Key Insights

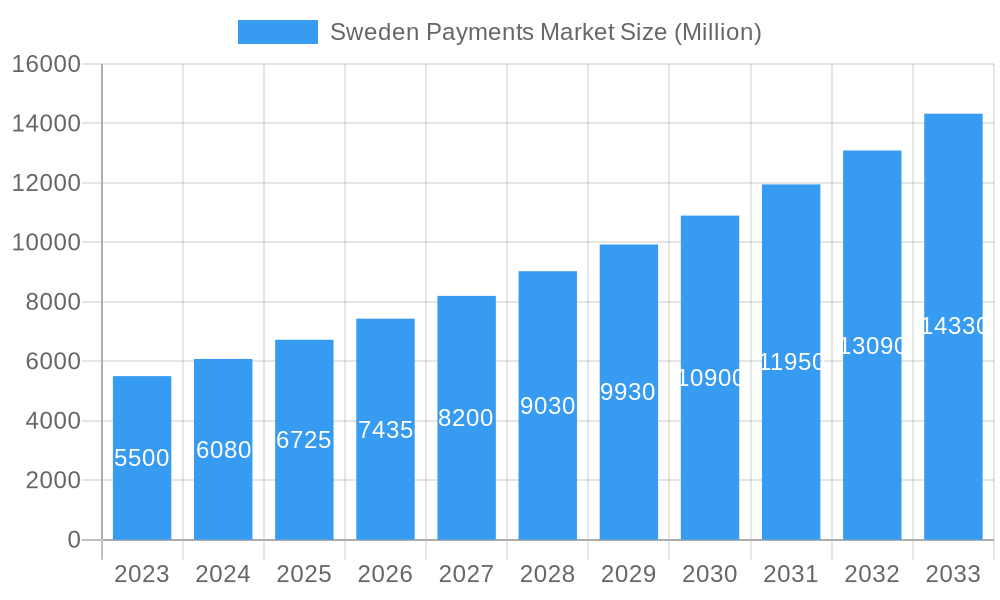

The Sweden Payments Market is projected for substantial expansion, forecasted to reach a market size of 2.01 billion by 2025, driven by a significant Compound Annual Growth Rate (CAGR) of 38.47%. This robust growth is fueled by the accelerating adoption of digital payment methods, enhanced by consumer demand for convenience and security. The thriving e-commerce sector, alongside governmental and financial institution initiatives promoting cashless transactions, fosters payment innovation. Advancements in payment technologies, including mobile wallets and modern POS systems, are improving user experience and increasing transaction volumes. The retail sector is leading the transition to digital and card payments, with entertainment and healthcare sectors also rapidly adopting these solutions. The "Others" category for online sales likely includes in-app purchases and subscription services, contributing to market growth.

Sweden Payments Market Market Size (In Billion)

Potential growth restraints include the necessity for stringent cybersecurity to maintain consumer trust, evolving regulatory landscapes, and the continued preference for cash in specific segments. Despite these, the digital transformation trend is dominant. Key market players such as Stripe, Klarna Bank AB, and WorldPay are driving innovation with solutions addressing evolving consumer and business needs. The market is characterized by intense competition and strategic alliances focused on service expansion and market penetration. The ongoing development of secure, user-friendly, and diverse payment options is expected to outweigh challenges, ensuring the Sweden Payments Market's continued vibrancy and growth.

Sweden Payments Market Company Market Share

This detailed analysis provides an SEO-optimized overview of the Sweden Payments Market, highlighting its size, growth trajectory, and key dynamics for industry stakeholders.

Sweden Payments Market: In-Depth Analysis & Future Outlook (2019-2033)

Unlock the potential of the dynamic Swedish payments landscape with our comprehensive market report. This in-depth analysis provides critical insights into the evolution of payment modes, end-user industries, and key players shaping Sweden's digital transaction future. Explore growth trajectories, technological disruptions, and emerging opportunities within the parent market and its child segments. This report is an indispensable resource for payment service providers, financial institutions, technology vendors, and investors seeking to navigate and capitalize on the rapidly expanding Swedish payments sector.

Key Report Features:

- Study Period: 2019–2033

- Base Year: 2025

- Estimated Year: 2025

- Forecast Period: 2025–2033

- Historical Period: 2019–2024

- Values Presented in: Million Units

Sweden Payments Market Market Dynamics & Structure

The Swedish payments market is characterized by a high degree of technological adoption and a competitive landscape driven by innovation and regulatory support. Market concentration is observed among established financial institutions and nimble fintech players, with significant market share held by providers offering seamless digital experiences. Technological innovation is a primary driver, fueled by advancements in mobile payments, contactless technology, and open banking initiatives, fostering a more inclusive and efficient payment ecosystem. Regulatory frameworks, such as PSD2, have further spurred competition and innovation by encouraging third-party access to financial data, leading to a surge in new payment solutions. Competitive product substitutes are plentiful, ranging from traditional card payments to digital wallets and instant payment systems, forcing providers to continuously enhance their offerings. End-user demographics, particularly the digitally savvy Swedish population, are increasingly demanding convenient, secure, and fast payment methods, influencing product development and adoption rates. Mergers and acquisitions (M&A) trends, while not as prevalent as in larger markets, are indicative of strategic consolidations aimed at expanding market reach and technological capabilities.

- Market Concentration: Dominated by a mix of large banks and specialized fintechs, with a trend towards platform consolidation.

- Technological Innovation: Driven by mobile-first strategies, NFC technology, and open banking APIs, fostering real-time payments.

- Regulatory Framework: PSD2 and national initiatives promoting digital payments create a fertile ground for innovation and competition.

- Competitive Product Substitutes: Wide array of options from card payments and mobile wallets to direct bank transfers and QR-code solutions.

- End-User Demographics: High digital penetration and a preference for frictionless, mobile-centric transactions.

- M&A Trends: Strategic acquisitions focused on enhancing service portfolios and expanding customer bases.

Sweden Payments Market Growth Trends & Insights

The Swedish payments market is poised for substantial growth, driven by a confluence of evolving consumer behaviors, robust technological advancements, and supportive economic policies. The market size is projected to expand at a significant Compound Annual Growth Rate (CAGR) during the forecast period, reflecting a sustained increase in digital transaction volumes and values. This expansion is fueled by the high adoption rates of digital payment methods among the Swedish population, who have embraced contactless payments, mobile wallets, and instant payment systems with enthusiasm. Technological disruptions, such as the proliferation of QR-code payments and the increasing integration of payments into non-traditional platforms, are further reshaping the market. Consumer behavior shifts are a key indicator, with a growing preference for convenience, security, and personalized payment experiences. The demand for seamless online and offline transactions continues to rise, prompting businesses to invest in advanced payment infrastructure. The penetration of smartphones and reliable internet connectivity across Sweden provides a solid foundation for the continued adoption of digital payment solutions, pushing traditional cash transactions further into decline. The market's resilience and adaptability to new technologies underscore its potential for sustained and dynamic growth.

Dominant Regions, Countries, or Segments in Sweden Payments Market

The Swedish payments market demonstrates a clear dominance in specific segments, particularly within the Point of Sale (POS) and Online Sale modes of payment, driven by the Retail and Entertainment end-user industries. Within the Point of Sale segment, Card Pay and Digital Wallet (includes Mobile Wallets) are the leading modes. Card payments have a deeply ingrained presence, supported by widespread acceptance infrastructure and consumer familiarity. However, the rapid adoption of mobile wallets, facilitated by services like Swish and integrated into consumer devices, is rapidly closing the gap and, in some instances, surpassing card transactions for everyday purchases due to their convenience and speed. The surge in e-commerce and the increasing digitalization of the retail sector are the primary catalysts for the dominance of these POS payment methods.

The Online Sale segment is heavily influenced by the Others category, which encompasses a wide array of innovative online payment solutions, including direct bank transfers, Buy Now Pay Later (BNPL) services, and integrated payment gateways. The Retail end-user industry is a significant contributor to this dominance, with online retail sales experiencing exponential growth. Consumers increasingly prefer the convenience of purchasing goods and services online, demanding secure and swift payment options. The Entertainment sector, including streaming services, gaming, and event ticketing, also contributes substantially to online payment volumes, often leveraging digital wallets and BNPL for recurring subscriptions and impulse purchases.

Geographically, the market is largely unified due to Sweden's excellent digital infrastructure and high internet penetration nationwide. However, urban centers like Stockholm, Gothenburg, and Malmö tend to exhibit higher adoption rates for cutting-edge payment technologies and a greater volume of digital transactions, mirroring global trends where metropolitan areas often lead in fintech adoption. Factors contributing to this dominance include a higher concentration of businesses investing in advanced payment technologies, a larger digitally active population, and greater access to diverse payment service providers. The ongoing development of contactless technology and the increasing use of smartphones for payments further solidify the lead of card and digital wallet payments in both online and offline retail environments.

- Leading Mode of Payment (POS): Card Pay and Digital Wallet (including Mobile Wallets) due to convenience and widespread infrastructure.

- Leading Mode of Payment (Online): Integrated payment gateways and direct bank transfers, supported by BNPL solutions.

- Dominant End-User Industry: Retail, driven by robust e-commerce growth and in-store digital adoption.

- Key Growth Driver: Increasing consumer preference for digital, contactless, and mobile-first payment solutions.

- Geographic Concentration: Urban centers exhibit higher adoption of advanced payment technologies, mirroring global fintech trends.

Sweden Payments Market Product Landscape

The Swedish payments market is characterized by a dynamic product landscape marked by continuous innovation and a focus on user experience. Key product developments revolve around enhancing transaction speed, security, and convenience across various payment channels. This includes the evolution of contactless payment solutions, the integration of biometric authentication for mobile payments, and the development of sophisticated fraud detection systems. The rise of Buy Now Pay Later (BNPL) services and their seamless integration into e-commerce checkouts represents a significant product innovation, catering to consumer demand for flexible payment options. Furthermore, the application of AI and machine learning in payment platforms is enabling personalized payment experiences and more effective risk management. Performance metrics consistently highlight improved transaction success rates, reduced chargebacks, and enhanced customer satisfaction as key indicators of successful product deployment.

Key Drivers, Barriers & Challenges in Sweden Payments Market

The Swedish payments market is propelled by several key drivers, including the high digital literacy of the population, strong government support for digitalization, and the widespread adoption of smartphones. Technological advancements in contactless payments and mobile wallets are creating frictionless transaction experiences. The increasing demand for instant payment solutions and the growing e-commerce sector further contribute to market expansion.

Key Drivers:

- High Digital Penetration: Extensive smartphone ownership and internet access across Sweden.

- Consumer Demand for Convenience: Preference for fast, secure, and easy payment methods.

- E-commerce Growth: Surging online retail activities driving digital transaction volumes.

- Government Initiatives: Supportive policies and infrastructure promoting digital payments.

Key Barriers & Challenges:

- Intense Competition: A crowded market with established players and emerging fintechs.

- Cybersecurity Concerns: The constant threat of data breaches and fraud requires robust security measures.

- Regulatory Compliance: Navigating evolving payment regulations and data privacy laws.

- Interoperability Issues: Ensuring seamless integration across diverse payment systems and platforms.

- Cost of Infrastructure Upgrade: High investment required for businesses to adopt and maintain advanced payment technologies.

Emerging Opportunities in Sweden Payments Market

Emerging opportunities in the Swedish payments market are abundant, particularly in niche segments and through the application of innovative technologies. The continued growth of cross-border e-commerce presents a significant avenue for payment providers to offer specialized international payment solutions. The integration of payments into the Internet of Things (IoT) devices, such as smart appliances and wearables, is an untapped area with substantial potential for automated and seamless transactions. Furthermore, the increasing demand for embedded finance solutions, where payment functionalities are integrated directly into non-financial platforms and applications, offers a substantial growth trajectory. The development of open banking-driven solutions that provide personalized financial management tools and payment options also represents a key opportunity, catering to a consumer base increasingly interested in holistic financial services.

Growth Accelerators in the Sweden Payments Market Industry

The Sweden payments market industry is experiencing significant growth acceleration driven by several key catalysts. Technological breakthroughs, particularly in areas like biometric authentication and AI-powered fraud detection, are enhancing both security and user experience, encouraging greater adoption of digital payments. Strategic partnerships between traditional financial institutions and innovative fintech companies are fostering the development of new, integrated payment solutions that leverage the strengths of both. Market expansion strategies, including the introduction of new payment services tailored to specific merchant needs or consumer demographics, are also playing a crucial role. The ongoing digitalization of businesses across all sectors, from small enterprises to large corporations, is creating a constant demand for efficient and modern payment processing capabilities, further fueling the industry's growth trajectory.

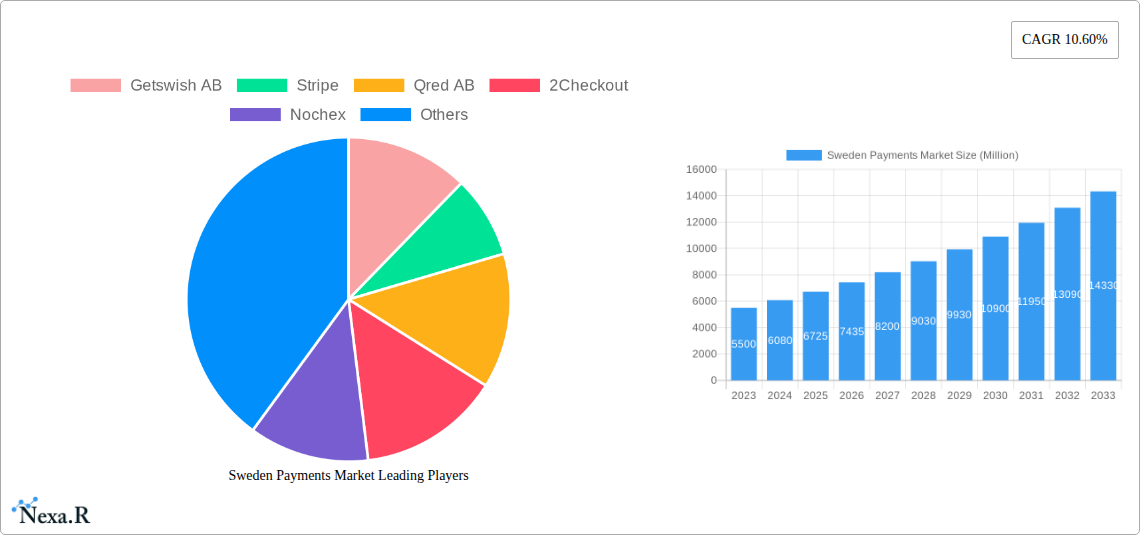

Key Players Shaping the Sweden Payments Market Market

- Getswish AB

- Stripe

- Qred AB

- 2Checkout

- Nochex

- Braintree

- QuickPay

- Klarna Bank AB

- WorldPay

- Wirecard

Notable Milestones in Sweden Payments Market Sector

- February 2022: Adyen joins Swish, expanding enterprise access to fast and secure Swish payments for approximately 8 million Swedes and over 300,000 companies connected to Swish via 12 banks.

- May 2022: PayPal's Point of Sale (POS) software solution enables sellers in the UK, Sweden, and the Netherlands to accept contactless payments on standard Android NFC smartphones or other mobile devices using Tap to Pay with Zettle, accessible via the PayPal Zettle Go app.

In-Depth Sweden Payments Market Market Outlook

The Sweden Payments Market is set for sustained expansion, driven by a robust combination of technological innovation and evolving consumer preferences. Growth accelerators, including the continued development of seamless mobile payment ecosystems, the increasing adoption of Buy Now Pay Later (BNPL) services, and the integration of payment solutions within various digital platforms, will shape the future landscape. The market's outlook is strongly positive, with significant potential in cross-border transactions and embedded finance. Strategic opportunities lie in catering to niche markets, enhancing cybersecurity measures, and leveraging open banking to provide personalized financial management tools. The Swedish market is well-positioned to embrace the next wave of payment evolution, promising a dynamic and lucrative environment for stakeholders.

Sweden Payments Market Segmentation

-

1. Mode of Payment

-

1.1. Point of Sale

- 1.1.1. Card Pay

- 1.1.2. Digital Wallet (includes Mobile Wallets)

- 1.1.3. Cash

- 1.1.4. Others

-

1.2. Online Sale

- 1.2.1. Others (

-

1.1. Point of Sale

-

2. End-user Industry

- 2.1. Retail

- 2.2. Entertainment

- 2.3. Healthcare

- 2.4. Hospitality

- 2.5. Other End-user Industries

Sweden Payments Market Segmentation By Geography

- 1. Sweden

Sweden Payments Market Regional Market Share

Geographic Coverage of Sweden Payments Market

Sweden Payments Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 38.47% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 5.1.1. Point of Sale

- 5.1.1.1. Card Pay

- 5.1.1.2. Digital Wallet (includes Mobile Wallets)

- 5.1.1.3. Cash

- 5.1.1.4. Others

- 5.1.2. Online Sale

- 5.1.2.1. Others (

- 5.1.1. Point of Sale

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Retail

- 5.2.2. Entertainment

- 5.2.3. Healthcare

- 5.2.4. Hospitality

- 5.2.5. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Sweden

- 5.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 6. Sweden Payments Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 6.1.1. Point of Sale

- 6.1.1.1. Card Pay

- 6.1.1.2. Digital Wallet (includes Mobile Wallets)

- 6.1.1.3. Cash

- 6.1.1.4. Others

- 6.1.2. Online Sale

- 6.1.2.1. Others (

- 6.1.1. Point of Sale

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Retail

- 6.2.2. Entertainment

- 6.2.3. Healthcare

- 6.2.4. Hospitality

- 6.2.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Getswish AB

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Stripe

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Qred AB

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 2Checkout

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Nochex

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Braintree

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 QuickPay

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Klarna Bank AB

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 WorldPay

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Wirecard*List Not Exhaustive

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Getswish AB

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Sweden Payments Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Sweden Payments Market Share (%) by Company 2025

List of Tables

- Table 1: Sweden Payments Market Revenue billion Forecast, by Mode of Payment 2020 & 2033

- Table 2: Sweden Payments Market Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 3: Sweden Payments Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Sweden Payments Market Revenue billion Forecast, by Mode of Payment 2020 & 2033

- Table 5: Sweden Payments Market Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 6: Sweden Payments Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Sweden Payments Market?

The projected CAGR is approximately 38.47%.

2. Which companies are prominent players in the Sweden Payments Market?

Key companies in the market include Getswish AB, Stripe, Qred AB, 2Checkout, Nochex, Braintree, QuickPay, Klarna Bank AB, WorldPay, Wirecard*List Not Exhaustive.

3. What are the main segments of the Sweden Payments Market?

The market segments include Mode of Payment, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.01 billion as of 2022.

5. What are some drivers contributing to market growth?

High Proliferation of E-commerce. including the rise of m-commerce and cross-border e-commerce supported by the increase in purchasing power; Enablement Programs by Key Retailers and Government encouraging digitization and contactless payments in the market; Government Trials of Sweden's first digital national bank currency e-krona.

6. What are the notable trends driving market growth?

Retail is expected to grow significantly in the country.

7. Are there any restraints impacting market growth?

Security Concerns Related to Cyber Attacks and Data Breaches; Lack of Robust and Reliable Infrastructure in Remote Regions.

8. Can you provide examples of recent developments in the market?

February 2022 - Adyen is the next bank to join Swish, providing enterprise customers with easy, fast, and secure Swish payments. About 8 million Swedes and more than 300,000 companies are connected to Swish. Currently, 12 banks offer Swish to their customers, and each bank is responsible for the provision, terms, and conditions of the Swish service it provides and for all fees.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Sweden Payments Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Sweden Payments Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Sweden Payments Market?

To stay informed about further developments, trends, and reports in the Sweden Payments Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence