Key Insights

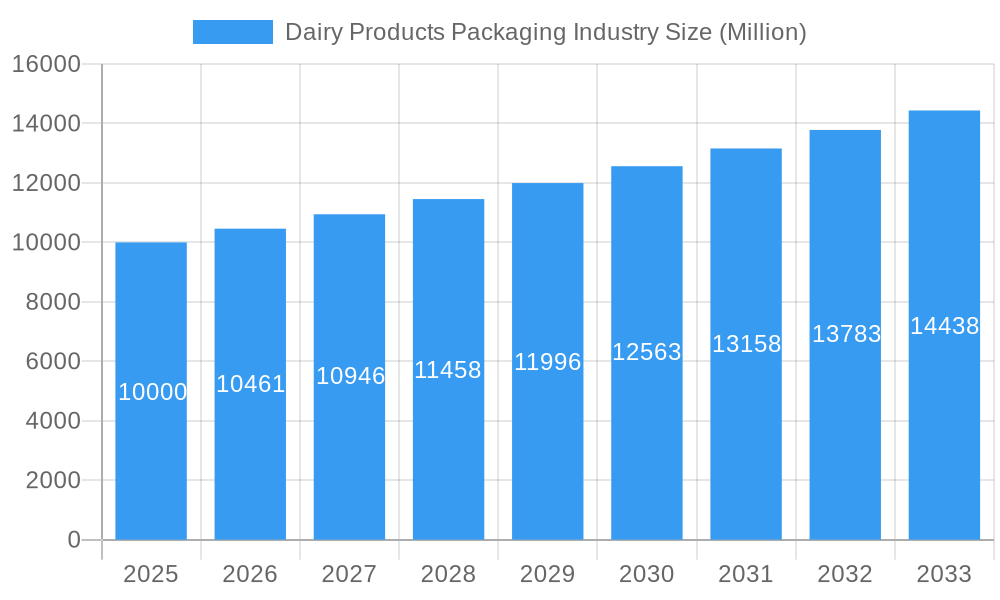

The dairy products packaging market, currently valued at approximately $XX billion (estimated based on provided CAGR and market trends), is experiencing steady growth, projected at a compound annual growth rate (CAGR) of 4.61% from 2025 to 2033. This expansion is driven by several key factors. Increasing consumer demand for convenient and shelf-stable dairy products fuels the need for innovative packaging solutions. The rising popularity of single-serve and on-the-go options, coupled with the growing awareness of sustainability, is pushing the adoption of eco-friendly materials like recycled paperboard and plant-based plastics. Furthermore, technological advancements in packaging design and material science are enabling better preservation, extended shelf life, and enhanced product protection. Significant growth is expected in regions like Asia-Pacific, fueled by rising disposable incomes and changing dietary habits. However, fluctuating raw material prices and increasing regulatory scrutiny on packaging waste pose significant challenges. The market is segmented by material (plastic, paper and paperboard, glass, metal), product type (milk, cheese, frozen foods, yogurt, cultured products), and package type (bottles, pouches, cartons and boxes, bags and wraps). Key players in this competitive landscape include Consolidated Container Company LLC, Stora Enso Oyj, Ball Corporation, and others, constantly striving for innovation and sustainability to maintain market share.

Dairy Products Packaging Industry Market Size (In Billion)

The market segmentation offers lucrative opportunities for specialized packaging solutions. For instance, the demand for flexible pouches for yogurt and cultured products is expected to surge due to their portability and cost-effectiveness. Similarly, the increasing focus on sustainable practices is creating a significant opportunity for companies offering eco-friendly packaging options made from recycled and renewable materials. The growth in the frozen food segment within the dairy industry is also driving demand for specialized packaging that maintains product quality during freezing and thawing. Regional variations in consumer preferences and regulatory landscapes present both challenges and opportunities for companies operating in this dynamic market. Companies that can effectively adapt to these trends, innovate in packaging technology, and prioritize sustainability will be best positioned for success in the coming years.

Dairy Products Packaging Industry Company Market Share

Dairy Products Packaging Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the Dairy Products Packaging market, encompassing market dynamics, growth trends, regional dominance, product landscape, key challenges and opportunities, and key players. The study period covers 2019-2033, with a base year of 2025 and a forecast period of 2025-2033. The report offers invaluable insights for industry professionals, investors, and stakeholders seeking to understand and capitalize on the evolving dynamics of this crucial sector. Market values are presented in Million units.

Dairy Products Packaging Industry Market Dynamics & Structure

The dairy products packaging market is characterized by moderate concentration, with key players vying for market share through innovation and strategic acquisitions. Technological advancements, driven by sustainability concerns and consumer demand for convenience, are reshaping the landscape. Stringent regulatory frameworks regarding material safety and recyclability present both challenges and opportunities. Competition from alternative packaging materials influences market dynamics, while the growing demand for dairy products, particularly in emerging economies, fuels market expansion. The market size in 2025 is estimated at xx Million units.

- Market Concentration: Moderately concentrated, with the top 10 players holding an estimated xx% market share in 2025.

- Technological Innovation: Focus on sustainable materials (e.g., recycled plastics, plant-based alternatives), lightweight packaging, and improved barrier properties.

- Regulatory Framework: Stringent regulations on food safety and environmental impact drive innovation and necessitate compliance.

- Competitive Substitutes: Alternative packaging materials like biodegradable plastics and compostable films pose a competitive threat.

- End-User Demographics: Growing demand from health-conscious consumers and expanding global populations drive market growth.

- M&A Trends: Strategic acquisitions and partnerships are prevalent, particularly among companies focused on sustainable packaging solutions. The number of M&A deals in 2024 was xx.

Dairy Products Packaging Industry Growth Trends & Insights

The dairy products packaging market exhibits steady growth, fueled by rising dairy consumption and the increasing demand for convenient, shelf-stable packaging. Technological disruptions, such as the adoption of advanced barrier films and sustainable materials, are driving innovation and market expansion. Consumer preference shifts towards eco-friendly and functional packaging contribute to the market's evolution. The market is projected to witness a CAGR of xx% during the forecast period (2025-2033). Market penetration of sustainable packaging solutions is increasing at a rate of xx% annually. Specific market segments, like those catering to yogurt and cultured products, display faster growth rates. Analysis of consumer behavior reveals a strong preference for recyclable and compostable packaging. The increasing adoption of e-commerce and home delivery further drives the demand for robust and tamper-evident packaging.

Dominant Regions, Countries, or Segments in Dairy Products Packaging Industry

North America and Europe currently dominate the dairy products packaging market, driven by high dairy consumption, established infrastructure, and stringent environmental regulations. However, Asia-Pacific is witnessing the fastest growth due to rapid urbanization, increasing disposable incomes, and rising dairy consumption. Within the product segment, milk and yogurt packaging represent the largest market share. Plastic remains the dominant packaging material due to its versatility and cost-effectiveness, while the demand for sustainable alternatives like paper and paperboard is rapidly increasing.

- Leading Region: North America

- Fastest-Growing Region: Asia-Pacific

- Dominant Material Segment: Plastic (xx Million units in 2025)

- Largest Product Segment: Milk (xx Million units in 2025)

- Key Drivers: Rising disposable incomes, expanding population, increased preference for convenience, and stringent environmental regulations.

Dairy Products Packaging Industry Product Landscape

The dairy products packaging industry showcases a diverse range of products designed to meet specific needs, from shelf-stable cartons and pouches to lightweight bottles and innovative barrier films. Technological advancements focus on extending shelf life, enhancing product protection, and optimizing sustainability. Unique selling propositions include enhanced barrier properties, improved recyclability, and reduced environmental impact. For example, the use of recycled content is increasing in packaging solutions.

Key Drivers, Barriers & Challenges in Dairy Products Packaging Industry

Key Drivers:

- Growing demand for dairy products globally.

- Increasing preference for convenient and shelf-stable packaging.

- Technological advancements in materials and packaging design.

- Stringent environmental regulations promoting sustainable packaging solutions.

Key Challenges:

- Fluctuations in raw material prices.

- Stringent regulations related to food safety and environmental compliance.

- Competition from alternative packaging materials.

- Supply chain disruptions affecting the timely delivery of raw materials and packaging solutions. Estimated impact on market growth in 2024: xx%.

Emerging Opportunities in Dairy Products Packaging Industry

- Growing demand for sustainable and eco-friendly packaging options.

- Increased focus on lightweighting and reducing packaging material usage.

- Expansion into emerging markets with high growth potential.

- Development of innovative packaging solutions with enhanced functionalities like smart packaging and tamper-evidence features.

Growth Accelerators in the Dairy Products Packaging Industry Industry

Technological breakthroughs in barrier film technology, the increased adoption of recycled materials, and strategic partnerships fostering innovation are key catalysts driving long-term growth in the dairy products packaging industry. Furthermore, market expansion into developing economies and the rising popularity of e-commerce present significant opportunities.

Key Players Shaping the Dairy Products Packaging Industry Market

Notable Milestones in Dairy Products Packaging Industry Sector

- May 2021: Stora Enso partnered with Pulpex to produce fiber-based bottles, offering a sustainable alternative to plastic.

- August 2021: Huhtamaki acquired Elif Holding A.S., expanding its presence in emerging markets.

- September 2021: Greiner Packaging introduced chemically recycled polypropylene into its packaging, showcasing commitment to sustainability.

In-Depth Dairy Products Packaging Industry Market Outlook

The dairy products packaging market is poised for significant growth driven by continued innovation in sustainable materials and packaging designs. Strategic partnerships, focused on developing eco-friendly solutions, will shape the industry’s future. Expansion into new markets and the rising adoption of e-commerce will further propel market expansion, creating lucrative opportunities for both established and emerging players.

Dairy Products Packaging Industry Segmentation

-

1. Material

- 1.1. Plastic

- 1.2. Paper and Paperboard

- 1.3. Glass

- 1.4. Metal

-

2. Product

- 2.1. Milk

- 2.2. Cheese

- 2.3. Frozen Foods

- 2.4. Yogurt

- 2.5. Cultured Products

-

3. Package Type

- 3.1. Bottles

- 3.2. Pouches

- 3.3. Cartons and Boxes

- 3.4. Bags and Wraps

- 3.5. Other Package Types

Dairy Products Packaging Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Dairy Products Packaging Industry Regional Market Share

Geographic Coverage of Dairy Products Packaging Industry

Dairy Products Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Consumer Preference Towards Protein-based Products; Increasing Adoption of Packages Incorporating Small Portion Size

- 3.3. Market Restrains

- 3.3.1. ; Greenhouse Gas Emission due to Dairy Activities Leading to Legislative Issues

- 3.4. Market Trends

- 3.4.1. Milk Occupies the Largest Market Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Dairy Products Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Material

- 5.1.1. Plastic

- 5.1.2. Paper and Paperboard

- 5.1.3. Glass

- 5.1.4. Metal

- 5.2. Market Analysis, Insights and Forecast - by Product

- 5.2.1. Milk

- 5.2.2. Cheese

- 5.2.3. Frozen Foods

- 5.2.4. Yogurt

- 5.2.5. Cultured Products

- 5.3. Market Analysis, Insights and Forecast - by Package Type

- 5.3.1. Bottles

- 5.3.2. Pouches

- 5.3.3. Cartons and Boxes

- 5.3.4. Bags and Wraps

- 5.3.5. Other Package Types

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Latin America

- 5.4.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Material

- 6. North America Dairy Products Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Material

- 6.1.1. Plastic

- 6.1.2. Paper and Paperboard

- 6.1.3. Glass

- 6.1.4. Metal

- 6.2. Market Analysis, Insights and Forecast - by Product

- 6.2.1. Milk

- 6.2.2. Cheese

- 6.2.3. Frozen Foods

- 6.2.4. Yogurt

- 6.2.5. Cultured Products

- 6.3. Market Analysis, Insights and Forecast - by Package Type

- 6.3.1. Bottles

- 6.3.2. Pouches

- 6.3.3. Cartons and Boxes

- 6.3.4. Bags and Wraps

- 6.3.5. Other Package Types

- 6.1. Market Analysis, Insights and Forecast - by Material

- 7. Europe Dairy Products Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Material

- 7.1.1. Plastic

- 7.1.2. Paper and Paperboard

- 7.1.3. Glass

- 7.1.4. Metal

- 7.2. Market Analysis, Insights and Forecast - by Product

- 7.2.1. Milk

- 7.2.2. Cheese

- 7.2.3. Frozen Foods

- 7.2.4. Yogurt

- 7.2.5. Cultured Products

- 7.3. Market Analysis, Insights and Forecast - by Package Type

- 7.3.1. Bottles

- 7.3.2. Pouches

- 7.3.3. Cartons and Boxes

- 7.3.4. Bags and Wraps

- 7.3.5. Other Package Types

- 7.1. Market Analysis, Insights and Forecast - by Material

- 8. Asia Pacific Dairy Products Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Material

- 8.1.1. Plastic

- 8.1.2. Paper and Paperboard

- 8.1.3. Glass

- 8.1.4. Metal

- 8.2. Market Analysis, Insights and Forecast - by Product

- 8.2.1. Milk

- 8.2.2. Cheese

- 8.2.3. Frozen Foods

- 8.2.4. Yogurt

- 8.2.5. Cultured Products

- 8.3. Market Analysis, Insights and Forecast - by Package Type

- 8.3.1. Bottles

- 8.3.2. Pouches

- 8.3.3. Cartons and Boxes

- 8.3.4. Bags and Wraps

- 8.3.5. Other Package Types

- 8.1. Market Analysis, Insights and Forecast - by Material

- 9. Latin America Dairy Products Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Material

- 9.1.1. Plastic

- 9.1.2. Paper and Paperboard

- 9.1.3. Glass

- 9.1.4. Metal

- 9.2. Market Analysis, Insights and Forecast - by Product

- 9.2.1. Milk

- 9.2.2. Cheese

- 9.2.3. Frozen Foods

- 9.2.4. Yogurt

- 9.2.5. Cultured Products

- 9.3. Market Analysis, Insights and Forecast - by Package Type

- 9.3.1. Bottles

- 9.3.2. Pouches

- 9.3.3. Cartons and Boxes

- 9.3.4. Bags and Wraps

- 9.3.5. Other Package Types

- 9.1. Market Analysis, Insights and Forecast - by Material

- 10. Middle East and Africa Dairy Products Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Material

- 10.1.1. Plastic

- 10.1.2. Paper and Paperboard

- 10.1.3. Glass

- 10.1.4. Metal

- 10.2. Market Analysis, Insights and Forecast - by Product

- 10.2.1. Milk

- 10.2.2. Cheese

- 10.2.3. Frozen Foods

- 10.2.4. Yogurt

- 10.2.5. Cultured Products

- 10.3. Market Analysis, Insights and Forecast - by Package Type

- 10.3.1. Bottles

- 10.3.2. Pouches

- 10.3.3. Cartons and Boxes

- 10.3.4. Bags and Wraps

- 10.3.5. Other Package Types

- 10.1. Market Analysis, Insights and Forecast - by Material

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Consolidated Container Company LLC

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Stora Enso Oyj

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Ball Corporation

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Greiner Packaging international Gmb

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Berry Global Group Inc

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Huhtamaki Group

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Winpak Ltd

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Amcor PLC

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 International Paper Company

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Sealed Air Corporation

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Saudi Basic Industries Corporation

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Consolidated Container Company LLC

List of Figures

- Figure 1: Global Dairy Products Packaging Industry Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Dairy Products Packaging Industry Revenue (undefined), by Material 2025 & 2033

- Figure 3: North America Dairy Products Packaging Industry Revenue Share (%), by Material 2025 & 2033

- Figure 4: North America Dairy Products Packaging Industry Revenue (undefined), by Product 2025 & 2033

- Figure 5: North America Dairy Products Packaging Industry Revenue Share (%), by Product 2025 & 2033

- Figure 6: North America Dairy Products Packaging Industry Revenue (undefined), by Package Type 2025 & 2033

- Figure 7: North America Dairy Products Packaging Industry Revenue Share (%), by Package Type 2025 & 2033

- Figure 8: North America Dairy Products Packaging Industry Revenue (undefined), by Country 2025 & 2033

- Figure 9: North America Dairy Products Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Dairy Products Packaging Industry Revenue (undefined), by Material 2025 & 2033

- Figure 11: Europe Dairy Products Packaging Industry Revenue Share (%), by Material 2025 & 2033

- Figure 12: Europe Dairy Products Packaging Industry Revenue (undefined), by Product 2025 & 2033

- Figure 13: Europe Dairy Products Packaging Industry Revenue Share (%), by Product 2025 & 2033

- Figure 14: Europe Dairy Products Packaging Industry Revenue (undefined), by Package Type 2025 & 2033

- Figure 15: Europe Dairy Products Packaging Industry Revenue Share (%), by Package Type 2025 & 2033

- Figure 16: Europe Dairy Products Packaging Industry Revenue (undefined), by Country 2025 & 2033

- Figure 17: Europe Dairy Products Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Dairy Products Packaging Industry Revenue (undefined), by Material 2025 & 2033

- Figure 19: Asia Pacific Dairy Products Packaging Industry Revenue Share (%), by Material 2025 & 2033

- Figure 20: Asia Pacific Dairy Products Packaging Industry Revenue (undefined), by Product 2025 & 2033

- Figure 21: Asia Pacific Dairy Products Packaging Industry Revenue Share (%), by Product 2025 & 2033

- Figure 22: Asia Pacific Dairy Products Packaging Industry Revenue (undefined), by Package Type 2025 & 2033

- Figure 23: Asia Pacific Dairy Products Packaging Industry Revenue Share (%), by Package Type 2025 & 2033

- Figure 24: Asia Pacific Dairy Products Packaging Industry Revenue (undefined), by Country 2025 & 2033

- Figure 25: Asia Pacific Dairy Products Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Latin America Dairy Products Packaging Industry Revenue (undefined), by Material 2025 & 2033

- Figure 27: Latin America Dairy Products Packaging Industry Revenue Share (%), by Material 2025 & 2033

- Figure 28: Latin America Dairy Products Packaging Industry Revenue (undefined), by Product 2025 & 2033

- Figure 29: Latin America Dairy Products Packaging Industry Revenue Share (%), by Product 2025 & 2033

- Figure 30: Latin America Dairy Products Packaging Industry Revenue (undefined), by Package Type 2025 & 2033

- Figure 31: Latin America Dairy Products Packaging Industry Revenue Share (%), by Package Type 2025 & 2033

- Figure 32: Latin America Dairy Products Packaging Industry Revenue (undefined), by Country 2025 & 2033

- Figure 33: Latin America Dairy Products Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Middle East and Africa Dairy Products Packaging Industry Revenue (undefined), by Material 2025 & 2033

- Figure 35: Middle East and Africa Dairy Products Packaging Industry Revenue Share (%), by Material 2025 & 2033

- Figure 36: Middle East and Africa Dairy Products Packaging Industry Revenue (undefined), by Product 2025 & 2033

- Figure 37: Middle East and Africa Dairy Products Packaging Industry Revenue Share (%), by Product 2025 & 2033

- Figure 38: Middle East and Africa Dairy Products Packaging Industry Revenue (undefined), by Package Type 2025 & 2033

- Figure 39: Middle East and Africa Dairy Products Packaging Industry Revenue Share (%), by Package Type 2025 & 2033

- Figure 40: Middle East and Africa Dairy Products Packaging Industry Revenue (undefined), by Country 2025 & 2033

- Figure 41: Middle East and Africa Dairy Products Packaging Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Material 2020 & 2033

- Table 2: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Product 2020 & 2033

- Table 3: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Package Type 2020 & 2033

- Table 4: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Region 2020 & 2033

- Table 5: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Material 2020 & 2033

- Table 6: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Product 2020 & 2033

- Table 7: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Package Type 2020 & 2033

- Table 8: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 9: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Material 2020 & 2033

- Table 10: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Product 2020 & 2033

- Table 11: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Package Type 2020 & 2033

- Table 12: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Material 2020 & 2033

- Table 14: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Product 2020 & 2033

- Table 15: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Package Type 2020 & 2033

- Table 16: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 17: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Material 2020 & 2033

- Table 18: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Product 2020 & 2033

- Table 19: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Package Type 2020 & 2033

- Table 20: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 21: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Material 2020 & 2033

- Table 22: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Product 2020 & 2033

- Table 23: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Package Type 2020 & 2033

- Table 24: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Dairy Products Packaging Industry?

The projected CAGR is approximately 4.3%.

2. Which companies are prominent players in the Dairy Products Packaging Industry?

Key companies in the market include Consolidated Container Company LLC, Stora Enso Oyj, Ball Corporation, Greiner Packaging international Gmb, Berry Global Group Inc, Huhtamaki Group, Winpak Ltd, Amcor PLC, International Paper Company, Sealed Air Corporation, Saudi Basic Industries Corporation.

3. What are the main segments of the Dairy Products Packaging Industry?

The market segments include Material, Product, Package Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

Increasing Consumer Preference Towards Protein-based Products; Increasing Adoption of Packages Incorporating Small Portion Size.

6. What are the notable trends driving market growth?

Milk Occupies the Largest Market Share.

7. Are there any restraints impacting market growth?

; Greenhouse Gas Emission due to Dairy Activities Leading to Legislative Issues.

8. Can you provide examples of recent developments in the market?

September 2021 - Greiner Packaging announced Emmi CAFFÈ LATTE, Europe's leading ready-to-drink iced coffee brand, will start incorporating its new chemically recycled polypropylene into packaging. Greiner Packaging makes these cups from chemically recycled material that comes from Borealis.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Dairy Products Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Dairy Products Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Dairy Products Packaging Industry?

To stay informed about further developments, trends, and reports in the Dairy Products Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence