for Flexible Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global High Barrier Films for Flexible Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global High Barrier Films for Flexible Packaging Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global High Barrier Films for Flexible Packaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil High Barrier Films for Flexible Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina High Barrier Films for Flexible Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America High Barrier Films for Flexible Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global High Barrier Films for Flexible Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global High Barrier Films for Flexible Packaging Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global High Barrier Films for Flexible Packaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom High Barrier Films for Flexible Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany High Barrier Films for Flexible Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France High Barrier Films for Flexible Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy High Barrier Films for Flexible Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain High Barrier Films for Flexible Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia High Barrier Films for Flexible Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux High Barrier Films for Flexible Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics High Barrier Films for Flexible Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe High Barrier Films for Flexible Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global High Barrier Films for Flexible Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global High Barrier Films for Flexible Packaging Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global High Barrier Films for Flexible Packaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey High Barrier Films for Flexible Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel High Barrier Films for Flexible Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC High Barrier Films for Flexible Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa High Barrier Films for Flexible Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa High Barrier Films for Flexible Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa High Barrier Films for Flexible Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global High Barrier Films for Flexible Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global High Barrier Films for Flexible Packaging Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global High Barrier Films for Flexible Packaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China High Barrier Films for Flexible Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India High Barrier Films for Flexible Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan High Barrier Films for Flexible Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea High Barrier Films for Flexible Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN High Barrier Films for Flexible Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania High Barrier Films for Flexible Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific High Barrier Films for Flexible Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the High Barrier Films for Flexible Packaging?

The projected CAGR is approximately 6.2%.

2. Which companies are prominent players in the High Barrier Films for Flexible Packaging?

Key companies in the market include Toppan Printing, Dai Nippon Printing, Amcor, Ultimet Films Limited, DuPont, Toray Advanced Film, Mitsubishi PLASTICS, Toyobo, Schur Flexibles Group, Sealed Air, Mondi, Wipak, 3M, QIKE, Berry Plastics, Taghleef Industries, Fraunhofer POLO, Sunrise, JBF RAK, Konica Minolta, FUJIFILM, Biofilm.

3. What are the main segments of the High Barrier Films for Flexible Packaging?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "High Barrier Films for Flexible Packaging," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the High Barrier Films for Flexible Packaging report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the High Barrier Films for Flexible Packaging?

To stay informed about further developments, trends, and reports in the High Barrier Films for Flexible Packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence