Key Insights

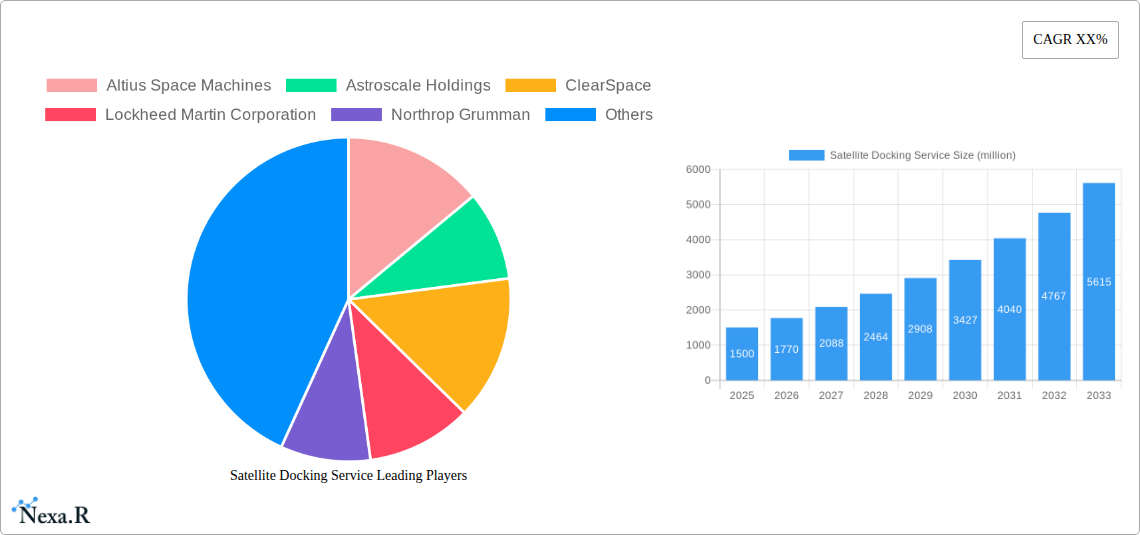

The global Satellite Docking Service market is poised for significant expansion, projected to reach an estimated $1,500 million by 2025. This growth is fueled by a robust Compound Annual Growth Rate (CAGR) of 18%, indicating a dynamic and rapidly evolving sector. The increasing demand for satellite servicing, including refueling, repair, and life extension, is a primary driver. As the number of satellites in orbit escalates, particularly with the proliferation of mega-constellations for telecommunications and earth observation, the need for efficient and cost-effective ways to maintain and extend their operational lifespan becomes paramount. This market is also benefiting from advancements in robotics and autonomous systems, enabling more sophisticated docking maneuvers and complex servicing tasks. Furthermore, the growing concerns around space debris are indirectly boosting the market, as docking services can facilitate controlled de-orbiting of defunct satellites. The market is segmented by application, with Commercial entities representing the largest share due to the massive investments in satellite infrastructure for broadband internet and data services. However, Civil Government and Military applications are also showing strong growth, driven by the need for enhanced national security, scientific research, and disaster management capabilities.

The competitive landscape features established aerospace giants like Lockheed Martin Corporation and Northrop Grumman alongside specialized companies such as Astroscale Holdings and Orbit Fab, who are at the forefront of developing innovative docking technologies and service models. The market faces certain restraints, including the high initial cost of developing and deploying docking infrastructure and the regulatory complexities surrounding space operations. Nevertheless, the overarching trend towards a more sustainable and operational space ecosystem strongly supports market expansion. Key growth opportunities lie in developing standardized docking interfaces, enabling interoperability between different satellite systems, and in offering a comprehensive suite of in-orbit services. The Asia Pacific region, particularly China and India, is expected to emerge as a significant growth hub due to substantial government investments in space exploration and satellite programs. The integration of artificial intelligence and machine learning in guiding docking procedures will further revolutionize the market, making space operations more efficient and secure.

Satellite Docking Service Market Report: Navigating the Future of In-Orbit Servicing

This comprehensive report delves into the rapidly evolving Satellite Docking Service market, providing in-depth analysis and actionable insights for industry stakeholders. Covering the period from 2019 to 2033, with a base year of 2025, this report leverages critical data and expert analysis to forecast market trajectories, identify key growth drivers, and illuminate emerging opportunities in the burgeoning in-orbit servicing sector. With a focus on both parent and child markets, this report offers a holistic view of the satellite docking service ecosystem, essential for strategic decision-making in this transformative industry.

Satellite Docking Service Market Dynamics & Structure

The satellite docking service market, a critical component of the broader space economy, is characterized by a moderately concentrated structure, driven by significant technological innovation and evolving regulatory landscapes. Key players are investing heavily in advanced rendezvous, proximity operations, and docking (RPOD) technologies, aiming to enable a new era of in-orbit servicing, assembly, and manufacturing (OSAM). The market is experiencing robust growth due to increasing satellite constellations, the growing need for space debris mitigation, and the potential for extending satellite lifespans.

- Market Concentration: Dominated by a few key players with substantial R&D capabilities, the market also features emerging startups pushing innovative solutions.

- Technological Innovation Drivers: Advancements in AI-powered navigation, robotic manipulation, and standardized docking interfaces are crucial. The development of reusable launch vehicles further reduces launch costs, making in-orbit servicing more economically viable.

- Regulatory Frameworks: Emerging international and national regulations concerning space debris, orbital traffic management, and responsible satellite operations are shaping the market's future.

- Competitive Product Substitutes: While direct substitutes are limited, the inherent cost and complexity of docking services drive interest in alternative solutions like on-orbit refueling and deorbiting technologies, which can partially address mission longevity and debris concerns.

- End-User Demographics: Primarily driven by commercial satellite operators, civil government space agencies (e.g., NASA, ESA), and military defense departments seeking enhanced operational capabilities and debris removal solutions.

- M&A Trends: The market is witnessing strategic acquisitions and partnerships as larger corporations seek to integrate specialized docking capabilities into their broader space offerings. For instance, the recent acquisition of a small satellite servicing startup by a major aerospace firm signifies a trend toward consolidation.

Satellite Docking Service Growth Trends & Insights

The satellite docking service market is poised for exponential growth, driven by an escalating demand for sustainable space operations and advanced in-orbit capabilities. The market size is projected to expand significantly, fueled by the increasing deployment of large satellite constellations for broadband communication, Earth observation, and IoT services. The imperative to address the growing challenge of space debris and to prolong the operational life of expensive satellites further amplifies the adoption rates for docking services. Technological disruptions, such as the advent of autonomous docking systems and advanced robotic arms, are not only enhancing the efficiency and safety of these operations but also paving the way for entirely new service paradigms, including on-orbit manufacturing and satellite refueling.

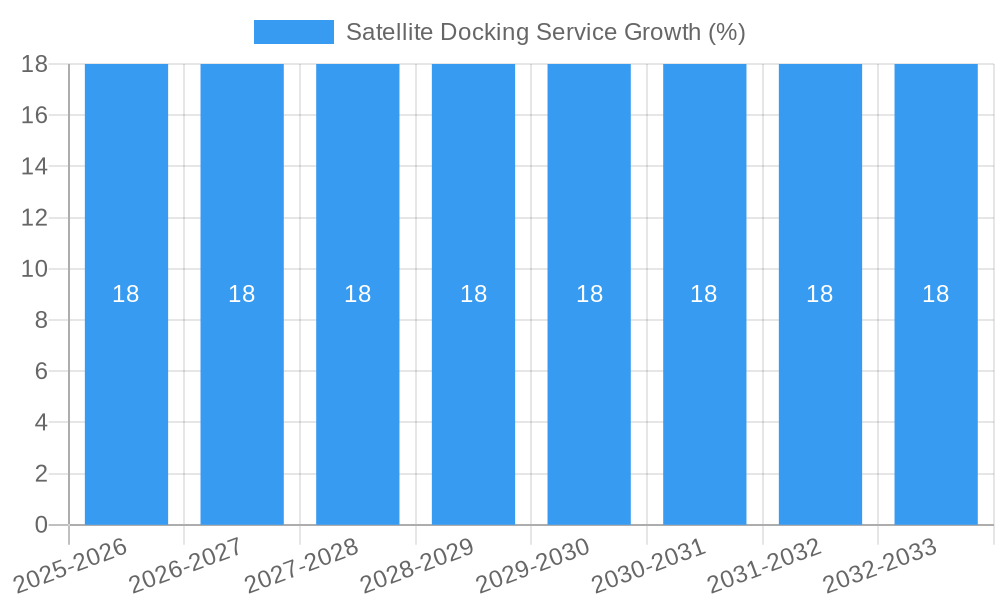

Consumer behavior within the space industry is shifting towards a more service-oriented model. Satellite operators are increasingly viewing docking services not as a niche offering but as a fundamental capability for maximizing their space asset investments. This paradigm shift is evident in the growing willingness to incorporate docking interfaces into satellite designs from the outset, anticipating future servicing needs. The market penetration of these services is expected to rise dramatically as the cost of space access continues to decline and the proven benefits of in-orbit servicing become more apparent through successful missions. The projected Compound Annual Growth Rate (CAGR) is estimated at xx% for the forecast period, indicating a robust expansion trajectory. The market is transitioning from experimental phases to operational deployments, driven by a clear understanding of the economic advantages, such as reduced total cost of ownership for satellite constellations and the creation of entirely new revenue streams for service providers. This evolution is supported by ongoing advancements in robotics, artificial intelligence, and miniaturization of components, making complex docking maneuvers more accessible and cost-effective. The growing awareness of the environmental impact of space debris is also a significant market pull, compelling governmental agencies and commercial entities alike to invest in sustainable space practices, with docking services playing a pivotal role in active debris removal and responsible end-of-life management.

Dominant Regions, Countries, or Segments in Satellite Docking Service

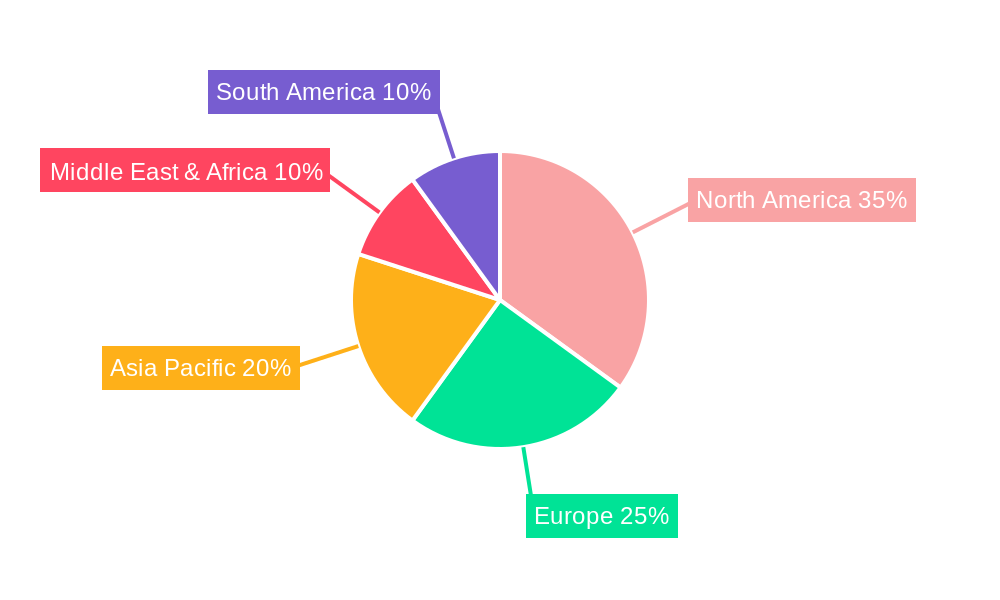

The satellite docking service market's dominance is currently being shaped by a confluence of technological innovation, robust governmental support, and a burgeoning commercial space sector. While specific regional market share data is dynamic, North America, particularly the United States, emerges as a leading force. This is attributed to a mature aerospace industry, significant investments from both government agencies like NASA and the Department of Defense, and a vibrant ecosystem of private companies pioneering advanced space technologies. The presence of key players such as Lockheed Martin Corporation, Northrop Grumman, and Rogue Space Systems underscores this leadership.

In terms of applications, the Commercial segment is a primary growth engine. The proliferation of large satellite constellations for communication, Earth observation, and navigation services necessitates sophisticated in-orbit servicing solutions, including docking, to ensure operational continuity, extend satellite lifespan, and enable complex constellation management. The economic imperative to maximize the return on investment for these multi-billion-dollar constellations drives the demand for efficient and reliable docking services. Furthermore, the burgeoning in-orbit servicing, assembly, and manufacturing (OSAM) market, which heavily relies on docking capabilities, presents substantial growth potential within the commercial sector.

Within the Types segment, Service Satellites are at the forefront of driving market growth. These specialized spacecraft are being developed specifically to perform tasks such as refueling, repairing, and upgrading other satellites. The increasing complexity and cost of individual satellites make the ability to service them in orbit a highly attractive proposition. Service satellites equipped with advanced docking mechanisms are crucial for enabling a wide range of in-orbit activities, from life extension missions for aging satellites to in-orbit assembly of larger structures. The ability of service satellites to dock with a variety of target satellites, including both new and existing platforms, highlights their pivotal role in the overall ecosystem. The market share of service satellites within the broader docking service landscape is projected to grow significantly as the OSAM market matures.

- North America (USA):

- Key Drivers: Strong government funding for space exploration and defense, a robust private space sector, and a focus on space debris mitigation.

- Market Share: Estimated to hold xx% of the global market share in 2025.

- Growth Potential: High, driven by the large number of satellite launches and the increasing demand for OSAM.

- Commercial Application:

- Key Drivers: Growth in LEO mega-constellations, demand for satellite lifespan extension, and the emergence of OSAM.

- Market Share: Projected to account for xx% of the total application market.

- Growth Potential: Extremely high, as commercial entities seek to optimize their space assets.

- Service Satellites Type:

- Key Drivers: Enabling refueling, repair, and upgrades; critical for OSAM and debris removal.

- Market Share: Expected to constitute xx% of the total type market.

- Growth Potential: Substantial, as they are the enablers of advanced in-orbit services.

Satellite Docking Service Product Landscape

The satellite docking service product landscape is characterized by rapid innovation, with companies developing sophisticated docking mechanisms, robotic arms, and autonomous navigation systems. Key product advancements include standardized docking interfaces designed for interoperability across different satellite platforms, such as the International Docking System Standard (IDSS). Innovations in robotic manipulation are enabling more precise and dexterous capture and mating of spacecraft, even in challenging orbital environments. Furthermore, the integration of advanced AI and machine learning algorithms is enhancing the autonomy of docking operations, reducing reliance on ground control and improving mission success rates. These advancements are crucial for enabling a wide array of services, from satellite refueling and repair to the assembly of larger structures in orbit and the responsible deorbiting of space debris.

Key Drivers, Barriers & Challenges in Satellite Docking Service

Key Drivers

The satellite docking service market is propelled by several key drivers, including the escalating need for space debris mitigation and the desire to extend the operational lifespan of satellites. The growing number of satellites in orbit creates a significant risk of collisions, making active debris removal services essential. Furthermore, the substantial investment in each satellite makes extending their functional life through refueling or repair highly economically attractive. Technological advancements in robotics, AI, and miniaturization are continuously improving the feasibility and safety of docking operations. The increasing deployment of large satellite constellations, particularly for communication and Earth observation, also fuels demand for efficient in-orbit servicing capabilities. Finally, the evolution of government policies and initiatives supporting sustainable space practices and the commercialization of space further bolsters market growth.

Barriers & Challenges

Despite the promising growth, the satellite docking service market faces significant barriers and challenges. High development and operational costs associated with complex docking systems and launch services remain a considerable hurdle. Technological maturity and standardization are still evolving; a lack of universally adopted docking interfaces can limit interoperability. Regulatory uncertainty and the absence of comprehensive international frameworks for in-orbit servicing and debris removal can also impede widespread adoption. Supply chain complexities for specialized components and the need for highly skilled personnel present further challenges. Competitive pressures from alternative solutions, such as advanced propulsion systems for deorbiting or on-orbit manufacturing without docking, also require continuous innovation. The inherent risks associated with orbital operations, including the possibility of mission failure during docking, necessitate stringent safety protocols and rigorous testing, adding to the overall cost and complexity.

Emerging Opportunities in Satellite Docking Service

Emerging opportunities in the satellite docking service market are abundant and span several key areas. The burgeoning in-orbit servicing, assembly, and manufacturing (OSAM) sector presents a significant avenue for growth, with docking services being fundamental to these operations. This includes the potential for assembling large space structures, manufacturing components in orbit, and conducting complex in-orbit repairs. The growing focus on active debris removal offers a substantial market, as governments and commercial entities seek solutions to mitigate the growing threat of space debris. Furthermore, the development of standardized, modular docking interfaces will unlock greater interoperability and reduce the cost of future missions. Opportunities also lie in providing refueling services for in-orbit satellites, extending their lifespan and mission capabilities. The increasing demand for space situational awareness and traffic management will also create a need for services that can dock with and move other objects.

Growth Accelerators in the Satellite Docking Service Industry

Several critical factors are accelerating growth within the satellite docking service industry. Technological breakthroughs in autonomous rendezvous and docking, advanced robotics, and AI-powered navigation are making these services more reliable, efficient, and cost-effective. Strategic partnerships and collaborations between established aerospace companies and innovative startups are fostering rapid development and market entry. The increasing governmental support and funding for OSAM technologies and space debris mitigation initiatives are providing significant momentum. Furthermore, the declining cost of space access due to reusable launch vehicles is making complex in-orbit operations more economically viable. Market expansion strategies, such as offering a comprehensive suite of in-orbit services beyond just docking, are also driving growth by creating new revenue streams and attracting a broader customer base.

Key Players Shaping the Satellite Docking Service Market

- Altius Space Machines

- Astroscale Holdings

- ClearSpace

- Lockheed Martin Corporation

- Northrop Grumman

- Orbit Fab

- QinetiQ

- Rogue Space Systems

- Starfish Space

Notable Milestones in Satellite Docking Service Sector

- 2019: Orbit Fab launched its first refueling depot in orbit, demonstrating a foundational element for future in-orbit servicing.

- 2020: Astroscale Holdings successfully conducted multiple debris removal technology demonstrations, highlighting progress in active debris removal capabilities.

- 2021: Lockheed Martin Corporation announced advancements in their robotic capture technology, crucial for debris removal and satellite servicing missions.

- 2022: ClearSpace was awarded a contract for the first major active debris removal mission by the European Space Agency, signaling significant market validation.

- 2023: Rogue Space Systems successfully demonstrated its orbital-servicing drone, "Scout," in proximity operations.

- 2024: Starfish Space completed a successful on-orbit demonstration of its docking technology, "Spore."

- 2024: QinetiQ continued to advance its robotics and autonomous systems for space applications, relevant to docking and servicing.

In-Depth Satellite Docking Service Market Outlook

The satellite docking service market is on a trajectory of significant expansion, driven by an undeniable need for sustainable space operations and enhanced in-orbit capabilities. Growth accelerators such as advancements in AI-powered autonomous docking, the increasing focus on active debris removal mandated by international bodies, and the economic viability offered by satellite life extension through refueling and repair will continue to propel the market forward. Strategic partnerships between established players like Lockheed Martin Corporation and innovative startups such as Orbit Fab are crucial for accelerating the development and deployment of these critical technologies. The future promises a robust ecosystem where docking services are not just an ancillary capability but an integral part of the space economy, enabling complex missions, fostering new business models, and ensuring the long-term sustainability of our orbital environment.

Satellite Docking Service Segmentation

-

1. Application

- 1.1. Commercial

- 1.2. Civil Government

- 1.3. Military

-

2. Types

- 2.1. Target Satellites

- 2.2. Service Satellites

Satellite Docking Service Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Satellite Docking Service REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Satellite Docking Service Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Commercial

- 5.1.2. Civil Government

- 5.1.3. Military

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Target Satellites

- 5.2.2. Service Satellites

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Satellite Docking Service Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Commercial

- 6.1.2. Civil Government

- 6.1.3. Military

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Target Satellites

- 6.2.2. Service Satellites

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Satellite Docking Service Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Commercial

- 7.1.2. Civil Government

- 7.1.3. Military

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Target Satellites

- 7.2.2. Service Satellites

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Satellite Docking Service Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Commercial

- 8.1.2. Civil Government

- 8.1.3. Military

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Target Satellites

- 8.2.2. Service Satellites

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Satellite Docking Service Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Commercial

- 9.1.2. Civil Government

- 9.1.3. Military

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Target Satellites

- 9.2.2. Service Satellites

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Satellite Docking Service Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Commercial

- 10.1.2. Civil Government

- 10.1.3. Military

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Target Satellites

- 10.2.2. Service Satellites

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Altius Space Machines

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Astroscale Holdings

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 ClearSpace

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Lockheed Martin Corporation

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Northrop Grumman

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Orbit Fab

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 QinetiQ

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Rogue Space Systems

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Starfish Space

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.1 Altius Space Machines

List of Figures

- Figure 1: Global Satellite Docking Service Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Satellite Docking Service Revenue (million), by Application 2024 & 2032

- Figure 3: North America Satellite Docking Service Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Satellite Docking Service Revenue (million), by Types 2024 & 2032

- Figure 5: North America Satellite Docking Service Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Satellite Docking Service Revenue (million), by Country 2024 & 2032

- Figure 7: North America Satellite Docking Service Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Satellite Docking Service Revenue (million), by Application 2024 & 2032

- Figure 9: South America Satellite Docking Service Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Satellite Docking Service Revenue (million), by Types 2024 & 2032

- Figure 11: South America Satellite Docking Service Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Satellite Docking Service Revenue (million), by Country 2024 & 2032

- Figure 13: South America Satellite Docking Service Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Satellite Docking Service Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Satellite Docking Service Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Satellite Docking Service Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Satellite Docking Service Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Satellite Docking Service Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Satellite Docking Service Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Satellite Docking Service Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Satellite Docking Service Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Satellite Docking Service Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Satellite Docking Service Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Satellite Docking Service Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Satellite Docking Service Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Satellite Docking Service Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Satellite Docking Service Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Satellite Docking Service Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Satellite Docking Service Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Satellite Docking Service Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Satellite Docking Service Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Satellite Docking Service Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Satellite Docking Service Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Satellite Docking Service Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Satellite Docking Service Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Satellite Docking Service Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Satellite Docking Service Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Satellite Docking Service Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Satellite Docking Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Satellite Docking Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Satellite Docking Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Satellite Docking Service Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Satellite Docking Service Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Satellite Docking Service Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Satellite Docking Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Satellite Docking Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Satellite Docking Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Satellite Docking Service Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Satellite Docking Service Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Satellite Docking Service Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Satellite Docking Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Satellite Docking Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Satellite Docking Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Satellite Docking Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Satellite Docking Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Satellite Docking Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Satellite Docking Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Satellite Docking Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Satellite Docking Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Satellite Docking Service Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Satellite Docking Service Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Satellite Docking Service Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Satellite Docking Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Satellite Docking Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Satellite Docking Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Satellite Docking Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Satellite Docking Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Satellite Docking Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Satellite Docking Service Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Satellite Docking Service Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Satellite Docking Service Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Satellite Docking Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Satellite Docking Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Satellite Docking Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Satellite Docking Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Satellite Docking Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Satellite Docking Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Satellite Docking Service Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Satellite Docking Service?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Satellite Docking Service?

Key companies in the market include Altius Space Machines, Astroscale Holdings, ClearSpace, Lockheed Martin Corporation, Northrop Grumman, Orbit Fab, QinetiQ, Rogue Space Systems, Starfish Space.

3. What are the main segments of the Satellite Docking Service?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Satellite Docking Service," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Satellite Docking Service report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Satellite Docking Service?

To stay informed about further developments, trends, and reports in the Satellite Docking Service, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence