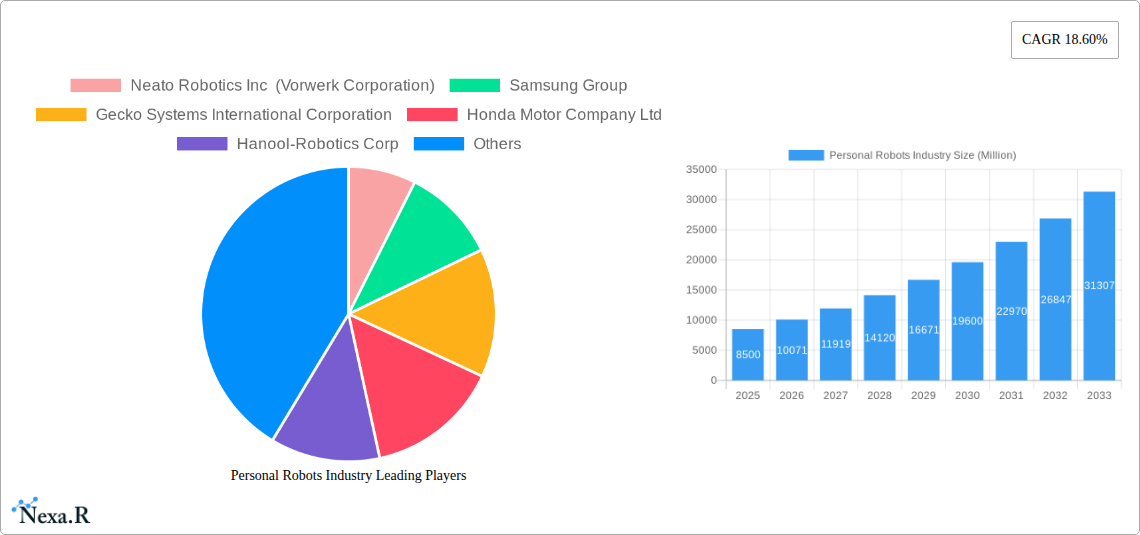

Key Insights

The global Personal Robots market is poised for substantial growth, projected to reach a significant market size by 2033. Fueled by a robust Compound Annual Growth Rate (CAGR) of 18.60%, this industry is experiencing a rapid expansion driven by increasing consumer adoption of automation in daily life. Key market drivers include the rising demand for convenience and efficiency in household tasks, the growing need for specialized assistance for the elderly and individuals with disabilities, and the escalating integration of smart home technologies, which inherently include personal robotic solutions for security and surveillance. The entertainment sector is also witnessing a surge in demand for interactive and educational robots, further propelling market expansion. This dynamic landscape is characterized by continuous innovation, with companies actively developing more sophisticated and user-friendly robotic companions.

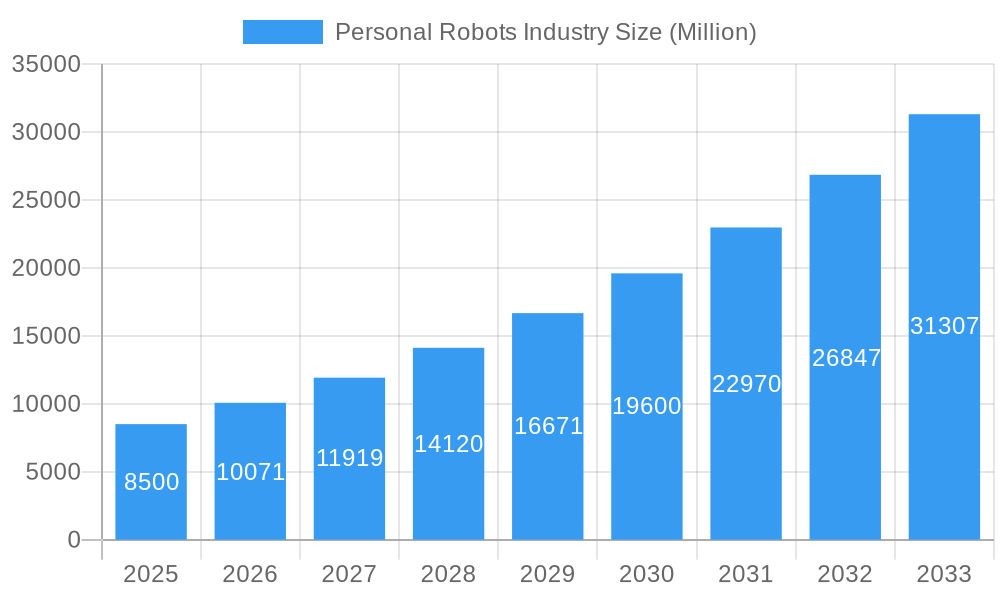

Personal Robots Industry Market Size (In Billion)

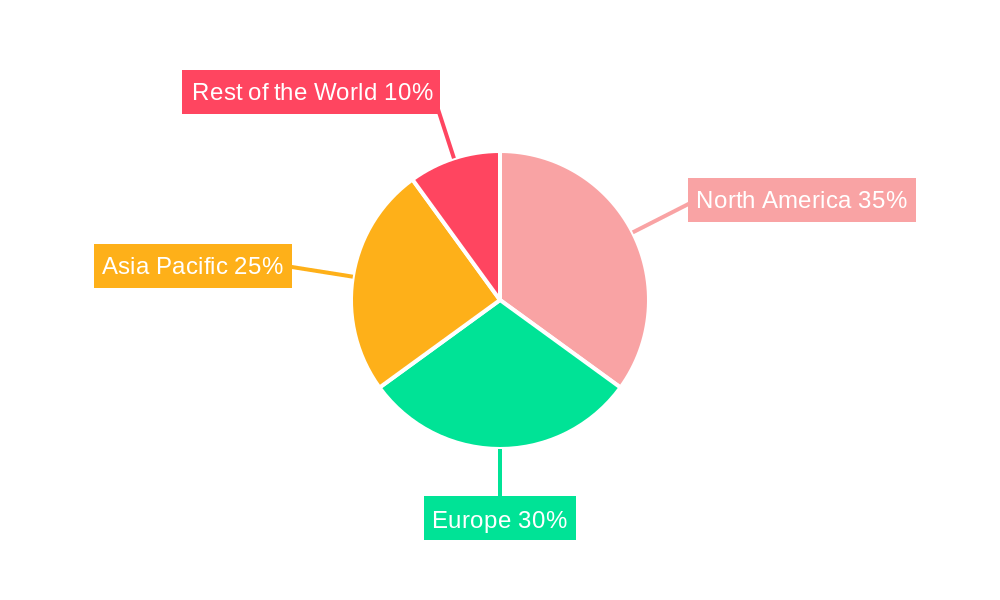

The market is segmented into several key areas, with Household Work and Elderly and Handicap Assistance expected to command significant shares due to demographic shifts and evolving lifestyle needs. The rise of advanced AI and machine learning is enabling personal robots to perform increasingly complex tasks, from cleaning and cooking to providing companionship and care. While growth is strong, the market faces certain restraints, including high initial costs of advanced robotic systems and potential consumer concerns regarding data privacy and security associated with interconnected devices. However, the relentless pace of technological advancement, coupled with strategic investments and partnerships among leading companies like iRobot, Ecovacs Robotics, Samsung, and Honda, is expected to overcome these challenges, paving the way for widespread adoption across various regions, particularly in North America and Europe, with Asia Pacific also emerging as a crucial growth hub.

Personal Robots Industry Company Market Share

Comprehensive Personal Robots Industry Report: Market Dynamics, Growth Forecasts, and Key Player Insights (2019-2033)

This in-depth report provides a panoramic view of the global Personal Robots Industry, meticulously analyzing market dynamics, growth trajectories, and the competitive landscape from 2019 to 2033. With a base year of 2025 and a forecast period extending to 2033, this study offers critical insights into the evolving personal robot market, encompassing household work, entertainment, elderly and handicap assistance, and home security. Leveraging high-traffic keywords such as "personal robots market," "household robots," "AI-powered robots," "robotics industry trends," and "smart home devices," this report is optimized for maximum search engine visibility and aims to engage industry professionals, investors, and researchers seeking a definitive understanding of this burgeoning sector. We explore the parent and child market segments to provide a granular view of market opportunities. All quantitative values are presented in Million units.

Personal Robots Industry Market Dynamics & Structure

The personal robots industry is characterized by a dynamic market structure driven by rapid technological advancements, increasing consumer adoption of smart home technologies, and a growing demand for automation in daily life. Market concentration varies across segments, with a few key players dominating the household cleaning robot segment while the elderly assistance and entertainment robot segments show higher fragmentation and potential for new entrants. Technological innovation, particularly in artificial intelligence (AI), machine learning, and sensor technology, acts as a primary growth driver, enabling robots to perform more complex tasks and interact more intuitively with humans. Regulatory frameworks are gradually evolving to address safety standards, data privacy, and ethical considerations associated with personal robotics. Competitive product substitutes, such as advanced smart home appliances and specialized service providers, pose a challenge, but the unique value proposition of personal robots in terms of convenience, efficiency, and personalized assistance continues to fuel demand. End-user demographics are expanding beyond early adopters to mainstream consumers, driven by increased affordability and the desire for enhanced quality of life. Mergers and acquisitions (M&A) trends indicate a consolidation phase in certain segments, with larger corporations acquiring innovative startups to expand their product portfolios and market reach. For instance, the acquisition of iRobot by Amazon signifies a major shift in the household robot landscape.

- Market Concentration: Highly concentrated in household cleaning; fragmented in elderly assistance and entertainment.

- Technological Innovation: AI, ML, advanced sensors, natural language processing are key drivers.

- Regulatory Frameworks: Evolving to address safety, privacy, and ethical concerns.

- Competitive Substitutes: Smart home appliances, specialized service providers.

- End-User Demographics: Expanding from early adopters to mainstream households.

- M&A Trends: Consolidation in mature segments, strategic acquisitions for technological advantage.

Personal Robots Industry Growth Trends & Insights

The personal robots industry is poised for robust growth, propelled by a confluence of technological breakthroughs, shifting consumer behaviors, and increasing societal needs. The market size is projected to expand significantly, driven by a compound annual growth rate (CAGR) of approximately 15.5% from 2025 to 2033. This growth is underpinned by escalating adoption rates of robotic solutions across various domestic applications. Technological disruptions, particularly in AI and robotics, are enabling more sophisticated functionalities, from autonomous navigation and object recognition to personalized interaction and task execution. Consumer behavior is shifting towards prioritizing convenience, efficiency, and seamless integration of technology into daily routines. The demand for robots that can assist with household chores, provide companionship, and support independent living for the elderly and individuals with disabilities is rapidly increasing. Market penetration is expected to deepen as product costs decrease and awareness of robotic capabilities grows. The historical period (2019-2024) witnessed initial traction, with early innovations in robotic vacuum cleaners and educational robots paving the way for broader acceptance. The estimated year of 2025 marks a pivotal point where mainstream adoption begins to accelerate, driven by more advanced and affordable offerings. Future growth will be further influenced by the development of more intuitive human-robot interaction, enhanced safety features, and the integration of robots into broader smart home ecosystems. The increasing prevalence of single-person households and an aging global population are significant demographic drivers contributing to the sustained growth of the personal robots market.

Dominant Regions, Countries, or Segments in Personal Robots Industry

The Household Work segment stands as the dominant force within the personal robots industry, significantly outperforming other segments in terms of market share and projected growth potential. This segment primarily encompasses robotic vacuum cleaners, mops, window cleaners, and lawnmowers, addressing a fundamental need for domestic task automation. The increasing prevalence of busy lifestyles and a growing desire for convenience among consumers worldwide are the primary drivers behind the segment's dominance.

- Key Drivers for Household Work Dominance:

- Convenience and Time-Saving: Robots automate time-consuming chores, freeing up consumers for other activities.

- Technological Advancements: Continuous innovation in navigation, mapping, and cleaning efficiency.

- Growing Smart Home Integration: Seamless integration with other smart home devices enhances functionality and appeal.

- Increased Disposable Income: Growing middle class in developed and developing economies can afford premium household solutions.

- Product Affordability: Declining manufacturing costs leading to more accessible price points for consumers.

North America, particularly the United States, is a leading region driving the growth of the personal robots industry, with a high adoption rate for smart home technologies and a strong consumer preference for innovative solutions. This is closely followed by Europe, where a strong emphasis on technological advancement and an aging population contribute to demand, especially in the elderly assistance segment. Asia-Pacific is emerging as a rapid growth region, fueled by increasing disposable incomes, rapid urbanization, and a burgeoning interest in AI and robotics, especially in the household work and entertainment segments.

- Market Share & Growth Potential: The Household Work segment is estimated to hold over 50% of the total personal robots market share in 2025, with a projected CAGR of 16.2% during the forecast period.

- Regional Dominance Factors:

- North America: High consumer spending power, early adoption of new technologies, strong presence of key manufacturers.

- Europe: Significant aging population driving demand for assistance robots, strong regulatory support for robotics research and development.

- Asia-Pacific: Rapid economic development, large consumer base, increasing investment in AI and robotics manufacturing, growing middle class.

The Elderly and Handicap Assistance segment is also experiencing substantial growth, driven by global demographic shifts towards an aging population and the desire to promote independent living. While currently smaller in market share compared to Household Work, its growth rate is projected to be higher, indicating significant future potential.

Personal Robots Industry Product Landscape

The personal robots industry is witnessing a surge in product innovation, driven by advancements in AI, sensor technology, and materials science. Current offerings range from sophisticated autonomous cleaning robots like the ECOVACS DEEBOT X1, featuring comprehensive vacuuming and mopping capabilities for a hands-free cleaning experience, to intelligent navigation systems in robots like Samsung's JetBot 90 AI+, capable of recognizing and avoiding obstacles. Beyond household chores, entertainment robots are evolving with enhanced interactive features and personalized content delivery, while elderly and handicap assistance robots are incorporating advanced mobility, safety monitoring, and communication functionalities. The unique selling propositions of these robots lie in their ability to perform complex tasks with minimal human intervention, enhance convenience, and improve the quality of life for their users. Technological advancements focus on improving battery life, increasing processing power for real-time decision-making, and developing more intuitive user interfaces for seamless interaction.

Key Drivers, Barriers & Challenges in Personal Robots Industry

Key Drivers: The personal robots industry is propelled by several significant drivers. Technological innovation, particularly in AI, machine learning, and advanced sensor technology, is enabling robots to perform increasingly complex and nuanced tasks. Growing consumer demand for convenience and automation in daily life, fueled by busy lifestyles and an aging population seeking assistance, is a primary market pull. Decreasing manufacturing costs and increasing affordability are making personal robots more accessible to a wider consumer base. Government initiatives and R&D funding in robotics also act as catalysts.

Barriers & Challenges: Despite its growth, the industry faces several challenges. High initial product costs for some advanced robots can still be a barrier to widespread adoption. Consumer concerns regarding data privacy and security are significant, especially with connected and AI-powered devices. Technical limitations, such as battery life, reliability in complex environments, and the need for ongoing maintenance, can hinder user experience. Regulatory hurdles and standardization for safety and interoperability are still in development. Public perception and trust in autonomous machines remain critical factors. Supply chain disruptions can also impact production and availability. For instance, the semiconductor shortage has affected the production of advanced robotic components, impacting the delivery of sophisticated personal robots. The projected impact of these challenges on the market can lead to a delay in market penetration for certain high-end segments, estimated at 5-10% for the next two years.

Emerging Opportunities in Personal Robots Industry

Emerging opportunities in the personal robots industry are abundant, driven by evolving consumer preferences and technological advancements. The elderly and handicap assistance segment presents a significant untapped market, with growing demand for robots that can support independent living, provide companionship, and assist with daily tasks. Personalized education and entertainment robots are gaining traction, offering adaptive learning experiences and interactive play. The integration of robots into smart home ecosystems to create more intuitive and responsive living environments is a key area for growth. Furthermore, opportunities exist in developing robots for niche applications such as pet care, gardening, and specialized home maintenance. The growing focus on sustainable and energy-efficient robotic solutions also presents a compelling avenue for innovation.

Growth Accelerators in the Personal Robots Industry Industry

Several factors are accelerating the growth of the personal robots industry. Continued breakthroughs in AI and machine learning are enhancing robot intelligence, enabling more sophisticated autonomy and human-like interaction. Strategic partnerships and collaborations between technology companies, research institutions, and consumer electronics manufacturers are fostering innovation and faster product development. Market expansion into emerging economies driven by increasing disposable incomes and a growing appetite for advanced technology will significantly boost global sales. The development of modular and customizable robotic platforms will also cater to diverse consumer needs. Furthermore, increasing government support for robotics research and development and the establishment of clearer ethical guidelines will foster greater consumer confidence and market acceptance.

Key Players Shaping the Personal Robots Industry Market

- Neato Robotics Inc (Vorwerk Corporation)

- Samsung Group

- Gecko Systems International Corporation

- Honda Motor Company Ltd

- Hanool-Robotics Corp

- F&P Robotics AG

- Segway Inc (Ninebot Company)

- iRobot Corporation

- Ecovacs Robotics Inc

- Sony Corporation

Notable Milestones in Personal Robots Industry Sector

- January 2022: ECOVACS, a service robotics company, unveiled its market-changing DEEBOT X1 cleaning robots at CES 2022. With fully automated and ultra-premium robotic vacuum & mop cleaning systems. The product offers an all-in-one solution with the ultimate goal of a cultural shift away from in-home, hands-on work to a truly hands-free and consistent cleaning experience.

- January 2021: Samsung Electronics Co., Ltd. introduced the new JetBot 90 AI+ that features smart technologies. The product is designed to optimize its cleaning route and respond to its environment. The new robot uses a 3D sensor to recognize the difference between objects such as a toy and the leg of a chair; the sensor also enables it to detect even small objects on the floor and recognizes a room's shape to maneuver around it.

In-Depth Personal Robots Industry Market Outlook

The future outlook for the personal robots industry is exceptionally promising, driven by sustained technological advancements and an increasing integration into the fabric of daily life. Growth accelerators such as the maturation of AI, development of more sophisticated sensors, and the increasing affordability of robotic components will continue to fuel market expansion. Strategic opportunities lie in addressing the growing needs of an aging global population with advanced elderly assistance robots, and in further developing robots that offer personalized entertainment and educational experiences. The expansion of smart home ecosystems will create further demand for interconnected robotic solutions. The industry's ability to foster public trust through enhanced safety and data privacy protocols will be crucial for unlocking its full market potential. Projections indicate continued strong CAGR, reaching an estimated xx Million units in value by 2033.

Personal Robots Industry Segmentation

-

1. Type

- 1.1. Household Work

- 1.2. Entertainment

- 1.3. Elderly and Handicap Assistance

- 1.4. Home Security and Surveillance

- 1.5. Other type

Personal Robots Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Rest of the World

Personal Robots Industry Regional Market Share

Geographic Coverage of Personal Robots Industry

Personal Robots Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 18.60% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing demand for Assistive Robots for Handicapped and Elderly People; Reducing Price of Personal Robots

- 3.3. Market Restrains

- 3.3.1. Technical Complexity Associated with Operating these Robots

- 3.4. Market Trends

- 3.4.1. Personal Robots for Household Work is Expected to Hold a Major Share of the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Personal Robots Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Household Work

- 5.1.2. Entertainment

- 5.1.3. Elderly and Handicap Assistance

- 5.1.4. Home Security and Surveillance

- 5.1.5. Other type

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Personal Robots Industry Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Household Work

- 6.1.2. Entertainment

- 6.1.3. Elderly and Handicap Assistance

- 6.1.4. Home Security and Surveillance

- 6.1.5. Other type

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Europe Personal Robots Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Household Work

- 7.1.2. Entertainment

- 7.1.3. Elderly and Handicap Assistance

- 7.1.4. Home Security and Surveillance

- 7.1.5. Other type

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Asia Pacific Personal Robots Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Household Work

- 8.1.2. Entertainment

- 8.1.3. Elderly and Handicap Assistance

- 8.1.4. Home Security and Surveillance

- 8.1.5. Other type

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Rest of the World Personal Robots Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Household Work

- 9.1.2. Entertainment

- 9.1.3. Elderly and Handicap Assistance

- 9.1.4. Home Security and Surveillance

- 9.1.5. Other type

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Competitive Analysis

- 10.1. Global Market Share Analysis 2025

- 10.2. Company Profiles

- 10.2.1 Neato Robotics Inc (Vorwerk Corporation)

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 Samsung Group

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Gecko Systems International Corporation

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Honda Motor Company Ltd

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Hanool-Robotics Corp

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 F&P Robotics AG*List Not Exhaustive

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 Segway Inc (Ninebot Company)

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 iRobot Corporation

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 Ecovacs Robotics Inc

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 Sony Corporation

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.1 Neato Robotics Inc (Vorwerk Corporation)

List of Figures

- Figure 1: Global Personal Robots Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Personal Robots Industry Revenue (Million), by Type 2025 & 2033

- Figure 3: North America Personal Robots Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Personal Robots Industry Revenue (Million), by Country 2025 & 2033

- Figure 5: North America Personal Robots Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Europe Personal Robots Industry Revenue (Million), by Type 2025 & 2033

- Figure 7: Europe Personal Robots Industry Revenue Share (%), by Type 2025 & 2033

- Figure 8: Europe Personal Robots Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: Europe Personal Robots Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Pacific Personal Robots Industry Revenue (Million), by Type 2025 & 2033

- Figure 11: Asia Pacific Personal Robots Industry Revenue Share (%), by Type 2025 & 2033

- Figure 12: Asia Pacific Personal Robots Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Asia Pacific Personal Robots Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Rest of the World Personal Robots Industry Revenue (Million), by Type 2025 & 2033

- Figure 15: Rest of the World Personal Robots Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Rest of the World Personal Robots Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Rest of the World Personal Robots Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Personal Robots Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Global Personal Robots Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Global Personal Robots Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 4: Global Personal Robots Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 5: Global Personal Robots Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 6: Global Personal Robots Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Global Personal Robots Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 8: Global Personal Robots Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: Global Personal Robots Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 10: Global Personal Robots Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Personal Robots Industry?

The projected CAGR is approximately 18.60%.

2. Which companies are prominent players in the Personal Robots Industry?

Key companies in the market include Neato Robotics Inc (Vorwerk Corporation), Samsung Group, Gecko Systems International Corporation, Honda Motor Company Ltd, Hanool-Robotics Corp, F&P Robotics AG*List Not Exhaustive, Segway Inc (Ninebot Company), iRobot Corporation, Ecovacs Robotics Inc, Sony Corporation.

3. What are the main segments of the Personal Robots Industry?

The market segments include Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Growing demand for Assistive Robots for Handicapped and Elderly People; Reducing Price of Personal Robots.

6. What are the notable trends driving market growth?

Personal Robots for Household Work is Expected to Hold a Major Share of the Market.

7. Are there any restraints impacting market growth?

Technical Complexity Associated with Operating these Robots.

8. Can you provide examples of recent developments in the market?

January 2022 - ECOVACS, a service robotics company, unveiled its market-changing DEEBOT X1 cleaning robots at CES 2022. With fully automated and ultra-premium robotic vacuum & mop cleaning systems. The product offers an all-in-one solution with the ultimate goal of a cultural shift away from in-home, hands-on work to a truly hands-free and consistent cleaning experience.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Personal Robots Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Personal Robots Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Personal Robots Industry?

To stay informed about further developments, trends, and reports in the Personal Robots Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence