Key Insights

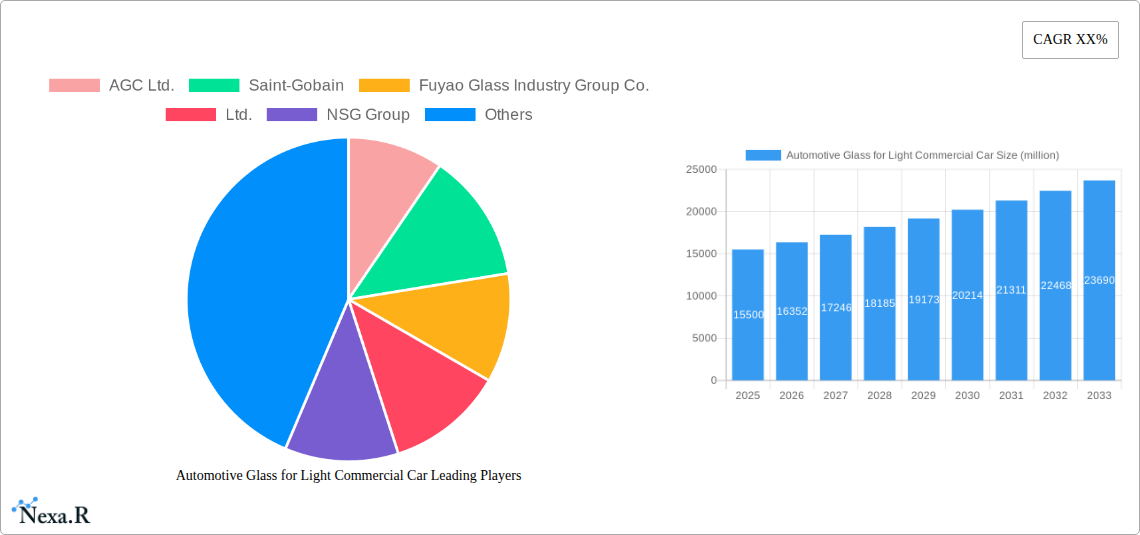

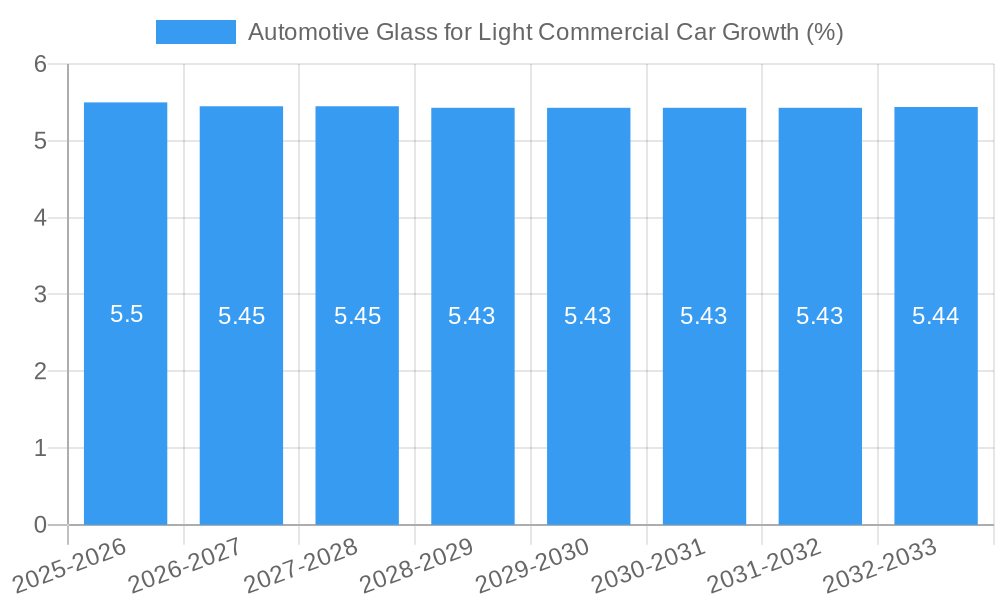

The global market for automotive glass specifically for light commercial vehicles (LCVs) is projected to reach an estimated value of approximately $15,500 million by 2025, exhibiting a robust Compound Annual Growth Rate (CAGR) of around 5.5% throughout the forecast period of 2025-2033. This substantial growth is primarily fueled by the escalating demand for LCVs across diverse sectors, including logistics, e-commerce delivery, and service industries. The increasing adoption of advanced driver-assistance systems (ADAS) also necessitates sophisticated automotive glass solutions, incorporating features like sensors and heating elements, further bolstering market expansion. Furthermore, the aftermarket replacement segment is expected to witness consistent growth, driven by the aging vehicle parc and the need for timely repairs and replacements to ensure vehicle safety and functionality.

The market landscape is characterized by the dominance of tempered glass due to its superior safety features, making it a preferred choice for LCVs. Laminated glass, offering enhanced security and acoustic insulation, is also gaining traction, particularly in premium LCV models. Key players like AGC Ltd., Saint-Gobain, Fuyao Glass Industry Group Co., Ltd., and NSG Group are actively investing in research and development to innovate and cater to evolving industry demands. Geographically, Asia Pacific, led by China and India, is anticipated to be the largest and fastest-growing market, attributed to robust LCV production and a burgeoning automotive sector. North America and Europe are also significant markets, driven by stringent safety regulations and a strong aftermarket segment. However, challenges such as fluctuating raw material prices and intense competition among manufacturers may present some restraints to the market's overall growth trajectory.

Automotive Glass for Light Commercial Car Market Analysis: A Comprehensive Report (2019-2033)

This in-depth report provides a panoramic view of the global automotive glass for light commercial car market, meticulously analyzing its dynamics, growth trajectory, and competitive landscape. Designed for industry professionals, manufacturers, suppliers, and investors, this study leverages high-traffic keywords and robust data to offer actionable insights. We explore the intricate interplay of parent and child markets, delving into segments such as Original Equipment Manufacturer (OEM) and Aftermarket Replacement (ARG), and types including Tempered, Laminated, and Other glass solutions. With a study period spanning from 2019 to 2033, including historical data (2019-2024), a base year (2025), and an extensive forecast period (2025-2033), this report delivers unparalleled market intelligence. All quantitative data is presented in million units for clarity and impact.

Automotive Glass for Light Commercial Car Market Dynamics & Structure

The automotive glass for light commercial car market exhibits a moderate concentration, with key players like AGC Ltd., Saint-Gobain, Fuyao Glass Industry Group Co., Ltd., and NSG Group holding significant market shares. Technological innovation is a primary driver, particularly advancements in lighter, stronger, and more integrated glass solutions, including acoustic and smart glass technologies. Regulatory frameworks, focusing on safety standards (e.g., improved impact resistance, shatterproof designs) and increasingly, energy efficiency mandates (e.g., solar-reflective coatings), are shaping product development. Competitive product substitutes are minimal for primary automotive glass functions, but innovations in materials for advanced driver-assistance systems (ADAS) integration present new competitive frontiers. End-user demographics, characterized by a growing demand for reliable and technologically advanced LCCs in logistics and service sectors, directly influence market trends. Mergers and acquisitions (M&A) activity, while moderate, aims to consolidate market presence and enhance technological capabilities.

- Market Concentration: Moderately concentrated with top 4 players holding approximately 65% market share.

- Technological Innovation Drivers: ADAS integration, lightweighting, enhanced durability, acoustic insulation, solar control.

- Regulatory Frameworks: Stringent safety standards (FMVSS, ECE), emissions regulations, and evolving ADAS deployment mandates.

- Competitive Product Substitutes: Limited for primary glass functions; focus shifting to materials supporting integrated electronics and sensors.

- End-User Demographics: Growing demand from logistics, e-commerce delivery, construction, and trades sectors for versatile and safe LCCs.

- M&A Trends: Strategic acquisitions to gain access to new technologies and expand geographical reach.

Automotive Glass for Light Commercial Car Growth Trends & Insights

The global automotive glass for light commercial car market is poised for robust expansion, driven by evolving industry dynamics and increasing LCC adoption across diverse commercial applications. The market size is projected to witness a significant upward trend, escalating from an estimated value in 2025 to a projected substantial figure by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 5.5% over the forecast period. This growth is underpinned by several key factors, including the surge in e-commerce necessitating efficient last-mile delivery solutions, which in turn fuels the demand for light commercial vehicles equipped with advanced safety and functional glazing. Furthermore, the increasing integration of sophisticated ADAS features in LCCs, such as cameras, sensors, and LiDAR, directly impacts the complexity and value of automotive glass, requiring specialized lamination and mounting capabilities. Consumer behavior is also shifting towards LCCs that offer enhanced comfort, connectivity, and safety, thereby driving OEM demand for premium glass solutions.

The adoption rates for specialized automotive glass, such as panoramic sunroofs and advanced acoustic glazing, are steadily increasing within the LCC segment, mirroring trends seen in passenger vehicles. Technological disruptions, including advancements in manufacturing processes that enable more intricate designs and enhanced performance characteristics, are contributing to market evolution. The development of self-healing glass and electrochromic technologies, while still nascent in LCCs, represents future growth avenues. Government initiatives promoting the adoption of commercial electric vehicles (EVs) are also indirectly benefiting the automotive glass market, as EVs often incorporate unique glass designs to optimize aerodynamics and battery management. The aftermarket replacement (ARG) segment is expected to remain a significant contributor, driven by the aging LCC fleet and the need for replacements due to wear and tear or accidental damage. Innovations in glass coatings for improved UV protection and thermal management are also gaining traction, aligning with consumer preferences for greater comfort and reduced operational costs. The overall market penetration of advanced glass technologies within the LCC sector is on an upward trajectory, indicating a maturing market that is increasingly valuing safety, efficiency, and technological sophistication in its glazing solutions.

Dominant Regions, Countries, or Segments in Automotive Glass for Light Commercial Car

The automotive glass for light commercial car market is experiencing significant growth and diversification across various regions and segments. Among the Applications, the Original Equipment Manufacturer (OEM) segment currently holds a dominant position and is projected to maintain its lead throughout the forecast period. This dominance is attributed to the consistent and substantial demand from LCC manufacturers for factory-fitted glazing solutions. The burgeoning global trade and logistics sector, coupled with the rapid expansion of e-commerce, is a primary driver for the increased production of new light commercial vehicles, thereby bolstering the OEM segment. Economic policies aimed at supporting manufacturing and trade infrastructure in key automotive hubs also contribute significantly to OEM demand.

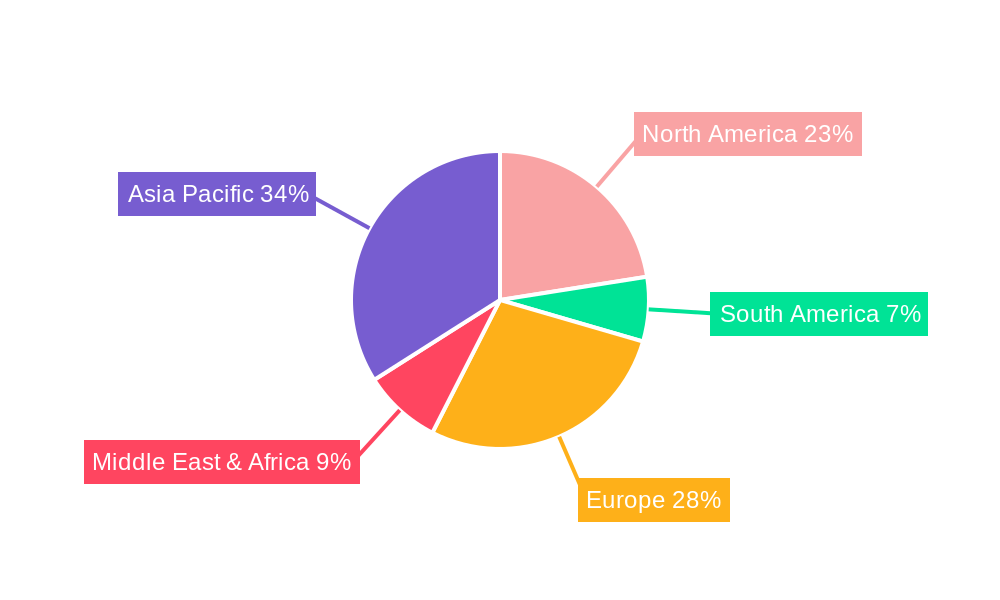

Geographically, North America and Europe are identified as dominant regions, driven by stringent safety regulations, a mature automotive industry, and a substantial existing fleet of light commercial vehicles requiring regular maintenance and replacement. The increasing adoption of electric LCCs in these regions, coupled with the growing demand for advanced driver-assistance systems (ADAS) that necessitate sophisticated windshield designs, further solidifies their leadership. Asia Pacific, particularly China, is emerging as a rapidly growing market due to its expansive manufacturing capabilities and increasing domestic demand for LCCs in logistics and last-mile delivery services.

Within the Types segment, Laminated glass is the leading category for windshields and side windows in light commercial vehicles. This is due to its superior safety features, such as enhanced shatter resistance and impact protection, which are critical for commercial applications where durability and occupant safety are paramount. The increasing regulatory emphasis on safety standards and the integration of ADAS components directly onto the windshield further propel the demand for laminated glass. Tempered glass remains important for other applications like rear windows and some side windows due to its strength and fracture characteristics, but laminated glass is increasingly preferred for its safety attributes. The growth potential for laminated glass is further amplified by innovations in its composite structure, offering improved acoustic insulation and UV protection, thereby enhancing driver comfort and operational efficiency for LCCs.

- Dominant Application: Original Equipment Manufacturer (OEM) – driven by new vehicle production and fleet expansion.

- Key Drivers: E-commerce growth, global trade, supportive manufacturing policies.

- Market Share: Approximately 70% of the total market in 2025.

- Growth Potential: Steady growth aligned with new LCC production forecasts.

- Dominant Region: North America and Europe, with Asia Pacific showing strong growth.

- Key Drivers: Safety regulations, mature automotive industry, EV adoption, ADAS integration.

- Market Share (North America & Europe Combined): Approximately 55% of the global market in 2025.

- Growth Potential: Continued strong demand due to fleet size and technological advancements.

- Dominant Type: Laminated Glass – essential for safety and ADAS integration.

- Key Drivers: Superior safety performance, regulatory compliance, integration of sensors and cameras.

- Market Share: Approximately 60% of the total glass types in 2025.

- Growth Potential: High growth due to increasing ADAS penetration and safety mandates.

Automotive Glass for Light Commercial Car Product Landscape

The automotive glass for light commercial car product landscape is evolving rapidly with innovations focused on enhancing safety, durability, and functionality. Manufacturers are increasingly incorporating advanced materials and coatings into windshields and windows. This includes lightweight, high-strength laminated glass solutions that offer superior impact resistance, crucial for the demanding environments LCCs often operate in. Features such as integrated antenna systems, rain sensors, and heating elements are becoming standard in premium LCC models. Furthermore, advancements in acoustic glass are being adopted to improve cabin comfort by reducing road and wind noise, thereby enhancing driver productivity and reducing fatigue during long haul journeys. The growing emphasis on electric LCCs is also driving the development of specialized glass with integrated thermal management properties to optimize battery performance and cabin temperature.

Key Drivers, Barriers & Challenges in Automotive Glass for Light Commercial Car

The automotive glass for light commercial car market is propelled by several key drivers including the escalating demand for LCCs in logistics and e-commerce, driven by global trade expansion and urban last-mile delivery needs. Increasing integration of advanced driver-assistance systems (ADAS) necessitates sophisticated, multi-functional windshields, boosting demand for specialized glass. Stringent automotive safety regulations worldwide mandate enhanced glass performance, favoring laminated and tempered glass technologies. Technological advancements in glass manufacturing and material science contribute to lighter, stronger, and more durable products.

However, the market faces significant barriers and challenges. Supply chain disruptions, particularly for specialized raw materials and components, can impact production volumes and lead times. The high cost of implementing advanced manufacturing technologies and R&D for innovative glass solutions can be a deterrent for smaller players. Intense competition among established manufacturers and the threat of new entrants, especially from emerging economies, can lead to price pressures. Evolving regulatory landscapes and the standardization of ADAS integration can also present compliance challenges and necessitate continuous product adaptation.

Emerging Opportunities in Automotive Glass for Light Commercial Car

Emerging opportunities in the automotive glass for light commercial car market lie in the growing demand for lightweight and energy-efficient glazing solutions for electric LCCs, which can improve battery range. The expansion of smart glass technologies, such as electrochromic and privacy glass, offers enhanced comfort and functionality for premium LCC segments. The increasing adoption of telematics and sensor integration within vehicles presents opportunities for glass manufacturers to embed advanced sensor technologies, creating value-added products for fleet management and safety. Furthermore, the burgeoning aftermarket for retrofitting older LCCs with modern safety and connectivity features opens up new avenues for specialized glass solutions. Untapped markets in developing economies with rapidly growing logistics sectors also represent significant growth potential.

Growth Accelerators in the Automotive Glass for Light Commercial Car Industry

Several catalysts are accelerating growth in the automotive glass for light commercial car industry. The rapid expansion of the global e-commerce sector and the subsequent surge in demand for last-mile delivery vehicles are primary growth engines. Strategic partnerships between automotive glass manufacturers and LCC OEMs to co-develop integrated glazing solutions for next-generation vehicles, particularly EVs, are crucial. Market expansion strategies focusing on emerging economies with developing logistics infrastructure are also key. Technological breakthroughs in manufacturing processes that reduce production costs and enhance customization capabilities are further fueling market growth. The increasing focus on vehicle safety and driver comfort, leading to higher adoption of advanced glass features like acoustic insulation and UV protection, also acts as a significant growth accelerator.

Key Players Shaping the Automotive Glass for Light Commercial Car Market

- AGC Ltd.

- Saint-Gobain

- Fuyao Glass Industry Group Co., Ltd.

- NSG Group

Notable Milestones in Automotive Glass for Light Commercial Car Sector

- 2021: Launch of advanced acoustic glass solutions for enhanced cabin quietness in LCCs by major manufacturers.

- 2022: Increased R&D investment in laminated glass with integrated sensor technology for ADAS.

- 2023: Introduction of lightweight glass composites for electric LCCs to improve energy efficiency.

- 2024: Strategic collaborations between glass suppliers and LCC manufacturers for next-generation EV models.

In-Depth Automotive Glass for Light Commercial Car Market Outlook

The automotive glass for light commercial car market is set for sustained and robust growth, driven by an amalgamation of technological advancements, evolving consumer preferences, and expanding industrial applications. The relentless surge in e-commerce and the resultant demand for efficient delivery fleets will continue to be a cornerstone of market expansion. Innovations in lightweight, impact-resistant glass, coupled with the integration of smart technologies for enhanced safety and driver assistance, will redefine product offerings. The transition towards electric LCCs presents a significant opportunity for specialized glass solutions that contribute to energy efficiency and thermal management. Strategic partnerships and a focus on emerging markets will further catalyze long-term growth, solidifying the automotive glass sector's vital role in the evolving landscape of light commercial mobility.

Automotive Glass for Light Commercial Car Segmentation

-

1. Application

- 1.1. Original Equipment Manufacturer (OEM)

- 1.2. Aftermarket Replacement (ARG)

-

2. Types

- 2.1. Tempered

- 2.2. Laminated

- 2.3. Others

Automotive Glass for Light Commercial Car Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Glass for Light Commercial Car REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Automotive Glass for Light Commercial Car Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Original Equipment Manufacturer (OEM)

- 5.1.2. Aftermarket Replacement (ARG)

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Tempered

- 5.2.2. Laminated

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Automotive Glass for Light Commercial Car Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Original Equipment Manufacturer (OEM)

- 6.1.2. Aftermarket Replacement (ARG)

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Tempered

- 6.2.2. Laminated

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Automotive Glass for Light Commercial Car Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Original Equipment Manufacturer (OEM)

- 7.1.2. Aftermarket Replacement (ARG)

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Tempered

- 7.2.2. Laminated

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Automotive Glass for Light Commercial Car Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Original Equipment Manufacturer (OEM)

- 8.1.2. Aftermarket Replacement (ARG)

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Tempered

- 8.2.2. Laminated

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Automotive Glass for Light Commercial Car Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Original Equipment Manufacturer (OEM)

- 9.1.2. Aftermarket Replacement (ARG)

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Tempered

- 9.2.2. Laminated

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Automotive Glass for Light Commercial Car Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Original Equipment Manufacturer (OEM)

- 10.1.2. Aftermarket Replacement (ARG)

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Tempered

- 10.2.2. Laminated

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 AGC Ltd.

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Saint-Gobain

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Fuyao Glass Industry Group Co.

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Ltd.

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 NSG Group

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.1 AGC Ltd.

List of Figures

- Figure 1: Global Automotive Glass for Light Commercial Car Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Automotive Glass for Light Commercial Car Revenue (million), by Application 2024 & 2032

- Figure 3: North America Automotive Glass for Light Commercial Car Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Automotive Glass for Light Commercial Car Revenue (million), by Types 2024 & 2032

- Figure 5: North America Automotive Glass for Light Commercial Car Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Automotive Glass for Light Commercial Car Revenue (million), by Country 2024 & 2032

- Figure 7: North America Automotive Glass for Light Commercial Car Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Automotive Glass for Light Commercial Car Revenue (million), by Application 2024 & 2032

- Figure 9: South America Automotive Glass for Light Commercial Car Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Automotive Glass for Light Commercial Car Revenue (million), by Types 2024 & 2032

- Figure 11: South America Automotive Glass for Light Commercial Car Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Automotive Glass for Light Commercial Car Revenue (million), by Country 2024 & 2032

- Figure 13: South America Automotive Glass for Light Commercial Car Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Automotive Glass for Light Commercial Car Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Automotive Glass for Light Commercial Car Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Automotive Glass for Light Commercial Car Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Automotive Glass for Light Commercial Car Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Automotive Glass for Light Commercial Car Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Automotive Glass for Light Commercial Car Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Automotive Glass for Light Commercial Car Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Automotive Glass for Light Commercial Car Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Automotive Glass for Light Commercial Car Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Automotive Glass for Light Commercial Car Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Automotive Glass for Light Commercial Car Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Automotive Glass for Light Commercial Car Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Automotive Glass for Light Commercial Car Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Automotive Glass for Light Commercial Car Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Automotive Glass for Light Commercial Car Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Automotive Glass for Light Commercial Car Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Automotive Glass for Light Commercial Car Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Automotive Glass for Light Commercial Car Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Automotive Glass for Light Commercial Car Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Automotive Glass for Light Commercial Car Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Automotive Glass for Light Commercial Car Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Automotive Glass for Light Commercial Car Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Automotive Glass for Light Commercial Car Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Automotive Glass for Light Commercial Car Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Automotive Glass for Light Commercial Car Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Automotive Glass for Light Commercial Car Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Automotive Glass for Light Commercial Car Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Automotive Glass for Light Commercial Car Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Automotive Glass for Light Commercial Car Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Automotive Glass for Light Commercial Car Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Automotive Glass for Light Commercial Car Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Automotive Glass for Light Commercial Car Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Automotive Glass for Light Commercial Car Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Automotive Glass for Light Commercial Car Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Automotive Glass for Light Commercial Car Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Automotive Glass for Light Commercial Car Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Automotive Glass for Light Commercial Car Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Automotive Glass for Light Commercial Car Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Automotive Glass for Light Commercial Car Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Automotive Glass for Light Commercial Car Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Automotive Glass for Light Commercial Car Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Automotive Glass for Light Commercial Car Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Automotive Glass for Light Commercial Car Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Automotive Glass for Light Commercial Car Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Automotive Glass for Light Commercial Car Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Automotive Glass for Light Commercial Car Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Automotive Glass for Light Commercial Car Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Automotive Glass for Light Commercial Car Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Automotive Glass for Light Commercial Car Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Automotive Glass for Light Commercial Car Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Automotive Glass for Light Commercial Car Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Automotive Glass for Light Commercial Car Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Automotive Glass for Light Commercial Car Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Automotive Glass for Light Commercial Car Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Automotive Glass for Light Commercial Car Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Automotive Glass for Light Commercial Car Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Automotive Glass for Light Commercial Car Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Automotive Glass for Light Commercial Car Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Automotive Glass for Light Commercial Car Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Automotive Glass for Light Commercial Car Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Automotive Glass for Light Commercial Car Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Automotive Glass for Light Commercial Car Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Automotive Glass for Light Commercial Car Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Automotive Glass for Light Commercial Car Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Automotive Glass for Light Commercial Car Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Glass for Light Commercial Car?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Automotive Glass for Light Commercial Car?

Key companies in the market include AGC Ltd., Saint-Gobain, Fuyao Glass Industry Group Co., Ltd., NSG Group.

3. What are the main segments of the Automotive Glass for Light Commercial Car?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Glass for Light Commercial Car," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Glass for Light Commercial Car report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Glass for Light Commercial Car?

To stay informed about further developments, trends, and reports in the Automotive Glass for Light Commercial Car, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence