Key Insights

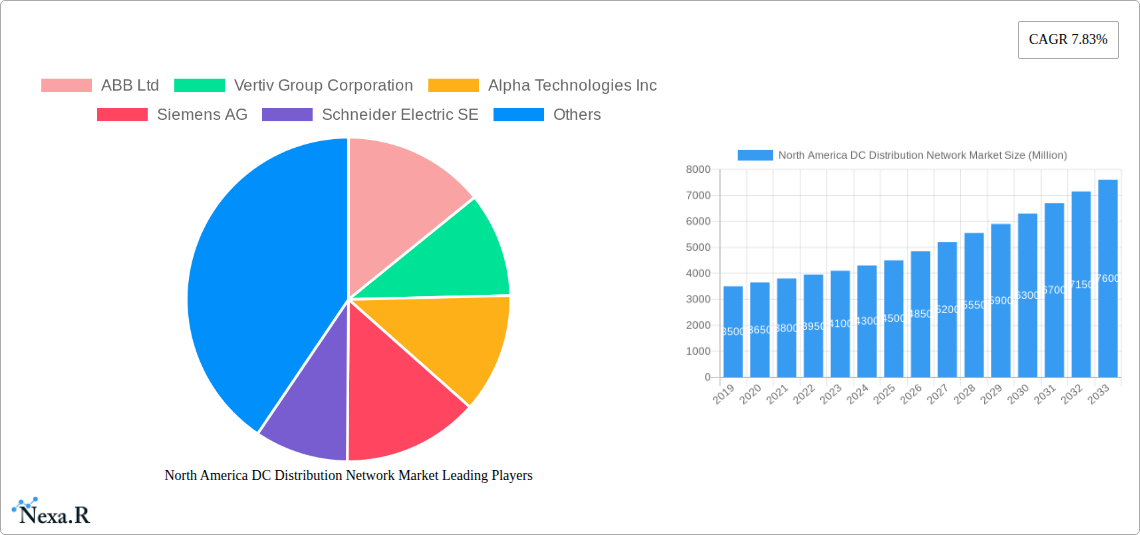

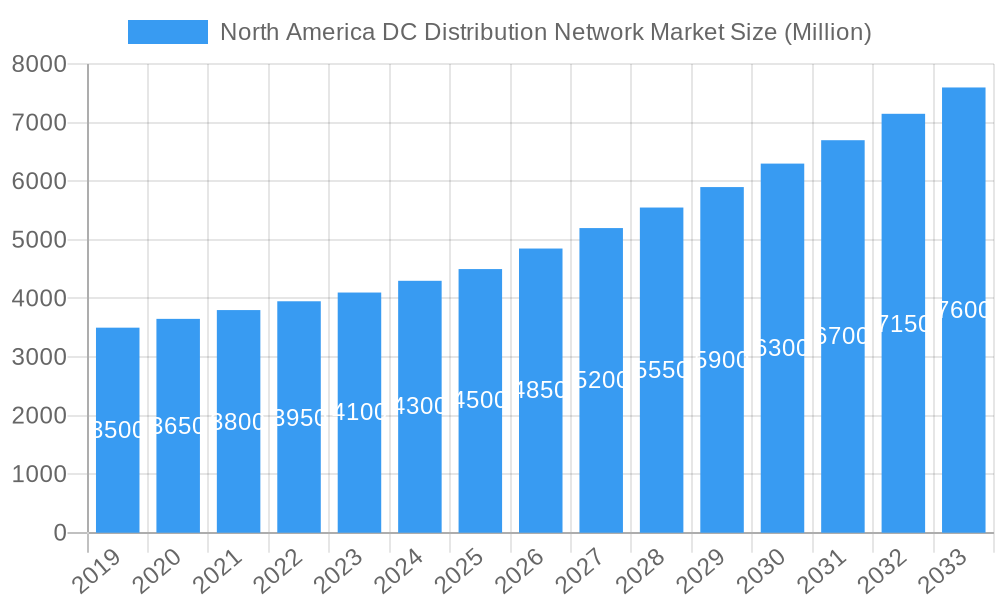

The North America DC Distribution Network Market is projected for significant expansion, reaching an estimated $9861.04 million by 2025, with a Compound Annual Growth Rate (CAGR) of 7.83% through 2033. This growth is propelled by the increasing integration of renewable energy and the demand for energy-efficient solutions. Key drivers include the need for reliable power in a digitized world, expanding data center infrastructure, and the rise of electric vehicles (EVs) requiring advanced DC charging. The evolution towards smart grids and distributed energy resources further bolsters DC distribution networks, offering superior efficiency and power quality over AC systems. The market segments, including High Voltage and Low & Medium Voltage, both show strong growth for applications ranging from industrial sites to residential EV charging.

North America DC Distribution Network Market Market Size (In Billion)

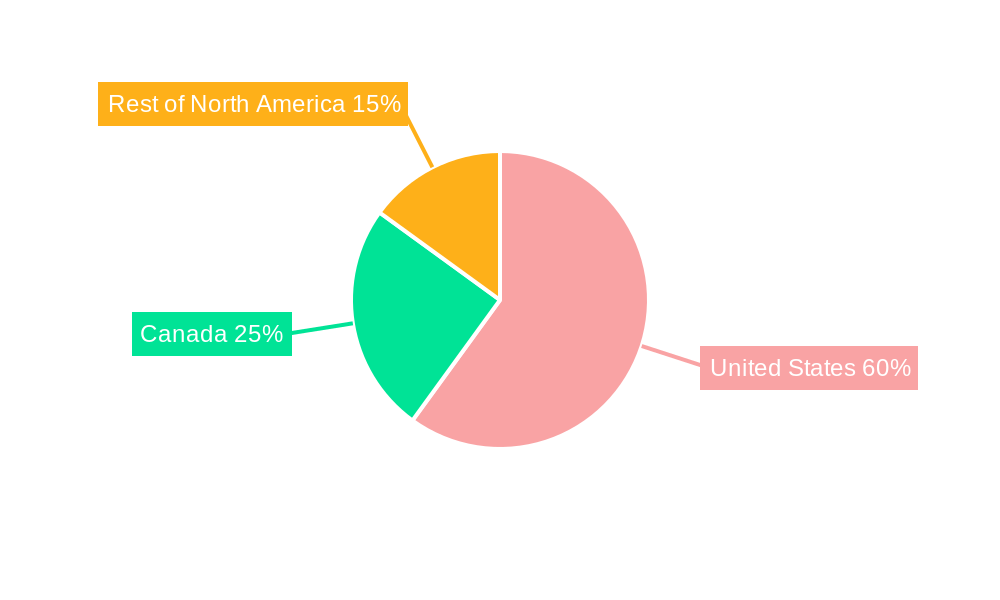

Market dynamics are shaped by emerging trends like microgrids, advanced DC-DC converters, and integrated energy storage systems, which enhance grid resilience and energy management. Restraints include substantial initial investment for DC infrastructure and the need for standardized regulations. However, the inherent efficiency and reduced carbon footprint of DC distribution are expected to overcome these hurdles. Leading companies such as Siemens AG, Schneider Electric SE, and Eaton Corporation Plc are investing in R&D to drive innovation. Geographically, the United States leads the market, with Canada and the Rest of North America also demonstrating considerable growth, supported by favorable government policies and a robust industrial sector.

North America DC Distribution Network Market Company Market Share

North America DC Distribution Network Market Report Description

Unlock the future of power distribution with our comprehensive report on the North America DC Distribution Network Market. This in-depth analysis delves into the rapidly evolving landscape of Direct Current (DC) power infrastructure across the United States, Canada, and the Rest of North America. Covering a meticulous study period from 2019 to 2033, with a base and estimated year of 2025, this report provides unparalleled insights into market dynamics, growth trends, and key player strategies.

The North America DC Distribution Network Market is witnessing a transformative surge driven by the increasing electrification of transportation, the growing adoption of renewable energy sources, and the demand for more efficient and reliable power solutions in data centers and industrial applications. This report is essential for DC distribution network providers, EV charging infrastructure developers, renewable energy integrators, smart grid technology manufacturers, utilities, and investors seeking to capitalize on this burgeoning market.

Our analysis meticulously segments the market by Voltage (High Voltage, Low and Medium Voltage) and End User (Residential, Commercial and Industrial), offering granular insights into segment-specific growth trajectories and adoption rates. We also explore the geographical nuances of the United States, Canada, and the Rest of North America, identifying regional strengths and untapped potential for DC distribution network deployment.

Key companies shaping this market include: ABB Ltd, Vertiv Group Corporation, Alpha Technologies Inc, Siemens AG, Schneider Electric SE, Robert Bosch GmbH, Secheron SA, Eaton Corporation Plc, Nextek Power Systems Inc, among others.

Report Highlights:

- Market Size and Forecast: Detailed market size estimations in million units for the base year 2025 and comprehensive forecasts for the period 2025–2033.

- Historical Analysis: In-depth review of market performance from 2019–2024.

- Segmentation Analysis: Granular breakdown of market trends by Voltage and End User segments.

- Geographical Insights: Focused analysis on the United States, Canada, and the Rest of North America.

- Industry Developments: Critical evaluation of key industry events and their impact on market trajectory.

- Competitive Landscape: Analysis of leading players and their strategic initiatives.

- Key Drivers, Barriers, and Opportunities: Comprehensive understanding of the forces shaping market growth and potential roadblocks.

Invest in actionable intelligence to navigate the complexities and seize the immense opportunities within the North America DC Distribution Network Market.

North America DC Distribution Network Market Market Dynamics & Structure

The North America DC Distribution Network Market is characterized by a moderate to high market concentration, with key players like ABB Ltd, Vertiv Group Corporation, Siemens AG, and Schneider Electric SE holding significant market share due to their established product portfolios and extensive R&D investments. Technological innovation is a primary driver, fueled by the relentless pursuit of higher efficiency, reduced energy losses, and enhanced grid stability. The advent of advanced power electronics, smart grid technologies, and integrated energy management systems is accelerating the adoption of DC distribution networks, especially in high-growth sectors like electric vehicle (EV) charging infrastructure and data centers. Regulatory frameworks are evolving to support the integration of DC systems, with government incentives and standards promoting cleaner energy solutions and grid modernization. Competitive product substitutes, such as advanced AC distribution technologies, remain a factor, but the inherent efficiency benefits of DC systems are increasingly offsetting these concerns for specific applications. End-user demographics are shifting towards a greater demand for reliable, scalable, and energy-efficient power solutions, particularly from industrial and commercial sectors aiming to reduce operational costs and carbon footprints. Mergers and acquisitions (M&A) trends are observed as companies seek to expand their technological capabilities, geographic reach, and product offerings within the DC ecosystem. For instance, acquisitions of specialized DC component manufacturers or software providers are common strategies.

- Market Concentration: Dominated by a few major players with specialized expertise and significant R&D capabilities.

- Technological Innovation Drivers: Focus on efficiency improvements, integration with renewables, and advanced control systems.

- Regulatory Frameworks: Supportive policies for electrification, EV charging infrastructure, and grid modernization are crucial.

- Competitive Product Substitutes: Advanced AC solutions, though DC offers distinct advantages in certain applications.

- End-User Demographics: Growing demand from data centers, EV charging networks, and industrial facilities seeking energy efficiency.

- M&A Trends: Strategic acquisitions to consolidate market position and acquire new technologies.

North America DC Distribution Network Market Growth Trends & Insights

The North America DC Distribution Network Market is projected for robust growth, driven by a confluence of technological advancements, evolving energy policies, and shifting consumer behavior. The market size is expected to witness a significant expansion from an estimated value of USD XXXX million units in 2025 to USD YYYY million units by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately XX% during the forecast period. This upward trajectory is underpinned by the increasing demand for reliable and efficient power delivery solutions, particularly in segments like electric vehicle (EV) charging infrastructure, data centers, and renewable energy integration. The adoption rates for DC distribution networks are steadily increasing as their inherent advantages – such as higher efficiency, reduced conversion losses, and simplified integration with DC sources like solar PV and battery storage – become more apparent.

Technological disruptions are playing a pivotal role. Innovations in high-power semiconductor devices, advanced grid control software, and modular DC power architectures are enhancing the performance, scalability, and cost-effectiveness of these systems. The development of compact and intelligent DC-DC converters and inverters is crucial for optimizing power flow and reducing installation footprints. Furthermore, the growing emphasis on smart grids and distributed energy resources (DERs) positions DC distribution networks as a natural fit for managing bidirectional power flow and enhancing grid resilience. Consumer behavior is also evolving; businesses are increasingly prioritizing sustainability and operational efficiency, leading to a greater willingness to invest in advanced power infrastructure. The rise of decentralized energy generation and storage further fuels the need for flexible and efficient DC distribution solutions that can seamlessly integrate these resources. For instance, the proliferation of rooftop solar installations and the growing adoption of battery energy storage systems (BESS) create a natural synergy with DC microgrids and distribution systems. The push towards decarbonization across industries is a significant catalyst, driving investments in technologies that minimize energy waste and facilitate the integration of renewable energy sources. This includes the electrification of transportation fleets and industrial processes, which inherently benefit from DC power. The North American market, with its proactive stance on climate action and technological innovation, is at the forefront of this transformation, making the DC distribution network a critical component of its future energy landscape.

Dominant Regions, Countries, or Segments in North America DC Distribution Network Market

The North America DC Distribution Network Market is significantly influenced by the economic policies, technological adoption rates, and infrastructure development within its constituent regions. The United States stands out as the dominant country driving market growth, owing to its vast industrial base, early adoption of advanced technologies, and substantial investments in electric vehicle (EV) charging infrastructure and renewable energy projects. Government initiatives, such as the Bipartisan Infrastructure Law, and significant private sector investments in energy transition are creating a fertile ground for the expansion of DC distribution networks. The country's robust demand for high-performance data centers, which heavily rely on stable and efficient DC power, further solidifies its leading position.

Within the segmentation by End User, the Commercial and Industrial segment is the primary driver of market expansion. This dominance is attributed to the significant energy consumption of these sectors and their keen interest in optimizing operational costs, enhancing power reliability, and achieving sustainability goals. Large manufacturing facilities, commercial buildings, and burgeoning data center hubs are increasingly opting for DC distribution networks to reduce energy losses, improve power quality, and facilitate the integration of on-site renewable energy generation. The Low and Medium Voltage segment within the Voltage classification also exhibits substantial growth, reflecting the widespread application of DC distribution in localized energy systems, microgrids, and EV charging stations.

- United States Dominance: Fueled by aggressive EV adoption, substantial renewable energy investments, and a large industrial and commercial sector.

- Commercial and Industrial Segment Growth: Driven by demand for energy efficiency, reliability, and sustainability in data centers, manufacturing, and large commercial spaces.

- Low and Medium Voltage Segment Expansion: Supported by the proliferation of localized DC systems, microgrids, and EV charging infrastructure.

- Key Drivers in the US: Government incentives for clean energy, corporate sustainability mandates, and the rapid growth of the EV market.

- Market Share: The United States is estimated to command over XX% of the North American DC distribution network market.

- Growth Potential: Significant untapped potential exists in upgrading aging grid infrastructure and expanding DC microgrids for critical facilities.

North America DC Distribution Network Market Product Landscape

The North America DC Distribution Network Market is characterized by a dynamic product landscape driven by continuous innovation in power electronics and system integration. Key product innovations include highly efficient DC-DC converters and inverters with advanced control algorithms, modular and scalable DC power distribution units, and integrated battery energy storage systems (BESS) designed for seamless grid interaction. Companies are focusing on developing compact, lightweight, and robust solutions for diverse applications, from large-scale industrial grids to localized EV charging hubs. Performance metrics are continually being pushed, with a focus on maximizing energy efficiency, minimizing harmonic distortion, and ensuring robust protection against grid disturbances. Unique selling propositions often revolve around enhanced reliability, reduced footprint, lower total cost of ownership, and simplified installation and maintenance. Technological advancements are also geared towards enabling bidirectional power flow, facilitating the integration of distributed energy resources, and supporting smart grid functionalities.

Key Drivers, Barriers & Challenges in North America DC Distribution Network Market

Key Drivers:

The North America DC Distribution Network Market is propelled by several significant drivers. The exponential growth of the electric vehicle (EV) sector necessitates robust and efficient DC charging infrastructure. The increasing adoption of renewable energy sources, such as solar and wind power, which inherently generate DC electricity, creates a strong demand for DC distribution networks to minimize conversion losses. Furthermore, the energy-intensive operations of data centers and the drive for enhanced energy efficiency and reliability across industrial and commercial sectors are compelling reasons for DC adoption. Government policies promoting grid modernization and decarbonization also act as powerful catalysts.

Barriers & Challenges:

Despite the strong growth drivers, the market faces several challenges. The initial high capital investment for implementing DC distribution infrastructure can be a significant barrier for some organizations. A lack of standardized regulations and interoperability issues between different DC system components can also hinder widespread adoption. The perception of DC systems as complex and requiring specialized expertise for installation and maintenance persists, although this is gradually changing. Supply chain disruptions for critical electronic components and the need for skilled labor to manage and operate these advanced systems also present ongoing challenges. Competitive pressures from established AC infrastructure and the need for substantial grid upgrades to fully leverage DC benefits are also factors to consider.

Emerging Opportunities in North America DC Distribution Network Market

Emerging opportunities in the North America DC Distribution Network Market are vast and multifaceted. The expansion of DC microgrids for critical infrastructure like hospitals, military bases, and remote communities offers significant potential for enhanced resilience and reliability. The integration of DC distribution networks with advanced battery energy storage systems presents a lucrative avenue for grid stabilization, peak shaving, and seamless renewable energy integration. Furthermore, the growing trend of electrification in various industries, including maritime and aviation, will create new demands for specialized DC power solutions. The development of smart charging solutions for electric fleets and the potential for vehicle-to-grid (V2G) technology integration will also drive innovation and market growth. The ongoing research and development into advanced materials for power electronics and novel DC switching technologies are paving the way for more cost-effective and higher-performing solutions.

Growth Accelerators in the North America DC Distribution Network Market Industry

Several key catalysts are accelerating the growth of the North America DC Distribution Network Market. Technological breakthroughs in wide-bandgap semiconductor materials, such as silicon carbide (SiC) and gallium nitride (GaN), are enabling the development of more efficient, smaller, and more robust power electronic components essential for DC systems. Strategic partnerships between technology providers, utilities, and end-users are fostering collaborative innovation and facilitating the deployment of pilot projects and large-scale implementations. Market expansion strategies, including the development of new business models that emphasize energy-as-a-service and performance-based contracts, are making DC distribution networks more accessible and attractive to a wider range of customers. The increasing focus on cybersecurity for smart grid infrastructure is also driving the integration of advanced security features into DC distribution solutions, further enhancing their appeal.

Key Players Shaping the North America DC Distribution Network Market Market

- ABB Ltd

- Vertiv Group Corporation

- Alpha Technologies Inc

- Siemens AG

- Schneider Electric SE

- Robert Bosch GmbH

- Secheron SA

- Eaton Corporation Plc

- Nextek Power Systems Inc

Notable Milestones in North America DC Distribution Network Market Sector

- January 2022: Eaton announced a USD 4.9 million award from the US Department of Energy to reduce the cost and complexity of deploying a direct-current (DC) distribution network for fast electric vehicle charging in the country. Eaton is likely to develop and demonstrate a novel, compact, and turnkey solution for DC fast-charging infrastructure that is likely to reduce costs by 65% through improvements in power conversion and grid interconnection technology, charger integration and modularity, and installation time.

- March 2022: In line with shared commitments to decarbonize, National Grid and Siemens Energy teamed up to undertake an upgrade of a National Grid substation using Siemens Energy-designed fluorinated gas-free Blue DC circuit breakers, which are made of clean air insulation and vacuum switching technology. Scheduled for commissioning in the year 2023, Siemens Energy's Blue DC circuit breakers will be installed in Massachusetts, United States, in substations that serve several Massachusetts communities. The first Siemens Energy Blue circuit breaker installation will be in the National Grid's US electricity network.

In-Depth North America DC Distribution Network Market Market Outlook

The future outlook for the North America DC Distribution Network Market is exceptionally positive, driven by an intensifying global commitment to sustainability and electrification. Continued advancements in power electronics, intelligent control systems, and energy storage integration will further solidify the advantages of DC distribution. The rapid expansion of electric vehicle charging infrastructure, coupled with the decentralization of energy generation through renewables, will create sustained demand for efficient DC power management. Strategic collaborations between key industry players and supportive government policies are expected to accelerate market penetration and drive innovation. Emerging applications in areas like smart buildings, resilient microgrids, and industrial automation will also contribute significantly to market growth. The focus will remain on developing scalable, cost-effective, and highly reliable DC solutions that can seamlessly integrate with existing and future energy ecosystems, positioning the North American market as a global leader in advanced power distribution.

North America DC Distribution Network Market Segmentation

-

1. Voltage

- 1.1. High Voltage

- 1.2. Low and Medium Voltage

-

2. End User

- 2.1. Residential

- 2.2. Commercial and Industrial

-

3. Geography

- 3.1. United States

- 3.2. Canada

- 3.3. Rest of North America

North America DC Distribution Network Market Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Rest of North America

North America DC Distribution Network Market Regional Market Share

Geographic Coverage of North America DC Distribution Network Market

North America DC Distribution Network Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.83% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. NRP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Voltage

- 5.1.1. High Voltage

- 5.1.2. Low and Medium Voltage

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Residential

- 5.2.2. Commercial and Industrial

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. United States

- 5.3.2. Canada

- 5.3.3. Rest of North America

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Rest of North America

- 5.1. Market Analysis, Insights and Forecast - by Voltage

- 6. North America DC Distribution Network Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Voltage

- 6.1.1. High Voltage

- 6.1.2. Low and Medium Voltage

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Residential

- 6.2.2. Commercial and Industrial

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. United States

- 6.3.2. Canada

- 6.3.3. Rest of North America

- 6.1. Market Analysis, Insights and Forecast - by Voltage

- 7. United States North America DC Distribution Network Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Voltage

- 7.1.1. High Voltage

- 7.1.2. Low and Medium Voltage

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. Residential

- 7.2.2. Commercial and Industrial

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. United States

- 7.3.2. Canada

- 7.3.3. Rest of North America

- 7.1. Market Analysis, Insights and Forecast - by Voltage

- 8. Canada North America DC Distribution Network Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Voltage

- 8.1.1. High Voltage

- 8.1.2. Low and Medium Voltage

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. Residential

- 8.2.2. Commercial and Industrial

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. United States

- 8.3.2. Canada

- 8.3.3. Rest of North America

- 8.1. Market Analysis, Insights and Forecast - by Voltage

- 9. Rest of North America North America DC Distribution Network Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Voltage

- 9.1.1. High Voltage

- 9.1.2. Low and Medium Voltage

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. Residential

- 9.2.2. Commercial and Industrial

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. United States

- 9.3.2. Canada

- 9.3.3. Rest of North America

- 9.1. Market Analysis, Insights and Forecast - by Voltage

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 ABB Ltd

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Vertiv Group Corporation

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 Alpha Technologies Inc

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 Siemens AG

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 Schneider Electric SE

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 Robert Bosch GmbH

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 Secheron SA

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 Eaton Corporation Plc

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 Nextek Power Systems Inc *List Not Exhaustive

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.1 ABB Ltd

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: North America DC Distribution Network Market Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: North America DC Distribution Network Market Share (%) by Company 2025

List of Tables

- Table 1: North America DC Distribution Network Market Revenue million Forecast, by Voltage 2020 & 2033

- Table 2: North America DC Distribution Network Market Revenue million Forecast, by End User 2020 & 2033

- Table 3: North America DC Distribution Network Market Revenue million Forecast, by Geography 2020 & 2033

- Table 4: North America DC Distribution Network Market Revenue million Forecast, by Region 2020 & 2033

- Table 5: North America DC Distribution Network Market Revenue million Forecast, by Voltage 2020 & 2033

- Table 6: North America DC Distribution Network Market Revenue million Forecast, by End User 2020 & 2033

- Table 7: North America DC Distribution Network Market Revenue million Forecast, by Geography 2020 & 2033

- Table 8: North America DC Distribution Network Market Revenue million Forecast, by Country 2020 & 2033

- Table 9: North America DC Distribution Network Market Revenue million Forecast, by Voltage 2020 & 2033

- Table 10: North America DC Distribution Network Market Revenue million Forecast, by End User 2020 & 2033

- Table 11: North America DC Distribution Network Market Revenue million Forecast, by Geography 2020 & 2033

- Table 12: North America DC Distribution Network Market Revenue million Forecast, by Country 2020 & 2033

- Table 13: North America DC Distribution Network Market Revenue million Forecast, by Voltage 2020 & 2033

- Table 14: North America DC Distribution Network Market Revenue million Forecast, by End User 2020 & 2033

- Table 15: North America DC Distribution Network Market Revenue million Forecast, by Geography 2020 & 2033

- Table 16: North America DC Distribution Network Market Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America DC Distribution Network Market?

The projected CAGR is approximately 7.83%.

2. Which companies are prominent players in the North America DC Distribution Network Market?

Key companies in the market include ABB Ltd, Vertiv Group Corporation, Alpha Technologies Inc, Siemens AG, Schneider Electric SE, Robert Bosch GmbH, Secheron SA, Eaton Corporation Plc, Nextek Power Systems Inc *List Not Exhaustive.

3. What are the main segments of the North America DC Distribution Network Market?

The market segments include Voltage, End User, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 9861.04 million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Integration Of Renewable Energy Generation4.; Aging Power Grids And Investments In Transmission And Distribution Infrastructure.

6. What are the notable trends driving market growth?

Low and Medium Voltage Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Lack Of Investor Confidence Due To Sociopolitical Instability In Some Countries.

8. Can you provide examples of recent developments in the market?

January 2022: Eaton announced a USD 4.9 million award from the US Department of Energy to reduce the cost and complexity of deploying a direct-current (DC) distribution network for fast electric vehicle charging in the country. Eaton is likely to develop and demonstrate a novel, compact, and turnkey solution for DC fast-charging infrastructure that is likely to reduce costs by 65% through improvements in power conversion and grid interconnection technology, charger integration and modularity, and installation time.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America DC Distribution Network Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America DC Distribution Network Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America DC Distribution Network Market?

To stay informed about further developments, trends, and reports in the North America DC Distribution Network Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence