Key Insights

The Ovenable Food Packaging market is projected for significant expansion, anticipated to reach $427.4 billion by 2025, driven by a Compound Annual Growth Rate (CAGR) of 5.7%. This growth is fueled by evolving consumer lifestyles, increasing demand for convenient meal solutions, and advancements in dual-ovenable packaging technologies. The emphasis on quick meal preparation and reduced cleanup is a primary driver. Material science innovations are enhancing packaging's ability to withstand high temperatures, maintain food integrity, and improve the cooking experience, broadening its application scope. Heightened focus on food safety and extended shelf life further bolsters demand for specialized ovenable packaging.

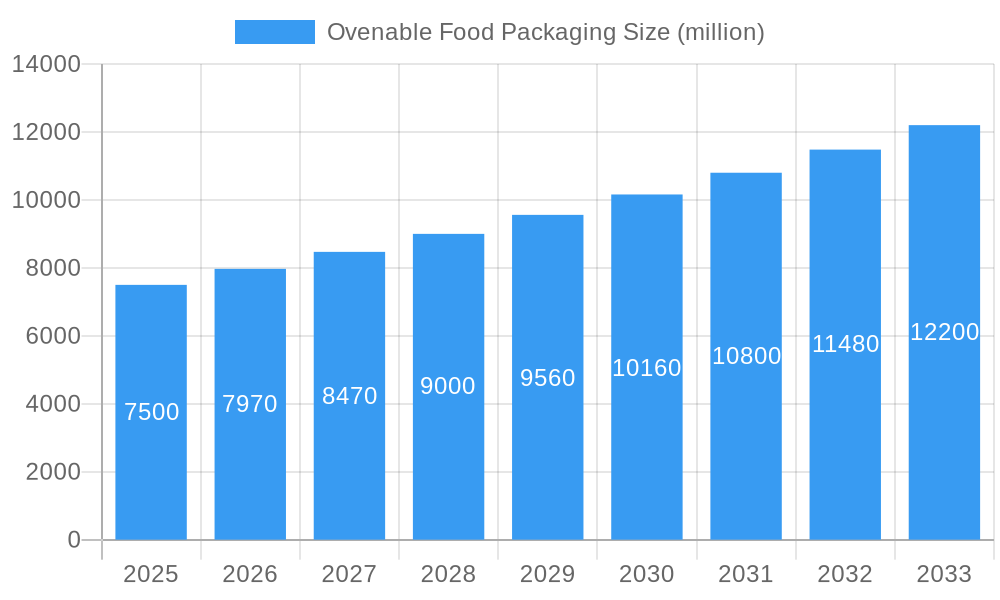

Ovenable Food Packaging Market Size (In Billion)

Market segmentation highlights 'Meat' as a leading application due to widespread consumption and the popularity of ready-to-cook meat products. While 'Bread' is also a significant segment, the 'Others' category, encompassing prepared meals and ethnic cuisines, is expected to experience substantial growth, reflecting diversified convenient food offerings. 'Plastics' currently dominate material types due to their versatility, cost-effectiveness, and barrier properties. However, 'Paper'-based ovenable packaging is gaining traction, driven by environmental consciousness and regulatory favor for sustainable alternatives. Key industry players are actively investing in R&D to innovate and capture market share with advanced, eco-friendly, and high-performance solutions.

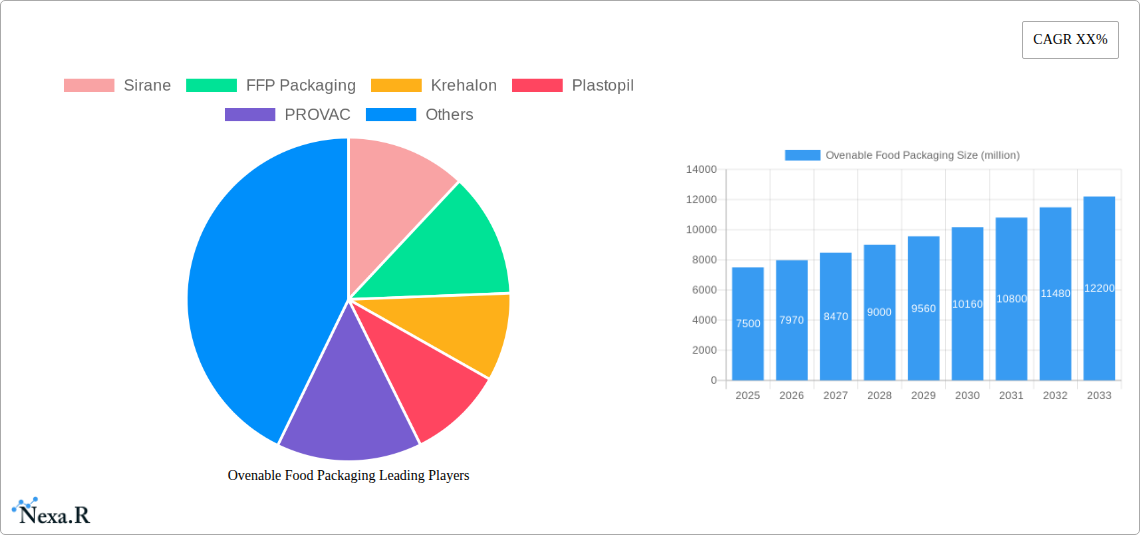

Ovenable Food Packaging Company Market Share

This comprehensive report, "Ovenable Food Packaging Market: Global Outlook, Growth Trends, and Forecast," delivers an in-depth analysis of the dynamic ovenable food packaging industry. Covering a study period from 2019 to 2033, with a base year of 2025, this report provides critical insights into market size, segmentation, regional dominance, key players, and future trajectory. We leverage extensive data to present a clear roadmap for industry professionals seeking to capitalize on the growing demand for convenient and high-performance food packaging solutions.

Ovenable Food Packaging Market Dynamics & Structure

The ovenable food packaging market exhibits a moderately consolidated structure, with key players investing heavily in technological innovation to gain a competitive edge. Drivers of innovation are primarily fueled by the escalating consumer demand for convenience, the desire for ready-to-heat meal solutions, and advancements in material science that enable packaging to withstand high oven temperatures without compromising food quality or safety. Regulatory frameworks, particularly those related to food contact materials and sustainability, are shaping product development and market entry strategies. Competitive product substitutes, such as conventional plastic trays and disposable aluminum foil containers, are present, but ovenable packaging offers distinct advantages in terms of aesthetic appeal and direct-to-oven functionality. End-user demographics are increasingly favoring younger, busy households and individuals seeking time-saving meal preparation options. Mergers and acquisitions (M&A) activity in the sector is driven by the pursuit of expanded product portfolios, geographical reach, and enhanced manufacturing capabilities. For instance, a notable M&A deal volume of 22 deals in the last five years indicates a trend towards consolidation. Innovation barriers include the high cost of research and development for novel materials and the stringent testing required to meet food safety standards, often estimated at $1.5 million to $3 million per new material development.

- Market Concentration: Moderate, with key players holding significant market share.

- Technological Innovation Drivers: Convenience, ready-to-heat meals, advanced materials.

- Regulatory Frameworks: Food contact safety, sustainability mandates.

- Competitive Product Substitutes: Conventional plastics, aluminum foil.

- End-User Demographics: Busy households, convenience-seeking consumers.

- M&A Trends: Consolidation for portfolio expansion and market reach.

Ovenable Food Packaging Growth Trends & Insights

The global ovenable food packaging market is projected to experience robust growth, with an estimated market size of $12,500 million units in 2025, escalating to $18,900 million units by 2033, signifying a Compound Annual Growth Rate (CAGR) of 5.2% during the forecast period. This expansion is propelled by significant shifts in consumer behavior and lifestyle. The increasing urbanization and the proliferation of dual-income households globally are creating a heightened demand for convenient food solutions that minimize preparation time. Ovenable packaging directly addresses this need by allowing consumers to heat or cook food directly in the packaging, reducing the number of dishes to wash and simplifying the cooking process. Technological advancements in polymer science and manufacturing processes are crucial in this evolution. Innovations in materials like high-performance plastics, such as PET and PP, and advanced coated papers are enabling the development of packaging that can withstand higher temperatures, maintain structural integrity, and prevent food spoilage. The adoption rate of ovenable packaging is also being influenced by the growing popularity of premium convenience foods, including gourmet ready-meals, ethnic cuisine kits, and artisanal bakery products. These segments often leverage ovenable packaging to maintain product freshness, enhance visual appeal upon heating, and offer a superior consumer experience. Market penetration is expected to climb from 28% in 2025 to 41% by 2033, reflecting increased consumer acceptance and wider availability across retail channels. The COVID-19 pandemic further accelerated this trend, as consumers sought at-home dining solutions that mirrored restaurant quality and convenience. Online food delivery services and meal kit subscriptions, which often utilize ovenable packaging for optimal delivery and reheating, have also played a pivotal role in driving adoption rates and market penetration. The ongoing research into sustainable and recyclable ovenable packaging solutions is also a significant factor, addressing environmental concerns and aligning with evolving consumer preferences for eco-conscious products. This commitment to sustainability, coupled with the inherent convenience, is set to fuel substantial market expansion in the coming years. The market size in 2019 was $9,200 million units, growing to an estimated $11,800 million units in 2024, showcasing a steady upward trajectory.

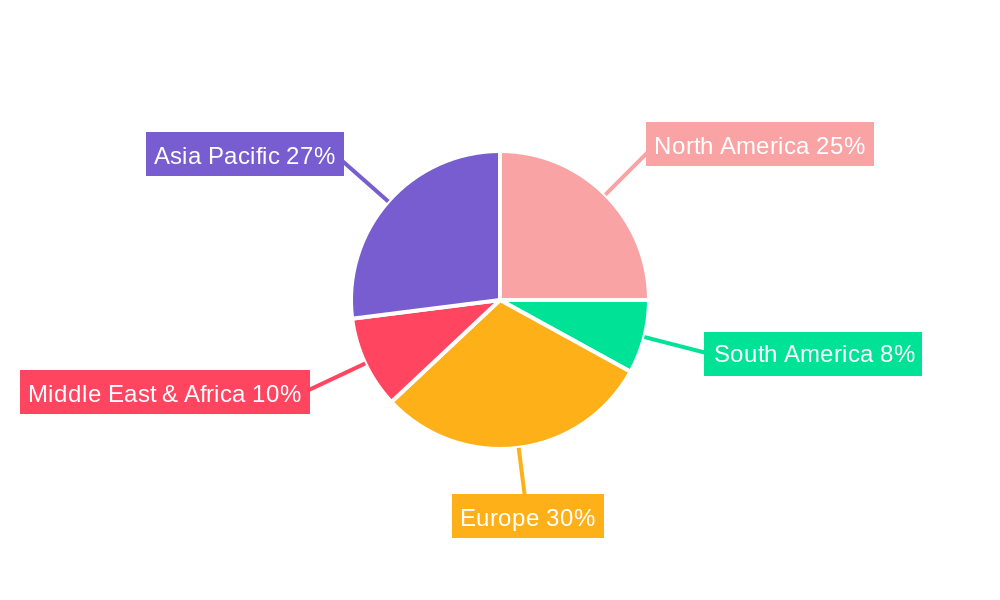

Dominant Regions, Countries, or Segments in Ovenable Food Packaging

North America, led by the United States, currently dominates the ovenable food packaging market, holding an estimated 35% market share in 2025. This regional dominance is attributed to several key factors, including a mature consumer market with a high disposable income, a well-established food processing industry, and a strong consumer preference for convenience. The large prevalence of single-person households and dual-income families in the US further amplifies the demand for ready-to-heat meals, a segment where ovenable packaging excels. Economic policies that support food manufacturing and innovation, coupled with robust retail infrastructure, facilitate the widespread availability and adoption of ovenable food packaging products.

Within the Application segment, the Meat application currently holds the largest market share, estimated at 42% in 2025. This is driven by the growing popularity of pre-portioned and ready-to-cook meat products, such as marinated chicken breasts, ready-to-roast roasts, and convenience meat meals. These products often require oven heating for optimal flavor and texture, making ovenable packaging an ideal choice for maintaining freshness and extending shelf life. The Bread application is a significant and growing segment, projected to capture 25% of the market by 2025, fueled by the demand for artisan breads, pastries, and ready-to-bake doughs that benefit from direct oven heating to achieve a fresh, home-baked quality. The Others segment, encompassing a wide range of products like prepared meals, desserts, and ethnic cuisines, is also experiencing substantial growth, expected to account for 33% by 2025, driven by the increasing variety and sophistication of convenient food offerings.

In terms of Types, Plastics constitute the dominant segment, projected to hold 68% of the market share in 2025. This is due to the versatility, durability, and excellent barrier properties of various plastics, such as PET, PP, and high-performance composites, which can be engineered to withstand oven temperatures while preserving food quality and preventing leakage. The Paper segment, though smaller, is experiencing significant growth, estimated at 32% in 2025. This growth is propelled by advancements in coated paperboard and specialized paper-based solutions that offer improved heat resistance and grease barrier properties, catering to the increasing consumer demand for sustainable and recyclable packaging options. The growth potential in emerging economies, particularly in Asia-Pacific, presents a substantial opportunity for market expansion due to rising disposable incomes and evolving dietary habits.

- Dominant Region: North America (USA) due to consumer demand and industry maturity.

- Leading Application: Meat, driven by convenience meat products and ready-to-cook meals.

- Leading Type: Plastics, owing to their functional properties and versatility.

- Growth Potential: Asia-Pacific, fueled by increasing disposable incomes and evolving consumer preferences.

Ovenable Food Packaging Product Landscape

The ovenable food packaging product landscape is characterized by continuous innovation focused on enhancing performance, sustainability, and consumer convenience. Key product developments include high-barrier plastic trays and films (e.g., PET, PP blends) capable of withstanding temperatures exceeding 220°C for extended periods, preserving food freshness and preventing spoilage. Advanced coated paperboard solutions are emerging, offering excellent grease and moisture resistance with improved ovenability, catering to the demand for more sustainable options. Unique selling propositions include the ability to directly transfer food from refrigerator to oven, eliminating the need for separate cooking vessels, thus reducing cleanup. Technological advancements in printing and lamination techniques enable vibrant, appealing graphics directly on ovenable packaging, enhancing shelf presence and brand recognition. These products are primarily applied in the packaging of ready-to-heat meals, meat products, baked goods, and desserts, offering superior food quality and consumer appeal.

Key Drivers, Barriers & Challenges in Ovenable Food Packaging

Key Drivers:

- Growing Demand for Convenience: Consumers increasingly seek time-saving meal solutions.

- Advancements in Material Science: Development of high-temperature resistant and barrier-enhanced materials.

- Rise of Ready-to-Eat & Ready-to-Cook Meals: These segments heavily rely on ovenable packaging for optimal product delivery.

- Sustainability Initiatives: Growing consumer and regulatory pressure for eco-friendly packaging solutions.

- Technological Innovations in Manufacturing: Enabling efficient and cost-effective production of ovenable packaging.

Barriers & Challenges:

- High R&D and Material Costs: Developing and implementing new ovenable materials can be expensive, estimated at 15-20% higher than conventional packaging.

- Regulatory Compliance: Stringent food safety regulations and testing requirements for high-temperature applications.

- Consumer Education: Ensuring consumers understand safe usage and disposal of ovenable packaging.

- Competition from Traditional Packaging: Established and lower-cost alternatives like aluminum and conventional plastics.

- Supply Chain Volatility: Potential disruptions in the availability and pricing of specialized raw materials.

Emerging Opportunities in Ovenable Food Packaging

Emerging opportunities in the ovenable food packaging sector lie in the development of fully compostable and biodegradable ovenable materials, addressing the growing consumer and regulatory push for sustainability. The expansion of premium and gourmet ready-meal markets, particularly those catering to niche dietary requirements (e.g., vegan, gluten-free), presents a significant avenue for growth. Furthermore, the integration of smart packaging features, such as temperature indicators or freshness sensors, within ovenable solutions can enhance consumer trust and product safety. Untapped markets in developing economies, where convenience foods are gaining traction, also represent a substantial growth frontier. The increasing popularity of direct-to-consumer (DTC) food businesses and subscription boxes also creates a demand for innovative and aesthetically pleasing ovenable packaging.

Growth Accelerators in the Ovenable Food Packaging Industry

Growth in the ovenable food packaging industry is being significantly accelerated by strategic partnerships between material manufacturers and food producers. These collaborations foster co-innovation, leading to the development of tailored packaging solutions that meet specific product needs and consumer preferences. Technological breakthroughs in sustainable barrier coatings and high-heat resistant bioplastics are also acting as major growth accelerators, enabling brands to offer both convenience and environmental responsibility. Furthermore, market expansion strategies targeting developing economies, where the adoption of convenience foods is on an upward trajectory, are vital for long-term growth. The increasing investment in automation and advanced manufacturing processes is improving production efficiency and reducing costs, making ovenable packaging more accessible.

Key Players Shaping the Ovenable Food Packaging Market

- Sirane

- FFP Packaging

- Krehalon

- Plastopil

- PROVAC

- Clifton Packaging

- Package Concepts & Materials

- Flexipol

- DXC Packaging

- KM Packaging

Notable Milestones in Ovenable Food Packaging Sector

- 2019: Sirane launches its "EvoWrap" range of ovenable and freezable films, enhancing product versatility.

- 2020: FFP Packaging invests in new high-speed converting lines to increase production of ovenable trays.

- 2021: Krehalon develops advanced barrier films with improved ovenability and shelf-life extension capabilities.

- 2022: Plastopil introduces a new generation of sustainable ovenable plastic trays with a reduced carbon footprint.

- 2023 (Q1): PROVAC enhances its portfolio with innovative ovenable lidding films for a wider range of food applications.

- 2023 (Q3): Clifton Packaging secures a major contract for ovenable packaging solutions for a leading ready-meal producer.

- 2024: Package Concepts & Materials rolls out new ovenable paperboard solutions for the bakery segment.

In-Depth Ovenable Food Packaging Market Outlook

The outlook for the ovenable food packaging market remains exceptionally promising, fueled by persistent consumer demand for convenience and continuous innovation in material science and manufacturing. Growth accelerators such as the increasing focus on sustainability, the expansion of e-commerce in the food sector, and the development of personalized meal solutions will continue to shape the market's trajectory. Strategic opportunities lie in further exploring bio-based and recyclable ovenable materials, enhancing product functionality with smart technologies, and penetrating emerging markets with tailored solutions. The market is poised for sustained growth, presenting lucrative avenues for companies that can adapt to evolving consumer preferences and technological advancements, with an estimated market value of $18,900 million units by 2033.

Ovenable Food Packaging Segmentation

-

1. Application

- 1.1. Meat

- 1.2. Bread

- 1.3. Others

-

2. Types

- 2.1. Plastics

- 2.2. Paper

Ovenable Food Packaging Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Ovenable Food Packaging Regional Market Share

Geographic Coverage of Ovenable Food Packaging

Ovenable Food Packaging REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Ovenable Food Packaging Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Meat

- 5.1.2. Bread

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Plastics

- 5.2.2. Paper

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Ovenable Food Packaging Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Meat

- 6.1.2. Bread

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Plastics

- 6.2.2. Paper

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Ovenable Food Packaging Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Meat

- 7.1.2. Bread

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Plastics

- 7.2.2. Paper

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Ovenable Food Packaging Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Meat

- 8.1.2. Bread

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Plastics

- 8.2.2. Paper

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Ovenable Food Packaging Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Meat

- 9.1.2. Bread

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Plastics

- 9.2.2. Paper

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Ovenable Food Packaging Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Meat

- 10.1.2. Bread

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Plastics

- 10.2.2. Paper

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Sirane

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 FFP Packaging

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Krehalon

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Plastopil

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 PROVAC

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Clifton Packaging

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Package Concepts & Materials

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Flexipol

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 DXC Packaging

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 KM Packaging

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Sirane

List of Figures

- Figure 1: Global Ovenable Food Packaging Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Ovenable Food Packaging Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Ovenable Food Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Ovenable Food Packaging Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Ovenable Food Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Ovenable Food Packaging Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Ovenable Food Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Ovenable Food Packaging Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Ovenable Food Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Ovenable Food Packaging Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Ovenable Food Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Ovenable Food Packaging Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Ovenable Food Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Ovenable Food Packaging Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Ovenable Food Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Ovenable Food Packaging Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Ovenable Food Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Ovenable Food Packaging Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Ovenable Food Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Ovenable Food Packaging Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Ovenable Food Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Ovenable Food Packaging Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Ovenable Food Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Ovenable Food Packaging Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Ovenable Food Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Ovenable Food Packaging Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Ovenable Food Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Ovenable Food Packaging Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Ovenable Food Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Ovenable Food Packaging Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Ovenable Food Packaging Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Ovenable Food Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Ovenable Food Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Ovenable Food Packaging Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Ovenable Food Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Ovenable Food Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Ovenable Food Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Ovenable Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Ovenable Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Ovenable Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Ovenable Food Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Ovenable Food Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Ovenable Food Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Ovenable Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Ovenable Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Ovenable Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Ovenable Food Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Ovenable Food Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Ovenable Food Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Ovenable Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Ovenable Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Ovenable Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Ovenable Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Ovenable Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Ovenable Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Ovenable Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Ovenable Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Ovenable Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Ovenable Food Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Ovenable Food Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Ovenable Food Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Ovenable Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Ovenable Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Ovenable Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Ovenable Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Ovenable Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Ovenable Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Ovenable Food Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Ovenable Food Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Ovenable Food Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Ovenable Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Ovenable Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Ovenable Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Ovenable Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Ovenable Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Ovenable Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Ovenable Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Ovenable Food Packaging?

The projected CAGR is approximately 5.7%.

2. Which companies are prominent players in the Ovenable Food Packaging?

Key companies in the market include Sirane, FFP Packaging, Krehalon, Plastopil, PROVAC, Clifton Packaging, Package Concepts & Materials, Flexipol, DXC Packaging, KM Packaging.

3. What are the main segments of the Ovenable Food Packaging?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 427.4 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Ovenable Food Packaging," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Ovenable Food Packaging report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Ovenable Food Packaging?

To stay informed about further developments, trends, and reports in the Ovenable Food Packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence