Key Insights

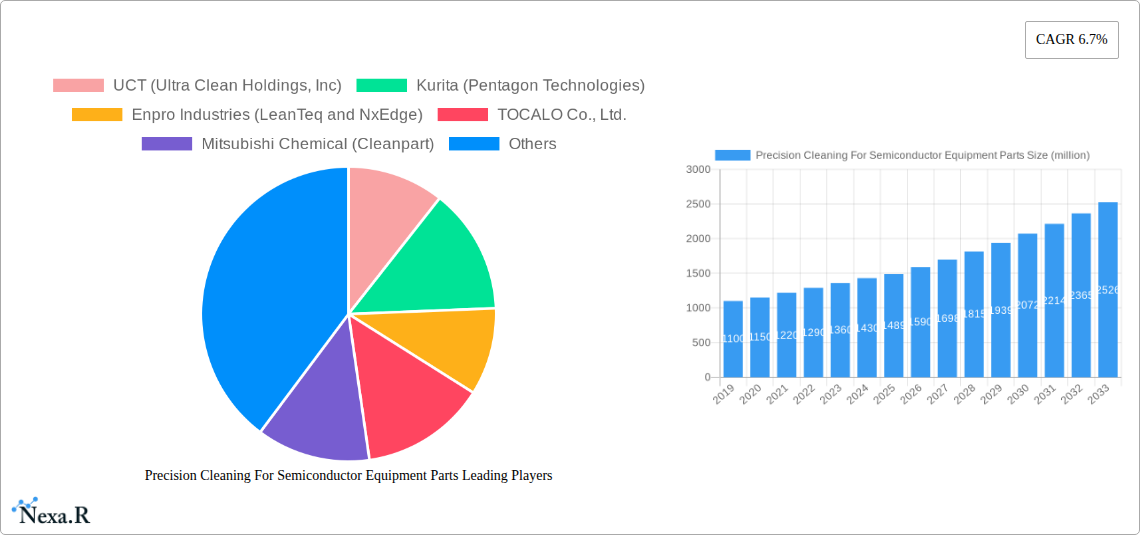

The global market for Precision Cleaning for Semiconductor Equipment Parts is poised for significant growth, projected to reach approximately USD 1489 million in 2025, with an estimated Compound Annual Growth Rate (CAGR) of 6.7% extending through 2033. This robust expansion is primarily fueled by the relentless demand for advanced semiconductors across burgeoning sectors like artificial intelligence, 5G, and the Internet of Things (IoT). The intricate and sensitive nature of semiconductor manufacturing necessitates the highest standards of cleanliness for equipment parts to ensure optimal performance, yield, and device reliability. As wafer sizes continue to increase, particularly with the growing dominance of 300mm equipment, the need for specialized and highly effective precision cleaning solutions intensifies. Companies are investing heavily in sophisticated cleaning technologies and processes to maintain the integrity of critical components such as those used in etching, thin film deposition (CVD/PVD), lithography, ion implantation, diffusion, and chemical mechanical planarization (CMP). This market dynamism is characterized by a focus on innovation in cleaning chemistries, automated systems, and particle control, all critical for meeting the exacting standards of the semiconductor industry.

The market is segmented by application, with Semiconductor Etching Equipment Parts, Semiconductor Thin Film (CVD/PVD), and Lithography Machines representing key areas driving demand. The shift towards larger wafer diameters, with 300mm equipment parts leading the charge, underscores the industry's commitment to higher throughput and lower costs per chip. However, the continued relevance of 200mm and even older 150mm equipment in niche applications and for specific markets ensures a diversified demand landscape. Geographically, Asia Pacific, particularly China, South Korea, and Taiwan, is expected to remain the largest and fastest-growing market due to its substantial semiconductor manufacturing base. North America and Europe also represent significant markets, driven by advanced research and development and a growing focus on reshoring semiconductor production. Key players such as UCT (Ultra Clean Holdings, Inc), Kurita (Pentagon Technologies), Enpro Industries, and Mitsubishi Chemical are actively engaged in strategic partnerships, mergers, and acquisitions to enhance their technological capabilities and market reach, further shaping the competitive environment.

This comprehensive report delves into the dynamic and critical market for precision cleaning services and solutions for semiconductor manufacturing equipment parts. With the semiconductor industry's relentless pursuit of miniaturization and increased performance, the demand for ultra-clean components and meticulous cleaning processes is paramount. This analysis leverages extensive data from 2019-2024 (historical period), with a base year of 2025 and a forecast period extending to 2033, providing critical insights into market evolution, growth drivers, and future opportunities. The report targets semiconductor manufacturers, equipment OEMs, cleaning service providers, and technology investors seeking to understand and capitalize on this specialized market.

Precision Cleaning For Semiconductor Equipment Parts Market Dynamics & Structure

The precision cleaning market for semiconductor equipment parts exhibits a moderately concentrated structure, with key players strategically positioning themselves to cater to the evolving needs of wafer fabrication and advanced packaging. Technological innovation remains a primary driver, fueled by the industry's insatiable demand for lower defect rates and enhanced equipment uptime. Companies are investing heavily in advanced cleaning chemistries, plasma technologies, and automated cleaning systems designed for delicate and complex component geometries. Regulatory frameworks, particularly those related to environmental impact and the use of hazardous materials, influence the adoption of greener cleaning solutions and waste management practices. Competitive product substitutes, such as in-situ cleaning methods and component redesign for self-cleaning properties, are emerging but currently lack the comprehensive efficacy of dedicated precision cleaning services. End-user demographics are increasingly sophisticated, demanding tailored solutions for specific equipment types and materials, including exotic alloys and specialized polymers used in advanced etch, deposition, and lithography processes. Mergers and acquisition (M&A) trends are evident as larger entities seek to expand their service portfolios and geographical reach, consolidating market share and enhancing their technological capabilities. For instance, the historical period saw an estimated $500 million in M&A deals, with a projected increase to $800 million in the forecast period, reflecting the industry's consolidation. Innovation barriers include the high capital investment required for cutting-edge cleaning technologies and the stringent qualification processes for new cleaning methods, often taking 12-24 months for approval in leading foundries.

- Market Concentration: Moderately concentrated with a few dominant global players and a growing number of specialized regional providers.

- Technological Innovation Drivers: Miniaturization in chip design, demand for higher yields, development of new semiconductor materials, and the need for extended equipment lifespan.

- Regulatory Frameworks: Focus on environmental compliance, hazardous substance reduction, and waste stream management.

- Competitive Product Substitutes: In-situ cleaning technologies, advanced material coatings, and modular equipment design.

- End-User Demographics: Increasingly specialized requirements for different fab processes (etch, deposition, lithography, CMP), material compatibility, and particle-level cleanliness standards.

- M&A Trends: Strategic acquisitions for technology integration, service expansion, and market share consolidation.

Precision Cleaning For Semiconductor Equipment Parts Growth Trends & Insights

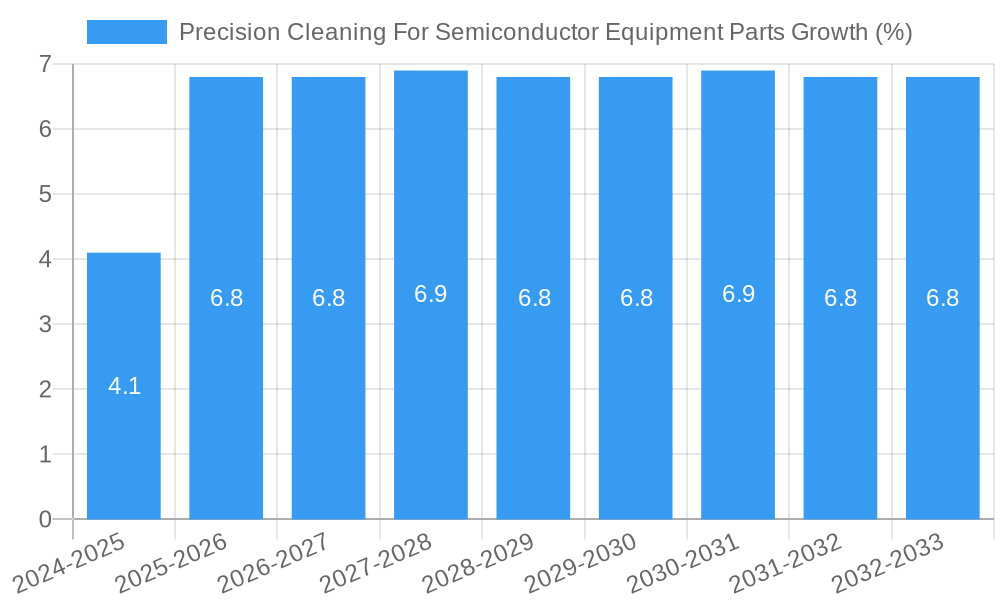

The precision cleaning market for semiconductor equipment parts is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of 10.5% from 2025 to 2033, reaching an estimated market size of $25 billion by 2033. This growth is underpinned by the escalating complexity of semiconductor manufacturing processes and the continuous drive for higher yields and device reliability. The base year, 2025, sees the market valued at approximately $12 billion, reflecting sustained demand driven by the ongoing expansion of global semiconductor manufacturing capacity and the ramp-up of new fabrication plants. Adoption rates for advanced cleaning solutions are steadily increasing as fabs recognize the direct correlation between component cleanliness and wafer quality, translating into significant cost savings by minimizing rework and scrap. Technological disruptions, such as the introduction of supercritical CO2 cleaning and advanced ion bombardment techniques, are gaining traction, offering environmentally friendly and highly effective alternatives to traditional wet cleaning methods. Consumer behavior shifts are characterized by an increasing preference for integrated cleaning solutions that encompass material analysis, process optimization, and contamination control throughout the equipment lifecycle. The market penetration of specialized cleaning services is projected to reach 75% by 2030, up from an estimated 60% in 2025, driven by the recognition of cleaning as a critical, value-adding step rather than a mere operational necessity. Adoption of 300mm equipment parts cleaning is leading the charge, representing 65% of the market in 2025, with significant growth anticipated in the cleaning of parts for advanced lithography and etching, areas demanding the utmost precision. The market is evolving from transactional cleaning services to strategic partnerships focused on predictive maintenance and contamination prevention strategies, a trend supported by the increasing investment in R&D by key industry players.

Dominant Regions, Countries, or Segments in Precision Cleaning For Semiconductor Equipment Parts

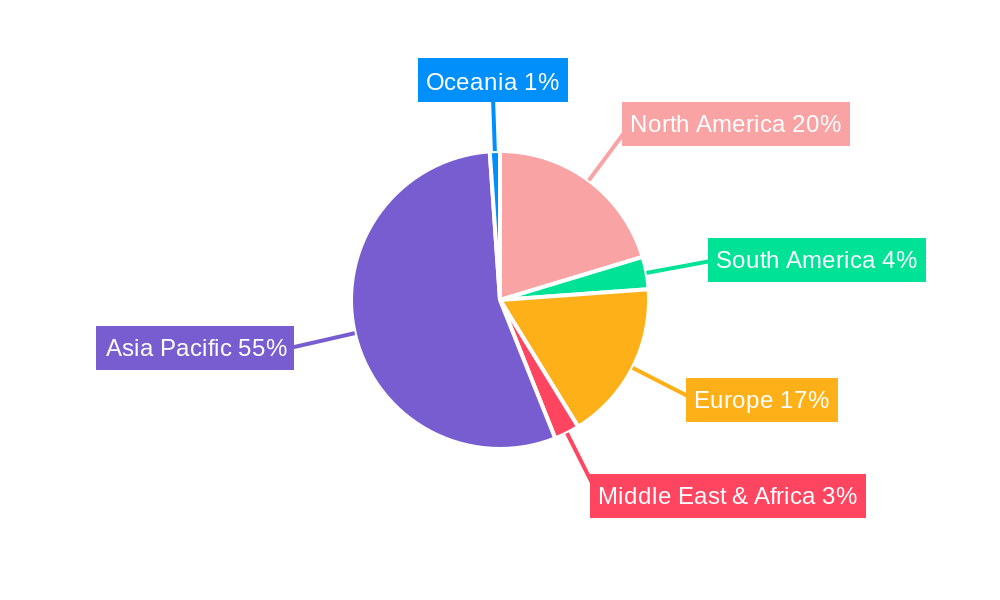

The Asia-Pacific region is the undisputed dominant force in the precision cleaning for semiconductor equipment parts market, driven by its status as the global epicenter of semiconductor manufacturing. This dominance is further amplified by the substantial presence of leading foundry and Integrated Device Manufacturer (IDM) operations, particularly in Taiwan, South Korea, and mainland China. In 2025, the Asia-Pacific region is estimated to account for 60% of the global market share, with a projected CAGR of 11.2% during the forecast period.

Within the Asia-Pacific, Taiwan stands out as a key country, housing some of the world's largest and most technologically advanced foundries. Its extensive ecosystem of semiconductor manufacturers, coupled with a strong government focus on supporting the high-tech industry, creates a perpetual demand for high-quality precision cleaning services. Taiwan's market share is estimated at 25% of the global market in 2025, with significant contributions from the Semiconductor Etching Equipment Parts and Semiconductor Thin Film (CVD/PVD) segments, which together represent approximately 45% of the regional demand.

South Korea follows closely, driven by the aggressive expansion strategies of its leading conglomerates in memory and logic chip manufacturing. The country's focus on next-generation semiconductor technologies, including advanced DRAM and NAND flash production, necessitates the most stringent cleaning standards for equipment parts. South Korea's market share is projected at 20% in 2025, with a particular emphasis on Lithography Machines and Diffusion Equipment Parts, areas where sub-micron particle contamination can be catastrophic.

Mainland China is the fastest-growing segment within Asia-Pacific, fueled by massive domestic investments and a strategic push towards semiconductor self-sufficiency. Its market share is expected to surge from 15% in 2025 to over 25% by 2033, driven by the rapid build-out of new fabs and the increasing demand for cleaning services across all equipment types. The CMP Equipment Parts and Ion Implant segments are witnessing substantial growth in China.

The dominance of Asia-Pacific is propelled by several key drivers:

- Economic Policies: Favorable government incentives, tax breaks, and direct investments in the semiconductor industry create an environment ripe for growth.

- Infrastructure: Well-established industrial zones, advanced logistics networks, and access to skilled labor support the operational efficiency of cleaning service providers.

- Market Share and Growth Potential: The sheer volume of wafer fabrication in the region, coupled with the continuous technological upgrades, ensures sustained demand for precision cleaning. The 300mm Equipment Parts segment, accounting for over 70% of the regional market, is a primary contributor to this dominance.

Precision Cleaning For Semiconductor Equipment Parts Product Landscape

The product landscape for precision cleaning in semiconductor equipment parts is characterized by a dual focus on advanced chemical formulations and sophisticated cleaning equipment. Innovations include ultra-high purity solvents and proprietary aqueous solutions designed for specific material compatibility, minimizing etching or damage to sensitive surfaces such as silicon wafers, ceramics, and specialty coatings. Performance metrics emphasize particle reduction down to single-digit nanometers, trace metal removal to parts-per-trillion levels, and organic contaminant elimination. Companies are developing specialized cleaning agents for complex geometries found in etch chambers, deposition sources, and lithography optics. Unique selling propositions often revolve around proprietary cleaning methodologies, such as advanced ultrasonic cavitation, supercritical fluid extraction, and plasma-enhanced cleaning, offering superior efficacy and reduced environmental impact. Technological advancements are also seen in the development of automated cleaning systems that integrate inline metrology and real-time particle monitoring, ensuring consistent and validated cleaning outcomes.

Key Drivers, Barriers & Challenges in Precision Cleaning For Semiconductor Equipment Parts

Key Drivers:

- Technological Advancements in Semiconductors: The relentless miniaturization and increasing complexity of semiconductor devices necessitate exceptionally clean equipment parts to achieve higher yields and device performance.

- Increasingly Stringent Cleanliness Standards: Fabs are demanding lower particle counts and trace metal contamination levels, driving the need for advanced cleaning technologies and services.

- Extended Equipment Lifespan and Reduced Downtime: Effective precision cleaning prolongs the operational life of expensive semiconductor equipment and minimizes costly unscheduled downtime.

- Growth of Advanced Packaging: The emergence of sophisticated packaging technologies requires meticulous cleaning of specialized components involved in the process.

- Government Initiatives and Investments: Global efforts to boost domestic semiconductor manufacturing capacity are spurring demand for related services, including precision cleaning.

Barriers & Challenges:

- High Capital Investment: Acquiring and maintaining state-of-the-art cleaning equipment and cleanroom facilities requires substantial financial outlay.

- Skilled Workforce Shortage: A lack of highly trained technicians and chemists with expertise in semiconductor-grade cleaning processes poses a significant challenge.

- Environmental Regulations: Increasing scrutiny on chemical usage and waste disposal necessitates the development and adoption of greener cleaning solutions.

- Cost Pressures: Semiconductor manufacturers are constantly seeking cost reductions, putting pressure on cleaning service providers to offer competitive pricing without compromising quality.

- Supply Chain Disruptions: Global supply chain issues can impact the availability of critical cleaning chemicals, equipment parts, and specialized materials, leading to production delays and increased costs. The impact of such disruptions can range from a 5-15% increase in operational costs and a 2-4 week delay in service delivery.

Emerging Opportunities in Precision Cleaning For Semiconductor Equipment Parts

Emerging opportunities lie in the development of environmentally friendly cleaning solutions, such as bio-based solvents and closed-loop recycling systems for cleaning chemistries, addressing growing sustainability concerns within the industry. The expansion of advanced packaging technologies, including 3D NAND and heterogeneous integration, presents a significant opportunity for specialized cleaning services tailored to these novel materials and intricate component designs. Furthermore, the increasing adoption of Industry 4.0 principles in semiconductor manufacturing opens doors for smart cleaning solutions that integrate AI-driven predictive maintenance, real-time contamination monitoring, and automated process optimization, offering enhanced efficiency and traceability. Untapped markets in emerging semiconductor manufacturing hubs also represent significant growth potential.

Growth Accelerators in the Precision Cleaning For Semiconductor Equipment Parts Industry

Key growth accelerators for the precision cleaning industry include rapid advancements in extreme ultraviolet (EUV) lithography, which demands unparalleled cleanliness for critical components. Strategic partnerships between cleaning service providers and semiconductor equipment manufacturers are crucial for co-developing optimized cleaning protocols for next-generation machinery. The continuous drive for higher wafer yields and the associated reduction in defectivity are powerful motivators for fabs to invest more in precision cleaning as a proactive measure rather than a reactive solution. Furthermore, the increasing prevalence of specialized materials like GaN and SiC in power electronics manufacturing creates a demand for cleaning processes that can handle their unique properties.

Key Players Shaping the Precision Cleaning For Semiconductor Equipment Parts Market

- UCT (Ultra Clean Holdings, Inc)

- Kurita (Pentagon Technologies)

- Enpro Industries (LeanTeq and NxEdge)

- TOCALO Co., Ltd.

- Mitsubishi Chemical (Cleanpart)

- KoMiCo

- Cinos

- Hansol IONES

- WONIK QnC

- Dftech

- Frontken Corporation Berhad

- KERTZ HIGH TECH

- Hung Jie Technology Corporation

- Shih Her Technology

- HTCSolar

- Persys Group

- MSR-FSR LLC

- Value Engineering Co., Ltd

- Neutron Technology Enterprise

- Ferrotec (Anhui) Technology Development Co., Ltd

- Jiangsu Kaiweitesi Semiconductor Technology Co., Ltd.

- HCUT Co., Ltd

- Suzhou Ever Distant Technology

- Chongqing Genori Technology Co., Ltd

- GRAND HITEK

Notable Milestones in Precision Cleaning For Semiconductor Equipment Parts Sector

- 2019: Introduction of advanced supercritical CO2 cleaning technologies offering a greener alternative.

- 2020: Increased investment in AI and machine learning for predictive contamination analysis in cleaning processes.

- 2021: Major semiconductor equipment manufacturers began offering integrated cleaning solutions as part of their service packages.

- 2022: Significant advancements in plasma cleaning technologies for nanoscale particle removal.

- 2023: Growing adoption of single-wafer cleaning techniques for enhanced process control.

- 2024: Expansion of precision cleaning services to support emerging semiconductor materials like Gallium Nitride (GaN).

In-Depth Precision Cleaning For Semiconductor Equipment Parts Market Outlook

The future market outlook for precision cleaning for semiconductor equipment parts is exceptionally bright, driven by the indispensable role of cleanliness in enabling next-generation semiconductor technologies. Growth accelerators, including the relentless pursuit of smaller feature sizes, the adoption of new materials, and the expansion of advanced packaging, will continue to fuel demand. Strategic partnerships and the integration of digital technologies like AI and IoT for process optimization and predictive maintenance will further solidify the market's growth trajectory. The increasing global emphasis on supply chain resilience and domestic manufacturing will also spur significant investment in cleaning infrastructure. Opportunities for sustainable cleaning solutions and specialized services for niche applications present considerable long-term potential.

Precision Cleaning For Semiconductor Equipment Parts Segmentation

-

1. Application

- 1.1. Semiconductor Etching Equipment Parts

- 1.2. Semiconductor Thin Film (CVD/PVD)

- 1.3. Lithography Machines

- 1.4. Ion Implant

- 1.5. Diffusion Equipment Parts

- 1.6. CMP Equipment Parts

- 1.7. Others

-

2. Type

- 2.1. 300mm Equipment Parts

- 2.2. 200mm Equipment Parts

- 2.3. 150mm and Others

Precision Cleaning For Semiconductor Equipment Parts Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Precision Cleaning For Semiconductor Equipment Parts REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 6.7% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Precision Cleaning For Semiconductor Equipment Parts Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Semiconductor Etching Equipment Parts

- 5.1.2. Semiconductor Thin Film (CVD/PVD)

- 5.1.3. Lithography Machines

- 5.1.4. Ion Implant

- 5.1.5. Diffusion Equipment Parts

- 5.1.6. CMP Equipment Parts

- 5.1.7. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. 300mm Equipment Parts

- 5.2.2. 200mm Equipment Parts

- 5.2.3. 150mm and Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Precision Cleaning For Semiconductor Equipment Parts Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Semiconductor Etching Equipment Parts

- 6.1.2. Semiconductor Thin Film (CVD/PVD)

- 6.1.3. Lithography Machines

- 6.1.4. Ion Implant

- 6.1.5. Diffusion Equipment Parts

- 6.1.6. CMP Equipment Parts

- 6.1.7. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. 300mm Equipment Parts

- 6.2.2. 200mm Equipment Parts

- 6.2.3. 150mm and Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Precision Cleaning For Semiconductor Equipment Parts Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Semiconductor Etching Equipment Parts

- 7.1.2. Semiconductor Thin Film (CVD/PVD)

- 7.1.3. Lithography Machines

- 7.1.4. Ion Implant

- 7.1.5. Diffusion Equipment Parts

- 7.1.6. CMP Equipment Parts

- 7.1.7. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. 300mm Equipment Parts

- 7.2.2. 200mm Equipment Parts

- 7.2.3. 150mm and Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Precision Cleaning For Semiconductor Equipment Parts Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Semiconductor Etching Equipment Parts

- 8.1.2. Semiconductor Thin Film (CVD/PVD)

- 8.1.3. Lithography Machines

- 8.1.4. Ion Implant

- 8.1.5. Diffusion Equipment Parts

- 8.1.6. CMP Equipment Parts

- 8.1.7. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. 300mm Equipment Parts

- 8.2.2. 200mm Equipment Parts

- 8.2.3. 150mm and Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Precision Cleaning For Semiconductor Equipment Parts Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Semiconductor Etching Equipment Parts

- 9.1.2. Semiconductor Thin Film (CVD/PVD)

- 9.1.3. Lithography Machines

- 9.1.4. Ion Implant

- 9.1.5. Diffusion Equipment Parts

- 9.1.6. CMP Equipment Parts

- 9.1.7. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. 300mm Equipment Parts

- 9.2.2. 200mm Equipment Parts

- 9.2.3. 150mm and Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Precision Cleaning For Semiconductor Equipment Parts Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Semiconductor Etching Equipment Parts

- 10.1.2. Semiconductor Thin Film (CVD/PVD)

- 10.1.3. Lithography Machines

- 10.1.4. Ion Implant

- 10.1.5. Diffusion Equipment Parts

- 10.1.6. CMP Equipment Parts

- 10.1.7. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. 300mm Equipment Parts

- 10.2.2. 200mm Equipment Parts

- 10.2.3. 150mm and Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 UCT (Ultra Clean Holdings Inc)

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Kurita (Pentagon Technologies)

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Enpro Industries (LeanTeq and NxEdge)

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 TOCALO Co. Ltd.

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Mitsubishi Chemical (Cleanpart)

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 KoMiCo

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Cinos

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Hansol IONES

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 WONIK QnC

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Dftech

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Frontken Corporation Berhad

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 KERTZ HIGH TECH

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Hung Jie Technology Corporation

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Shih Her Technology

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 HTCSolar

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Persys Group

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 MSR-FSR LLC

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Value Engineering Co. Ltd

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Neutron Technology Enterprise

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Ferrotec (Anhui) Technology Development Co. Ltd

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Jiangsu Kaiweitesi Semiconductor Technology Co. Ltd.

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 HCUT Co. Ltd

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 Suzhou Ever Distant Technology

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 Chongqing Genori Technology Co. Ltd

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.25 GRAND HITEK

- 11.2.25.1. Overview

- 11.2.25.2. Products

- 11.2.25.3. SWOT Analysis

- 11.2.25.4. Recent Developments

- 11.2.25.5. Financials (Based on Availability)

- 11.2.1 UCT (Ultra Clean Holdings Inc)

List of Figures

- Figure 1: Global Precision Cleaning For Semiconductor Equipment Parts Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Precision Cleaning For Semiconductor Equipment Parts Revenue (million), by Application 2024 & 2032

- Figure 3: North America Precision Cleaning For Semiconductor Equipment Parts Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Precision Cleaning For Semiconductor Equipment Parts Revenue (million), by Type 2024 & 2032

- Figure 5: North America Precision Cleaning For Semiconductor Equipment Parts Revenue Share (%), by Type 2024 & 2032

- Figure 6: North America Precision Cleaning For Semiconductor Equipment Parts Revenue (million), by Country 2024 & 2032

- Figure 7: North America Precision Cleaning For Semiconductor Equipment Parts Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Precision Cleaning For Semiconductor Equipment Parts Revenue (million), by Application 2024 & 2032

- Figure 9: South America Precision Cleaning For Semiconductor Equipment Parts Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Precision Cleaning For Semiconductor Equipment Parts Revenue (million), by Type 2024 & 2032

- Figure 11: South America Precision Cleaning For Semiconductor Equipment Parts Revenue Share (%), by Type 2024 & 2032

- Figure 12: South America Precision Cleaning For Semiconductor Equipment Parts Revenue (million), by Country 2024 & 2032

- Figure 13: South America Precision Cleaning For Semiconductor Equipment Parts Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Precision Cleaning For Semiconductor Equipment Parts Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Precision Cleaning For Semiconductor Equipment Parts Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Precision Cleaning For Semiconductor Equipment Parts Revenue (million), by Type 2024 & 2032

- Figure 17: Europe Precision Cleaning For Semiconductor Equipment Parts Revenue Share (%), by Type 2024 & 2032

- Figure 18: Europe Precision Cleaning For Semiconductor Equipment Parts Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Precision Cleaning For Semiconductor Equipment Parts Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Precision Cleaning For Semiconductor Equipment Parts Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Precision Cleaning For Semiconductor Equipment Parts Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Precision Cleaning For Semiconductor Equipment Parts Revenue (million), by Type 2024 & 2032

- Figure 23: Middle East & Africa Precision Cleaning For Semiconductor Equipment Parts Revenue Share (%), by Type 2024 & 2032

- Figure 24: Middle East & Africa Precision Cleaning For Semiconductor Equipment Parts Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Precision Cleaning For Semiconductor Equipment Parts Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Precision Cleaning For Semiconductor Equipment Parts Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Precision Cleaning For Semiconductor Equipment Parts Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Precision Cleaning For Semiconductor Equipment Parts Revenue (million), by Type 2024 & 2032

- Figure 29: Asia Pacific Precision Cleaning For Semiconductor Equipment Parts Revenue Share (%), by Type 2024 & 2032

- Figure 30: Asia Pacific Precision Cleaning For Semiconductor Equipment Parts Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Precision Cleaning For Semiconductor Equipment Parts Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Precision Cleaning For Semiconductor Equipment Parts Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Precision Cleaning For Semiconductor Equipment Parts Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Precision Cleaning For Semiconductor Equipment Parts Revenue million Forecast, by Type 2019 & 2032

- Table 4: Global Precision Cleaning For Semiconductor Equipment Parts Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Precision Cleaning For Semiconductor Equipment Parts Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Precision Cleaning For Semiconductor Equipment Parts Revenue million Forecast, by Type 2019 & 2032

- Table 7: Global Precision Cleaning For Semiconductor Equipment Parts Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Precision Cleaning For Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Precision Cleaning For Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Precision Cleaning For Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Precision Cleaning For Semiconductor Equipment Parts Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Precision Cleaning For Semiconductor Equipment Parts Revenue million Forecast, by Type 2019 & 2032

- Table 13: Global Precision Cleaning For Semiconductor Equipment Parts Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Precision Cleaning For Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Precision Cleaning For Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Precision Cleaning For Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Precision Cleaning For Semiconductor Equipment Parts Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Precision Cleaning For Semiconductor Equipment Parts Revenue million Forecast, by Type 2019 & 2032

- Table 19: Global Precision Cleaning For Semiconductor Equipment Parts Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Precision Cleaning For Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Precision Cleaning For Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Precision Cleaning For Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Precision Cleaning For Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Precision Cleaning For Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Precision Cleaning For Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Precision Cleaning For Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Precision Cleaning For Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Precision Cleaning For Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Precision Cleaning For Semiconductor Equipment Parts Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Precision Cleaning For Semiconductor Equipment Parts Revenue million Forecast, by Type 2019 & 2032

- Table 31: Global Precision Cleaning For Semiconductor Equipment Parts Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Precision Cleaning For Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Precision Cleaning For Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Precision Cleaning For Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Precision Cleaning For Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Precision Cleaning For Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Precision Cleaning For Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Precision Cleaning For Semiconductor Equipment Parts Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Precision Cleaning For Semiconductor Equipment Parts Revenue million Forecast, by Type 2019 & 2032

- Table 40: Global Precision Cleaning For Semiconductor Equipment Parts Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Precision Cleaning For Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Precision Cleaning For Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Precision Cleaning For Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Precision Cleaning For Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Precision Cleaning For Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Precision Cleaning For Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Precision Cleaning For Semiconductor Equipment Parts Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Precision Cleaning For Semiconductor Equipment Parts?

The projected CAGR is approximately 6.7%.

2. Which companies are prominent players in the Precision Cleaning For Semiconductor Equipment Parts?

Key companies in the market include UCT (Ultra Clean Holdings, Inc), Kurita (Pentagon Technologies), Enpro Industries (LeanTeq and NxEdge), TOCALO Co., Ltd., Mitsubishi Chemical (Cleanpart), KoMiCo, Cinos, Hansol IONES, WONIK QnC, Dftech, Frontken Corporation Berhad, KERTZ HIGH TECH, Hung Jie Technology Corporation, Shih Her Technology, HTCSolar, Persys Group, MSR-FSR LLC, Value Engineering Co., Ltd, Neutron Technology Enterprise, Ferrotec (Anhui) Technology Development Co., Ltd, Jiangsu Kaiweitesi Semiconductor Technology Co., Ltd., HCUT Co., Ltd, Suzhou Ever Distant Technology, Chongqing Genori Technology Co., Ltd, GRAND HITEK.

3. What are the main segments of the Precision Cleaning For Semiconductor Equipment Parts?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 1489 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Precision Cleaning For Semiconductor Equipment Parts," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Precision Cleaning For Semiconductor Equipment Parts report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Precision Cleaning For Semiconductor Equipment Parts?

To stay informed about further developments, trends, and reports in the Precision Cleaning For Semiconductor Equipment Parts, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence