Key Insights

The global Recyclable PET Food Plastic Packaging market is poised for significant expansion, driven by heightened consumer consciousness around environmental sustainability and supportive regulatory frameworks promoting eco-friendly alternatives. The market, valued at approximately $91.03 billion in the base year 2025, is projected to achieve a robust CAGR of 8.89%. This growth is underpinned by the increasing demand for premium, convenient, and ethically sourced pet food. Key factors propelling this trend include the humanization of pets and a rising preference for packaging that ensures optimal freshness and extended shelf life. The substantial growth of the overall pet food industry, especially in emerging markets, further amplifies the need for specialized and sustainable packaging solutions.

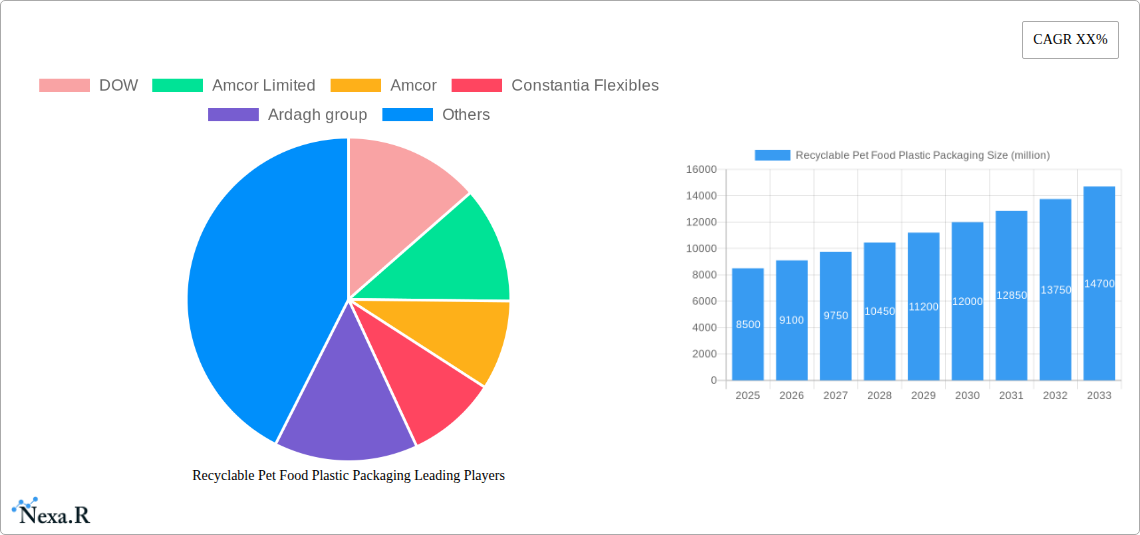

Recyclable Pet Food Plastic Packaging Market Size (In Billion)

The market is predominantly segmented by application into Cat Food and Dog Food packaging, reflecting the substantial volume of these product categories. The "Others" segment, covering packaging for aquatic, avian, and small animal foods, also exhibits promising growth. Regarding packaging types, both Dry and Wet Pet Food packaging bags are critical, with ongoing advancements in material science yielding high-performance, recyclable options. Leading companies such as DOW, Amcor Limited, and Constantia Flexibles are spearheading innovation through significant investments in R&D for sustainable materials and manufacturing processes. Challenges include the potentially higher costs of certain recyclable materials and the necessity for enhanced recycling infrastructure. Nevertheless, the prevailing shift towards a circular economy and the growing consumer preference for environmentally responsible brands are expected to sustain market growth.

Recyclable Pet Food Plastic Packaging Company Market Share

Recyclable Pet Food Plastic Packaging Market Report

Unlock the future of sustainable pet food packaging with our comprehensive market analysis. This report provides an in-depth look at the rapidly evolving recyclable pet food plastic packaging industry, exploring market dynamics, growth trends, regional dominance, product innovations, and the key players shaping its trajectory. With increasing consumer demand for eco-friendly solutions and stringent regulatory pressures, understanding this market is crucial for businesses aiming for growth and sustainability.

Recyclable Pet Food Plastic Packaging Market Dynamics & Structure

The recyclable pet food plastic packaging market exhibits a moderately concentrated structure, with key players like Amcor Limited, Constantia Flexibles, and Sonoco Products Co holding significant market shares. Technological innovation is a primary driver, with advancements in recyclable barrier films, mono-material solutions, and chemical recycling technologies enabling greater sustainability without compromising product integrity. Regulatory frameworks, particularly in North America and Europe, are increasingly mandating the use of recyclable packaging, pushing manufacturers to adopt more sustainable practices. Competitive product substitutes, such as paper-based packaging and compostable alternatives, are emerging but often face challenges in terms of cost, performance, and scalability for dog food packaging and cat food packaging. End-user demographics are shifting, with a growing segment of environmentally conscious pet owners willing to pay a premium for sustainable products. Mergers and acquisitions (M&A) are a notable trend, as larger companies seek to consolidate their market position and acquire innovative technologies. For instance, recent M&A activity has seen strategic acquisitions aimed at expanding capabilities in wet pet food packaging bags and dry pet food packaging bags.

- Market Concentration: Moderate, with 5-7 major players accounting for over 50% of the market share.

- Technological Innovation Drivers: Development of high-barrier recyclable films, advancement in mechanical and chemical recycling processes for PET and PP.

- Regulatory Frameworks: Increasing EPR (Extended Producer Responsibility) schemes and single-use plastic bans in key developed economies.

- Competitive Product Substitutes: Paper-based pouches, glass containers, metal cans (though less prevalent for dry food).

- End-User Demographics: Growing segment of eco-conscious millennials and Gen Z pet owners.

- M&A Trends: Focus on acquiring companies with advanced recycling technologies and expanding geographical reach. Estimated deal volume in the last two years: 8-10 significant transactions.

Recyclable Pet Food Plastic Packaging Growth Trends & Insights

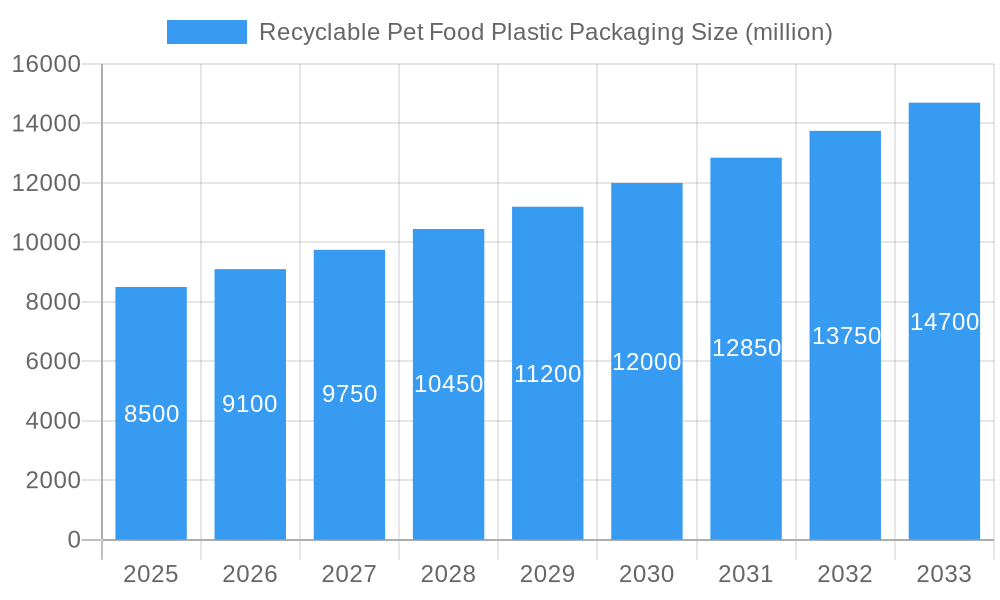

The recyclable pet food plastic packaging market is poised for robust growth, projected to expand from an estimated $15,500 million in 2025 to $22,800 million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 5.2% during the forecast period. This expansion is fueled by a confluence of accelerating factors, including escalating global pet ownership, a heightened consumer awareness regarding environmental sustainability, and progressive governmental policies advocating for circular economy principles. The shift towards premium and specialized pet food products also necessitates advanced packaging solutions that can maintain product freshness and appeal, further stimulating demand for innovative recyclable materials.

Technological advancements play a pivotal role in shaping the growth trajectory. The development of advanced barrier properties in mono-material plastic packaging for cat food and dog food has been a significant disruption, offering performance comparable to traditional multi-layer laminates while ensuring recyclability. Furthermore, innovations in recyclable PET packaging and recyclable PP packaging are enabling the creation of more sophisticated and aesthetically pleasing packaging formats for both dry pet food packaging bags and wet pet food packaging bags. The penetration of these recyclable solutions is increasing across all market segments, driven by a growing understanding of their long-term economic and environmental benefits.

Consumer behavior is a critical influencer. A substantial and growing segment of pet owners are actively seeking out brands that demonstrate a commitment to environmental responsibility. This conscious consumerism translates directly into purchasing decisions, rewarding companies that offer products with recyclable packaging and transparent sustainability claims. The "green premium" is becoming increasingly accepted, with consumers willing to invest more in products that align with their values. This trend is particularly pronounced in developed markets, but its influence is spreading globally. The Others segment, which includes specialized pet foods, treats, and supplements, is also witnessing increased demand for sustainable packaging, mirroring the trends in core cat food and dog food markets.

The base year of 2025 represents a critical inflection point, with significant investments in research and development and the scaling of recycling infrastructure expected to accelerate adoption rates. The historical period (2019-2024) has laid the groundwork, characterized by initial market exploration, early regulatory nudges, and growing consumer interest. The forecast period (2025-2033) will see these trends mature, with recyclable pet food plastic packaging becoming the norm rather than the exception. The market penetration for recyclable solutions is estimated to grow from around 35% in 2025 to over 65% by 2033. Disruptions are expected to continue, with the potential for breakthroughs in advanced recycling technologies to further enhance the appeal and feasibility of plastic packaging in a circular economy.

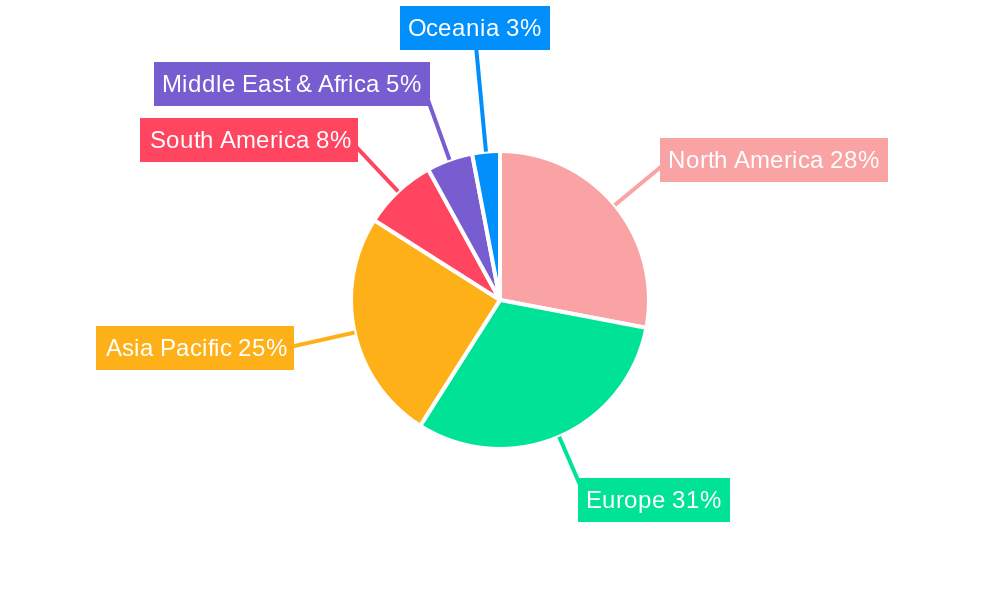

Dominant Regions, Countries, or Segments in Recyclable Pet Food Plastic Packaging

The North America region is currently emerging as a dominant force in the recyclable pet food plastic packaging market, driven by a potent combination of factors including high pet ownership rates, a deeply ingrained consumer preference for sustainability, and proactive regulatory initiatives. The United States, in particular, is a significant market, characterized by a large and affluent pet owner demographic that is increasingly prioritizing eco-friendly products. Government policies, such as extended producer responsibility (EPR) programs and mandates aimed at reducing plastic waste, are creating a favorable environment for the adoption of recyclable pet food plastic packaging. The presence of major pet food manufacturers and packaging converters, including Amcor Limited, Sonoco Products Co, and HUHTAMAKI, further solidifies North America's leadership.

From an application perspective, Dog Food represents the largest segment within the recyclable pet food plastic packaging market. This dominance is attributable to the sheer volume of dog food consumed globally and the increasing demand for premium and specialized dog food options that require robust and appealing packaging. The Cat Food segment follows closely, also experiencing significant growth due to similar trends in pet ownership and consumer preferences. The Others segment, encompassing treats, supplements, and specialized diets, is also witnessing a notable expansion, driven by innovation and niche market demands for sustainable packaging solutions.

In terms of packaging types, Dry Pet Food Packaging Bags currently command the largest market share. These bags, often made from flexible plastic films, are integral to preserving the freshness and extending the shelf life of dry kibble. The development of advanced mono-material dry pet food packaging bags that are both recyclable and offer superior barrier properties is a key driver in this segment. Wet Pet Food Packaging Bags, while historically relying on more traditional materials like pouches with aluminum layers, are also rapidly transitioning towards recyclable alternatives, as manufacturers and consumers alike seek sustainable options for this product category. The market share for Dry Pet Food Packaging Bags is estimated at 65% in 2025.

Economic policies, such as incentives for using recycled content and investments in recycling infrastructure, are crucial for fostering growth. Infrastructure development, including advanced sorting and recycling facilities, is critical for the successful implementation of recyclable pet food plastic packaging. The growth potential in North America is substantial, driven by ongoing technological advancements and increasing consumer demand for sustainable products. For instance, the market share of recyclable packaging in the US dog food segment alone is projected to reach over 70% by 2030.

- Leading Region: North America (estimated market share: 40% in 2025).

- Dominant Country: United States (significant contributor to North American market share).

- Leading Application Segment: Dog Food (estimated market share: 55% in 2025).

- Second Leading Application Segment: Cat Food (estimated market share: 30% in 2025).

- Dominant Packaging Type: Dry Pet Food Packaging Bags (estimated market share: 65% in 2025).

- Key Drivers: High pet ownership, consumer demand for sustainability, supportive regulatory frameworks, presence of major industry players.

- Growth Potential: Significant, fueled by continued innovation and increasing consumer awareness.

Recyclable Pet Food Plastic Packaging Product Landscape

The recyclable pet food plastic packaging product landscape is characterized by continuous innovation aimed at balancing performance, sustainability, and aesthetics. Manufacturers are increasingly focusing on mono-material solutions, primarily utilizing Polyethylene (PE) and Polypropylene (PP), which are more readily recyclable than traditional multi-layer laminates. These advancements enable the creation of flexible packaging with enhanced barrier properties against moisture, oxygen, and light, crucial for maintaining the freshness and nutritional value of dog food and cat food. Unique selling propositions include improved puncture resistance, enhanced printability for brand differentiation, and a reduced environmental footprint. Technological advancements in resin formulations and processing techniques are enabling higher percentages of post-consumer recycled (PCR) content to be incorporated without compromising structural integrity or food safety.

Key Drivers, Barriers & Challenges in Recyclable Pet Food Plastic Packaging

Key Drivers: The recyclable pet food plastic packaging market is propelled by several key drivers. Growing consumer demand for sustainable products is paramount, with pet owners actively seeking brands that align with their environmental values. Stringent government regulations and initiatives, such as plastic reduction targets and EPR schemes, are mandating a shift towards recyclable packaging solutions. Technological advancements in recyclable materials and recycling infrastructure are making these solutions more viable and cost-effective. Furthermore, the increasing premiumization of pet food necessitates high-quality packaging that preserves product integrity and brand appeal.

Barriers & Challenges: Despite the positive outlook, the market faces significant barriers and challenges. The cost of implementing new recyclable materials and retooling production lines can be substantial for manufacturers. The availability and scalability of high-quality recycled feedstock remain a concern for consistent production. Inconsistent recycling infrastructure and consumer awareness regarding proper disposal methods can hinder the actual recyclability of materials. The performance limitations of some recyclable materials compared to traditional multi-layer packaging, particularly in terms of barrier properties for highly sensitive products, also pose a challenge. Supply chain disruptions and the volatility of raw material prices can further impact profitability and market stability.

Emerging Opportunities in Recyclable Pet Food Plastic Packaging

Emerging opportunities within the recyclable pet food plastic packaging market lie in the development of advanced chemical recycling technologies that can process a wider range of plastic waste, including complex multi-layer films, into high-quality new materials. The untapped potential in emerging economies, where pet ownership is rising and environmental consciousness is gaining traction, presents a significant growth avenue. Innovative design solutions for shelf-ready recyclable packaging that enhance consumer appeal and ease of use are also gaining traction. Furthermore, the integration of digital technologies for enhanced traceability and consumer engagement regarding the recyclability of packaging offers a unique competitive advantage.

Growth Accelerators in the Recyclable Pet Food Plastic Packaging Industry

Several catalysts are accelerating growth in the recyclable pet food plastic packaging industry. Strategic partnerships between pet food brands and packaging manufacturers are fostering collaborative innovation and faster market adoption of sustainable solutions. Significant investments in research and development of novel barrier technologies for mono-material films are overcoming previous performance limitations. Government incentives and supportive policies encouraging the use of recycled content and the development of circular economy models are playing a crucial role. The increasing corporate sustainability commitments by major pet food companies are also driving demand for recyclable packaging across their product portfolios.

Key Players Shaping the Recyclable Pet Food Plastic Packaging Market

- DOW

- Amcor Limited

- Amcor

- Constantia Flexibles

- Ardagh group

- Coveris

- Sonoco Products Co

- Mondi Group

- HUHTAMAKI

- Printpack

- Winpak

- ProAmpac

- ORG Technology

- BOBST

Notable Milestones in Recyclable Pet Food Plastic Packaging Sector

- 2019/2020: Increased regulatory focus on single-use plastics in major European markets, driving R&D for recyclable alternatives.

- 2020/2021: Launch of several high-barrier mono-material PET and PP films suitable for wet and dry pet food by key players like Amcor and DOW.

- 2021/2022: Significant M&A activity as larger companies acquire specialized recyclable packaging technology providers.

- 2022/2023: Growing consumer demand for "eco-friendly" labeled pet food products, leading to increased adoption of recyclable packaging by brands.

- 2023/2024: Advancements in chemical recycling technologies show promise for creating a truly circular economy for plastic pet food packaging.

- 2024: Major pet food brands set ambitious targets for 100% recyclable or reusable packaging by 2030, accelerating market demand.

In-Depth Recyclable Pet Food Plastic Packaging Market Outlook

The recyclable pet food plastic packaging market outlook is exceptionally positive, driven by enduring growth accelerators. The sustained rise in global pet ownership, coupled with an intensifying consumer demand for environmentally responsible products, will continue to be the primary engine of market expansion. Technological breakthroughs in mono-material barrier films and advanced recycling technologies are expected to further solidify the viability and performance of recyclable plastic packaging, addressing previous limitations. Strategic collaborations between packaging innovators and leading pet food manufacturers, alongside supportive government policies and corporate sustainability mandates, will foster a dynamic and growth-oriented market. The market is poised to witness significant penetration of recyclable packaging solutions across all segments, making it an indispensable component of the future pet food industry.

Recyclable Pet Food Plastic Packaging Segmentation

-

1. Application

- 1.1. Cat Food

- 1.2. Dog Food

- 1.3. Cat Litter

- 1.4. Others

-

2. Types

- 2.1. Dry Pet Food Packaging Bags

- 2.2. Wet Pet Food Packaging Bags

Recyclable Pet Food Plastic Packaging Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Recyclable Pet Food Plastic Packaging Regional Market Share

Geographic Coverage of Recyclable Pet Food Plastic Packaging

Recyclable Pet Food Plastic Packaging REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.89% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Recyclable Pet Food Plastic Packaging Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Cat Food

- 5.1.2. Dog Food

- 5.1.3. Cat Litter

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Dry Pet Food Packaging Bags

- 5.2.2. Wet Pet Food Packaging Bags

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Recyclable Pet Food Plastic Packaging Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Cat Food

- 6.1.2. Dog Food

- 6.1.3. Cat Litter

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Dry Pet Food Packaging Bags

- 6.2.2. Wet Pet Food Packaging Bags

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Recyclable Pet Food Plastic Packaging Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Cat Food

- 7.1.2. Dog Food

- 7.1.3. Cat Litter

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Dry Pet Food Packaging Bags

- 7.2.2. Wet Pet Food Packaging Bags

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Recyclable Pet Food Plastic Packaging Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Cat Food

- 8.1.2. Dog Food

- 8.1.3. Cat Litter

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Dry Pet Food Packaging Bags

- 8.2.2. Wet Pet Food Packaging Bags

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Recyclable Pet Food Plastic Packaging Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Cat Food

- 9.1.2. Dog Food

- 9.1.3. Cat Litter

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Dry Pet Food Packaging Bags

- 9.2.2. Wet Pet Food Packaging Bags

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Recyclable Pet Food Plastic Packaging Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Cat Food

- 10.1.2. Dog Food

- 10.1.3. Cat Litter

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Dry Pet Food Packaging Bags

- 10.2.2. Wet Pet Food Packaging Bags

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 DOW

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Amcor Limited

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Amcor

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Constantia Flexibles

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Ardagh group

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Coveris

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Sonoco Products Co

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Mondi Group

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 HUHTAMAKI

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Printpack

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Winpak

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 ProAmpac

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 ORG Technology

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 BOBST

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.1 DOW

List of Figures

- Figure 1: Global Recyclable Pet Food Plastic Packaging Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Recyclable Pet Food Plastic Packaging Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Recyclable Pet Food Plastic Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Recyclable Pet Food Plastic Packaging Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Recyclable Pet Food Plastic Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Recyclable Pet Food Plastic Packaging Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Recyclable Pet Food Plastic Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Recyclable Pet Food Plastic Packaging Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Recyclable Pet Food Plastic Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Recyclable Pet Food Plastic Packaging Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Recyclable Pet Food Plastic Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Recyclable Pet Food Plastic Packaging Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Recyclable Pet Food Plastic Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Recyclable Pet Food Plastic Packaging Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Recyclable Pet Food Plastic Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Recyclable Pet Food Plastic Packaging Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Recyclable Pet Food Plastic Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Recyclable Pet Food Plastic Packaging Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Recyclable Pet Food Plastic Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Recyclable Pet Food Plastic Packaging Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Recyclable Pet Food Plastic Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Recyclable Pet Food Plastic Packaging Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Recyclable Pet Food Plastic Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Recyclable Pet Food Plastic Packaging Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Recyclable Pet Food Plastic Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Recyclable Pet Food Plastic Packaging Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Recyclable Pet Food Plastic Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Recyclable Pet Food Plastic Packaging Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Recyclable Pet Food Plastic Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Recyclable Pet Food Plastic Packaging Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Recyclable Pet Food Plastic Packaging Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Recyclable Pet Food Plastic Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Recyclable Pet Food Plastic Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Recyclable Pet Food Plastic Packaging Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Recyclable Pet Food Plastic Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Recyclable Pet Food Plastic Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Recyclable Pet Food Plastic Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Recyclable Pet Food Plastic Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Recyclable Pet Food Plastic Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Recyclable Pet Food Plastic Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Recyclable Pet Food Plastic Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Recyclable Pet Food Plastic Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Recyclable Pet Food Plastic Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Recyclable Pet Food Plastic Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Recyclable Pet Food Plastic Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Recyclable Pet Food Plastic Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Recyclable Pet Food Plastic Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Recyclable Pet Food Plastic Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Recyclable Pet Food Plastic Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Recyclable Pet Food Plastic Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Recyclable Pet Food Plastic Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Recyclable Pet Food Plastic Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Recyclable Pet Food Plastic Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Recyclable Pet Food Plastic Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Recyclable Pet Food Plastic Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Recyclable Pet Food Plastic Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Recyclable Pet Food Plastic Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Recyclable Pet Food Plastic Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Recyclable Pet Food Plastic Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Recyclable Pet Food Plastic Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Recyclable Pet Food Plastic Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Recyclable Pet Food Plastic Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Recyclable Pet Food Plastic Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Recyclable Pet Food Plastic Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Recyclable Pet Food Plastic Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Recyclable Pet Food Plastic Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Recyclable Pet Food Plastic Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Recyclable Pet Food Plastic Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Recyclable Pet Food Plastic Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Recyclable Pet Food Plastic Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Recyclable Pet Food Plastic Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Recyclable Pet Food Plastic Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Recyclable Pet Food Plastic Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Recyclable Pet Food Plastic Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Recyclable Pet Food Plastic Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Recyclable Pet Food Plastic Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Recyclable Pet Food Plastic Packaging Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Recyclable Pet Food Plastic Packaging?

The projected CAGR is approximately 8.89%.

2. Which companies are prominent players in the Recyclable Pet Food Plastic Packaging?

Key companies in the market include DOW, Amcor Limited, Amcor, Constantia Flexibles, Ardagh group, Coveris, Sonoco Products Co, Mondi Group, HUHTAMAKI, Printpack, Winpak, ProAmpac, ORG Technology, BOBST.

3. What are the main segments of the Recyclable Pet Food Plastic Packaging?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 91.03 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Recyclable Pet Food Plastic Packaging," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Recyclable Pet Food Plastic Packaging report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Recyclable Pet Food Plastic Packaging?

To stay informed about further developments, trends, and reports in the Recyclable Pet Food Plastic Packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence