Key Insights

The European metal closures market is projected for robust growth, expected to reach 9.79 billion by 2025, with a Compound Annual Growth Rate (CAGR) of 4.28% from 2025 to 2033. This expansion is primarily driven by the significant demand from the food and beverage industries, representing the largest end-user segments. Increasing consumer preference for packaged goods, alongside stringent quality and safety regulations, mandates the use of dependable and secure metal closures. Additionally, the pharmaceutical sector's continuous requirement for tamper-evident and sterile packaging solutions further fuels market growth. Key growth catalysts include evolving packaging designs, advancements in closure technologies enhancing convenience and sustainability, and a growing focus on extending product shelf-life. Companies are increasing investments in advanced manufacturing and exploring recyclable materials to meet regulatory and consumer demands.

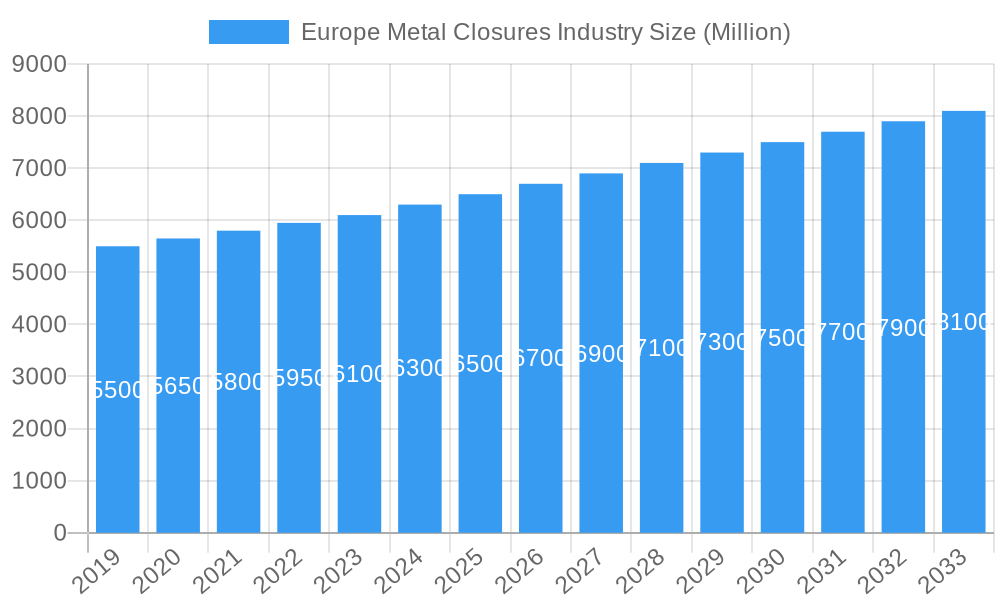

Europe Metal Closures Industry Market Size (In Billion)

Despite strong growth potential, the market faces challenges. Rising raw material costs, particularly for aluminum and steel, may impact manufacturer profitability and pricing. Intense competition and the entry of new players create a dynamic landscape. However, trends such as packaging miniaturization, the rise of premium and artisanal products, and the adoption of smart packaging with traceability features are expected to unlock new growth opportunities. Europe, with its developed economies and discerning consumer base, represents a key market. Leading countries like the United Kingdom, Germany, France, and Italy are anticipated to drive consumption and innovation, supported by strong manufacturing sectors and vibrant end-user industries.

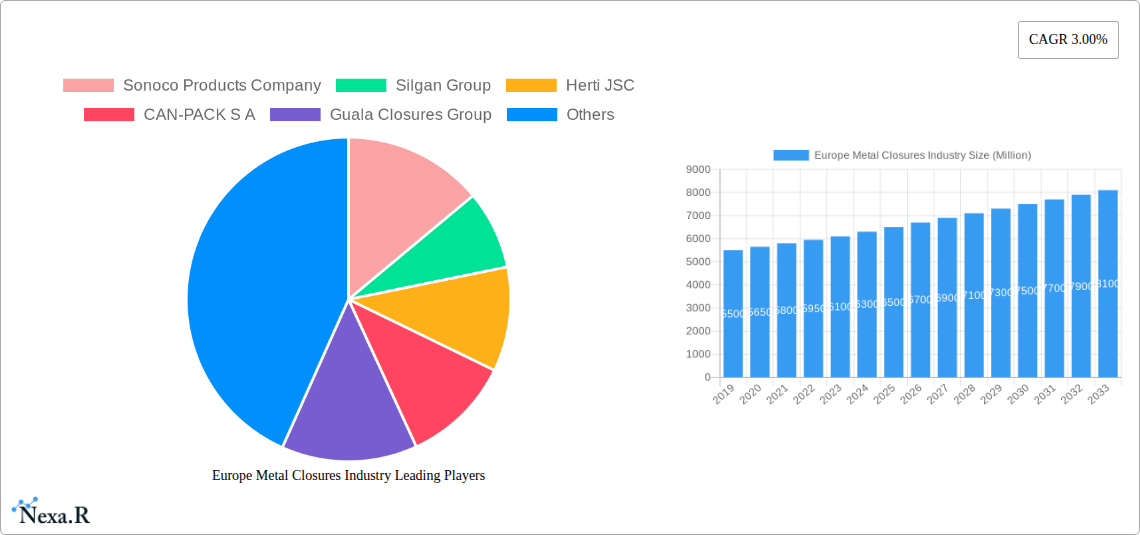

Europe Metal Closures Industry Company Market Share

This comprehensive report provides an in-depth analysis of the Europe Metal Closures Industry, vital for packaging across food, beverage, pharmaceutical, and other sectors. Covering the historical period 2019-2024, with a base year of 2025 and a forecast extending to 2033, the report offers actionable insights for stakeholders navigating this dynamic market. It focuses on market structure, growth drivers, regional trends, product innovation, and key players, serving as an essential resource for manufacturers, suppliers, investors, and industry professionals. Market values are presented in billions for clarity.

Europe Metal Closures Industry Market Dynamics & Structure

The Europe Metal Closures Industry exhibits a moderately concentrated market structure, with a few large global players dominating a significant portion of the market share. Technological innovation remains a key driver, with ongoing advancements in material science, manufacturing processes, and smart closure technologies aimed at enhancing product safety, shelf-life, and consumer convenience. Regulatory frameworks, particularly those concerning food contact materials, recyclability, and sustainability, significantly influence market dynamics, pushing manufacturers towards eco-friendly solutions. Competitive product substitutes, primarily from plastic and composite materials, present a constant challenge, necessitating continuous innovation in metal closure design and functionality to maintain market relevance. End-user demographics, such as an aging population and increasing demand for convenience, shape product requirements. Mergers and acquisition (M&A) trends are also notable, with larger entities consolidating their market positions and expanding their product portfolios. For instance, the past study period has seen strategic acquisitions aimed at integrating supply chains and gaining access to new markets.

- Market Concentration: Dominated by a few key players, leading to a competitive yet consolidated landscape.

- Technological Innovation: Driven by advancements in lightweighting, barrier properties, tamper-evidence, and ease of opening.

- Regulatory Frameworks: Stringent regulations on food safety, sustainability, and recycling are shaping product development and market entry.

- Competitive Landscape: Intense competition from plastic and alternative closure materials necessitates continuous value proposition enhancement.

- End-User Demographics: Influenced by shifting consumer preferences towards premium, convenient, and sustainably packaged goods.

- M&A Trends: Strategic consolidations and acquisitions aimed at market expansion and portfolio diversification.

Europe Metal Closures Industry Growth Trends & Insights

The Europe Metal Closures Industry is poised for robust growth throughout the forecast period, driven by a confluence of factors including escalating demand from key end-user sectors and evolving consumer preferences. The market size is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 4.5% from 2025 to 2033. This growth is underpinned by the sustained demand for metal closures in the Beverage sector, particularly for carbonated soft drinks, beer, and juices, where the need for hermetic sealing and product integrity is paramount. The Food industry also represents a significant contributor, with metal closures being essential for preserving perishable goods such as dairy products, jams, sauces, and baby food. Pharmaceutical applications are experiencing steady growth, fueled by the increasing production of medicines and healthcare products requiring secure and tamper-evident packaging.

Technological disruptions are playing a pivotal role in shaping adoption rates. Innovations in material science have led to the development of thinner, yet stronger, metal alloys, reducing material consumption and enhancing sustainability credentials. Advanced coating technologies are further improving barrier properties, extending shelf life, and preventing product degradation. The adoption of smart closure technologies, incorporating features like track-and-trace capabilities and authentication markers, is gaining traction, particularly in high-value segments like pharmaceuticals and premium beverages, to combat counterfeiting and enhance supply chain transparency.

Consumer behavior shifts are also a key growth accelerator. There's a growing consumer awareness and preference for products packaged in materials perceived as more sustainable and premium, which metal closures often fulfill. The recyclability of metal, a significant advantage, resonates with environmentally conscious consumers. Furthermore, the demand for convenience is driving the development of easy-open and resealable metal closures, catering to on-the-go consumption and reducing product waste. The increasing urbanization and the rise of e-commerce are also contributing to the demand for robust and reliable packaging solutions that can withstand the rigors of transit. Market penetration of advanced metal closure solutions is expected to deepen as manufacturers invest in research and development to meet these evolving demands. The overall market trajectory indicates a positive and sustainable growth path, with innovation and adaptability being key to capitalizing on emerging opportunities.

Dominant Regions, Countries, or Segments in Europe Metal Closures Industry

The Beverage segment within the Europe Metal Closures Industry is currently the dominant force driving market growth, exhibiting a significant market share of approximately 45% in the base year 2025. This dominance is attributed to several key factors, including high consumption rates of packaged beverages across Europe, a robust carbonated soft drink and beer market, and the continuous demand for metal closures that ensure product integrity and safety for a wide array of liquid consumables. The beverage industry's reliance on metal closures for sealing carbonated drinks, preserving freshness, and providing tamper-evidence makes it a cornerstone of the metal closures market.

Within the beverage segment, countries like Germany, France, the United Kingdom, and Italy represent the leading markets due to their large populations, developed economies, and established food and beverage manufacturing bases. Economic policies in these countries, which often support domestic manufacturing and export, further bolster the demand for metal closures. Infrastructure development, particularly in logistics and distribution networks, ensures the efficient supply of packaged beverages to consumers, indirectly fueling the demand for closures.

The Food segment follows closely as a significant growth driver, accounting for an estimated 35% of the market share in 2025. The demand here is driven by the need for secure and long-lasting packaging for a diverse range of products, including dairy, preserves, sauces, and processed foods. Consumer preference for convenience and longer shelf-life also plays a crucial role in the continued adoption of metal closures in this sector.

The Pharmaceuticals segment, while smaller in market share (around 15% in 2025), is experiencing rapid growth. This expansion is fueled by the increasing production of medicines, the need for stringent child-resistant and tamper-evident closures, and the overall growth of the healthcare industry across Europe. Regulatory requirements for pharmaceutical packaging are exceptionally high, driving innovation and the adoption of advanced metal closure solutions.

The "Other End-User Industries" segment, encompassing cosmetics, personal care, and industrial applications, contributes the remaining market share. While this segment might not be as large as food and beverage, it offers niche growth opportunities driven by specific product requirements and emerging applications. The overall dominance of the beverage sector, supported by the strong performance of the food and pharmaceutical segments, shapes the current landscape and future trajectory of the Europe Metal Closures Industry. Market share estimations are based on the aggregate volume of metal closures used across these end-user segments.

Europe Metal Closures Industry Product Landscape

The Europe Metal Closures Industry is characterized by a diverse and evolving product landscape focused on enhancing functionality, sustainability, and consumer appeal. Innovations in lightweighting technologies have led to the development of thinner yet robust metal closures, optimizing material usage and reducing costs. Advanced barrier coatings are increasingly being applied to metal closures to improve product shelf-life and protect contents from moisture, oxygen, and light, especially crucial for food and pharmaceutical applications. Tamper-evident features are a critical aspect, with advancements in pull-ring designs and sealing mechanisms ensuring product integrity and consumer safety. The industry is also witnessing a rise in easy-open and resealable closure solutions, catering to the growing demand for convenience and on-the-go consumption. Unique selling propositions often lie in the combination of superior sealing performance, aesthetic appeal, and enhanced user experience, such as tactile grip enhancements for easier opening. Technological advancements are also paving the way for more sustainable production processes and the increased use of recycled metal content in closures.

Key Drivers, Barriers & Challenges in Europe Metal Closures Industry

The Europe Metal Closures Industry is propelled by several key drivers. Technological advancements in material science, manufacturing efficiency, and smart closure functionalities are crucial for innovation and competitive advantage. Growing demand from end-user industries like food and beverage, driven by population growth and evolving consumption patterns, provides a consistent market. Sustainability and recyclability are significant drivers, as metal closures are highly valued for their recyclability, aligning with circular economy initiatives and consumer preferences. Stringent regulatory requirements for product safety and shelf-life indirectly push for higher-quality closure solutions.

However, the industry faces notable barriers and challenges. Competition from plastic and alternative packaging materials remains a significant threat, often offering cost advantages or specific functional benefits. Fluctuations in raw material prices, particularly aluminum and steel, can impact manufacturing costs and profitability. Supply chain disruptions, as experienced globally, can affect the availability and timely delivery of materials and finished products. Increasing environmental regulations concerning energy consumption and emissions in manufacturing processes can add to operational costs.

Emerging Opportunities in Europe Metal Closures Industry

Emerging opportunities in the Europe Metal Closures Industry are primarily centered around the growing demand for sustainable packaging solutions and the integration of smart technologies. The circular economy push creates significant potential for metal closures due to their high recyclability rates, driving demand for closures made from recycled content and facilitating closed-loop systems. Innovative applications in niche sectors, such as premium spirits, specialty foods, and advanced pharmaceutical packaging, offer lucrative avenues for growth. The increasing adoption of smart closures with integrated QR codes or NFC tags for traceability, authentication, and consumer engagement presents a substantial opportunity for added value and differentiation. Furthermore, the development of specialty closures designed for specific product needs, such as enhanced shelf-life extension or ease of use for specific consumer demographics, is another area of potential expansion.

Growth Accelerators in the Europe Metal Closures Industry Industry

Several catalysts are accelerating the growth of the Europe Metal Closures Industry. Technological breakthroughs in material science, leading to lighter, stronger, and more sustainable metal alloys, are enhancing the competitiveness of metal closures. Strategic partnerships and collaborations between closure manufacturers and packaging converters are fostering innovation and expanding market reach. The increasing focus on Brand Protection and Anti-Counterfeiting is driving the adoption of advanced tamper-evident and authentication features in metal closures, particularly in the pharmaceutical and premium beverage sectors. Market expansion strategies, including penetration into emerging markets within Europe and the development of customized solutions for specific regional demands, are also contributing to growth. Furthermore, the growing consumer preference for premium and sustainable packaging directly benefits the metal closures sector due to its inherent recyclability and perceived quality.

Key Players Shaping the Europe Metal Closures Industry Market

- Sonoco Products Company

- Silgan Group

- Herti JSC

- CAN-PACK S A

- Guala Closures Group

- Technocap Group

- Crown Holdings Incorporated

- Pelliconi & C SpA

Notable Milestones in Europe Metal Closures Industry Sector

- 2021: Guala Closures Group's acquisition of Manaksia Industries Limited's aluminum closure business, expanding its global footprint.

- 2022: Crown Holdings Incorporated's investment in advanced coating technologies to enhance the sustainability and functionality of its metal closures.

- 2023 (Q3): Silgan Group announces strategic investments in its European manufacturing facilities to increase capacity for high-demand beverage closures.

- 2023 (Q4): CAN-PACK S A highlights advancements in its lightweight aluminum closure portfolio, focusing on material reduction and environmental benefits.

- 2024 (Q1): Herti JSC introduces a new range of child-resistant metal closures for pharmaceutical applications, meeting stringent safety standards.

In-Depth Europe Metal Closures Industry Market Outlook

The Europe Metal Closures Industry is set for sustained growth, driven by a confluence of favorable market dynamics and strategic growth accelerators. The persistent demand from the beverage and food sectors, coupled with the rising importance of sustainable packaging, positions metal closures favorably. Innovations in lightweighting, advanced barrier technologies, and smart functionalities will continue to enhance their competitive edge against alternative materials. The industry's ability to adapt to evolving regulatory landscapes and capitalize on the increasing consumer preference for recyclability will be paramount. Strategic investments in manufacturing capabilities and the development of specialized closure solutions for high-value segments like pharmaceuticals and premium goods will further fuel this growth trajectory, ensuring a robust and dynamic future for the Europe Metal Closures Industry.

Europe Metal Closures Industry Segmentation

-

1. End-user

- 1.1. Food

- 1.2. Beverage

- 1.3. Pharmaceuticals

- 1.4. Other End-User Industries

Europe Metal Closures Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

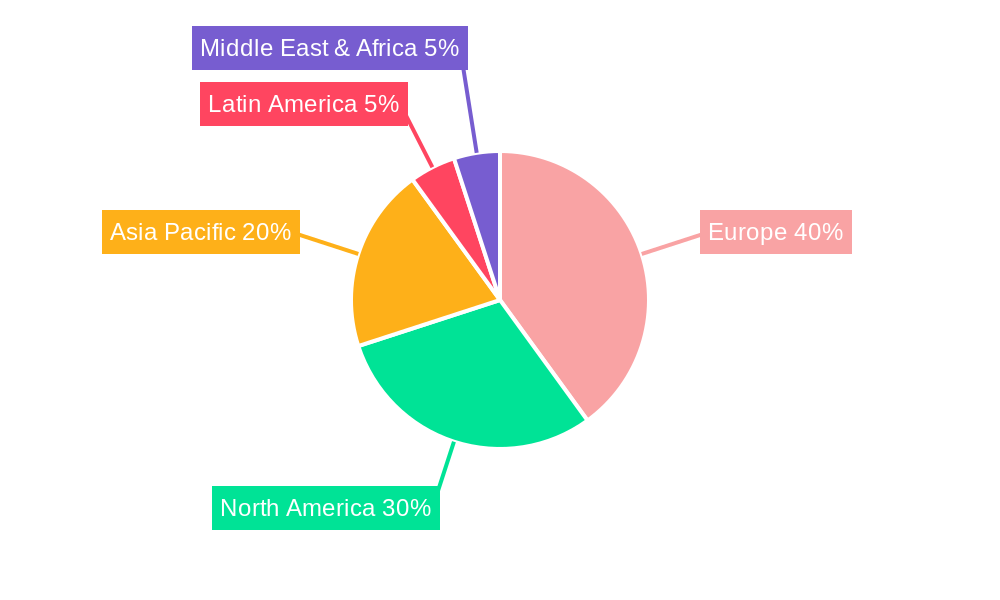

Europe Metal Closures Industry Regional Market Share

Geographic Coverage of Europe Metal Closures Industry

Europe Metal Closures Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.28% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End-user

- 5.1.1. Food

- 5.1.2. Beverage

- 5.1.3. Pharmaceuticals

- 5.1.4. Other End-User Industries

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by End-user

- 6. Europe Metal Closures Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End-user

- 6.1.1. Food

- 6.1.2. Beverage

- 6.1.3. Pharmaceuticals

- 6.1.4. Other End-User Industries

- 6.1. Market Analysis, Insights and Forecast - by End-user

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Sonoco Products Company

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Silgan Group

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Herti JSC

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 CAN-PACK S A

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Guala Closures Group

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Technocap Group*List Not Exhaustive

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Crown Holdings Incorporated

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Pelliconi & C SpA

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.1 Sonoco Products Company

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Metal Closures Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Metal Closures Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Metal Closures Industry Revenue billion Forecast, by End-user 2020 & 2033

- Table 2: Europe Metal Closures Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Europe Metal Closures Industry Revenue billion Forecast, by End-user 2020 & 2033

- Table 4: Europe Metal Closures Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 5: United Kingdom Europe Metal Closures Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 6: Germany Europe Metal Closures Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 7: France Europe Metal Closures Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Italy Europe Metal Closures Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Spain Europe Metal Closures Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Netherlands Europe Metal Closures Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Belgium Europe Metal Closures Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Sweden Europe Metal Closures Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Norway Europe Metal Closures Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Poland Europe Metal Closures Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Denmark Europe Metal Closures Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Metal Closures Industry?

The projected CAGR is approximately 4.28%.

2. Which companies are prominent players in the Europe Metal Closures Industry?

Key companies in the market include Sonoco Products Company, Silgan Group, Herti JSC, CAN-PACK S A, Guala Closures Group, Technocap Group*List Not Exhaustive, Crown Holdings Incorporated, Pelliconi & C SpA.

3. What are the main segments of the Europe Metal Closures Industry?

The market segments include End-user .

4. Can you provide details about the market size?

The market size is estimated to be USD 9.79 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Consumption of Convenience Food; Innovation and Added Value Offering to Change the Image of Food Cans.

6. What are the notable trends driving market growth?

Beverage Industry Expected to Exhibit Maximum Adoption.

7. Are there any restraints impacting market growth?

; Stringent Regulations on the Usage of Plastic Bottles.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Metal Closures Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Metal Closures Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Metal Closures Industry?

To stay informed about further developments, trends, and reports in the Europe Metal Closures Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence